ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

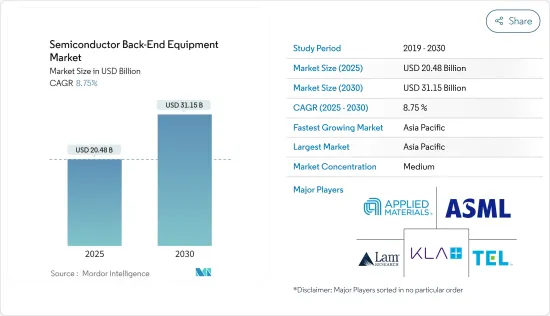

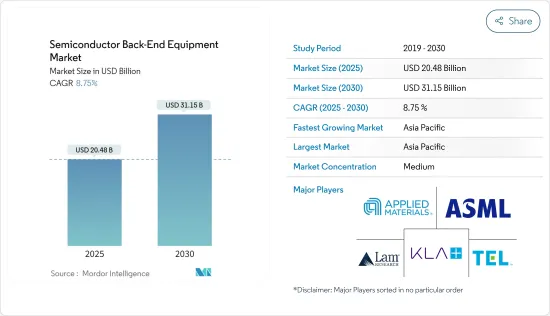

반도체 백엔드 장비 시장 규모는 2025년에 204억 8,000만 달러로 추정되고, 2030년에는 311억 5,000만 달러에 이를 것으로 예측되며, 예측 기간 2025년부터 2030년까지 CAGR 8.75%로 성장할 전망입니다.

주요 하이라이트

에너지 전환, 전동화, AI 등의 기술을 도입하는 것이 세계 시장에서 반도체 수요를 재형성하는 최전선이 되고 있습니다. 예를 들어 인공지능(AI)을 반도체 산업에 통합하는 것은 혁신, 효율성, 기회의 새로운 시대를 말하는 것입니다. 과거에 반도체 산업은 주로 다른 하이테크 분야의 인에이블러 역할을 했습니다.

그러나 AI를 통해 반도체는 기술 개발을 변화시키는 최전선에 서서 업계의 경제 상황을 재구성하고 있습니다. 예를 들어, AI를 탑재한 칩은 자율주행차에 사용되고 있습니다. 이렇게 하면 주변 상황에 따라 실시간으로 판단할 수 있습니다. 또한 AI를 탑재한 칩은 헬스케어 업계에서도 환자의 실시간 모니터링 및 건강 문제를 검출하는데 사용되고 있습니다. 이러한 혁신은 생활과 일을 일변시켜 생활을 보다 친숙하고 효율적인 것으로 만듭니다.

또한, 재생 불가능한 연료에 대한 의존도를 줄이고 기후 변화와 싸우기 위해 세계는 점점 더 신재생 에너지원으로 이동하고 있습니다. 전기는 이러한 전환을 달성하기 위한 중요한 전략이며, 반도체는 에너지 생성, 저장 및 소비 방법을 변화시키는 데 핵심적인 역할을 합니다.

반도체, 특히 아날로그 제품과 임베디드 프로세싱 제품은 보다 스마트하고 신뢰성이 높고 사용하기 쉬운 태양에너지 저장 시스템과 전기자동차 충전 시스템을 통해 전기를 실현하기에 적합한 위치에 있습니다. 이와 같이 각 기업은 고전압 파워, 전류 및 전압 센싱, 에지 및 프로세싱, 커넥티비티 제품의 4개의 중요한 분야에 주력함으로써, 다양한 최종 사용자 시장에서의 반도체의 역학의 변화에 대응해, 선진 반도체 웨이퍼, 패키징, 조립 공정의 백앤드 장비의 역할을 추진하는 중요한 역할을 하고 있습니다.

반도체 산업은 급속히 확대되고 있으며, 반도체 제조 장치 수요도 급증하고 있습니다. 그러나 반도체 제조 장비의 가격은 반도체 산업에 매우 중요한 요소가 되었습니다. 장치 비용은 반도체 생산 비용에 현저한 영향을 미치며 최종 제품의 가격에 영향을 미칩니다. 이것은 시장의 성장을 억제할 것으로 예상됩니다.

거시 경제 불확실성, 개인 소비 감소, 세계 경제 변동과 같은 요인은 칩 수요를 방해할 것으로 예상됩니다. 일반적으로 경기후퇴기에는 개인 소비가 감소하고 반도체에 크게 의존하는 스마트폰, 태블릿, 노트북 등의 가전 제품에 대한 수요가 감소합니다. 만일 세계 경제의 악화가 이어져 소비자 수요가 더욱 약해진다고 가정합니다. 이 경우 이러한 요인은 향후 몇 년동안 반도체 시장에 악영향을 미칠 것으로 예상됩니다.

반도체 백엔드 장비 시장 동향

어셈블리 패키징 부문이 크게 성장할 것으로 예상

이 부문의 성장은 팬아웃 웨이퍼 레벨 패키징(FOWLP), 웨이퍼 레벨 패키징(WLP), 시스템 인 패키지(SiP)와 같은 최첨단 패키징 기술이 받아들여지고 있는 것으로 배경으로 보입니다. 게다가 최근의 고급 패키징을 통해 여러 집적 회로를 단일 패키지로 통합할 수 있는 스택형 WLCSP와 같은 패키징 기술도 등장했습니다. 이러한 진보에는 로직 칩과 메모리 칩의 조합과 적층 메모리 칩이 포함됩니다. 그 결과, 첨단 패키징 수요가 급증할 것으로 예상되며, 이에 대응하는 장비의 구매가 필요합니다.

다양한 분야에서 반도체 IC의 사용이 급증함에 따라 반도체 패키징과 어셈블리 장치에 대한 요구가 증가하고 있습니다. 그 일례로서 일렉트로닉스 업계에서는 전자기기와 그 용도의 보급으로 이러한 장치의 필요성이 확대되고 있습니다. 이것은 수요 증가에 크게 기여할 것으로 예상됩니다. 마찬가지로, 반도체의 소형화, 고속화, 고효율화에 대한 요구가 높아짐으로써, 첨단 패키징 기술에 대한 수요를 뒷받침해 반도체 패키징 장치 수요를 높여가고 있습니다.

다양한 산업 분야에서 반도체의 세계적 요구가 증가함에 따라 반도체 생산 능력의 확대로 이어져 반도체 백엔드 장비 시장의 성장을 뒷받침하고 있습니다. 2023년 8월, 저명한 반도체 파운드리인 TSMC는 최첨단 패키징 장비를 제공하는 여러 공급업체에 새로운 주문을 시작했습니다. Gudeng Precision Industrial, Apic Yamada, Disco, Scientech는 회사와 긴밀하게 협력하는 공급업체 중 하나입니다. TSMC가 장비 공급업체와의 제휴를 결정한 것은 첨단 패키징 능력 강화를 위한 회사의 지속적인 노력을 반영한 것입니다.

반도체 칩의 이용과 생산이 현저하게 성장하고 있는 것은 반도체 패키징과 조립 장치 분야의 확대를 지지하는 중요한 원동력이 되고 있습니다. 게다가 SIA가 지원하는 WSTS에 의한 최근 업계 예측은 2023년 세계 매출이 9.4% 감소한 이후 2024년에는 13.1% 증가할 것으로 예측했습니다. 이 예측은 2023년 세계 매출액이 5,200억 달러에 이르렀고, 2022년 5,741억 달러에서 감소한 것으로 평가되었습니다. 2024년에는 세계 매출이 5,884억 달러로 증가할 것으로 예상됩니다. 이러한 긍정적인 산업 동향은 패키징 장비 공급업체가 시장 기회를 활용할 수 있게 하는 것으로 보입니다.

이 시장은 Micron, TSMC, ASE와 같은 저명한 벤더들이 패키징 기술에 투자하는 것 외에도 다른 벤더들이 이러한 기술에 의해 가져온 이점을 활용함으로써 견인될 것으로 예상됩니다. Apple, Samsung, Intel 등은 첨단 칩 패키징(ACP)을 활용하여 여러 컴포넌트를 하나의 보드에 통합함으로써 디바이스의 성능과 효율성을 높였습니다. 이러한 기업의 채용은 ATP 장비의 성장을 가속할 것으로 보입니다.

아시아태평양이 시장의 대폭 성장에 기대

중국은 1,500억 달러의 자금 지원을 받아 야심찬 반도체 의제를 추진하고 있습니다. 이 나라는 국내 IC 산업을 강화하고 칩 생산을 증가시키는 것을 목표로 하고 있습니다. 현재 진행 중인 미국과 중국의 무역전쟁은 최첨단 공정 기술이 집중되는 이 중요한 분야에서의 긴장을 격화시키고, 많은 중국 기업을 반도체 파운드리에 대한 투자로 이끌고 있습니다. 중국은 주조, 질화갈륨(GaN), 탄화규소(SiC) 시장에서 크게 확대된 캠페인 등 반도체 부문을 강화하기 위한 다양한 이니셔티브를 발표하고 있습니다.

이 지역에서 반도체 사업의 성장과 칩 생산 능력의 향상은 백앤드 장비 수요를 촉진할 것으로 예상됩니다. 중국의 하이테크 산업은 통신, 신재생 에너지, 전기자동차(EV)의 강력한 존재를 활용하여 세계의 기술 밸류 체인을 상승시키는 것을 목표로 하고 있습니다.

이 분야 외에도이 산업은 현재 첨단 반도체에도 주력하고 있습니다. 이러한 전환은 주로 첨단 노드 제조의 진보, 메모리 시장 확대, 탄화규소(SiC) 경쟁에 대한 적극적인 참여, 첨단 패키징 및 제조 장비에 대한 전략적 투자에 의해 추진되고 있습니다. 중국 전역에서 파운드리 사업 확대와 팹 투자가 진행됨에 따라 시장이 활성화될 것으로 예상됩니다.

한국은 지난 수년간 반도체 산업에서 현저한 성장을 이루고 있으며, 생산량과 출하량이 모두 크게 증가하고 있습니다. 이 급성장은 기술 진보의 부활을 보여주며 한국 경제와 세계의 하이테크 분야에 좋은 징조입니다. 삼성과 SK하이닉스 등 한국의 주요 반도체 기업은 세계 반도체 산업에서 주요 기업으로서의 지위를 확립하고 있습니다. 이 지역의 칩 생산 능력 확대는 백앤드 장비 시장을 더욱 밀어올릴 것으로 보입니다.

이 지역의 다양한 시장에서 칩 수요의 급증은 백앤드 반도체 사업에 주목하고 있습니다. 백앤드를 전문으로 하는 기업은 향후 수년간 적극적인 투자와 기술적 진보를 지속할 것으로 예상됩니다.

반도체 백엔드 장비 산업 개요

반도체 백엔드 장비 시장은 세계 기업 및 중소기업 모두가 존재하기 때문에 반고체화되고 있습니다. 시장의 주요 기업으로는 ASML Holding NV, Applied Materials Inc., LAM Research Corporation, Tokyo Electron Corporation, KLA Corporation 등이 있습니다. 시장 기업들은 제품 라인업을 강화하고 지속 가능한 경쟁 우위를 얻기 위해 파트너십, 사업 확대, 인수 등의 전략을 채택하고 있습니다.

2023년 12월-Applied Materials Inc.와 CEA-Leti는 ICAPS 시장(IoT, 통신, 자동차, 전력, 센서)을 지원하는 특수 반도체 용도를 위한 재료 공학 솔루션에 초점을 맞춘 공동 연구소를 설립하여 협력 관계를 확대했습니다. 이 실험실은 IoT, 전기자동차, 스마트 그리드 인프라에 대한 수요에 대응하여 차세대 디바이스의 혁신을 가속화하는 것을 목표로 합니다. 이 프로젝트는 ICAPS 디바이스의 성능 향상, 전력 소비 감소, 시장 출시까지의 시간 단축을 실현하기 위한 재료 공학의 과제를 다루고 있습니다.

2023년 11월-Samsung Electronics와 ASML홀딩은 한국 공동 연구개발시설에 1조 원(7억 6,000만 달러)을 투자하는 예비계약을 체결했습니다. ASML 본사에서 조인된 각서에 기재된 이 제휴는 ASML의 최첨단 극단 자외선(EUV) 장치를 사용한 메모리 칩의 개발에 초점을 맞춘 것입니다. 세계에서 유일한 EUV 스캐너 제조업체인 ASML의 기술은 복잡한 반도체 패터닝, 제조 간소화, 생산 수율 향상에 매우 중요합니다. 연구개발 센터는 ASML이 공동으로 설립한 최초의 해외 시설로 차세대 EUV 기술을 기반으로 한 초미세 반도체 제조 공정 개발에 집중합니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 전제조건 및 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도-Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

밸류체인 및 공급망 분석

COVID-19, 거시경제 동향, 지정학적 시나리오의 영향

제5장 시장 역학

시장 성장 촉진요인

전기자동차 및 하이브리드 차량의 반도체 수요 증가

신규 파운드리의 설립 수요(국제적인 칩 부족)

시장 성장 억제요인

높은 셋업 비용

제품의 끊임없는 진화가 수요에 영향

제6장 시장 세분화

유형별

측정 및 검사

다이싱

본딩

조립 및 포장

지역별

미국

유럽

중국

한국

대만

일본

기타 아시아태평양

세계 기타 지역

제7장 경쟁 구도

기업 프로파일

ASML Holding NV

Applied Materials Inc.

LAM Research Corporation

Tokyo Electron Limited

KLA Corporation

Advantest Corporation

Onto Innovation Inc.

Screen Holdings Co., Ltd.

Teradyne Inc.

Nordson Corporation

제8장 투자 분석

제9장 시장의 미래

AJY

영문 목차

영문목차

The Semiconductor Back-End Equipment Market size is estimated at USD 20.48 billion in 2025, and is expected to reach USD 31.15 billion by 2030, at a CAGR of 8.75% during the forecast period (2025-2030).

Key Highlights

Incorporating technologies such as energy transition, electrification, and AI has been at the forefront of reshaping the demand for semiconductors in the global market. For instance, integrating artificial intelligence (AI) into the semiconductor industry signals a new era of innovation, efficiency, and opportunity. In the past, the industry primarily served as an enabler for other high-tech sectors.

However, with AI, semiconductors are at the forefront of transforming technology development, reshaping the industry's economic landscape. For instance, AI-powered chips are used in self-driving cars. This enables them to make real-time decisions based on their surroundings. AI-powered chips are also used in the healthcare industry for real-time monitoring of patients and detecting health issues. These innovations can transform the way of living and working, making lives more accessible and efficient.

Furthermore, the world is increasingly shifting toward renewable energy sources to reduce reliance on non-renewable fuels and combat climate change. Electrification is a key strategy for achieving this transition, and semiconductors are playing a central role in revolutionizing how energy is generated, stored, and consumed.

Semiconductors, particularly analog and embedded processing products, are well positioned to enable electrification through smarter, more reliable, and accessible solar-energy storage and electric-vehicle charging systems. Thus, companies are playing a significant role in addressing the changing dynamics of semiconductors in various end-user markets by focusing on four critical areas, namely high-voltage power, current and voltage sensing, edge processing, and connectivity products, thus driving the role of back-end equipment for advanced semiconductor wafers, packaging, and assembly process.

The semiconductor industry has been expanding rapidly, and the demand for semiconductor manufacturing equipment has also surged. However, the price of these machines has turned out to be a crucial factor in the industry. The equipment cost can have a noteworthy impact on the production cost of semiconductors, affecting the final product's price. This is expected to restrain the market's growth.

Factors such as macroeconomic uncertainty, decreased consumer spending, and fluctuations in the global economy are expected to hamper chip demand. Consumer spending typically decreases during an economic downturn, reducing demand for consumer electronics like smartphones, tablets, and laptops, which rely heavily on semiconductors. Suppose the global economy continues to deteriorate and consumer demand weakens further. In that case, these factors are anticipated to have a detrimental effect on the semiconductor market in the upcoming years.

Semiconductor Back-End Equipment Market Trends

Assembly and Packaging Segment is Expected to Witness Significant Growth

The segment's growth is expected to be driven by the increasing acceptance of cutting-edge packaging techniques such as fan-out wafer-level packaging (FOWLP), wafer-level packaging (WLP), and system-in-package (SiP). Furthermore, recent advancements have led to the emergence of packaging technologies like stacked WLCSPs, which enable the integration of multiple integrated circuits in a single package. These advancements encompass a combination of logic and memory chips, as well as stacked memory chips. As a result, the demand for advanced packaging is anticipated to surge, necessitating the acquisition of corresponding equipment.

The surge in the utilization of semiconductor ICs in various sectors has led to a rise in the requirement for semiconductor packaging and assembly equipment. An example is the electronics industry's expanding necessity for such equipment, driven by the widespread use of electronic devices and their applications. This is anticipated to be a significant factor contributing to the increased demand. Likewise, the growing need for smaller, faster, and more efficient semiconductors is propelling the demand for advanced packaging technologies, fueling the demand for semiconductor packaging equipment.

The increasing global need for semiconductors in different industries has led to an expansion in their production capacity, consequently fueling the growth of the semiconductor back-end equipment market. In August 2023, TSMC, a prominent semiconductor foundry, initiated new orders with multiple suppliers of state-of-the-art packaging equipment. Gudeng Precision Industrial, Apic Yamada, Disco, and Scientech are among the suppliers working closely with the company. TSMC's decision to engage with equipment suppliers reflects its ongoing commitment to enhancing its advanced packaging capabilities.

The significant growth in the utilization and production of semiconductor chips is a key driver behind the expansion of the semiconductor packaging and assembly equipment sector. Moreover, a recent industry forecast by WSTS, supported by SIA, predicts a 9.4% decline in global sales for 2023, followed by a 13.1% increase in 2024. The forecast anticipates that global sales will amount to USD 520 billion in 2023, a decrease from the USD 574.1 billion recorded in 2022. By 2024, global sales are expected to rise to USD 588.4 billion. These positive industry trends will enable packaging equipment vendors to capitalize on market opportunities.

The market is anticipated to be driven by the investments made by prominent vendors such as Micron, TSMC, and ASE in packaging technologies, along with other vendors capitalizing on the advantages offered by these technologies. Apple, Samsung, and Intel are among the companies that utilize advanced chip packaging (ACP) to enhance device performance and efficiency by consolidating multiple components onto a single substrate. Such adoption by the companies will enhance the growth of ATP equipment.

Asia-Pacific Expected to Witness Significant Growth in the Market

China is pursuing an ambitious semiconductor agenda with the support of USD 150 billion in funding. The country aims to enhance its domestic IC industry and increase its chip production. The ongoing US-China trade war has intensified tensions in this crucial sector, where the most advanced process technology is concentrated, leading many Chinese companies to invest in semiconductor foundries. China has unveiled various initiatives to strengthen its semiconductor sector, such as a substantial expansion campaign in the foundry, gallium-nitride (GaN), and silicon carbide (SiC) markets.

The growing semiconductor business and increasing chip production capabilities in the region are expected to drive the demand for back-end equipment. China's tech industry aims to ascend the global technology value chain by capitalizing on its strong presence in telecommunications, renewables, and electric vehicles (EVs).

In addition to these sectors, the industry is now focusing on advanced semiconductors. This transition is primarily driven by advancements in advanced node manufacturing, the expansion of the memory market, active involvement in the silicon carbide (SiC) race, and strategic investments in advanced packaging and manufacturing equipment. The growing foundry business and investments in fabs throughout China are anticipated to stimulate the market.

South Korea has seen notable growth in its semiconductor industry over the past few years, with a substantial increase in both production and shipments. This surge indicates a resurgence in technological advancement, which bodes well for the country's economy and the global tech sector. Leading South Korean semiconductor companies like Samsung and SK Hynix have established themselves as key players in the global semiconductor industry. The expanding chip production capabilities in the region will further boost the market for back-end equipment.

The surge in chip demand across various markets in the region has brought attention to the back-end semiconductor business. Companies specializing in back-end processes are anticipated to persist in making aggressive investments and technological advancements in the upcoming years.

Semiconductor Back-End Equipment Industry Overview

The semiconductor back-end equipment market is semi-consolidated due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are ASML Holding NV, Applied Materials Inc., LAM Research Corporation, Tokyo Electron Limited, and KLA Corporation. Players in the market are adopting strategies such as partnerships, expansions, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

December 2023: Applied Materials and CEA-Leti have expanded their collaboration with a joint lab focusing on materials engineering solutions for specialty semiconductor applications, catering to ICAPS markets (IoT, communications, automotive, power, and sensors). The lab aims to accelerate innovation for next-gen devices by addressing demands from IoT, electric vehicles, and smart grid infrastructure. Projects will tackle materials engineering challenges to enhance ICAPS device performance, reduce power consumption, and achieve faster time to market.

November 2023: Samsung Electronics and ASML Holding have inked a preliminary agreement to invest 1 trillion WON (USD 760 million) in a joint research and development facility in South Korea. The collaboration, outlined in a memorandum of understanding signed at ASML's headquarters, focuses on advancing memory chips using ASML's cutting-edge extreme ultraviolet (EUV) equipment. As the exclusive EUV scanner manufacturer globally, ASML's technology is pivotal for intricate semiconductor patterning, streamlining manufacturing, and enhancing production yields. The R&D center, the first overseas facility jointly established by ASML, will concentrate on developing ultra-fine semiconductor manufacturing processes based on next-generation EUV technology.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Value Chain / Supply Chain Analysis

4.4 Impact of COVID-19, Macro Economic Trends, and Geopolitical Scenarios

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Demand for Semiconductors in Electric and Hybrid Vehicles

5.1.2 Demand for Setting Up New Foundries (International Chip Shortage)

5.2 Market Restraints

5.2.1 High Setup Costs

5.2.2 Constant Evolution of Products Influencing Demand