전기 및 전자산업은 국내 최대입니다. 예를 들어 일본의 일렉트로닉스산업은 2022년 국내 생산이 전년 대비 2% 증가하여 총액 843억 4,000만 달러에 이르렀습니다. 전자 부품의 사용 증가, 5G 기술의 성장에 의한 전기 측정기 수요 증가에 의한 것입니다.

2022년 자동차산업은 수익 점유율의 25.65%를 차지해 국내 2위의 유망산업이 되었습니다. 2022년 일본 자동차산업은 전년 대비 15.15%의 성장을 이루었습니다. 이는 주로 국내 자동차 생산 대수 증가로 인한 것으로, 2022년에는 전년 대비 3.49% 증가한 941만대를 기록했습니다.

항공우주산업은 항공우주산업의 지출 증가로 CAGR은 7.69%를 나타내 매출액에서 국내에서 가장 급성장하고 있는 산업으로, 이는 예측기간 중 엔지니어링 플라스틱 수요를 견인할 것으로 예측됩니다. 일본 항공우주부품 생산 수입은 2029년까지 약 170억 달러에 달할 것으로 전망됩니다.

일본의 엔지니어링 플라스틱 시장 동향

국내 전기 및 전자기기 생산을 지원하는 정부의 시책

일본의 일렉트로닉스 산업은 부품이나 디바이스의 생산에 뛰어나고, 전고체 전지나 의료용 카메라 등의 주요 기술을 낳고 있습니다. 정부의 탈탄소화를 위한 대처와, 동산업이 자랑으로 하는 공장 자동화이나 텔레워크를 중심으로 한 일 방식 개혁을 향한 기능 개발에 의해 새로운 혁신이 기대됩니다.

미국과 중국 무역전쟁으로 인한 칩 부족에 직면해 원격 근무화에 따른 수요 증가가 2019년 국내 전자기기 생산에 영향을 주었습니다. 연속적으로 2020년 COVID-19 팬데믹 관련 혼란으로 인해 일본의 전자부품 디바이스·전자회로 제조업의 사업소수는 전년의 약 3,860에서 감소하여 약 3,790과 10년 만의 저수준이 되었습니다. 2020년 일본의 생산액은 소비자용 전자 기기가 429억 800만엔, 산업용 전자 기기가 2,556억 7,600만엔이었습니다.

일본은 2020년부터 2021년까지 전기 및 전자제품 생산 수익이 19.2% 증가했습니다. 2021년 일본 전자 산업의 총 생산액은 11조 엔에 육박했습니다. 이 산업에는 소비자 전자 장비, 산업용 전자 장비, 전자 부품 및 장치가 포함됩니다. 가전제품은 일본 경제 생산의 3분의 1을 차지합니다.

미국 대통령과 일본의 총리는 반도체 제조 능력을 강화할 것을 약속하며 일본도 혁신 부문에 투자하고 있기 때문에 예측 기간 중에 일본의 전자산업이 활성화될 가능성이 있습니다.

일본의 엔지니어링 플라스틱 산업 개요

일본의 엔지니어링 플라스틱 시장은 적당히 통합되어 있으며 상위 5개 기업에서 63.27%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 서론

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

항공우주

자동차

건축 및 건설

전기 및 전자

포장

수출입 동향

가격 동향

재활용 개요

폴리아미드(PA) 재활용 동향

폴리카보네이트(PC) 재활용 동향

폴리에틸렌 테레프탈레이트(PET) 재활용 동향

스티렌 공중합체(ABS 및 SAN) 재활용 동향

규제 프레임워크

일본

밸류체인과 유통채널 분석

제5장 시장 세분화

최종 사용자 산업

항공우주

자동차

건축 및 건설

전기 및 전자

산업 및 기계

포장

기타

수지 유형

불소수지

하위 수지 유형별

에틸렌테트라플루오로에틸렌(ETFE)

플루오르화 에틸렌-프로필렌(FEP)

폴리테트라플루오로에틸렌(PTFE)

폴리비닐플루오라이드(PVF)

폴리비닐리덴 플루오라이드(PVDF)

기타 하위 수지

액정 폴리머(LCP)

폴리아미드(PA)

하위 수지 유형별

아라미드

폴리아미드(PA) 6

폴리아미드(PA) 66

폴리프탈아미드

폴리부틸렌테레프탈레이트(PBT)

폴리카보네이트(PC)

폴리에테르에테르케톤(PEEK)

폴리에틸렌 테레프탈레이트(PET)

폴리이미드(PI)

폴리메틸메타크릴레이트(PMMA)

폴리옥시메틸렌(POM)

스티렌 공중합체(ABS 및 SAN)

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

AGC Inc.

Asahi Kasei Corporation

Daicel Corporation

Daikin Industries, Ltd.

Kuraray Co., Ltd.

Kureha Corporation

MCT PET Resin Co Ltd

Mitsubishi Chemical Corporation

PBI Advanced Materials Co.,Ltd.

Polyplastics-Evonik Corporation

Sumitomo Chemical Co., Ltd.

Techno-UMG Co., Ltd.

Teijin Limited

Toray Industries, Inc.

UBE Corporation

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

KTH

영문 목차

영문목차

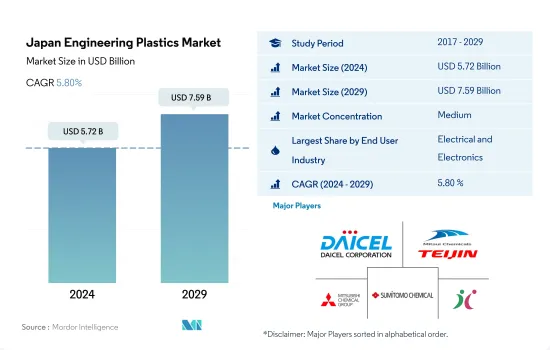

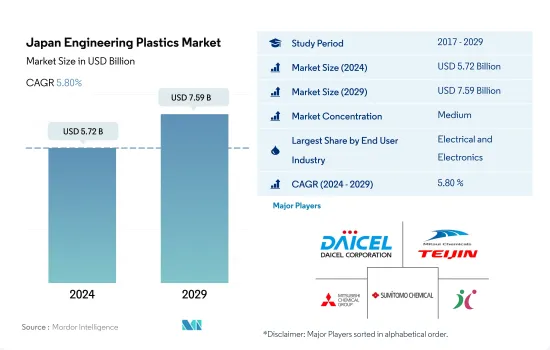

The Japan Engineering Plastics Market size is estimated at 5.72 billion USD in 2024, and is expected to reach 7.59 billion USD by 2029, growing at a CAGR of 5.80% during the forecast period (2024-2029).

The electrical and electronics industry to maintain its dominance in terms of both value and volume

Engineering plastics have applications ranging from interior wall panels and doors in aerospace to rigid and flexible packaging. In Japan, the engineering plastics market is led by the packaging, electrical and electronics, and automotive industries. Packaging and electrical and electronics industries accounted for around 26.89% and 27.23% of the engineering plastics market volume in 2022.

The electrical and electronics sector is the largest in the country. For instance, the Japanese electronics industry experienced a 2% Y-o-Y increase in domestic production in 2022, reaching a total of USD 84.34 billion. This growth was mainly attributed to the strong performance of electronic components and devices in exports, the rising usage of electronic components in vehicles, and the increasing demand for electric measuring instruments due to the growth of 5G technology. These factors led to higher consumption of engineering plastics in the country, with volume growth of 1.12% in 2022 compared to the previous year.

In 2022, the automotive industry accounted for 25.65% of the revenue share, which made it the second largest promising industry in the country. In 2022, the Japanese automotive industry grew at a Y-o-Y rate of 15.15% compared to the previous year. This was mainly due to an increase in vehicle production in the country, which was recorded at 9.41 million units in 2022, 3.49% higher than the previous year.

Aerospace is the fastest-growing industry in the country in terms of revenue, with a projected CAGR of 7.69%, owing to increased spending in the aerospace industry, which is expected to drive the demand for engineering plastics during the forecast period. Japan's aerospace component production revenue is expected to reach around USD 17 billion by 2029.

Japan Engineering Plastics Market Trends

Government policies to support domestic electrical and electronics production

The Japanese electronics industry excels in the production of components and devices, creating key technologies, such as all-solid batteries and medical cameras. The government's efforts toward decarbonization and the industry's proficiency in this field will enable further innovations by developing functions geared toward factory automation and telework-led workstyle reforms.

The country faced chip shortages caused by the trade war between the United States and China, and the increased demand that followed the move to remote working that affected the production of electronics in the country in 2019. Consecutively, due to COVID-19 pandemic-related disruptions in 2020, the number of businesses in the Japanese electronic parts, devices, and electronic circuits manufacturing industry hit a decade low of approximately 3.79 thousand establishments, a decrease from around 3.86 thousand in the previous year. The country produced consumer electronic equipment of JPY 42,908 million, by value, and industrial electronic equipment of JPY 25,5676 million, by value, in 2020.

Japan registered an increase of 19.2% in electrical and electronics production revenue from 2020 to 2021. The total production value of the electronics industry in Japan reached close to JPY 11 trillion in 2021. The industry encompasses consumer electronic equipment, industrial electronic equipment, and electronic components and devices. Consumer electronics account for a third of Japan's economic output.

The US President and Japanese Prime Minister pledged to bolster semiconductor manufacturing capacity, and the country is also investing in the innovation sector, which may boost the electronic industry in the country during the forecast period.

Japan Engineering Plastics Industry Overview

The Japan Engineering Plastics Market is moderately consolidated, with the top five companies occupying 63.27%. The major players in this market are Daicel Corporation, MCT PET Resin Co Ltd, Mitsubishi Chemical Corporation, Sumitomo Chemical Co., Ltd. and Techno-UMG Co., Ltd. (sorted alphabetically).

4.4.4 Styrene Copolymers (ABS and SAN) Recycling Trends

4.5 Regulatory Framework

4.5.1 Japan

4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Electrical and Electronics

5.1.5 Industrial and Machinery

5.1.6 Packaging

5.1.7 Other End-user Industries

5.2 Resin Type

5.2.1 Fluoropolymer

5.2.1.1 By Sub Resin Type

5.2.1.1.1 Ethylenetetrafluoroethylene (ETFE)

5.2.1.1.2 Fluorinated Ethylene-propylene (FEP)

5.2.1.1.3 Polytetrafluoroethylene (PTFE)

5.2.1.1.4 Polyvinylfluoride (PVF)

5.2.1.1.5 Polyvinylidene Fluoride (PVDF)

5.2.1.1.6 Other Sub Resin Types

5.2.2 Liquid Crystal Polymer (LCP)

5.2.3 Polyamide (PA)

5.2.3.1 By Sub Resin Type

5.2.3.1.1 Aramid

5.2.3.1.2 Polyamide (PA) 6

5.2.3.1.3 Polyamide (PA) 66

5.2.3.1.4 Polyphthalamide

5.2.4 Polybutylene Terephthalate (PBT)

5.2.5 Polycarbonate (PC)

5.2.6 Polyether Ether Ketone (PEEK)

5.2.7 Polyethylene Terephthalate (PET)

5.2.8 Polyimide (PI)

5.2.9 Polymethyl Methacrylate (PMMA)

5.2.10 Polyoxymethylene (POM)

5.2.11 Styrene Copolymers (ABS and SAN)

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 AGC Inc.

6.4.2 Asahi Kasei Corporation

6.4.3 Daicel Corporation

6.4.4 Daikin Industries, Ltd.

6.4.5 Kuraray Co., Ltd.

6.4.6 Kureha Corporation

6.4.7 MCT PET Resin Co Ltd

6.4.8 Mitsubishi Chemical Corporation

6.4.9 PBI Advanced Materials Co.,Ltd.

6.4.10 Polyplastics-Evonik Corporation

6.4.11 Sumitomo Chemical Co., Ltd.

6.4.12 Techno-UMG Co., Ltd.

6.4.13 Teijin Limited

6.4.14 Toray Industries, Inc.

6.4.15 UBE Corporation

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

8.1 Global Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)