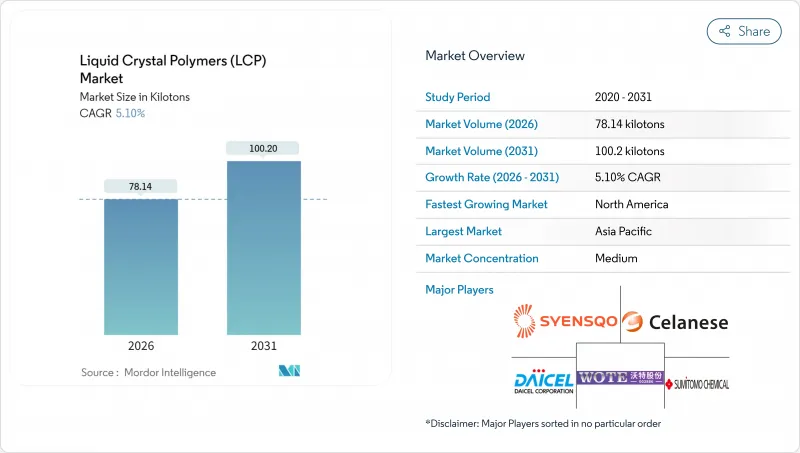

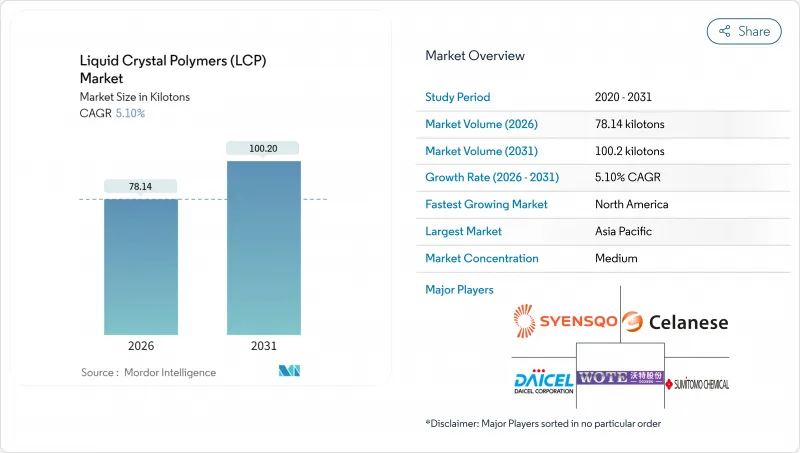

액정폴리머(LCP) 시장은 2025년 74.35킬로톤에서 2026년에는 78.14킬로톤으로 성장할 전망입니다. 2026-2031년에 걸쳐 CAGR 5.10%의 성장이 예상되며, 2031년까지 100.2킬로톤에 달할 것으로 예측되고 있습니다.

이러한 상승 곡선은 세 가지 상호 연결된 기둥에 기반합니다. 5G 네트워크 하드웨어의 꾸준한 보급, 배터리 전기차로의 가속화되는 전환, 그리고 고주파 전자 어셈블리의 소형화를 위한 업계 전반의 추진입니다. 이러한 최종 용도 각각은 열 응력 하에서 치수 정확도를 유지하고, 밀리미터파 주파수에서 무시할 만한 전기적 손실을 보이며, 긴 수명 동안 기계적 무결성을 유지하는 폴리머를 요구합니다. 가격보다 물량이 채택을 결정하는 이유는 설계 엔지니어들이 주로 낮은 유전율, 낮은 손실률, 우수한 내습성을 위해 LCP 등급을 선택하기 때문입니다. 이러한 배경 속에서 액정폴리머 시장은 차세대 안테나 모듈, 고전압 인버터 패키지, 유연한 고밀도 상호 연결을 위한 핵심 소재로 부상했습니다. 특수 이산 및 이올의 안정적인 원료 공급을 확보할 수 있는 기업들은 다운스트림 수요 증가에 따라 대규모 물량을 확보할 수 있는 입지를 구축하고 있습니다.

광대역 안테나 연구에 따르면 LCP 기판은 밀리미터파 주파수에서 유전율 3.5 미만, 손실 탄젠트 0.004 미만을 유지하여 28GHz 기지국용 소형 어레이 요소를 신호 저하 없이 구현합니다. 이 소재는 기계 방향 수축률이 0.05%로 낮아 다중입력 다중출력(MIMO) 빔 포밍에 사용되는 미세 회로에서 임피던스 제어를 유지합니다. 폴리플라스틱스는 2025년까지 중합 생산 능력을 25,000톤으로 확대하여, 중국이 70만 개의 신규 5G 기지국을 추가하고 미국 사업자들이 기존 사이트를 개조함에 따라 휴대폰 및 인프라 수요를 충족시킬 계획입니다. 유전체 허용오차가 엄격함에도 불구하고, 기존 사출 장비의 비용 효율적인 가공은 액정폴리머 시장을 대량 생산 라디오 모듈에 매력적으로 유지합니다. 이로 인한 생태계는 6G 대비 성능 범위를 목표로 하는 OEM(원본 장비 제조업체)의 설계 유연성을 강화합니다.

열변성 등급은 구리 버스바의 0.1-2.0 X 10-5/°C 열팽창 계수와 일치하여 800V 인버터에서 솔더 접합부를 열화시키는 전단 응력을 제거합니다. 에너지 변환 연구에 따르면 LCP 냉각판은 200A 충전 속도에서 배터리 모듈 전체에 걸쳐 ±2°C 온도 균일성을 유지하면서 36%의 중량 절감을 달성합니다. 셀라네즈는 -40-150°C 사이 3,000회 열 사이클을 변형 없이 견디는 초고유동성 변형체를 소형 보드-투-보드 커넥터용으로 출시했습니다. 자동차 제조사들의 탄소 크레딧 전략은 부품 경량화를 장려하여 액정폴리머 시장을 후드 내 센서에서 트랙션 전압 어셈블리로 확장시키고 있습니다. 공급 계약은 이제 OEM의 순환성 목표를 충족시키기 위해 설계 지원 및 재생재 회수 옵션을 묶어 제공합니다.

폴리페닐렌 설파이드(PPS)는 250°C 연속 사용이 가능하며 원자재 비용이 35-50% 낮아, 소비자 가전 분야에서 일반 커넥터가 LCP를 대체하고 있습니다. 자동차 1차 공급업체들은 절연 성능이 필수적이지 않은 비중요 하우징의 경우 고온 나일론으로 전환하는 이중 금형 전략을 협의 중입니다. LCP 사출 설비는 ±2°C 배럴 제어와 300°C 이상의 금형 온도를 요구하여 에너지 소비와 사이클 타임 비용을 증가시켜 신흥 경제국의 채택을 저해합니다. 최근 바이오 기반 변종은 프리미엄을 8-10% 좁혔으나, 대량 생산 부품에 대한 가격 평준화는 여전히 요원합니다. 이 비용 격차는 액정폴리머 시장의 일반 전자제품 시장으로의 광범위한 침투를 계속해서 지연시키고 있습니다.

열변성 등급은 2025년 생산량의 92.58%를 차지하며, 확고한 공급망과 기존 용융 가공 장비와의 호환성을 입증했습니다. 이 소재들은 280-340°C에서 유동성을 유지하면서도 결정 구조를 보존하여 내재적 난연성을 제공하며, 초박형 커넥터에서 할로겐 첨가제의 사용을 불필요하게 합니다. 3.2 미만의 일관된 등방성 유전율 값으로 열가소성 LCP는 아시아태평양 지역 5G 스마트폰 안테나 기판의 선호 소재입니다. 2025년 셀라네즈가 UL 94 V-0 등급을 유지한 60% 바이오 함량 변형을 출시하며 지속가능성이 주목받았습니다. 용융성 LCP는 부피 기준 7.42%에 불과하지만, 항공우주 복합재가 3.2GPa 이상의 인장 강도를 가진 용액 방사 섬유를 요구함에 따라 7.12%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 제조업체들은 운영 비용 절감을 위해 용매 회수 장치에 투자하고 있지만, 자본 지출(CAPEX) 장벽으로 인해 용융성 생산 능력은 소수의 통합 생산 업체로 제한됩니다. 3D 프린팅 레이돔용 리오트로픽 필라멘트에 대한 첨가제 제조업체의 인증이 진행됨에 따라, 이 하위 부문의 액정폴리머 시장 규모는 특히 방위 플랫폼 분야에서 확대될 것으로 예상됩니다.

본 액정폴리머(LCP) 보고서는 제품 유형별(열가소성 LCP 및 용융성 LCP), 최종 사용자 산업별(항공우주, 자동차, 전기 및 전자, 산업, 기계, 기타 최종 사용자 산업), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 예측은 수량(톤) 및 금액(달러)으로 제공됩니다.

아시아태평양 지역은 중합부터 완제품 모듈까지 리드 타임을 단축하는 전용 전자 생태계의 지원으로 2025년 가치의 72.45%를 차지하며 선도적 위치를 유지했습니다. 중국의 5G 기지국 구축에 대한 정부 보조금은 안정적인 수요를 보장하는 반면, 일본의 자동차 부품 공급업체들은 무결점 기준을 충족하기 위해 레이더 커넥터에 LCP를 계속해서 지정하고 있습니다. 닝보 주변의 생산 클러스터는 항구와의 근접성으로 혜택을 받아 유럽 휴대폰 제조사에 공급하는 수출업체들의 물류 비용을 절감합니다.

북미는 2031년까지 5.98%라는 가장 빠른 CAGR을 기록했습니다. 이는 무선 통신 사업자가 중대역 스펙트럼을 저손실 기판이 필요한 대규모 MIMO 어레이로 업그레이드했기 때문입니다. Sumitomo Chemical이 2025년 Syensqo의 Nate 수지 자산을 인수했을 때 텍사스 주 파일럿 라인도 포함되어 방위 전자 기기를 위한 국내 공급 안보를 강화했습니다. 항공우주 주요 제조업체는 이러한 현지 조달원을 활용하여 항공전자기기에서 알루미늄 EMI 실드의 LCP 대체품의 인정을 추진하고 있습니다. 이는 정부의 지원을 받은 국내 회귀 정책과도 일치하는 움직임입니다.

유럽은 수소 환경에서 LCP의 화학적 내구성을 중시하는 연료전지 스택 개발사들에 힘입어 중간 단일자리 수 성장률을 유지했습니다. 자동차 OEM 업체들은 EU(유럽연합) 규정 2019/631에 따른 2027년 CO2 차량 배출 목표를 충족하기 위해 800V 인버터 설계에 LCP 헤더 플레이트를 적용하고 있습니다. 헝가리와 스웨덴에 건설된 기가팩토리들은 고전압 배터리 케이스용 증산 능력을 시사하며, 이로 인해 액정 폴리머 시장에 대한 지역적 수요가 확대되고 있습니다.

The Liquid Crystal Polymers Market is expected to grow from 74.35 kilotons in 2025 to 78.14 kilotons in 2026 and is forecast to reach 100.2 kilotons by 2031 at 5.10% CAGR over 2026-2031.

This upward curve rests on three interconnected pillars: the steady roll-out of 5G network hardware, the accelerating shift toward battery-electric vehicles, and the industry-wide drive to miniaturize high-frequency electronic assemblies. Each of these end-uses requires polymers that maintain dimensional accuracy under thermal stress, exhibit negligible electrical loss at millimeter-wave frequencies, and retain mechanical integrity over long service lives. Volume rather than price determines adoption, because design engineers primarily choose LCP grades for their low dielectric constants, low dissipation factors, and excellent moisture resistance. Against that backdrop, the liquid crystal polymer market has become a critical input for next-generation antenna modules, high-voltage inverter packages, and flexible high-density interconnects. Firms able to secure reliable feedstocks of specialty diacids and diols position themselves to capture outsized volumes as downstream demand rises.

Wideband antenna studies show that LCP substrates sustain dielectric constants below 3.5 and loss tangents under 0.004 at mmWave frequencies, enabling compact array elements for 28 GHz base stations without signal degradation. The material exhibits machine-direction shrinkage as low as 0.05%, maintaining impedance control in fine-line circuits used for Multiple-Input and Multiple-Output (MIMO) beam-forming. Polyplastics lifted polymerization capacity to 25,000 tons in 2025 to satisfy handset and infrastructure demand as China adds 700,000 new 5G base stations and United States operators retrofit legacy sites. Despite tight dielectric tolerances, cost-effective processing on conventional injection equipment keeps the liquid crystal polymer market attractive for high-volume radio modules. The resulting ecosystem strengthens design flexibility for original equipment manufacturers (OEMs) targeting 6G-ready performance envelopes.

Thermotropic grades match the 0.1-2.0 X 10-5/°C coefficient of thermal expansion of copper busbars, eliminating shear stress that degrades solder joints in 800 V inverters. Energy-conversion research confirms that LCP cooling plates achieve a 36% weight saving while maintaining +-2°C temperature uniformity across battery modules at 200 A charge rates. Celanese introduced ultra-high-flow variants for miniature board-to-board connectors that survive 3,000 thermal cycles between -40°C and 150°C without warpage. Automakers' carbon-credit strategies reward component light-weighting, expanding the liquid crystal polymer market beyond under-hood sensors into traction voltage assemblies. Supply agreements now bundle design support and recyclate take-back options to satisfy OEM circularity targets.

Polyphenylene sulfide delivers 250°C continuous service at 35-50% lower raw-material cost, steering commodity connectors away from LCP in consumer electronics. Automotive Tier 1 suppliers negotiate dual-tooling strategies so that non-critical housings default to high-temperature nylons when dielectric performance is non-essential. Injection setups for LCP require +-2°C barrel control and mold temperatures above 300°C, raising energy consumption and cycle-time costs, discouraging adoption in emerging economies. Recent bio-based variants narrow the premium by 8-10%, yet price parity remains distant for high-volume parts. This cost gap continues to slow the broader penetration of the liquid crystal polymer market into commodity electronics.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Thermotropic grades accounted for 92.58% of 2025 volume, underscoring their entrenched supply chains and compatibility with conventional melt-processing equipment. These materials flow at 280-340°C yet retain their crystalline order, yielding inherent flame retardancy and eliminating the need for halogen additives in ultrathin connectors. Consistent isotropic dielectric values below 3.2 make thermotropic LCPs the preferred choice for antenna substrates in 5G smartphones across the Asia-Pacific region. Sustainability gained momentum in 2025 when Celanese introduced a 60% bio-content variant that did not compromise its UL 94 V-0 ratings. Lyotropic LCP, though only 7.42% by volume, benefits from a 7.12% CAGR as aerospace composites demand solution-spun fibers with tensile strengths above 3.2 GPa. Manufacturers invest in solvent recovery units to reduce operating costs, but CAPEX hurdles limit lyotropic capacity to a handful of integrated producers. As additive manufacturers qualify lyotropic filaments for 3D-printed radomes, the liquid crystal polymer market size in this sub-segment is expected to expand, particularly in defense platforms.

The Liquid Crystal Polymer Report is Segmented by Product Type (Thermotropic LCP and Lyotropic LCP), End-User Industry (Aerospace, Automotive, Electrical and Electronics, Industrial and Machinery, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

The Asia-Pacific region retained its leadership position, accounting for 72.45% of the 2025 value, bolstered by dedicated electronics ecosystems that compress lead times from polymerization to finished modules. Government subsidies in China for 5G base-station roll-outs ensure stable offtake, while Japan's automotive tier suppliers continue to specify LCP in radar connectors to meet zero-defect mandates. Production clusters around Ningbo benefit from port proximity, cutting logistics costs for exporters serving European handset makers.

North America posted the fastest 5.98% CAGR to 2031 as wireless carriers upgraded mid-band spectrum with massive MIMO arrays that require low-loss substrates. Sumitomo Chemical's 2025 acquisition of Syensqo's neat-resin assets included pilot lines in Texas, reinforcing domestic supply security for defense electronics. Aerospace primes leverage these local sources to qualify LCP replacements for aluminum EMI shields in avionics, aligning with stimulus-backed on-shoring agendas.

Europe maintained mid-single-digit growth, driven by fuel-cell stack developers that value LCP's chemical resilience in hydrogen environments. Automotive OEMs incorporate LCP header plates in 800 V inverter designs to meet 2027 CO2 fleet targets under EU (European Union) Regulation 2019/631. Deployment of gigafactories in Hungary and Sweden signals incremental capacity for high-voltage battery enclosures, widening regional demand for the liquid crystal polymer market.