미국의 플라스틱 뚜껑 및 마개 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

United States (US) Plastic Caps and Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1689891

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

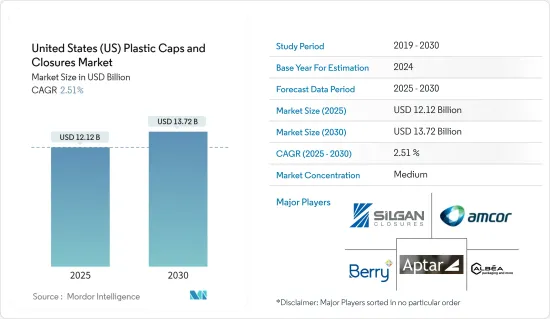

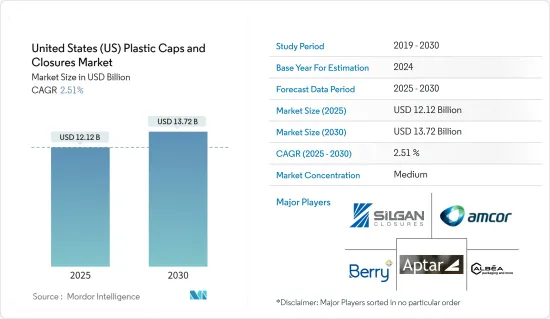

미국의 플라스틱 뚜껑 및 마개 시장 규모는 2025년 121억 2,000만 달러에 이를 것으로 예상되고 예측 기간(2025-2030년)의 CAGR은 2.51%를 나타내 2030년에는 137억 2,000만 달러에 달할 것으로 전망됩니다.

주요 하이라이트

플라스틱 뚜껑 및 마개는 PP와 PE를 주원료로 제조됩니다. 산업계는 이러한 재료에 크게 의존하고 있으며, 비용 효율적인 밀봉 솔루션을 제공합니다.

마찬가지로 소비자들 사이에서 건강 지향이 높아지는 가운데 포장 음료와 의약품 수요가 급증하고 뚜껑 및 마개 시장을 뒷받침하고 있습니다.

특히 2023년 Beverage Marketing Corporation과 International Bottled Water Association은 미국에서 가장 많이 소비되는 음료는 병 워터라고 보고했습니다. 구체적으로는 2023년의 병이 들어간 식수 시장은 0.4% 증가와 2022년의 1.1% 증가로부터 둔화해, 2021년과 2020년에 각각 관측된 4.6%와 4.1%의 강력한 성장률로부터 대폭 저하되었습니다.

또한 미국 고객들 사이에서 식수 수요가 증가하고 있는 것도 플라스틱 뚜껑 및 마개 시장을 뒷받침하고 있습니다. 불가결합니다.물의 오염이나 안전성에 대한 우려에 대한 의식의 고조가 병들이 식수 수요를 밀어 올리고 있어, 이 동향은 예측 기간 중에도 계속될 것으로 예상되기 때문에 시장 전체에서 플라스틱 뚜껑 수요가 급증할 가능성이 있습니다.

원재료 가격은 플라스틱 뚜껑 및 마개의 비용에 직접 영향을 미칩니다. 는 특히 제조업체가 코스트 증가를 고객에게 전가할 수 없는 경우, 이익률을 압박할 가능성이 있습니다.

미국 플라스틱 뚜껑 및 마개 시장 동향

폴리에틸렌(PE)이 가장 급성장하는 원료 부문이 될 전망

폴리에틸렌(PE)은 가장 내구성 있는 플라스틱 중 하나로 화학약품에 강하고 저비용입니다.

HDPE와 LDPE는 뚜껑과 마개에 사용되는 주요 재료입니다. 강도와 내구성으로 유명한 HDPE 플라스틱은 컬러 매치가 가능해, 일반적으로 백색을 볼 수 있습니다.그 적응성과 내구성에 의해 HDPE는 화장품용 병의 가장 유력한 선택지가 되고 있습니다.

볼레아리스는 HDPE 뚜껑과 마개의 성장은 유리병의 금속 뚜껑이(PET제에) 대체해진 것과, 간식용의 소형 병을 좋아하는 소비 패턴의 변화에 크게 기인하고 있다고 지적하고 있습니다.

미국 화학공업협회에 따르면 2023년에는 미국에서 HDPE, LDPE, LLDPE를 포함한 70억 5,000만 파운드의 폴리에틸렌이 생산되었습니다.

그 강도와 비용 효율이 높기 때문에 미국의 많은 산업에서는 LDPE보다 HDPE가 선호되고 있습니다.

미국의 플라스틱 뚜껑 및 마개 시장은 폴리에틸렌 산업의 수출 이니셔티브에 전략적 중점을 두고 있기 때문에 현저한 성장을 보여주고 있습니다. 미국 상무부의 데이터에 따르면, 2023년 1분기의 미국 PE 수출 출하량은 전년 대비 30% 증가한 3조 1,964억 3,700만 톤(70억 5,000만 파운드)이었습니다.

음료 분야가 큰 시장 점유율을 차지할 전망

뚜껑 및 마개는 탄산음료와 비탄산음료를 포함한 음료산업에 있어서 용기, 파우치, 병을 밀봉하는 데 있어서 매우 중요합니다.

싱글서브 음료 수요 증가와 포장 음료의 유통기한을 연장하는 핫필 프로세스가 함께 미국 뚜껑 및 마개 시장의 성장을 가속할 것으로 보입니다. 건강 지수를 높이기 위해 기업은 핫필 프로세스를 선호하고 있습니다.

다양한 핫필 공정이 음료 업계에서 일반적이 됨에 따라, 핫필 플라스틱 병은 점점 보급되고 있습니다.

스포츠 뚜껑 시장은 병들이 식수나 에너지 드링크 수요 증가와 함께 확대하고 있습니다. 스포츠 뚜껑은 중량이 있음에도 불구하고, 개조 방지 기능을 갖추고 있습니다. 음료 다이제스트에 따르면 2023년 미국 탄산음료(CSD) 시장에서 코카콜라의 소매 판매량 점유율은 40%를 넘어섰습니다.

음료용 마개에 영향을 미치는 또 다른 유력한 동향은 전자상거래의 대두입니다.

미국의 플라스틱 뚜껑 및 마개 시장 개요

미국의 플라스틱 뚜껑 및 마개 시장은 반고정 구조를 유지하고 있으며, 이 경향은 예측 기간 동안 계속될 것으로 보입니다.

2024년 3월 - 세계 레스토랑 브랜드인 서브웨이는 2025년 1월 1일부터 미국 레스토랑에서 음료를 공급하기 위해 펩시코와 10년간 계약을 맺었다고 발표했습니다. 수년간 프리트레이와의 파트너십은 2030년까지 연장되었으며, 미국 간식과 음료 포트폴리오는 하나공급업체로 통합되어 전체 시스템의 효율성을 높일 수 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

산업 밸류체인 분석

COVID-19 팬데믹 시장에 대한 영향 평가

제5장 시장 역학

시장 성장 촉진요인

포장 식품과 의약품에 대한 수요

중소규모의 최종 사용자 산업에서의 수요 증가

시장의 과제

원재료 비용의 변동

제6장 시장 세분화

원재료별

폴리에틸렌(PE)

폴리에틸렌 테레프탈레이트(PET)

폴리프로필렌(PP)

기타 재료(폴리스티렌 및 PVC)

유형별

스레드

디스펜싱

스레드 없음

어린이 보호

용도별

식품

의약품 및 헬스케어

음료

화장품 및 세면용품

가정용 화학제품

기타 용도

제7장 경쟁 구도

기업 프로파일

Silgan Closures(Silgan Holdings Inc.)

Amcor Ltd

Aptargroup Inc.

Berry Global Inc.

Albea Services SAS

Trimas Corporation

Tetra Pak International SA

Guala Closures Group(Guala Pack SPA)

MJS Packaging

O Berk Company LLC

Closure Systems International Inc.

Bericap Holding

제8장 투자 분석

제9장 시장 기회와 앞으로의 동향

KTH

영문 목차

영문목차

The United States Plastic Caps and Closures Market size is estimated at USD 12.12 billion in 2025, and is expected to reach USD 13.72 billion by 2030, at a CAGR of 2.51% during the forecast period (2025-2030).

Key Highlights

Plastic caps and closures utilize PP and PE as primary raw materials for manufacturing. Industries heavily rely on these materials, providing a cost-effective sealing solution. The demand for packaged food and pharmaceutical drugs has been steadily increasing, consequently impacting the caps and closures market, which is expected to see a rise in demand during the forecast period.

Similarly, amid a growing trend of health-consciousness among consumers, the demand for packaged beverages and pharmaceutical drugs is surging, propelling the caps and closures market. This rise is particularly pronounced in the plastic caps and closures segment, driven by the increasing accessibility of bottled water, which is a favored choice for health-conscious consumers.

Notably, in 2023, the Beverage Marketing Corporation and the International Bottled Water Association reported that bottled water claimed the top spot as the most consumed beverage in the United States. While the growth rate in the sector has tapered, the leading beverage category, in terms of volume, marked record highs in both producer revenues and total gallons. Specifically, in 2023, the bottled water market saw a modest increase of 0.4%, a slowdown from the 1.1% growth in 2022 and a significant decline from the robust growth rates of 4.6% and 4.1% observed in 2021 and 2020, respectively.

Also, the rise in bottled water demand among customers in the United States is propelling the plastic caps and closures market. These components are essential for sealing water bottles to prevent spills, facilitate transportation, and enhance shelf life. The growing awareness of water contamination and safety concerns is driving up the demand for bottled water, a trend expected to continue during the forecast period, potentially spiking the demand for plastic caps across the market.

Raw material prices directly impact the cost of plastic caps and closures. When the price of plastic resins rises, manufacturers face increased costs in sourcing, processing, and transforming these materials into packaging products. The escalation in raw material costs can strain profit margins, particularly if manufacturers cannot pass on the increased costs to customers. Consequently, this may result in reduced investments in innovation, expansion, or even downsizing, thus restraining the market's growth.

United States (US) Plastic Caps and Closures Market Trends

Polyethylene (PE) is expected to be the Fastest Growing Raw Material Segment

Polyethylene (PE) is one of the most durable plastics available, exhibiting resistance to chemicals and boasting a low cost. Derived from petroleum polymers, PE can withstand various environmental hazards, typically categorized as high-density polyethylene (HDPE) and low-density polyethylene (LDPE).

HDPE and LDPE represent the primary materials used in caps and closures. HDPE variants find extensive use in water, dairy, and juice bottles, favored for their excellent organoleptic properties, particularly in water bottle closures, due to their longstanding preference. Renowned for strength and durability, HDPE plastics can be color-matched and commonly found in white. Its adaptability and durability position HDPE as a top choice for cosmetic bottles.

Borealis notes that the growth in HDPE caps and closures is largely attributed to the replacement of metal caps on glass bottles (by PET) and shifting consumption patterns favoring smaller bottles for refreshments.

According to the American Chemistry Council, in 2023, the United States produced 7.05 billion pounds of polyethylene, including HDPE, LDPE, and LLDPE. Injection molding technology, particularly influential in the LDPE segment, contributes to the production of medical devices, caps, and closures.

Due to its strength and cost-effectiveness, many industries in the United States prefer HDPE over LDPE. HDPE's rigidity makes it an ideal packaging choice for impact-resistant goods. The chemical industry emerges as a major consumer, propelling the market's growth.

The US plastic caps and closures market is experiencing a notable increase, driven by a strategic emphasis on the polyethylene industry's export initiatives. Asia has emerged as a critical market for these exports. According to data from the US Commerce Department, US PE export shipments in the first quarter of 2023 increased by 30% compared to the previous year, totaling 3,196,437 million metric tons (mt) or 7.05 billion pounds.

The Beverage Segment is expected to Hold Major Market Share

Caps and closures are crucial in sealing containers, pouches, and bottles in the beverage industry, encompassing carbonated and non-carbonated drinks. They safeguard against foreign particles and preserve the flavor and taste of beverages. The beverage segment encompasses bottled water, fruit juices, ready-to-drink beverages, and energy drinks.

The escalating demand for single-serve beverages, coupled with the hot fill process that extends the shelf life of packaged drinks, is set to propel growth in the US caps and closures market. Companies favor plastic bottles for hot fill processes as they eliminate the need for preservatives, enhancing the drink's health quotient. Notably, the advantages of hot-fill plastic bottles include extended product shelf life and preservative-free content, their lightweight composition, and their cost-effectiveness due to their plastic composition.

Hot-fill plastic bottles are increasingly prevalent as various hot-fill processes become commonplace in the beverage industry. The rising prominence of hot-fill applications, particularly in the ready-to-drink segment, is anticipated to drive market growth.

The market for sports caps is expanding alongside the increasing demand for bottled water and energy drinks. Despite their weight, sports closures offer tamper-evident features. Diverse sports closure designs vary in aesthetics, neck diameters, and tamper-evident solutions catering to cold, dry, or wet aseptic filling requirements. According to Beverage Digest, in 2023, Coca-Cola's retail volume share of the US carbonated soft drink (CSD) market exceeded 40%. North America accounted for nearly 37% of the Coca-Cola Company's total revenue during the same period. The company's global net operating revenue in 2023 was approximately USD 46 billion.

Another influential trend impacting beverage closures is the rise of e-commerce. The convenience of online shopping presents an opportunity for companies to access new consumers and cater to the growing demand for at-home delivery. Consequently, more food and beverage sales are transitioning to direct-to-consumer e-commerce platforms.

United States (US) Plastic Caps and Closures Market Overview

The plastic caps and closures market maintains a semi-consolidated structure in the United States, a trend expected to continue during the forecast period. Key characteristics of this market include moderate exit barriers, a preference for established brands, and significant merger and acquisition activities. Noteworthy players in this market landscape are Silgan Closures (Silgan Holdings Inc.), Amcor Ltd, Aptargroup Inc., Berry Global Inc., and Albea Services SAS.

In March 2024 - Subway, a global restaurant brand, announced a 10-year agreement with PepsiCo to supply beverages in US restaurants beginning January 1, 2025. Subway's longstanding partnership with Frito-Lay will extend through 2030, bringing the brand's US snack and beverage portfolio together under one supplier and driving more efficiency across the system.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Degree of Competition

4.3 Industry Value Chain Analysis

4.4 Assessment of Impact of the COVID-19 Pandemic on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Demand for Packaged Food and Pharmaceutical Drugs

5.1.2 Increasing Demand from Small and Medium-Scale End-user Industries