일렉트로그로믹 및 액정 폴리머 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Electrochromic and Liquid Crystal Polymer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1750286

리서치사:Global Market Insights Inc.

발행일:2025년 05월

페이지 정보:영문 300 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

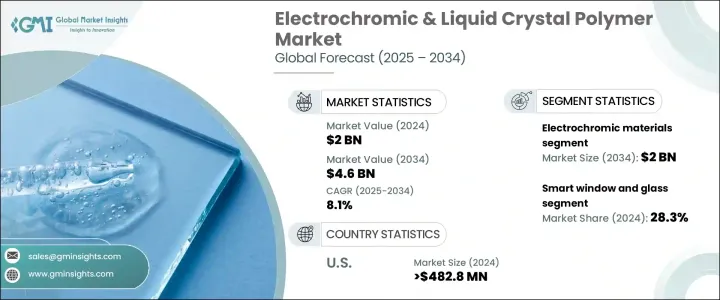

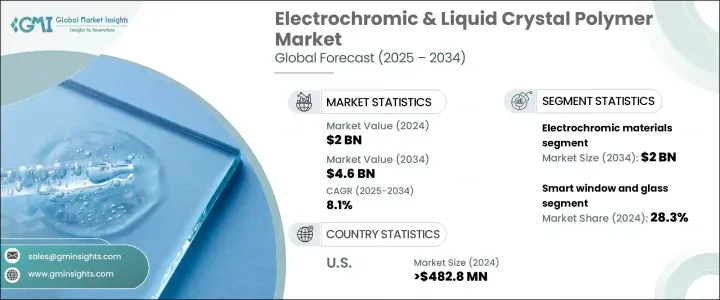

세계의 일렉트로그로믹 및 액정 폴리머 시장은 2024년 20억 달러로 평가되었으며, 자동차와 건축 등 산업에서 에너지 효율적인 솔루션에 대한 수요가 증가함에 따라 CAGR 8.1%로 성장해 2034년까지 46억 달러에 이를 것으로 추정되고 있습니다.

전기 신호에 반응하여 광학 특성을 변화시키는 일렉트로크로믹 재료는 첨단 창 기술에 필수적입니다. 에너지 관리를 개선하고 온실가스 배출량을 줄이기 위한 세계의 노력과 일치하며, 공조의 필요성을 줄이는데 도움이 됩니다.

자동차 분야에서는 드라이버의 쾌적성과 안전성을 높이기 위해, 백미러나 선루프에 일렉트로크로믹 재료가 사용되고 있습니다. 또, ADAS(첨단 운전 지원 시스템)나 자율 주행 기술의 진화에도 공헌하고 있습니다. 일렉트로크로믹 재료는 차내의 온도를 최적으로 유지해, 에너지 절약에 공헌합니다. 액정 폴리머 제품 수요 증가는 고성능 재료가 필요한 통신이나 일렉트로닉스 산업에도 뒷받침되고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

20억 달러

예측 금액

46억 달러

CAGR

8.1%

일렉트로크로믹 재료 분야는 2024년 9억 150만 달러의 매출을 계상했습니다.이러한 재료는 에너지 효율이 높고, 기능적, 심미적인 환경에서 다양한 용도에 이상적입니다.

스마트 창과 유리는 최대 응용 분야이며 28.3%의 점유율을 차지합니다.이 창은 빛과 열의 통과를 자동으로 조정할 수 있으므로 에너지 효율적인 건물과 자동차에 대한 수요 증가가 이 동향을 뒷받침합니다. 결과적으로 인공 조명과 에어컨에 대한 의존도가 떨어집니다. 일렉트로크로믹 장치와 액정 장치를 스마트 창에 통합하면 세계의 지속가능성 목표를 달성하는 데 기여하는 동시에 고급 주택과 상업용 부동산의 편안함과 프라이버시가 향상됩니다.

미국 일렉트로그로믹 및 액정 폴리머 시장 규모는 2024년 4억 8,280만 달러였습니다. 이 창은 에너지 소비를 약 20% 삭감할 수 있기 때문에 이산화탄소 배출량의 삭감에 공헌하고 지속 가능한 에너지 솔루션으로의 이행을 지원하고 있습니다.

Toray Industries, Sumitomo Chemical Company, Solvay, Saint-Gobain, AGC 등 이 업계의 기업은 R&D에 투자하여 시장 점유율을 확대하는 데 주력하고 있습니다. 다양한 산업에서 증가하는 수요에 부응하고 있습니다. 각 회사는 또한 건축 계약자 및 자동차 제조업체와 전략적 파트너십을 연결하여 새로운 건축물과 자동차 모델에 이러한 첨단 재료가 널리 채택되도록 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

시장 소개

트럼프 정권에 의한 관세에 대한 영향

무역에 미치는 영향

무역량의 혼란

보복 조치

업계에 미치는 영향

공급측의 영향(원재료)

주요 원재료의 가격 변동

공급망 재구성

생산 비용에 미치는 영향

수요측의 영향(판매가격)

최종 시장에의 가격 전달

시장 점유율 동향

소비자의 반응 패턴

영향을 받는 주요 기업

전략적인 업계 대응

공급망 재구성

가격 설정 및 제품 전략

정책관여

전망과 향후 검토 사항

무역 통계(HS코드)

주요 수출국, 2021-2024

주요 수입국, 2021-2024

업계 밸류체인 분석

기술 개요

일렉트로크로믹 재료

액정 폴리머

폴리머 분산 액정(PDLC)

기술의 비교 분석

시장 역학

시장 성장 촉진요인

시장 성장 억제요인

시장 기회

시장의 과제

업계에 미치는 영향요인

성장 가능성 분석

업계의 잠재적 위험 및 과제

규제 프레임워크과 기준

일렉트로크로믹 디바이스의 ASTM 규격

에너지 효율 규제

건축 기준법과 인증

자동차 업계의 표준

제조 공정 분석

일렉트로크로믹 재료의 제조

액정 폴리머 합성

디바이스 제조 기술

원재료 분석 및 조달 전략

가격 분석

지속가능성과 환경영향 평가

PESTEL 분석

Porter's Five Forces 분석

제4장 경쟁 구도

시장 점유율 분석

전략 틀

합병과 인수

합작투자와 콜라보레이션

신제품 개발

확대 전략

경쟁 벤치마킹

벤더 상황

경쟁 포지셔닝 매트릭스

전략적 대시보드

기술 도입 및 혁신 평가

신규 참가자 시장 진출 전략

제5장 시장 규모와 예측 : 기술별, 2021-2034년

주요 동향

일렉트로크로믹 재료

무기 일렉트로크로믹 재료

유기 일렉트로크로믹 재료

하이브리드 일렉트로크로믹 재료

액정 폴리머(LCP)

서모트로픽 LCPS

리오트로픽 LCPS

폴리머 분산 액정(PDLC)

통상 모드 PDLC

리버스 모드 PDLC

부유 입자 장치(SPD)

기타

제6장 시장 규모와 예측 : 용도별, 2021-2034년

주요 동향

스마트 윈도우와 유리

건축용 창

자동차 창문 및 선루프

항공기 창

선박의 창

전자부품

커넥터

회로 기판

안테나

마이크로 일렉트로닉스 패키지

디스플레이와 시각장치

스마트 디스플레이

웨어러블 디스플레이

표지판 및 정보 표시

자동차 부품

미러

조명 시스템

센서 및 컨트롤

구조 부품

의료기기

항공우주 및 방위용도

기타

제7장 시장 규모와 예측 : 최종 용도 산업별, 2021-2034년

주요 동향

건설 및 아키텍처

주택

상업 빌딩

공공시설

산업시설

자동차 및 운송

승용차

상용차

전기자동차

철도 및 대중교통기관

일렉트로닉스 및 통신

가전

통신 기기

컴퓨팅 및 IT 하드웨어

5G 인프라

항공우주 및 방어

헬스케어 및 의료

에너지와 발전

기타

제8장 시장 규모와 예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

한국

호주

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

Saint-Gobain

AGC

Gentex Corporation

Gauzy

Halio

ChromoGenics

Polytronix

Research Frontiers

Celanese Corporation

Solvay

Toray Industries

Sumitomo Chemical Company

Kuraray

Murata Manufacturing

Chiyoda Integre

RTP Company

SABIC

Ynvisible Interactive

Crown Electrokinetics

Smart Glass Group

Smart Films International

Corning Incorporated

Continental

Panasonic Holdings Corporation

JHS

영문 목차

영문목차

The Global Electrochromic and Liquid Crystal Polymer Market was valued at USD 2 billion in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 4.6 billion by 2034, driven by the increasing demand for energy-efficient solutions in industries like automotive and construction. Electrochromic materials, which change their optical properties in response to electrical signals, are essential for advanced window technologies. Smart windows are crucial in vehicles and buildings, enabling energy optimization by managing solar energy absorption and minimizing glare. This helps reduce the need for air conditioning, aligning with global efforts to improve energy management and lower greenhouse gas emissions. As industries seek to incorporate more sustainable technologies, the role of electrochromic materials continues to expand in improving energy efficiency.

In the automotive sector, these materials are used in rearview mirrors and sunroofs to enhance driver comfort and safety. They also contribute to the evolution of advanced driver-assistance systems (ADAS) and autonomous driving technologies. Electrochromic materials help maintain an optimal temperature inside vehicles, contributing to energy savings. The increasing demand for liquid crystal polymer products is also fueled by the telecommunications and electronics industries, where high-performance materials are required.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$2 Billion

Forecast Value

$4.6 Billion

CAGR

8.1%

The electrochromic materials segment generated USD 901.5 million in 2024, attributed to the materials' versatility in changing colors or transparency when voltage is applied, allowing them to control heat and light passage through windows, mirrors, and displays. These materials are highly energy-efficient, making them ideal for various applications in both functional and aesthetic settings. The development of more sophisticated technology, such as PDLC (polymer-dispersed liquid crystal), further enhances the market's potential by offering more color options and increased energy efficiency.

Smart windows and glass hold the largest application segment, representing 28.3% share. The increasing demand for energy-efficient buildings and vehicles has driven this trend, as these windows are capable of automatically regulating light and heat passage. This results in reduced reliance on artificial lighting and air conditioning. The integration of electrochromic or liquid crystal devices in smart windows helps meet global sustainability goals while also improving comfort and privacy in high-end residential and commercial real estate.

United States Electrochromic and Liquid Crystal Polymer Market generated USD 482.8 million in 2024. Government incentives like tax credits for installing smart glass have played a key role in promoting the adoption of electrochromic windows in commercial and residential buildings. These windows can reduce energy consumption by approximately 20%, contributing to reducing carbon emissions and supporting the transition toward sustainable energy solutions.

Companies in this industry, such as Toray Industries, Sumitomo Chemical Company, Solvay, Saint-Gobain, and AGC, focus on expanding their market share by investing in research and development. They are working on enhancing the performance and affordability of electrochromic products to meet the growing demand across various industries. Companies are also forging strategic partnerships with building contractors and vehicle manufacturers to ensure widespread adoption of these advanced materials in new constructions and vehicle models.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Report scope and objectives

1.2 Research design and approach

1.3 Data collection methods

1.3.1 Primary research

1.3.2 Secondary research

1.4 Market estimation and forecasting methodology

1.5 Assumptions and limitations

1.6 Data validation and triangulation techniques

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

3.1 Market Introduction

3.2 Trump administration tariffs

3.2.1 Impact on trade

3.2.1.1 Trade volume disruptions

3.2.1.2 Retaliatory measures

3.2.2 Impact on the industry

3.2.2.1 Supply-side impact (raw materials)

3.2.2.1.1 Price volatility in key materials

3.2.2.1.2 Supply chain restructuring

3.2.2.1.3 Production cost implications

3.2.2.2 Demand-side impact (selling price)

3.2.2.2.1 Price transmission to end markets

3.2.2.2.2 Market share dynamics

3.2.2.2.3 Consumer response patterns

3.2.3 Key companies impacted

3.2.4 Strategic industry responses

3.2.4.1 Supply chain reconfiguration

3.2.4.2 Pricing and product strategies

3.2.4.3 Policy engagement

3.2.5 Outlook and future considerations

3.3 Trade statistics (HS Code)

3.3.1 Major exporting countries, 2021-2024 (USD Mn)

3.3.2 Major importing countries, 2021-2024 (USD Mn)

3.4 Industry value chain analysis

3.5 Technology overview

3.5.1 Electrochromic materials

3.5.2 Liquid crystal polymers

3.5.3 Polymer dispersed liquid crystals (PDLC)

3.5.4 Comparative analysis of technologies

3.6 Market dynamics

3.6.1 Market drivers

3.6.2 Market restraints

3.6.3 Market opportunities

3.6.4 Market challenges

3.7 Industry impact forces

3.7.1 Growth potential analysis

3.7.2 Industry pitfalls & challenges

3.8 Regulatory framework & standards

3.8.1 ASTM standards for electrochromic devices

3.8.2 Energy efficiency regulations

3.8.3 Building codes & certifications

3.8.4 Automotive industry standards

3.9 Manufacturing process analysis

3.9.1 Electrochromic materials production

3.9.2 Liquid crystal polymer synthesis

3.9.3 Device fabrication techniques

3.10 Raw material analysis & procurement strategies