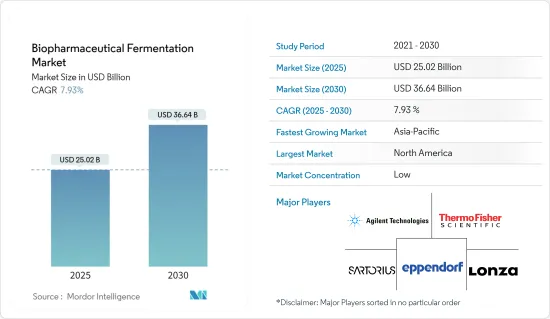

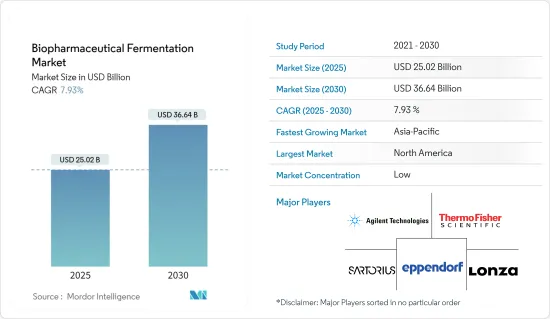

세계의 바이오 의약품 발효 시장 규모는 2025년에 250억 2,000만 달러로 추정되며 예측 기간 중(2025-2030년) CAGR은 7.93%로, 2030년에는 366억 4,000만 달러에 달할 것으로 예측됩니다.

이 시장은 비용효과가 높은 바이오시밀러의 도입으로 수요가 급증하고 바이오테크놀러지에 근거한 의약품의 보급이 진행되고 있습니다. 주요 기업은 제품의 출시나 전략적 이니셔티브를 통해, 이러한 의약품의 채용을 한층 더 강화하고 있습니다.

심혈관 질환과 같은 질병의 세계 증가는 바이오 테크놀로지 기반 의약품에 대한 수요를 밀어 올리고 있습니다. 2024년 1월 British Heart Foundation 보고서에 따르면 영국에서는 760만 명, 전 세계에서는 6억 2,000만명이 심혈관질환과 싸우고 있으며, 이 숫자는 고령화와 라이프스타일의 변화에 의해 증가 경향에 있습니다.

Eikonoklastes Therapeutics가 2022년 11월에 Forge Biologics와 제휴한 ALS 표적 유전자 치료제과 Sanofi가 2022년 8월에 제휴한 Janevent Biologics의 암 치료제와 같은 기업의 노력은 업계의 기세를 뒷받침하고 있습니다. 생물 제제 개발에 이러한 제휴는 보다 효과적인 치료를 실현하기 위해 선진적인 생물 제제와 혁신적인 약물 전달 시스템을 활용하는 것입니다.

그 결과, 암 부담 증가나 업계 기업에 의한 전략적 활동 증가 등의 요인이 시장 성장을 가속할 것으로 예측됩니다.

바이오 의약품 발효 시장은 예측 기간 동안 크로마토그래피 분야의 현저한 성장이 예측됩니다.

크로마토그래피는 분자의 크기, 전하, 소수성, 특정 리간드 결합에 따라 분자를 분리합니다. 크로마토그래피 유형의 선택은 발효 제품의 물리적 및 화학적 특성에 따라 달라집니다.

새로운 크로마토그래피 장치의 도입은 이 부문의 제품 포트폴리오를 확대하고 있습니다. 2023년 11월, 3M은 Harvest RC Chromatographic Clarifier, BT500으로 크로마토그래피 클라리파이어의 라인업을 확충했습니다. 이 500mL의 일회용의 청징화 장치는 단클론항체, 재조합 단백질, 생물 제제용으로 조정되어 있어 5-8%의 PCV(충전 세포량) 배양으로부터 불과 10분으로 예측 수량의 샘플을 제공합니다.

2022년 10월, Tosoh Bioscience GmbH는 다운스트림 공정 강화를 위해 설계된 Octave BIO 멀티컬럼 크로마토그래피(MCC) 시스템을 발표했습니다. BIO는 전임상부터 임상, GMP 제조에 이르기까지 모든 생체분자 제조 단계를 목표로 하는 MCC 장치의 첫 번째 시리즈 중 하나입니다.

제약 기업과 생명공학 기업 간의 전략적 파트너십은 효율적인 다운스트림 공정을 위한 크로마토그래피 솔루션을 강화할 예정입니다.

이러한 개발, 특히 제약회사와 생명공학기업 간의 제품 상시 및 제휴를 고려하면, 크로마토그래피 분야는 향후 수년간 크게 성장할 가능성이 있습니다.

북미는 예측 기간 동안 바이오 의약품 분야에서 큰 성장을 이루고 있습니다. 만성 질환이 유행함에 따라 의약품의 소비량이 증가하고 바이오 의약품 섹터를 더욱 뒷받침하고 있습니다.

기술적 진보, 제품 시장, 승인, 자금 조달, 제휴 등 업계 각사의 전략적 움직임은 시장 성장을 가속할 것으로 예측됩니다. 2024년 1월, 미국의 WuXi Biologics는 매사추세츠 주 우스터에 있는 새로운 시설을 업그레이드했습니다.

또한 북미에서는 류마티스 관절염, 당뇨병, 암 등의 질병이 증가하고 있으며 시장을 강화하고 있습니다. 2023년 캐나다 암 협회(CCS)의 보고서는 캐나다의 암 부담이 증가하고 있음을 강조하고 새로운 바이오 의약품의 기회 확대, 나아가 시장 성장을 시사하고 있습니다.

2024년 1월 Eurofins CDMO는 온타리오주에 제약회사용 파일럿 규모의 생물제제개발시설을 발표했습니다. 2023년 10월, Thermofisher Scientific은 미주리 주 세인트 루이스의 생물학적 제제 제조 능력을 향상 시켰습니다.

당뇨병이나 암 등의 질병 부담 증가, 바이오 의약품 발효에 대한 수요의 높아짐, 기업 활동의 활성화를 생각하면, 시장은 향후 수년에 성장하는 태세가 갖추어지고 있습니다.

수많은 세계적 및 지역적 기업들이 바이오 의약품 발효 시장의 세분화에 기여하고 있습니다. 높은 점유율을 가진 시장 주요 기업에는 Thermo Fisher Scientific Inc., Danaher Corporation, Sartorius Stedim Biotech, Merck KGaA, Eppendorf AG, F. Hoffmann-La Roche Ltd., Nova Biomedical Corporation, Lonza Group AG, Agilent Technologies, Becton, Dickinson, and Company 등이 있습니다.

The Biopharmaceutical Fermentation Market size is estimated at USD 25.02 billion in 2025, and is expected to reach USD 36.64 billion by 2030, at a CAGR of 7.93% during the forecast period (2025-2030).

The market has seen a surge in demand due to the introduction of cost-effective biosimilars, enhancing the uptake of biotech-based drugs. Fermentation plays a pivotal role in producing the active substances of these drugs. For instance, a January 2024 report from MJH Life Sciences highlighted a notable increase in cancer-related products, with certain categories capturing an 80% share of biosimilars. Key players, through product launches and strategic initiatives, have further bolstered the adoption of these drugs. A case in point is Boehringer Ingelheim's October 2023 launch of an unbranded biosimilar version of AbbVie's Humira, priced at a striking 81% discount to the original.

The global rise in disease prevalence, such as cardiovascular issues, has driven the demand for biotech-based drugs. A January 2024 British Heart Foundation report noted that 7.6 million individuals in England and 620 million worldwide are grappling with cardiovascular diseases, a figure on the rise due to aging and lifestyle changes. This escalating demand for biotech drugs is poised to propel market growth.

Company initiatives, such as Eikonoklastes Therapeutics' November 2022 partnership with Forge Biologics for ALS-targeting gene therapy and Sanofi's August 2022 alliance with Janevent Biologics for oncology drugs, underscore the industry's momentum. These collaborations in biologics development leverage advanced biologics and innovative drug delivery systems to create more effective treatments. Such advancements are expected to boost demand for biopharmaceutical fermentation, driving market growth during the forecast period.

Consequently, factors like the escalating cancer burden and increased strategic activities by industry players are anticipated to fuel market growth. However, the high costs associated with biopharmaceutical fermentation and installations may temper this expansion.

Significant growth is projected for the chromatography segment in the biopharmaceutical fermentation market during the forecast period. This growth is driven by rising demand for innovative biopharmaceutical drugs and the introduction of new products.

Chromatography separates molecules based on size, charge, hydrophobicity, and specific ligand binding. The choice of chromatography type depends on the physical and chemical characteristics of the fermentation products. For example, reversed-phase high-performance liquid chromatography (HPLC) is employed to purify recombinant human insulin and separate biological variant insulin molecules from various species.

The introduction of new chromatography devices is expanding the segment's product portfolio. For instance, in November 2023, 3M expanded its chromatographic clarifier lineup with the Harvest RC Chromatographic Clarifier, BT500. This 500-mL, single-use clarifier is tailored for monoclonal antibodies, recombinant proteins, and biologics, delivering predictive yield samples in just 10 minutes from a 5-8% packed cell volume (PCV) culture.

In October 2022, Tosoh Bioscience GmbH unveiled the Octave BIO Multi-Column Chromatography (MCC) system, designed for downstream process intensification. Paired with SkillPak BIO pre-packed columns, it streamlines pre-clinical process development. Octave BIO is the one of the first in a series of MCC instruments targeting all biomolecule manufacturing phases, from pre-clinical to clinical and GMP production.

Strategic partnerships between pharmaceutical and biotechnology firms are set to enhance chromatography solutions for efficient downstream processing. For example, in February 2024, Purolite and Repligen Corporation launched Praesto CH1, a 70μm agarose-based affinity resin, tailored for purifying specialized mAbs like bispecifics and recombinant antibody fragments.

Given these developments, especially product launches and collaborations between pharmaceutical and biotechnology firms, the chromatography segment is poised for substantial growth in the coming years.

North America is set for significant growth in the biopharmaceutical sector during the forecast period. This expansion is driven by a rising demand for biotech medications, heightened research and development activities, and increased investments in biopharmaceutical fermentation. Additionally, as chronic diseases become more prevalent, medication consumption rises, further propelling the biopharmaceutical sector. This trend not only boosts the demand for biologics and biotech drugs but also underscores the importance of biopharmaceutical fermentation.

Strategic moves by industry players, such as technological advancements, product launches, approvals, fundraising, and partnerships, are expected to drive market growth. For example, in January 2024, WuXi Biologics in the U.S. upgraded its new facility in Worcester, Massachusetts. This enhancement is set to raise the facility's commercial drug substance capacity from 24,000 liters to 36,000 liters, in response to growing service demand. Such an increase in capacity is poised to amplify the utilization of biopharmaceutical fermentation.

Furthermore, rising disease prevalence in North America, including rheumatoid arthritis, diabetes, and cancer, is bolstering the market. These diseases drive the demand for biotech and biological drugs, produced through biopharmaceutical fermentation. Highlighting this, a 2023 report from the Canadian Cancer Society (CCS) emphasized the escalating cancer burden in Canada, signaling a growing opportunity for new biopharmaceuticals and, consequently, market growth.

In January 2024, Eurofins CDMO unveiled its pilot-scale biologic drug development facility in Ontario, tailored for pharmaceutical companies. This facility offers range of services, such as upstream and downstream development, supplies for preclinical or Phase 1 trials. Additionally, in October 2023, Thermo Fisher Scientific boosted its manufacturing capacity in St. Louis, Missouri, for biologics production. The company further expanded its biopharmaceutical footprint by launching a cell therapy manufacturing facility in San Francisco, California, in March 2023.

Given the rising burdens of diseases like diabetes and cancer, the growing demand for biopharmaceutical fermentation, and heightened corporate activities, the market is poised for growth in the coming years.

Numerous global and regional players contribute to the fragmented nature of the biopharmaceutical fermentation market. Key players in the competitive landscape encompass both international and local firms. Notable companies holding significant market shares include Thermo Fisher Scientific Inc., Danaher Corporation, Sartorius Stedim Biotech, Merck KGaA, Eppendorf AG, F. Hoffmann-La Roche Ltd., Nova Biomedical Corporation, Lonza Group AG, Agilent Technologies, and Becton, Dickinson, and Company, among others.