액정 폴리머(LCP) 필름 및 라미네이트 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Liquid Crystal Polymer (LCP) Films And Laminates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1690701

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

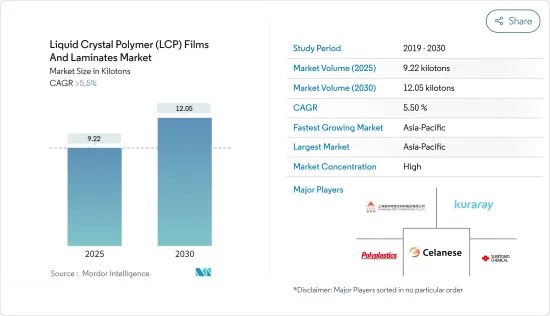

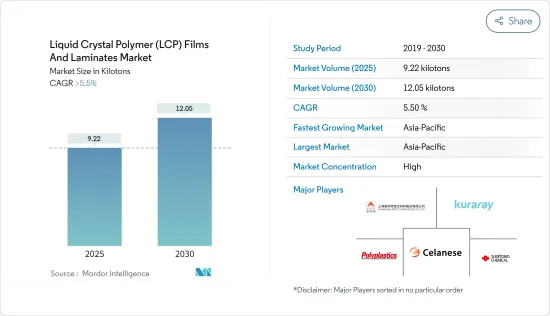

세계의 액정 폴리머(LCP) 필름 및 라미네이트 시장 규모는 2025년 9.22킬로톤으로 추정되며, 예측 기간 중(2025-2030년) CAGR 5.5%를 초과하고 2030년에는 12.05킬로톤에 달할 것으로 예측됩니다.

COVID-19 팬데믹은 액정 폴리머(LCP) 필름 및 라미네이트 시장에 부정적인 영향을 미쳤습니다. 전국적인 봉쇄와 엄격한 사회적 거리두기 조치로 다양한 전자기기의 제조 활동이 중단되어 액정 폴리머(LCP) 필름 및 라미네이트 시장에 영향을 미쳤습니다.

그러나, 액정 폴리머(LCP) 필름 및 라미네이트의 전자, 자동차, 포장 용도에 대한 수요 증가로 인해 시장은 이후 크게 회복되었습니다.

주요 하이라이트

전기 및 전자 부품의 소형화 수요 증가와 자동차 부품용 경량 재료의 개발에 의해 연구 시장 수요 증가가 전망됩니다.

액정 폴리머(LCP) 필름 및 라미네이트의 제조 및 가공 비용이 높은 것이 시장 성장의 방해가 될 것으로 예상됩니다.

ASEAN과 인도의 전자 시장의 잠재적 성장은 예측 기간 동안 시장에 성장 기회를 가져올 것으로 예상됩니다.

아시아태평양은 가장 큰 시장으로 중국, 인도, ASEAN 국가 등의 소비 증가로 예측 기간 동안 가장 빠르게 성장하는 시장이 될 것으로 예상됩니다.

액정 폴리머(LCP) 필름 및 라미네이트 시장 동향

시장을 독점하는 전자 제품 분야

액정 폴리머(LCP)와 라미네이트는 전자 산업 전반에 걸쳐 적용 범위를 확장하고 있습니다. LCP 필름은 저유전율, 높은 방습성, 제어 가능한 열팽창 계수, 고주파 특성, 비할로겐 난연성 등 우수한 전기적 및 기계적 특성을 갖추고 있습니다.

원격근무나 재택근무의 보급이 전자기기 수요를 밀어 올렸습니다. 또한 디지털화 투자의 활성화로 데이터 활용의 고도화가 진행되어 솔루션 서비스가 확대되었습니다. 이 때문에 전자 분야에서 사용되는 LCP 필름 및 라미네이트에 대한 수요가 증가할 것으로 예상됩니다.

세계의 전자 산업은 현저한 성장률을 기록했습니다. 일본전자정보기술산업협회(JEITA)에 따르면 세계 전자 및 IT산업의 생산액은 2021년 3조 3,600억 달러에 비해 2022년에는 3조 4,300억 달러로 전년대비 1%의 성장률을 기록했습니다. 게다가 2023년에는 전년 대비 3%의 성장률로 3조 5,200억 달러에 달할 것으로 예상됐습니다.

아시아태평양은 세계 전자제품 생산의 70% 이상을 차지합니다. 한국, 일본, 중국 등의 국가들이 전기 부품을 제조하여 세계의 다양한 산업에 공급하고 있습니다. 게다가 인도는 2025년까지 세계 제5위의 가전 및 일렉트로닉스 산업이 될 것으로 예상되고 있습니다.

인도의 일렉트로닉스 시스템 설계 및 제조(ESDM) 부문은 2025년까지 1,000억 달러 이상의 경제 가치를 창출할 것으로 예상됩니다. 인도에서의 전기 및 전자기기의 생산은 Make in India, National Policy of Electronics, Net Zero Imports in Electronics 등 국내 제조업의 성장에 커밋하는 정부의 정책에 의해 급속히 증가할 것으로 예상되고 있습니다. 전자 산업의 성장은 현재의 연구 시장을 견인할 것으로 예상됩니다.

마찬가지로 유럽에서는 독일의 전자 산업이 현저한 성장률을 기록했습니다. ZVEI에 따르면 독일의 전자 디지털 산업 매출은 전년 2,169억 달러(2,000억 유로)에 비해 2022년에는 2,435억 달러(2,245억 유로)에 달했습니다. 이와 같이 전자 산업의 성장은 이 나라의 액정 폴리머(LCP) 필름 및 라미네이트 시장 수요를 견인할 것으로 예상됩니다.

이러한 요인들로부터, 예측 기간 동안, 전자 응용 분야는 액정 폴리머(LCP) 필름 및 라미네이트 시장을 독점할 것으로 예상됩니다.

시장을 독점하는 아시아태평양

예측 기간 동안 아시아태평양은 액정 폴리머(LCP) 필름 및 라미네이트 시장을 독점할 것으로 예측됩니다. 액정 폴리머(LCP) 필름 및 라미네이트에 대한 수요가 증가하고 있는 것은 중국, 일본, 인도의 일렉트로닉스 산업과 자동차 산업입니다.

중국, 일본 등의 국가에서는 전자 산업이 현저한 성장률을 기록하고 있으며, 실리콘 코팅 시장을 견인하고 있습니다. 중국의 전자 산업 시장은 2021년에 10% 증가한 반면 2022년에는 13% 증가했습니다. 2023년의 예상 성장률은 7%입니다.

일본은 세계 최대의 일렉트로닉스 기업의 본거지이며, 다양한 전자기기나 디바이스의 생산에 큰 점유율을 누리고 있습니다. 전자정보기술산업협회(JEITA)에 따르면 2022년 일본 일렉트로닉스산업의 총 생산액은 약 743억 달러(11조 1,243억엔)에 달했고, 전년보다 8% 가까이 상승했습니다.

또한, 액정 폴리머(LCP) 필름 및 라미네이트에 대한 수요는 자동차 산업 및 수송 산업에서 증가하고 있습니다. 인도는 이 지역에서 2위의 자동차 제조업체가 되고 있습니다. OICA에 따르면 2022년 자동차 생산 대수는 545만대에 달했고, 2021년 439만대에서 24%의 성장을 보였습니다. 따라서 자동차 생산량 증가는 현재 연구 시장을 견인할 것으로 예상됩니다.

액정 폴리머(LCP) 필름은 포장 산업에도 응용되고 있습니다. 2022년 3월, TCPL Packaging Ltd.는 연포장 공장의 생산 능력을 두 배로 늘리고 상업 생산을 시작했습니다. 이 회사는 또한 고어 공장에 새로운 생산 라인을 추가하고 오프셋 생산 능력을 확대했습니다. 이러한 생산능력 확대로 시장 관계자도 예상되는 수요 증가에 대응하는 태세를 마련하고 있습니다.

이러한 요인으로부터 예측 기간 동안 아시아태평양이 액정 폴리머(LCP) 필름·라미네이트 시장을 독점하는 것으로 보여지고 있습니다.

액정 폴리머(LCP) 필름 및 라미네이트 산업 개요

액정 폴리머(LCP) 필름 및 라미네이트 시장은 그 특성상 부분적으로 통합되어 있습니다. 시장의 주요 기업으로는 Celanese Corporation, Kuraray, Polyplastics, Sumitomo Chemical Advanced Technologies, Shanghai PERT Composites, UENO FINE CHEMICALS INDUSTRY LTD 등이 있습니다.

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트·지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

전기 및 전자부품의 소형화 수요 증가

자동차 부품의 경량화 재료의 개발

기타 촉진요인

억제요인

높은 제조 및 가공 비용

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

유형

LCP 필름

LCP 라미네이트

용도

자동차 및 수송

일렉트로닉스

의료기기

기타 용도(산업기계, 포장 등)

지역

아시아태평양

중국

인도

일본

한국

인도네시아

말레이시아

태국

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

러시아

터키

북유럽 국가

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율(%)**/랭킹 분석

주요 기업의 전략

기업 프로파일

Celanese Corporation

KGK Chemical Corporation

KURARAY CO. LTD.

Panasonic Industry Co., Ltd.

Polyplastics Co. Ltd.

Rogers Corporation

RTP Company

Sumitomo Chemical Advanced Technologies

Syensqo

Toray Industries Inc.

UENO FINE CHEMICALS INDUSTRY LTD.

제7장 시장 기회와 앞으로의 동향

ASEAN과 인도의 일렉트로닉스 시장에서의 성장 가능성

기타 기회

JHS

영문 목차

영문목차

The Liquid Crystal Polymer Films And Laminates Market size is estimated at 9.22 kilotons in 2025, and is expected to reach 12.05 kilotons by 2030, at a CAGR of greater than 5.5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the liquid crystal polymer (LCP) films & laminates market. The nationwide lockdowns and strict social distancing measures had resulted in a halt in the manufacturing activities of various electronics, thereby affecting the market for liquid crystal polymer (LCP) films & laminates.

However, the market has recovered significantly since then, owing to the rising demand for liquid crystal polymer (LCP) films & laminates in electronics, automotive, and packaging applications.

Key Highlights

The increasing demand for miniaturization of electrical and electronic components and the development of lightweight materials for automobile components are expected to increase demand for the studied market.

The high manufacturing and processing costs of liquid crystal polymer (LCP) films and laminates are expected to hinder the market's growth.

The potential growth in the ASEAN and India electronics market is expected to create opportunities for the market during the forecast period.

Asia-Pacific region represents the largest market and is also expected to be the fastest-growing market over the forecast period, owing to the increasing consumption from countries such as China, India, and ASEAN countries.

Liquid Crystal Polymer (LCP) Films & Laminates Market Trends

Electronics Application Segment to Dominate The Market

Liquid crystal polymers (LCP) and laminates have widened their application scope across the electronics industry. LCP films offer excellent electrical and mechanical properties, such as a low dielectric constant, high moisture barriers, a controllable thermal coefficient of expansion, high-frequency properties, and non-halogen flame-retardant characteristics.

The spread of telework and stay-at-home demand drove up the demand for electronic equipment. Solution services grew as more investments in digitalization promoted more sophisticated data use. Thus, the demand for LCP films and laminates used in the electronics segment is expected to increase.

The global electronics industry registered a significant growth rate. According to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was valued at USD 3.43 trillion in 2022, registering a growth rate of 1% year on year, compared to USD 3.36 trillion in 2021. Moreover, the industry is expected to reach USD 3.52 trillion, with a growth rate of 3% year on year, by 2023.

Asia-Pacific accounts for more than 70% of global electronics production. Countries like South Korea, Japan, and China manufacture electrical components and supply them to various industries globally. Additionally, India is expected to become the world's fifth-largest consumer electronics and appliances industry by 2025.

India's electronics system design and manufacturing (ESDM) sector is expected to generate over USD 100 billion in economic value by 2025. Electrical and electronics production in India is expected to increase rapidly due to government initiatives with policies, such as Make in India, National Policy of Electronics, and Net Zero Imports in Electronics, which offer a commitment to growth in domestic manufacturing. The growing electronics industry is expected to drive the current studied market.

Similarly, in Europe, the German electronics industry registered a significant growth rate. According to the ZVEI, Germany's electro and digital industry turnover accounted for USD 243.5 billion (EUR 224.5 billion) in 2022 as compared to the USD 216.9 billion ( EUR 200 billion) turnover registered in the previous year. Thus, the growth in the electronics industry is expected to drive the market demand for Liquid Crystal Polymer (LCP) Films and laminates in the country.

Owing to all these factors, the electronics application segment is expected to dominate the market for liquid crystal polymer (LCP) films & laminates during the forecast period.

Asia-Pacific Region to Dominate the Market

Asia-Pacific region is expected to dominate the market for liquid crystal polymer (LCP) films & laminates during the forecast period. The rising demand for liquid crystal polymer (LCP) films & laminates is rising from the electronics and automotive industries in China, Japan, and India.

In countries like China and Japan, the electronics industry has registered a significant growth rate, thereby driving the market for silicone coatings. The Chinese electronics market increased by 13% in 2022 compared to 2021, when the market saw a 10% rise. The estimated growth rate for 2023 is 7%.

Japan is home to the world's largest electronics companies and enjoys a significant share in the production of various electronic equipment and devices. According to the Japan Electronics and Information Technology Industries Association (JEITA), in 2022, the total production value of the electronics industry in Japan amounted to around USD 74.3 billion (JPY 11,124.3 billion), showcasing a rise of nearly 8% from the previous year.

Furthermore, the demand for liquid crystal polymer (LCP) films & laminates is increasing in the automotive and transportation industries. India has become the second-largest automotive vehicle manufacturer in the region. According to OICA, the total production volume of automotive vehicles reached 5.45 million units in 2022, indicating a growth of 24% as compared to 4.39 million units registered in 2021. Thus, the increasing production volume of automotive vehicles is anticipated to drive the current studied market.

Liquid crystal polymer (LCP) films also find applications in the packaging industry. In March 2022, TCPL Packaging Ltd. doubled its flexible packaging plant capacity, which has now gone into commercial production. The company also expanded offset capacity by adding a new production line at the Goa plant. With these capacity expansions, market players are also poised to manage the expected higher demand.

Due to all such factors, the Asia-Pacific region is expected to dominate the market for liquid crystal polymer (LCP) films and laminates during the forecast period.

Liquid Crystal Polymer (LCP) Films and Laminates Industry Overview

The liquid crystal polymer (LCP) films and laminates market is partially consolidated in nature. Some of the major players in the market include (not in any particular order) Celanese Corporation, KURARAY CO. LTD., Polyplastics Co. Ltd., Sumitomo Chemical Advanced Technologies, Shanghai PERT Composites Co. Ltd, and UENO FINE CHEMICALS INDUSTRY LTD, amongst others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand for Miniaturization of Electrical and Electronic Components

4.1.2 Development of Lightweight Materials for Automobile Components

4.1.3 Other Drivers

4.2 Restraints

4.2.1 High Manufacturing and Processing Costs

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Type

5.1.1 LCP Films

5.1.2 LCP Laminates

5.2 Application

5.2.1 Automotive and Transportation

5.2.2 Electronics

5.2.3 Medical Devices

5.2.4 Other Applications (Industrial Machinery, Packaging, etc.)

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Indonesia

5.3.1.6 Malaysia

5.3.1.7 Thailand

5.3.1.8 Vietnam

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Spain

5.3.3.6 Russia

5.3.3.7 Turkey

5.3.3.8 NORDIC Countries

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Celanese Corporation

6.4.2 KGK Chemical Corporation

6.4.3 KURARAY CO. LTD.

6.4.4 Panasonic Industry Co., Ltd.

6.4.5 Polyplastics Co. Ltd.

6.4.6 Rogers Corporation

6.4.7 RTP Company

6.4.8 Sumitomo Chemical Advanced Technologies

6.4.9 Syensqo

6.4.10 Toray Industries Inc.

6.4.11 UENO FINE CHEMICALS INDUSTRY LTD.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Potential in Growth in ASEAN and India Electronics Market