ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

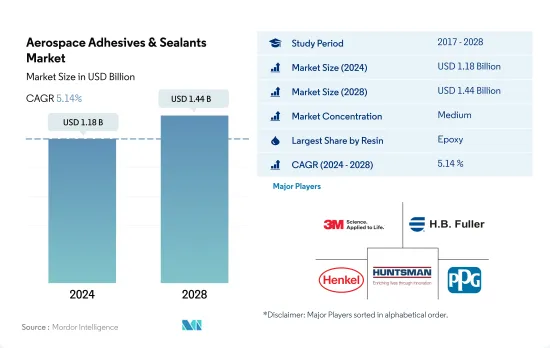

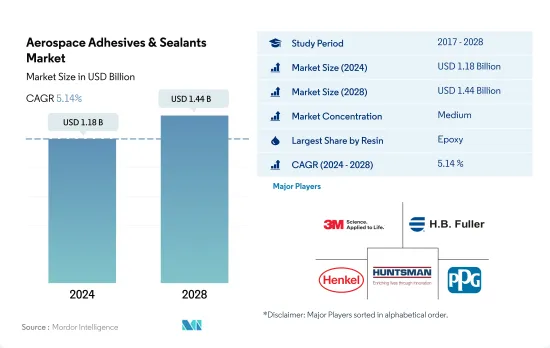

세계의 항공우주용 접착제 및 실란트 시장 규모는 2024년 11억 8,000만 달러, 2028년에는 14억 4,000만 달러에 이를 것으로 예측되며, 예측기간 중(2024-2028년) CAGR 5.14%로 성장할 전망입니다.

비용 절감과 효율성 향상으로 인해 무거운 조립 조인트 교체 수요 증가가 시장 수요를 높일 것으로 예상

접착제 및 실란트는 경량 항공기의 조립에 있어서 중요한 역할을 합니다.

항공우주용 접착제 및 실란트는 2021년 수량 기준으로 7.45%의 급성장을 보였습니다. 이는 생산시설의 재개에 의한 것으로, 2020년에 발생한 COVID-19의 영향에 의해 각국에서의 락 다운이 생산 시설의 정지를 일으켜, 접착제 및 실란트의 성장이 세계에서 감소했습니다.

항공우주용 접착제 및 실란트는 다양한 수지를 기반으로 하며, 에폭시 수지는 항공기 제조업체의 정확한 요구 사항을 충족하는 우수한 구조적 특성으로 인해 항공우주 용도에서 가장 많이 사용되는 수지 기반 접착제입니다. 샌드위치 패널, 가장자리 접착 및 공극 충전, 벌집 구조 및 기타 많은 용도와 같은 항공기의 내부 및 외부 부품 모두에서 사용됩니다.

이러한 항공기의 무게를 줄이기 위해 기계식 패스너, 나사, 용접 조인트와 같은 무거운 조립 조인트의 교체에 대한 수요 증가는 결국 연료 비용을 낮추는 데 도움이 됩니다.

탄소 삭감을 위한 혁신적인 기술 개발이 시장 수요를 끌어올립니다.

유럽에서는 민간 및 군용 헬리콥터, 항공기, 제트기 및 이들 부품을 제조하고 수출합니다. 민간 항공은 유럽 항공우주 산업에서 가장 큰 분야입니다. 프랑스, 독일, 이탈리아, 영국에는 항공우주 기업이 집중하고 있습니다. 그 때문에 유럽은 항공우주용 접착제 및 실란트의 소비량으로 제2위에 랭크되고 있습니다.

최근 북미 및 세계의 항공우주 산업은 탈탄소화의 압력에 직면해 있습니다.

전년대비 성장률이 2021년에 가장 높아지는 이유는 2020년에 COVID-19가 봉쇄되어 국제여행과 국내여행이 장기간 정지했기 때문에 유행관광 후에 레저관광이 고조되었기 때문입니다. 국제선 여객수는 2020년 4,100만명에서 2021년에는 5,900만명으로 증가합니다.

2020년 항공우주용 접착제 및 실란트 수요 감소는 전국적인 봉쇄를 일으킨 COVID-19 팬데믹의 영향, 전체적인 경기감속, 국제 및 국내항공여행 금지로 인한 것입니다.

세계 항공우주 접착제 및 실란트 시장 동향

민간항공과 군사항공의 급성장이 항공기 생산을 밀어올립니다.

세계의 항공우주산업은 북미, 아시아태평양, 유럽에 크게 지배되고 있습니다. 2021년에는 2020년의 1,807대에 대해 민간기, 일반기, 군용기를 포함한 합계 약 1,956대의 항공기가 이 나라에 납입되었습니다.

아시아태평양에서는 중국이 민간 항공우주 및 항공 서비스의 가장 크고 가장 급성장하고 있는 시장입니다.

유럽에서 독일은 가장 큰 항공우주 산업을 가지고 있으며 상대방 브랜드 제조업체(OEM), Tier I 공급업체, 시스템 통합사업자가 존재합니다. 2020년과 2021년에는 민간항공이 가장 높은 수익을 올리는 부문이 되어, 2019년의 320억 유로에 대해, 양년 모두 약 220억 유로가 되었습니다.

위의 모든 요인은 예측 기간 동안 세계 항공우주 산업에 영향을 줄 것으로 예상됩니다.

항공우주용 접착제 및 실란트 산업 개요

항공우주용 접착제 및 실란트 시장은 적당히 통합되어 있으며 상위 5개사에서 58.97%를 차지하고 있습니다. 이 시장의 주요 기업은 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC, PPG Industries, Inc.(알파벳순)가 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

항공우주

규제 프레임워크

아르헨티나

호주

브라질

캐나다

중국

EU

인도

인도네시아

일본

말레이시아

멕시코

러시아

사우디아라비아

싱가포르

남아프리카

한국

태국

미국

밸류체인과 유통채널 분석

제5장 시장 세분화

수지

아크릴

시아노아크릴레이트

에폭시

폴리우레탄

실리콘

VAE 및 EVA

기타 수지

기술

핫멜트

반응성

실란트

용제계

UV 경화형 접착제

수계

지역

아시아태평양

호주

중국

인도

인도네시아

일본

말레이시아

싱가포르

한국

태국

기타 아시아태평양

유럽

프랑스

독일

이탈리아

러시아

스페인

영국

기타 유럽

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

북미

캐나다

멕시코

미국

기타 북미

남미

아르헨티나

브라질

기타 남미

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

3M

Arkema Group

AVERY DENNISON CORPORATION

Beacon Adhesives, Inc.

Chemique Adhesives & Sealants Ltd

DELO Industrie Klebstoffe GmbH & Co. KGaA

Dow

HB Fuller Company

Henkel AG & Co. KGaA

Huntsman International LLC

Illinois Tool Works Inc.

Master Bond Inc.

Permabond LLC.

PPG Industries, Inc.

Solvay

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업의 개요

개요

Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 억제요인, 기회

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

The Aerospace Adhesives & Sealants Market size is estimated at 1.18 billion USD in 2024, and is expected to reach 1.44 billion USD by 2028, growing at a CAGR of 5.14% during the forecast period (2024-2028).

The rising demand for the replacement of heavier assembly joints to reduce costs and improve efficiency is expected to boost market demand

Adhesives and sealants play an important role in lightweight aircraft assemblies. Therefore, they are used in many structural applications, such as control systems, nacelle systems, fuselages, and engine parts.

The aerospace adhesives and sealants have shown a sudden growth of 7.45% in terms of volume in 2021. This has happened due to the economic recovery, regular supply of raw materials, and reopening of production facilities in many countries, including the United States, Canada, Germany, and China, which were impacted by the COVID-19 outbreak in 2020 where lockdowns in countries caused the shutdown of production facilities and reduction in the growth of adhesives and sealants across the world.

Aerospace adhesives and sealants are based on various resins, and epoxy resin is the most used resin-based adhesive in aerospace applications owing to its excellent structural properties, which fulfill the exact requirement of aircraft manufacturers. Epoxy adhesives are used in both interior and exterior parts of aircraft, such as sandwich panels used in fuselage construction, edge bonding and void filling, honeycomb structures, and many other applications. The tensile strength of these adhesives is up to 12000 psi(82 MPa) which is the highest among all other adhesives.

The rising demand for the replacement of heavier assembly joints, such as mechanical fasteners, screws, and weld joints, to lower the weight of air vehicles will ultimately help in lowering fuel costs. It is seen that expenditure on fuel costs by airlines has been reduced by almost 40% over the last decade. Thus, it will drive the demand for adhesives and sealants in the coming years.

Demand for innovative technology development for reducing carbon to boost market demand

European manufactures and exports both civil and military helicopters, aircraft, jets, and their components. Civil aviation is the largest segment in the European aerospace industry. Europe is home to over 3,000 companies with more than 880,000 employees. France, Germany, Italy, Spain, and the United Kingdom have a large concentration of aerospace companies. That is why Europe ranks second in the consumption of aerospace adhesives and sealants.

In recent years, the aerospace industry in North America and worldwide has been facing pressure for decarbonization. This can be done through innovative technology development for reducing carbon. This transition will lead to an increase in demand for aerospace adhesives and sealants, which will be used for adapting new technology in the forecast period, which is 2022-2028.

The year-on-year growth is highest in 2021 because of the post-pandemic boost in leisure tourism, as the lockdown in COVID-19 in 2020 put a long halt on international and domestic travel. For example, the number of international passengers traveling to and from North America increased from 41 million passengers in 2020 to 59 million passengers in 2021. This increase led to increasing in MRO business and aircraft aftermarket, which is the reason for the highest year-on-year growth in 2021.

The decline in demand for aerospace adhesives and sealants in 2020 is due to the impact of the COVID-19 pandemic, which caused a nationwide lockdown, an overall economic slowdown, and a ban on international and domestic air travel. For example, the number of international passengers flying to and from North America fell drastically from 159 million in 2019 to 41 million in 2020.

Global Aerospace Adhesives & Sealants Market Trends

Rapid growth of civil and military aviation will boost the aircraft production

The global aerospace industry is largely dominated by North America, Asia-Pacific, and Europe. The United States is both a global and regional leader in the aerospace industry due to its design, development, and production capabilities of technologically sophisticated aircraft, space systems, and military aircraft. In 2021, a total of around 1,956 units of aircraft, including civil, general, and military, were delivered to the country, compared to 1,807 units in 2020. It is forecast that the country may need 2,269 units of aircraft by 2028.

In the Asia-Pacific region, China is the largest and fastest-growing market for civil aerospace and aviation services. In 2021, the country experienced a decline in aircraft deliveries, registering around 264 units of total aircraft in civil, general, and military, compared to 367 units delivered in 2020. However, it is forecast to recover and reach 969 units in 2028.

In Europe, Germany has one of the largest aerospace industries, with the presence of original equipment manufacturers (OEMs), Tier I suppliers, and systems integrators. In 2021, the country saw an increase in aircraft deliveries, amounting to around 138 units of total aircraft in civil, general, and military, compared to 98 units in 2020. The market is projected to reach 262 units in 2028. In 2021, the aerospace industry's revenue stood at EUR 31.4 billion. In 2020 and 2021, civil aviation was the highest revenue-generating sector, amounting to around EUR 22 billion in both years, compared to EUR 32 billion in 2019. However, the market is not expected to recover until 2024-2025.

All the abovementioned factors are expected to impact the global aerospace industry during the forecast period.

Aerospace Adhesives & Sealants Industry Overview

The Aerospace Adhesives & Sealants Market is moderately consolidated, with the top five companies occupying 58.97%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and PPG Industries, Inc. (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Aerospace

4.2 Regulatory Framework

4.2.1 Argentina

4.2.2 Australia

4.2.3 Brazil

4.2.4 Canada

4.2.5 China

4.2.6 EU

4.2.7 India

4.2.8 Indonesia

4.2.9 Japan

4.2.10 Malaysia

4.2.11 Mexico

4.2.12 Russia

4.2.13 Saudi Arabia

4.2.14 Singapore

4.2.15 South Africa

4.2.16 South Korea

4.2.17 Thailand

4.2.18 United States

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 Resin

5.1.1 Acrylic

5.1.2 Cyanoacrylate

5.1.3 Epoxy

5.1.4 Polyurethane

5.1.5 Silicone

5.1.6 VAE/EVA

5.1.7 Other Resins

5.2 Technology

5.2.1 Hot Melt

5.2.2 Reactive

5.2.3 Sealants

5.2.4 Solvent-borne

5.2.5 UV Cured Adhesives

5.2.6 Water-borne

5.3 Region

5.3.1 Asia-Pacific

5.3.1.1 Australia

5.3.1.2 China

5.3.1.3 India

5.3.1.4 Indonesia

5.3.1.5 Japan

5.3.1.6 Malaysia

5.3.1.7 Singapore

5.3.1.8 South Korea

5.3.1.9 Thailand

5.3.1.10 Rest of Asia-Pacific

5.3.2 Europe

5.3.2.1 France

5.3.2.2 Germany

5.3.2.3 Italy

5.3.2.4 Russia

5.3.2.5 Spain

5.3.2.6 United Kingdom

5.3.2.7 Rest of Europe

5.3.3 Middle East & Africa

5.3.3.1 Saudi Arabia

5.3.3.2 South Africa

5.3.3.3 Rest of Middle East & Africa

5.3.4 North America

5.3.4.1 Canada

5.3.4.2 Mexico

5.3.4.3 United States

5.3.4.4 Rest of North America

5.3.5 South America

5.3.5.1 Argentina

5.3.5.2 Brazil

5.3.5.3 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 Arkema Group

6.4.3 AVERY DENNISON CORPORATION

6.4.4 Beacon Adhesives, Inc.

6.4.5 Chemique Adhesives & Sealants Ltd

6.4.6 DELO Industrie Klebstoffe GmbH & Co. KGaA

6.4.7 Dow

6.4.8 H.B. Fuller Company

6.4.9 Henkel AG & Co. KGaA

6.4.10 Huntsman International LLC

6.4.11 Illinois Tool Works Inc.

6.4.12 Master Bond Inc.

6.4.13 Permabond LLC.

6.4.14 PPG Industries, Inc.

6.4.15 Solvay

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)