US Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693564

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

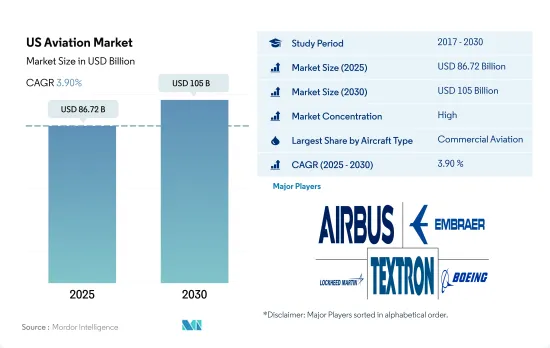

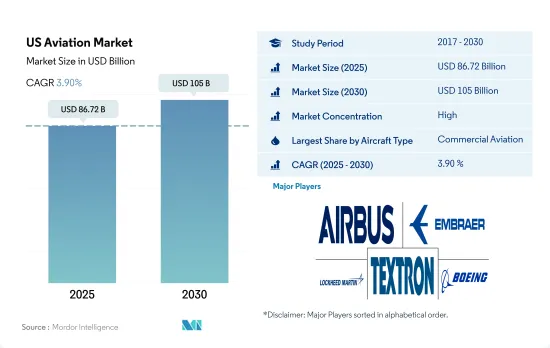

미국 항공 시장 규모는 2025년에 867억 2,000만 달러, 2030년에는 1,050억 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR은 3.90%를 나타낼 전망입니다.

미국 항공 시장에서 가장 큰 시장 점유율을 차지할 것으로 예상되는 민간 항공 부문

미국에는 민간항공, 군사항공, 일반항공을 포함하여 세계 최대이고 가장 다양한 항공시장이 있습니다.

전자상거래와 세계화는 항공화물 수요의 대폭적인 성장을 가속하고 있습니다. 민간항공은 세계에서 가장 기술적으로 진보하고 윤택한 자금을 가진 산업 중 하나입니다.

2022년에는 미국은 세계의 국방비 군사비의 39%를 차지해 8,770억 달러(0.7%) 증가했습니다.

미국 항공 시장은 민간 항공의 안정적인 수요, 군용 항공의 지속적인 현대화 노력, 일반 항공의 다양한 활동에 견인되어 번영을 계속하고 있습니다. 시장의 성장은 기술 혁신, 환경적 고려 사항, 그리고 진화하는 소비자 선호와 맞물려 있습니다. 세계의 상호 관계가 점점 긴밀해지는 가운데, 미국의 항공 시장은 앞으로도 국가의 경제와 안보의 중요한 기둥으로 남을 것으로 예측됩니다.

미국 항공 시장 동향

제한 완화와 여객 수 증가로 항공 여객 수송을 촉진

미국 항공사의 2022년 여객수는 전년 대비 30% 증가한 1억9,400만명, 2022년 통년(1월부터 12월까지)의 미국 항공사 여객수는 8억5,300만명으로, 2021년 6억5,8 00만명, 2020년의 3억 8,800만명을 상회했습니다. 그 결과, 미국의 항공사는 합계로 팬데믹 전의 92%, 국제선에서는 88.9%, 국내선에서는 92.45%의 수준을 회복했습니다.

스케줄에 따른 2023년 여름 시즌의 계획 용량 수준을 보면 미국 항공사가 운항을 계획한 좌석수는 2019년 여름보다 약 6% 많아졌습니다. 2023년 여름은 약 7억 1,560만석이 운항되었습니다. 대기업 네트워크 항공사 3사에도 변화가 보여, 아메리칸 항공은 2019년 대비 1.2% 증가의 좌석을 예정했지만, Delta Air Lines는 0.2% 감소, 유나이티드 항공은 3.3% 증가했습니다.

여행 수요 감소와 그에 따른 주요 항공사의 손실로 인해 항공사는 주로 와이드 바디 기계의 납품 예정을 연기하고 일부 기종의 조기 퇴역을 통해 기존 항공기를 재편성했습니다. 2020년 델타항공은 COVID-19 팬데믹에 의한 수익에 대한 영향을 줄이기 위해 227대의 항공기를 퇴역시켰습니다.

국방 지출 증가는 미국이 직면한 다양한 지정학적 위협에 기인합니다.

2022년 미국은 세계 국방비의 39%를 차지했으며 군사비는 8,770억 달러(0.7%) 증가했습니다. 2022년 미국은 공군부 예산을 발표했는데, 2023 회계연도 예산 요청액은 약 1,940억 달러로, 2022년도의 요구로부터 202억 달러(11.7%) 증가했습니다. 미국 국방부는 2023 회계연도(조달 및 연구, 개발, 시험 및 평가(RDT&E))에 2,760억 달러를 제안했으며, 내역은 조달이 1,459억 달러, RDT& E가 1,301억 달러로 구성 되었습니다.

요구액 2,760억 달러 중 565억 달러(연구개발비 168억 달러, 조달비 396억 달러)는 항공기의 연구개발, 항공기 취득, 초기 예비품, 항공기 지원 장비품 등 항공기와 관련 시스템에 충당되었습니다. 가장 비싼 단일 방어 프로그램인 5세대 F-35 합동 타격 전투기(JSF)는 해군(F-35C), 해병대(F-35B & C), 공군(F-35A)을 위한 61대의 항공기 요청에 110억 달러를 투자했습니다. 2023년도의 예산에는 24기의 F-15EX, 79기의 병수 지원기, 119기의 회전익 항공기, 12기의 UAV/UAS의 구입도 포함되어 있었습니다.

미국 육군의 2022년도 예산 요구는 1,730억 달러, 해군은 2,120억 달러, 공군은 2,130억 달러였습니다. 항공기 및 관련 시스템 부문은 다음과 같은 하위 그룹을 포함합니다 : 전투기(230억 달러), 화물기(50억 달러), 지원기(16억 달러)로 나머지는 UAS, 항공기 지원, 기술 개발, 항공기 개조 예산입니다.

미국 항공 산업 개요

미국 항공 시장은 상당히 통합되어 있으며 상위 5개사에서 86.35%를 차지하고 있습니다.이 시장의 주요 기업은 Airbus SE, Embraer, Lockheed Martin Corporation, Textron Inc.등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

항공 여객 수송량

항공화물 수송량

국내총생산

수입 여객 킬로(rpk)

인플레이션율

액티브 플릿 데이터

국방 지출

개인 부유층(hnwi)

규제 프레임워크

밸류체인 분석

제5장 시장 세분화

항공기 유형

민간 항공기

서브 항공기 유형별

화물기

여객기

바디 유형별

협폭동체 항공기

와이드 바디 기계

일반 여객기

서브 항공기 유형별

비즈니스 제트

바디 유형별

대형 제트기

소형 제트기

중형 제트기

피스톤 고정익기

기타

군용기

서브 항공기 유형별

고정익기

바디 유형별

다용도 항공기

훈련용 항공기

수송기

기타

회전익기

바디 유형별

멀티미션 헬리콥터

수송용 헬리콥터

기타

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Air Tractor Inc.

Airbus SE

ATR

Bombardier Inc.

Cirrus Design Corporation

Dassault Aviation

Embraer

General Dynamics Corporation

Honda Motor Co., Ltd.

Leonardo SpA

Lockheed Martin Corporation

MD Helicopters LLC.

Northrop Grumman Corporation

Pilatus Aircraft Ltd

Piper Aircraft Inc.

Robinson Helicopter Company Inc.

Textron Inc.

The Boeing Company

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

SHW

영문 목차

영문목차

The US Aviation Market size is estimated at 86.72 billion USD in 2025, and is expected to reach 105 billion USD by 2030, growing at a CAGR of 3.90% during the forecast period (2025-2030).

The Commercial Aviation Segment Is Expected To Occupy The Largest Market Share In The Us Aviation Market

The United States is home to one of the world's largest and most diverse aviation markets, encompassing commercial aviation, military aviation, and general aviation. Commercial aviation plays a pivotal role in the US economy, connecting millions of passengers and transporting vast amounts of cargo across the nation and around the globe. With a growing population and increasing disposable incomes, the demand for air travel in the US remains steady.

E-commerce and globalization have driven substantial growth in air cargo demand. The US airlines carried 194 million more passengers in 2022 than in 2021, up by 30% Y-o-Y. The US military aviation industry is one of the most technologically advanced and well-funded in the world. To maintain superiority, the US military continuously invests in research and development of advanced fighter jets and cutting-edge technologies, such as stealth and autonomous systems.

In 2022, the US accounted for 39% of global defense spending military spending, which increased by USD 877 billion in 2022, or 0.7%. General aviation covers a wide range of non-commercial flying activities, including private aviation, flight training, aerial surveys, and medical evacuation. It comprises a diverse fleet of aircraft, from small single-engine planes to business jets.

The US aviation market continues to thrive, driven by steady demand in commercial aviation, ongoing modernization efforts in military aviation, and the diverse activities of general aviation. The market's growth is intertwined with technological innovations, environmental considerations, and evolving consumer preferences. As the world becomes increasingly interconnected, the US aviation market is likely to remain a critical pillar of the nation's economy and security

US Aviation Market Trends

Ease of restrictions and rising passenger travel are driving air passenger traffic

US airlines carried 194 million more passengers in 2022 than in 2021, up by 30% Y-o-Y. For the full year 2022, January through December, US airlines carried 853 million passengers, up from 658 million in 2021 and 388 million in 2020. As a result, US carriers recovered 92% of their pre-pandemic levels in total, 88.9% of international traffic, and 92.45% of domestic traffic.

In terms of the planned capacity levels for the summer 2023 season based on schedules, the number of seats US airlines planned to operate was about 6% higher than during the summer of 2019. About 715.6 million seats were scheduled to operate in the summer of 2023, compared with 673.9 million four years ago, before the pandemic. The big three network carriers saw changes as well, with American Airlines scheduling 1.2% more seats compared to 2019, while Delta Air Lines was down by 0.2%, and United Airlines was up by 3.3%. Southwest Airlines intended to operate 142.5 million seats, up by 16.4% in 2019, and the capacity offered by Spirit Airlines was to be some 42.8% higher with 35.4 million seats.

The drop in travel demand and the associated losses faced by major airlines have resulted in airlines deferring their expected deliveries, mostly of widebody aircraft, and restructuring their existing fleet through the early retirement of a few aircraft models. For instance, in 2020, Delta Air Lines retired 227 aircraft to reduce the impact of the COVID-19 pandemic on revenue. Such deferrals impacted the delivery schedules of aircraft OEMs and compelled them to reduce their production rates in 2020 and 2021.

The increase in defense spending can be attributed to the various geopolitical threats faced by the US

In 2022, the US accounted for 39% of global defense spending military spending, which increased by USD 877 billion in 2022, or 0.7%. In 2022, the US released the Department of the Air Force budget, which outlined that for FY 2023, the budget request was approximately USD 194.0 billion, a USD 20.2 billion or 11.7% increase from the FY 2022 request. The US DoD proposed USD 276.0 billion in acquisition funds for FY2023 (Procurement and Research, Development, Test, and Evaluation (RDT&E)), which comprised USD 145.9 billion for Procurement and USD 130.1 billion for RDT&E. The financing requested in the budget is a balanced portfolio approach to implementing the National Defense Strategy recommendations.

Of the USD 276 billion in the request, USD 56.5 billion (USD 16.8 billion for RDT&E and USD 39.6 billion for Procurement) will finance aircraft and related systems, including money for aircraft R&D, aircraft acquisition, initial spares, and aircraft support equipment. The single most expensive defense program, the fifth generation F-35 Joint Strike Fighter (JSF), has USD 11.0 billion in requests for 61 aircraft for the Navy (F-35C), Marine Corps (F-35B & C), and Air Force (F-35A). Funding for FY 2023 also included the purchase of 24 F-15EX, 79 logistics and support aircraft, 119 rotary wing aircraft, and 12 UAV/UAS.

The US Army's budget request for FY 2022 was USD 173 billion, the Navy's was USD 212 billion, and the Air Force's request was USD 213 billion. The aircraft and related systems category includes the following subgroups: Combat Aircraft (USD 23.0 billion), Cargo Aircraft (USD 5.0 billion), Support Aircraft (USD 1.6 billion), with the remaining budget for UAS, aircraft support, technology development, and aircraft modifications.

US Aviation Industry Overview

The US Aviation Market is fairly consolidated, with the top five companies occupying 86.35%. The major players in this market are Airbus SE, Embraer, Lockheed Martin Corporation, Textron Inc. and The Boeing Company (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Air Passenger Traffic

4.2 Air Transport Freight

4.3 Gross Domestic Product

4.4 Revenue Passenger Kilometers (rpk)

4.5 Inflation Rate

4.6 Active Fleet Data

4.7 Defense Spending

4.8 High-net-worth Individual (hnwi)

4.9 Regulatory Framework

4.10 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)