Europe Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1690817

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

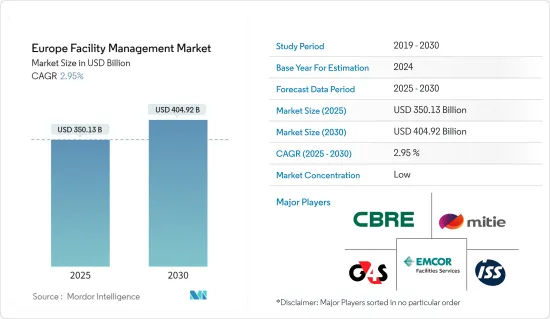

유럽의 시설 관리(FM) 시장 규모는 2025년에 3,501억 3,000만 달러로 추정되고, 2030년에는 4,049억 2,000만 달러에 이를 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 2.95%를 나타낼 전망입니다.

유럽은 시설 관리 서비스의 성숙도와 정교함 측면에서 가장 큰 아웃소싱 시장 중 하나로 꼽힙니다.

주요 하이라이트

소규모 현지 기업은 단일 계약과 단일 서비스 솔루션에 집중하는 반면, 이 지역의 시설 관리 비즈니스는 여러 대륙과 국가에 걸쳐 유명 벤더와 통합 계약을 맺고 운영됩니다. 여기에는 다국적 기업이 여러 지사에 대해 단일 계약으로 제공되는 편의성 때문에 여러 국가에 진출한 서비스 제공업체를 선택하는 경우도 포함됩니다.

또한 시설 관리(FM)는 조직의 인프라 관리, 전략, 건물 관리 절차, 업무 공간의 전반적인 조화를 포함합니다. 이 시스템은 조직의 서비스를 표준화하고 절차를 간소화하며, 나머지는 시설 관리 서비스가 처리합니다.

지난 10년 동안 유럽에서 사업을 운영하는 많은 서비스 제공업체는 특히 비핵심 기능을 아웃소싱하는 현재의 추세에 따라 FM 서비스에 대한 수요 증가를 활용하기 위해 입지를 넓히는 데 집중해 왔습니다. 2023년 10월, OCS는 교육 및 의료 분야의 중요 시설 관리 서비스를 전문으로 하는 영국 기업 Accuro를 인수했습니다. 이 그룹은 이번 계약을 통해 Accuro가 성장하고 발전하여 OCS와 통합되면 직원들에게 새로운 기회를 창출하여 역량을 향상시키고 더 나은 서비스를 제공할 수 있을 것이라고 밝혔습니다.

유럽의 시설 관리 시장 동향

상업용 건물 부문이 상당한 시장 점유율을 차지할 전망

투자 회사들은 주로 유럽의 주거용 또는 상업용 부동산 시장에 집중하고 있습니다. 상업용 건물은 수익성 높은 기회를 제공하기 때문에 매력적인 지역 투자 형태입니다.

유럽의 시설 관리 시장은 이 지역의 벤더와 상업 단체 간의 많은 파트너십을 관찰하고 있습니다. 예를 들어, 2023년 4월 BT Group은 7,500개 이상의 영국 부동산 포트폴리오에 시설 및 프로젝트 관리 서비스를 제공하여 8만 명 이상의 BT Group 및 Openreach 직원을 지원하기 위해 CBRE와의 계약을 연장했습니다.

마찬가지로 2023년 1월, ISS UK&I는 Virgin Media O2와 시설 관리 계약을 연장 및 확장했습니다. 영국 최대 엔터테인먼트 및 통신 회사 중 하나가 시설 서비스 제공을 조정할 수 있도록 지원하면서 합작 투자 이후 파트너십이 새롭고 흥미로운 단계로 발전했습니다. 이 계약을 통해 ISS는 Virgin Media O2의 영국 인프라에 종합 시설 관리 서비스를 제공하고, 모든 국가 기술 운영과 통합된 오피스 포트폴리오를 조정하여 운영 효율성과 서비스 품질을 향상시킬 수 있게 되었습니다.

스마트 빌딩 및 기타 IoT 기술 구축에 대한 관심이 높아짐에 따라 시장 공급업체는 IoT 기반 시설 관리를 도입하고 유럽에서 스마트 상업용 빌딩의 성장을 촉진할 수 있는 다양한 기회를 얻게 되었습니다. 2023년 5월, Planon은 기업들에게 부동산 및 시설 관리의 완벽한 솔루션을 제공하기 위해 SAP와의 전략적 파트너십을 발표했습니다. 그 결과, 부동산 포트폴리오를 최적화하여 관리함으로써 기업 조직과 상업용 부동산 회사에 도움이 되고 건설의 지속가능성을 개선할 수 있을 것으로 기대됩니다.

신축 및 노후 상업용 건물을 스마트 빌딩으로 전환하는 디지털화 추세는 부동산 가치를 높이고 시설 관리자와 건물주를 지원하는 데 도움이 됩니다. 독일의 시설 관리 서비스 산업은 다양한 사내 및 아웃소싱 시설 관리를 위한 맞춤형 솔루션에 대한 수요 증가로 인해 성장하고 있습니다. 주요 도시에 상업용 및 주거용 건물이 증가함에 따라 전국적으로 시설 관리 서비스에 대한 수요가 증가하고 있습니다.

투자자들은 하이브리드 근무 트렌드에도 불구하고 장기 임차인이 있는 현대식 사무실에 높은 관심을 보이고 있습니다. 업계 종사자들의 비즈니스 통찰력이 높아지고 자동차 산업에서 다른 분야로 경제가 다각화되면서 이 지역의 시설 관리 서비스에 대한 수요가 증가할 것으로 보입니다.

빅데이터는 시설 관리 팀이 효율성과 비용 절감을 목표로 하는 데 기여

지난 몇 년 동안 시설 관리는 빠르게 발전하여 유럽 산업에 광범위한 변화를 가져왔습니다.

공공 부문, 소매업, 전문 서비스, 의료, 기술, 물류, 제조, 교육 등 다양한 분야에서 아웃소싱 FM을 성공적으로 활용하고 있습니다. FM 서비스는 기업의 유형, 기업 규모, 운영 분야에 따라 다양한 영역에 중점을 두고 있습니다.

유럽 시장은 사내 서비스 제공에서 번들 서비스로, 더 나아가 단일 계약을 통한 통합 시설 관리 접근 방식으로 전환하는 것을 목표로 하고 있습니다.

향후 FM 조직이 첨단 혁신 기술을 개발함에 따라 데이터에 대한 상당한 투자가 증가할 것입니다. 기업들은 완전한 IoT 시스템 구축, 분석 기술 확립, 증강현실과 인공지능 활용을 통해 BDA 투자를 강화할 수 있습니다.

Cloudscene에 따르면 2023년 독일은 522개의 데이터 센터를 보유하여 유럽에서 가장 많은 데이터 센터를 보유하고 있는 국가 중 하나입니다. 독일의 인터넷 문맹률도 93.1%를 차지했습니다. 이러한 통계는 주로 빅데이터와 같은 도구에 의해 주도되는 데이터 처리 능력의 잠재적 발전을 나타냅니다. 시설 관리자는 데이터센터가 항상 접근 가능하고 안전하며 최적으로 운영되도록 보장합니다.

유럽의 시설 관리 산업 개요

유럽의 시설 관리 시장은 다양한 규모의 다양한 회사로 세분화되어 있습니다. 이 시장은 현재 겪고 있는 경기 침체를 상쇄하기 위해 기업들이 전략적 투자를 지속함에 따라 여러 파트너십, 인수합병, 인수가 이루어질 것으로 예상됩니다.

2023년 12월 : CBRE Global Workplace Solutions(GWS)와 영국의 주요 철도 제조업체 인 Alstom은 장기 시설 관리 파트너십을 연장하고 Alstom의 광범위하고 다양한 국내 포트폴리오를 하나의 계약으로 통합했습니다. 연장된 파트너십에 따라 CBRE와 GWS는 기술 서비스, 청소, 폐기물 관리 등 영국 전역의 주요 생산 및 유지보수 허브에 다각적인 시설 관리 서비스를 제공할 예정입니다.

2023년 7월 : G4S 화재 보안 팀은 브릭스 & 포레스터사와 공동으로 영국에서 주목도가 높은 3개의 대형 부동산 프로젝트에 임할 계획을 발표. Street, 리즈의 Phoenix는 오피스, 점포, 주택이 혼재해, 지속가능성과 도시 재생에 근거해 건설됩니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

유럽에서의 하드(MEP)와 소프트(서비스) FM의 주요 시장 동향

COVID-19 팬데믹 및 기타 거시경제 요인이 시장에 미치는 영향

제5장 시장 역학

시장 성장 촉진요인

FM의 상품화를 향한 성장 추세

워작업장 최적화 및 생산성에 대한 새로운 강조

시장의 과제

이익 마진 감소 및 거시 환경의 지속적인 변화

제6장 시장 세분화

시설 관리 유형별

사내 시설 관리

아웃소싱 시설 관리

단일 FM

번들 FM

통합 FM

최종 사용자별

상업용 빌딩

소매

정부 및 공공 기관

제조 및 산업

기타

국가명

영국

독일

프랑스

이탈리아

스페인

제7장 경쟁 구도

기업 프로파일

CBRE Group

Mitie Group PLC

Emcor Facilities Services WLL

Atlas FM Ltd

G4S Facilities Management UK Limited

ISS Global

JLL Limited

Engie FM Limited Cofely AG

Andron Facilities Management

Kier Group PLC

Vinci Facilities Limited

Compass Group

Sodexo Facilities Management Services

Aramark Corporation

OKIN Facility(OKIN Group)

Atalian Servesr(Atalian Global Services)

Apleona GmbH

제8장 투자 분석

제9장 시장의 미래

HBR

영문 목차

영문목차

The Europe Facility Management Market size is estimated at USD 350.13 billion in 2025, and is expected to reach USD 404.92 billion by 2030, at a CAGR of 2.95% during the forecast period (2025-2030).

Europe is considered one of the biggest outsourced markets for facility management services in terms of maturity and sophistication.

Key Highlights

The small local companies focus on single contracts and single-service solutions, whereas the region's facility management businesses operate with integrated contracts from prominent vendors across continents and countries. These include multinational companies choosing service providers with a presence in multiple countries due to the convenience offered under a single contract for various branches. However, due to the regional dynamics, more options are cropping up to combine facility management and corporate real estate.

Additionally, facility management (FM) covers infrastructure management for an organization, strategies, procedures for managing buildings, and general harmonization of the workplace. This system standardizes services and streamlines procedures for an organization, with the facility management service taking care of the rest.

Over the past decade, many service providers that have operations in Europe have been concentrating on growing their presence to leverage the growing demand for FM services, particularly due the current trend of outsourcing non-core functions. In October 2023, OCS acquired Accuro, a UK company specializing in critical facility management services in education and healthcare. The group stated that the agreement allows Accuro to grow and develop, creating new opportunities for its staff when integrated with OCS, enabling them to improve their capabilities and provide better services.

Europe Facility Management Market Trends

The Commercial Buildings Segment is Expected to Hold a Significant Market Share

Investment firms mainly focus on the residential or commercial property markets in Europe. Commercial buildings are an appealing form of regional investment as they offer lucrative opportunities. This trend will likely aid the growth of the facility management market in Europe during the forecast period. Commercial investments lead to higher cash flow potential and often provide better ROI.

The facility management market in Europe is observing many partnerships between vendors and commercial entities in the region. For instance, in April 2023, BT Group extended its agreement with CBRE to provide facilities and project management services to its UK portfolio of more than 7,500 properties to support over 80,000 BT Group and Openreach colleagues. The contract extension will extend the current partnership until 2026 to achieve a new and improved level of cooperation and service delivery.

Similarly, in January 2023, ISS UK&I extended and expanded its facilities management contract with Virgin Media O2. It took the partnership through a new and exciting phase after the joint venture, supporting one of the United Kingdom's largest entertainment and telecoms firms to align the facilities service delivery. The contract allows ISS to provide total facilities management services in Virgin Media O2's UK infrastructure, with all national technical operations and a combined office portfolio being aligned to achieve operating efficiencies and enhanced service quality.

The rising interest in establishing smart buildings and other IoT technologies provides various opportunities for market vendors to introduce IoT-based facility management and boost the growth of smart commercial buildings in Europe. In May 2023, Planon announced its strategic partnership with SAP to provide companies with a complete solution in real estate and facility management. As a result, optimized management of their real estate portfolios will benefit corporate organizations and commercial property firms and improve the sustainability of construction. This collaboration combines Planon with SAP's market-leading ERP capabilities to create a more comprehensive integration of processes and technologies.

Such digitalization trends of transforming new and old commercial buildings into smart buildings help boost property values and support facility managers and property owners. Germany's facility management service industry is growing due to the rising demand for customized solutions for different in-house and outsourced facility management. The growing number of commercial and residential buildings in major cities leads to the demand for facility management services nationwide. Rapid infrastructure development and the growing focus on integrated facility management services may influence the facility management market positively.

Investors are highly interested in modern offices with long-term tenants despite the trend of hybrid working. The growing business acumen among industry players and economic diversification from automobile industries to other avenues will likely increase the demand for facility management services in the region.

Big Data is Helping Facility Management Teams Aim for Efficiency and Cost Savings

Over the past several years, facility management has evolved rapidly, leading to widespread changes in the European industry. The region's facility management market is undergoing a paradigm shift due to the growing popularity of trends related to data, disruption, evolving amenities, and new workplace concepts.

Various sectors, including the public sector, retail, professional services, healthcare, technology, logistics, manufacturing, and education, have successfully used the outsourced FM. FM services focus on varied areas, depending on their type, the size of the company, and the sector in which it operates. It is not a one-size-fits-all approach. While some organizations only require a single service solution provider, other big organizations look for bundled services offering complete facility management solutions. These services also differ based on the type and amount of data generated by client organizations, with data analytics tools like Big Data helping almost all sizes of organizations and their contracts.

The European market aims to shift from in-house delivery of services to bundled services and further toward the integrated facilities management approach with single contracts. This integrated FM approach offers a range of services and longer-term contracts, adding value, driving better quality and economies of scale, and boosting the demand for outsourced services that require specialist expertise.

Future significant data investments by FM organizations will likely increase as they develop advanced and innovative technologies. The companies may enhance BDA investments by creating complete IoT systems, establishing analytical skills, and utilizing AR and AI. FM organizations need to partner with technology companies, consultants, and institutions offering higher education to scale up the applications for enterprise-level usage.

As per Cloudscene, in 2023, Germany had 522 data centers, which accounted for one of the highest numbers of data centers in Europe. Germany's internet literacy rate also accounted for 93.1%. Such statistics indicate the potential development of data processing capabilities, mainly driven by tools like Big Data. Facility managers ensure a data center is always accessible and secure and operates optimally. The emergence of technologies like Big Data necessitates the deployment of ample data center storage.

Europe Facility Management Industry Overview

The facility management market in Europe is fragmented, with diverse firms of different sizes. This market is expected to witness several partnerships, mergers, and acquisitions as organizations continue to invest strategically in offsetting the present slowdowns being experienced. The clients in this region are employing FM services to increase the ease of their business operations and tackle the energy crisis through energy-efficient facility management services.

December 2023: CBRE Global Workplace Solutions (GWS) and the United Kingdom's leading rail manufacturer, Alstom, extended their long-term facility management partnership, consolidating Alstom's extensive and varied national portfolio under one contract. Under the extended partnership, CBRE and GWS will provide a multi-faceted facilities management service for Alstom's critical production and maintenance hubs across the United Kingdom, including technical services, cleaning, and waste management.

July 2023: The G4S Fire and Security team announced their plan of working with Briggs & Forrester on three large, high-profile real estate projects in the United Kingdom. The Cocoa Works in York, 135 Park Street in London, and Phoenix in Leeds will provide a mix of office, retail, and residential space, which will be built based on sustainability and urban regeneration. G4S is the systems provider for the three projects to support these objectives by providing and installing fire and life safety equipment.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Key Market Trends in Hard (MEP) and Soft (Service) FM in Europe

4.4 Impact of the COVID-19 Pandemic and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Trend Toward Commoditization of FM

5.1.2 Renewed Emphasis on Workplace Optimization and Productivity

5.2 Market Challenges

5.2.1 Diminishing Profit Margins and Ongoing Changes in Macro-environment