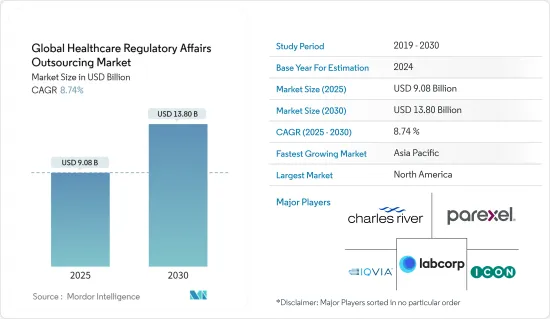

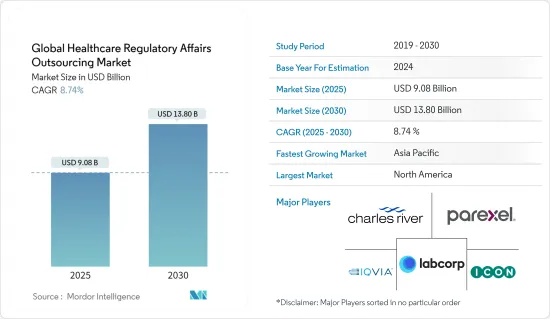

세계의 헬스케어 RA(Regulatory Affairs) 아웃소싱 시장 규모는 2025년에 90억 8,000만 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR 8.74%로 성장할 전망이며, 2030년에는 138억 달러에 달할 것으로 예측됩니다.

팬데믹 기간 동안 COVID-19 환자가 대량으로 유입된 결과 대량의 봉쇄가 발생하여 암 등 다양한 만성 질환의 임상 연구가 중단되었습니다. 팬데믹 중 임상시험 수가 감소한 결과, 헬스케어 RA 아웃소싱 서비스에 대한 수요가 감소했습니다. 예를 들어, 2021년 12월에 Frontiers in Medicine1 잡지에 게재된 연구에서는 팬데믹 중에 COVID-19 환자 수가 증가하여 임상시험 활동이 감소한 것으로 강조되었습니다. 이 출처는 또한 팬데믹 중 COVID-19 이외의 임상 개발에서 신약 신청이 감소했다고 말합니다.

따라서 세계 공급망의 혼란은 팬데믹 초기 단계에서 의약품 제조 및 유통에 영향을 주었고 시장 성장에 큰 영향을 미쳤습니다. 약사팀은 필수적인 의약품의 가용성과 안전성 확보에 관한 과제를 극복해야 했고, 규제의 적응이 필요했습니다.

또한 연구개발비 증가, 임상시험 건수 증가, 아웃소싱 비용 효과가 시장 성장의 원동력이 될 것으로 예상됩니다. 예를 들어, 2022년 2월에 발표된 Global Observatory on Health R&D analysis에 따르면, WHO의 대부분 지역에서 WHO International Clinical Trials Registry Platform(ICTRP)에 등록된 신규 모집의 임상시험 수는 지속적으로 증가하고 있습니다. 또한 WHO의 유럽, 아메리카, 서태평양 지역의 등록 시험 수는 다른 지역보다 높은 비율로 증가하고 있습니다. 예를 들어 2021년 서태평양 지역에 등록된 임상시험 수는 16,860건으로 851건이었던 아프리카의 약 20배였습니다. 이와 같이 임상시험 수 증가로 예측기간 동안 약사업무의 아웃소싱이 증가할 것으로 예상됩니다.

게다가 제약기업과 생명공학 기업에 의한 연구개발 투자 증가가 시장 성장의 원동력이 될 것으로 예상됩니다. PhRMA의 발표에 따르면, PhRMA 회원사는 2021년에 약 1,023억 달러를 연구개발 활동에 투자했습니다. 유럽 제약 단체 연합회(European Federation of Pharmaceutical Industries and Associations)가 2022년에 발표한 데이터에 따르면, 연구 개발 기반의 유럽 제약 업계는 지난 수년보다 증가했으며, 2021년에는 3,000억 유로(3,237억 달러)에 달했습니다. 또한 같은 정보원은 이 산업이 2021년에 415억 유로(447억 7,000만 달러)라는 다액의 연구개발 투자를 받았다고 말했습니다.

또한 M&A 등 주요 시장 기업의 다양한 전략적 활동이 시장 성장을 가속할 것으로 예상됩니다. 예를 들어, 2021년 7월 Covance는 환자 중심의 분산 임상시험(DCT)의 세계 리더인 GlobalCare를 인수하고 Covance의 DCT 서비스를 국제 시장으로 확대하고 환자 중심의 시험 설계에 대한 수요 증가에 대응합니다.

이와 같이 위의 요인은 헬스케어 서비스 산업 수요가 증가하고 예측 기간 동안 시장 성장이 촉진될 것으로 예상됩니다. 그러나 데이터 보안과 관련된 위험과 표준화의 부족은 조사 대상 시장의 주요 억제요인이 되었습니다.

제품등록이란 해당 국가 또는 지역에서 제품을 판매, 유통, 판매 및 수입할 수 있도록 해당 국가 및 지역에서 적용되는 당국이 승인하는 규제 당국에 대한 승인 신청을 의미합니다. 임상시험 등록신청서(Clinical Trial Application)란 해당 국가에서 임상시험을 실시할 수 있는 허가를 얻기 위해 해당 국가의 규제당국에 제출하는 서류를 말합니다. 임상시험 신청서에는 임상시험과 임상시험에 대한 자세한 정보가 기재되어 있으며, 규제 당국은 시험의 실행 가능성을 평가할 수 있습니다.

선진국과 신흥 국가 모두에서 임상시험 신청과 제품등록 아웃소싱이 증가하고 있는 것으로 예측기간에 걸쳐 제품등록과 임상시험신청 부문을 견인하고 있습니다. 제품 등록 프로세스의 복잡성, 업계 전문가 부족, 내부 능력 부족으로 인해 대부분의 제약 회사 및 의료기기 회사는 제품 등록 업무를 제3자 서비스 제공업체에 아웃소싱합니다. 또한, 약사 규제의 끊임없는 변경과 업데이트도 이러한 서비스의 아웃소싱을 뒷받침하고 있습니다. 예를 들어, 2022년 1월 31일, 유럽 의약청은 EU에서 임상시험의 규제 조화를 발표했습니다. 또한 새로운 임상시험 정보시스템(CTIS)을 시작하였습니다. 이것은 예측 기간 동안 이 분야의 성장을 가속할 것으로 예상됩니다.

따라서 위의 모든 요인은 예측 기간 동안 부문 성장을 가속할 것으로 예상됩니다.

상환 시나리오의 변화 및 제네릭 의약품의 경쟁으로 인한 가격 압력은 주요 제약 회사의 규제 관련 업무 아웃소싱을 일으키고 있으며, 북미에서 약사 아웃소싱 서비스의 성장을 이끌 것으로 예상됩니다. 또한, 연구개발 활동 활성화 및 임상시험 증가가 이 지역 시장 성장을 가속할 것으로 예상됩니다. 예를 들어, Global Observatory on Health R&D에 따르면, 미국은 2021년에 10,870건의 임상시험을 등록했으며, 전체의 18.1%를 차지했습니다. 이 출처에 따르면 캐나다에서는 2021년에 2,099건의 임상시험이 등록되어 전체의 3.5%를 차지했습니다. 이와 같이, 이 지역에서는 많은 임상시험이 실시되고 있어 약사 아웃소싱 시장을 견인할 가능성이 높습니다.

게다가 지역 주요 기업의 존재와 업계의 전략적 제휴가 시장 성장을 가속하고 있습니다. 예를 들어, 2021년 4월 Parexel과 Veeva Systems는 기술과 프로세스 혁신을 활용하여 임상시험을 가속화하기 위한 전략적 제휴를 발표했습니다. 양사는 서로의 약사 컨설팅 서비스로부터 이익을 얻게 됩니다.

따라서 위의 모든 요인들은 예측기간에 걸쳐 북미 시장 성장을 가속할 것으로 예상됩니다.

헬스케어 RA(Regulatory Affairs) 아웃소싱 시장은 다양한 시장 기업의 존재로 인해 약간 단편화된 시장이 되고 있습니다. 경쟁 구도에는 Charles River Laboratories, Syneos Health, Laboratory Corporation of America Holdings, ICON Plc, IQVIA, PAREXEL International Corporation, Thermo Fisher Scientific Inc.(PPD) 등, 높은 시장 점유율을 보유한 몇 개 기업 분석이 포함됩니다.

The Global Healthcare Regulatory Affairs Outsourcing Market size is estimated at USD 9.08 billion in 2025, and is expected to reach USD 13.80 billion by 2030, at a CAGR of 8.74% during the forecast period (2025-2030).

During the pandemic, the massive influx of COVID-19 patients resulted in mass lockdowns, which disrupted clinical studies of various chronic diseases such as cancer. The reduction in the number of clinical trials amid the pandemic resulted in a decrease in the demand for healthcare regulatory affairs outsourcing services. For instance, a study published in the Frontiers in Medicine1 in December 2021 highlighted that clinical trial activities decreased during the pandemic as the number of COVID-19 patients increased. The source also stated that new drug submissions dropped in non-COVID-19 clinical developments amid the pandemic.

Therefore, disruptions in the global supply chain affected the manufacturing and distribution of pharmaceutical products during the pandemic's initial phase, significantly impacting the market growth. Regulatory affairs teams had to navigate challenges related to ensuring the availability and safety of essential drugs, necessitating regulatory adaptations.

Moreover, growing R&D expenditure, the increasing number of clinical trials, and the cost-effectiveness of outsourcing are expected to drive market growth. For instance, according to Global Observatory on Health R&D analysis published on February 2022, there was a constant rise in the number of newly recruiting trials registered on the WHO International Clinical Trials Registry Platform (ICTRP) for most WHO regions. Moreover, the number of trials registered in WHO's Europe, Americas, and Western Pacific regions increased at a higher rate than in other regions. For instance, in 2021, Western Pacific registered 16,860 clinical trials, around 20 times higher than that in Africa, which accounted for 851 clinical trials. Thus, an increasing number of clinical trial studies are expected to increase regulatory affairs outsourcing over the forecast period.

Furthermore, increasing research and development investment by pharmaceutical and biotechnology firms is anticipated to drive market growth. As per the PhRMA, the members of PhRMA invested about USD 102.3 billion in R&D activities in 2021. As per the data published by the European Federation of Pharmaceutical Industries and Associations in 2022, the research-based European pharmaceutical industry has increased from the past years and reached the value of EUR 300 billion (USD 323.7 billion) in 2021. The same source also stated that this industry received a significant R&D investment of EUR 41.5 billion (USD 44.77 billion) in 2021.

Additionally, various strategic activities by key market players, such as mergers and acquisitions, are anticipated to drive market growth. For instance, in July 2021, Covance acquired GlobalCare, a global leader in patient-centric decentralized clinical trials (DCTs), to expand Covance's DCT offerings into international markets and meet the growing demand for patient-centric trial designs.

Thus, the factors mentioned above are expected to increase the demand for healthcare regulatory services in the industry, thereby driving market growth over the forecast period. However, the risk associated with data security and lack of standardization is the major restraining factor for the studied market.

Product Registration refers to the application for regulatory approval granted by the applicable authority in a given country or territory to allow a product to be marketed, distributed, sold, or imported into the country or region. The Clinical Trial Application refers to submission to the competent national regulatory authorities for getting authorization to conduct a clinical trial in the country. The clinical trial application contains detailed information about the investigational medicinal product and planned trial, allowing regulatory authorities to assess the study's feasibility.

The increase in outsourcing of clinical trial applications and product registrations in both developed and developing countries is driving the product registration and clinical trial application segment over the forecast period. Due to the complexity of the product registration process, lack of professionals in the industry, and lack of internal capability, most pharmaceutical and medical device companies outsource their product registration activities to third-party service providers. Furthermore, constant changes and updation in regulatory affairs also drive the outsourcing of such services. For instance, on 31 January 2022, the European Medicines Agency announced the regulatory harmonization of clinical trials in the EU. It also launched a new Clinical Trials Information System (CTIS). This is anticipated to propel the segment growth over the forecast period.

Thus, all factors mentioned above are expected to boost segment growth over the forecast period.

Pricing pressure due to the changing reimbursement scenario and generic competition is causing major pharmaceutical firms to outsource regulatory affairs activities expected to drive the growth of healthcare regulatory outsourcing services in North America. Additionally, growing research and development activity and rising clinical trials are anticipated to drive regional market growth. For instance, according to the Global Observatory on Health R&D, the United States registered 10,870 clinical trials in 2021, accounting for 18.1% of the total. According to the same source, Canada registered 2,099 clinical trials in 2021, accounting for 3.5% of the total. Thus, many clinical trials in the region are likely to drive the regulatory affairs outsourcing market.

Moreover, the presence of key regional players and strategic collaborations in the industry are driving the market's growth. For instance, in April 2021, Parexel and Veeva Systems announced a strategic partnership to speed up clinical trials by leveraging technology and process innovation. Both businesses will benefit from each other's regulatory consulting services.

Thus, all factors above are expected to boost the market growth in the North America region over the forecast period.

The Healthcare Regulatory Affairs Outsourcing Market is a slightly fragmented market owing to the presence of various market players. The competitive landscape includes an analysis of a few companies which hold significant market shares, including Charles River Laboratories, Syneos Health, Laboratory Corporation of America Holdings, ICON Plc., IQVIA, PAREXEL International Corporation, and Thermo Fisher Scientific Inc. (PPD), among others.