일본의 식품 및 음료 산업은 서양 음식에 대한 소비자의 선호도 변화와 대량 소비에서 소비자에 이르기까지 다양한 제품군에 힘입어 지속적으로 성장하고 있습니다. 미국 농무부(USDA) 데이터에 따르면 2023년 일본은 미국 농산물의 4위 시장으로 부상하여 총 수입액이 130억 달러에 달할 것으로 예상되며, 미국은 일본의 해외 식품 및 음료 공급업체 1위 자리를 굳건히할 것으로 보입니다.

일본에서는 주스나 생수와 같은 무알코올 음료에 대한 수요가 증가하고 있으며, 이는 플라스틱 캡에 대한 수요를 증가시키고 있습니다. 미국 농무부의 데이터는 일본이 미국의 무알코올 음료, 특히 미네랄 워터와 주스를 선호하고 있음을 강조합니다. 동시에 일본 소비자들은 더 건강한 음료와 무알코올 맥주를 선호하고 있으며, 이는 플라스틱 뚜껑과 마개에 대한 필요성을 더욱 증가시키고 있습니다.

일본 제조업체들은 제품 차별화에 중점을 두고 지속가능하고 고품질의 경쟁력 있는 가격의 제품에 투자하여 진화하는 소비자 수요에 부응하고 있습니다. 일본 클로저(Japan Closure)와 같은 기업은 재활용 가능한 플라스틱 캡 연구의 선구자이며, 환경 발자국을 줄이기 위해 바이오매스 함량이 30%인 캡을 도입하여 시장 성장을 가속하고 있습니다.

그러나 일본의 플라스틱 시장은 문제에 직면해 있습니다. 수요 및 공급의 불균형에 따라 변동하는 플라스틱 가격은 플라스틱 뚜껑과 마개의 제조 비용에 직접적인 영향을 미쳐 시장 성장을 저해할 수 있습니다. 또한 일본의 플라스틱 폐기물 증가는 플라스틱 포장 솔루션에 대한 수요를 제한하는 이중 과제를 안고 있습니다.

일본의 플라스틱 뚜껑 및 마개 시장 동향

나사식 캡이 가장 높은 점유율을 차지

나사식 캡은 밀폐성이 뛰어나 식품, 음료, 화장품, 의약품 등 다양한 분야에서 폭넓게 활용되고 있습니다.

일본 제조업체는 주로 HDPE, LDPE, 폴리프로필렌과 같은 수지 재료로 이러한 캡을 생산하며, 연속형에서 비연속형까지 다양한 유형의 나사산을 제공합니다. 이 캡은 특히 음료수 병에 인기가 높으며, 포장의 미관을 향상시키고 제품의 맛과 품질을 유지하는 데 매우 중요한 역할을 하므로 다양한 용도에서 수요가 증가하고 있습니다.

Amcor Group GmbH 및 Aptar Group Inc.와 같은 주요 기업이 시장을 선도하고 있으며, 다양한 최종사용자를 위해 나사산 캡을 맞춤화하고 있습니다. 예를 들어 Amcor의 13/415mm 나사산 리브형 라이너리스 캡은 특히 제약 및 퍼스널케어 최종 용도에 맞게 조정되었습니다. 이러한 캡의 다목적성과 장점은 식품 및 음료에서 홈케어, 반려동물 관리, 건강 보조 식품에 이르기까지 다양한 산업 분야에서 채택을 촉진하고 있습니다.

일본에서는 폴리에틸렌(PE), 폴리프로필렌(PP) 및 기타 수지를 사용한 나사식 캡이 증가하는 추세로 제품 수요가 증가하고 있습니다. 이러한 급격한 증가는 주로 포장 솔루션으로 인해 원료 플라스틱의 소비가 증가함에 따라 주로 원료 플라스틱 소비가 증가했기 때문입니다. 경제산업부의 최근 통계에 따르면 2024년 4월 폴리에틸렌(PE) 소비량은 84.03톤, 폴리프로필렌(PP) 소비량은 105.75톤에 달했습니다.

식품 부문이 시장을 독점할 것으로 예상

식품 제조의 발전은 일본의 식생활에 눈에 띄는 변화를 가져왔고, 전통적인 신선식품에서 대량 생산 및 가공식품으로 전환했습니다. 이러한 변화는 특히 일본의 젊은 세대와 맞벌이 부부가 선호하는 가공식품과 조리식품 증가로 이어져 시장 성장을 주도하고 있습니다.

미국 농무부(USDA)에 따르면 고령화가 진행되는 일본에서는 단백질이 풍부하고 영양가가 높은 식품에 대한 선호도가 높아지고 있습니다. 식품 포장용 플라스틱 뚜껑과 마개에 대한 수요가 급증하는 것은 일본의 육류 가공품에 대한 식욕 증가에 직접적으로 대응하는 것으로, 플라스틱 뚜껑과 마개의 생산량 증가에 대응해야 합니다.

일본에서는 잼, 피클, 향신료, 견과류는 보통 플라스틱 밀폐 캡이 달린 병이나 용기에 담겨 있습니다. 이러한 밀폐 용기는 오염과 변조를 방지하고 개봉 및 분배를 편리하게 할 수 있도록 설계되었습니다. 제품의 유통기한을 연장하고, 외부 요인으로부터 보호하며, 포장내 산소 농도를 조절하는 데 매우 중요한 역할을 하므로 시장 성장을 촉진하는 데 있으며, 매우 중요한 역할을 합니다.

가공육, 유제품, 베이커리 제품, 채소에 이르기까지 일본의 미국 수입 의존도는 탄탄한 식품 소매 부문에 크게 좌우되고 있습니다. 일본 세관 데이터에 따르면 미국은 육류 제품의 26%, 가공 채소의 12%, 신선 과일의 6%, 가공 과일의 4%를 일본에 공급하고 있으며, 이는 일본 시장에서 플라스틱 뚜껑과 마개에 대한 수요를 더욱 부추기고 있습니다.

일본의 플라스틱 뚜껑 및 마개 산업 개요

일본의 플라스틱 뚜껑 및 마개 시장은 적당히 통합되어 있으며, 다음과 같은 국내 기업이 존재합니다. Nippon Closures, Toyo Seiken Group Holdings Ltd, and International players including Amcor Group GmbH, Aptar Group Inc., and Tetra Pak. 시장에서 지위를 구축하기 위해 기업은 신제품 개발, 파트너십, 합병과 인수, 협업에 중점을 두고 있습니다.

2024년 4월 미국에 본사를 둔 Aptar Group Inc.는 최신 제품인 Future Desktop Closure를 발표했습니다. 이 혁신적인 클로저는 미용 및 퍼스널케어 분야를 위해 설계되었으며 폴리에틸렌(PE)으로만 만들어져 완전히 재활용할 수 있습니다. 특히 이 제품에는 안전한 잠금 링이 있으며, 운송의 신뢰성을 높이고 최종사용자에게 프리미엄 경험을 선사합니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 개요

제4장 시장 인사이트

시장 개요

산업 밸류체인 분석

업계의 매력 - Porter's Five Forces 분석

바이어의 교섭력

공급 기업의 교섭력

신규 진출업체의 위협

대체품의 위협

경쟁 기업 간 경쟁 관계

제5장 시장 역학

시장 성장 촉진요인

국내 식품 및 음료 부문의 부상

시장에서 혁신적 제품에 대한 수요 증가

시장이 해결해야 할 과제

일본에서 플라스틱 가격의 변동

제6장 업계의 규제와 정책과 규격

제7장 시장 세분화

수지별

폴리에틸렌(PE)

폴리에틸렌 테레프탈레이트(PET)

폴리프로필렌(PP)

기타 플라스틱 소재(폴리스티렌, PVC, 폴리카보네이트 등)

제품 유형별

나사식

디스펜서

비나사식

소아용

최종 용도 산업별

식품

음료

생수

탄산음료

주류

주스 & 에너지 드링크

기타 음료

퍼스널케어&화장품

가정용 화학제품

기타 최종 용도 산업

제8장 경쟁 구도

기업 개요

Amcor Group GmbH

Aptar Group Inc.

Sonoco Products Company

Nippon Closures Co. Ltd.

Toyo Seiken Group Holdings Ltd.

Nihon Yamamura Glass Co. Ltd.

Tetra Laval International S.A.

Mikasa Industry Co. Ltd.

제9장 재활용과 지속가능성 전망

제10장 향후 전망

KSA

영문 목차

영문목차

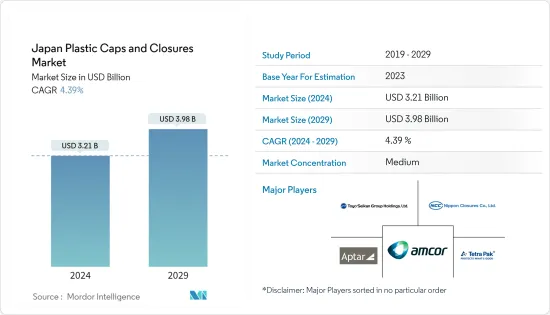

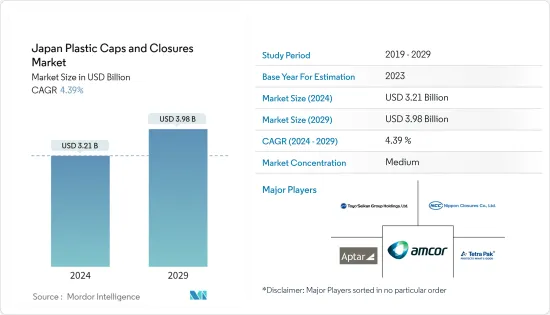

The Japan Plastic Caps And Closures Market size is estimated at USD 3.21 billion in 2024, and is expected to reach USD 3.98 billion by 2029, growing at a CAGR of 4.39% during the forecast period (2024-2029). In terms of shipment volume, the market is expected to grow from 18.21 billion units in 2024 to 21.78 billion units by 2029, at a CAGR of 3.65% during the forecast period (2024-2029).

Key Highlights

The Japanese food and beverage industry is on the rise, driven by shifting consumer tastes toward Western cuisine and a broad spectrum of products, ranging from bulk to consumer-oriented. According to data from the United States Department of Agriculture (USDA), in 2023, Japan emerged as the fourth largest market for United States agricultural goods, with imports totaling USD 13 billion, solidifying the United States as Japan's top foreign food and beverage supplier.

Japan's increasing appetite for non-alcoholic beverages, like juices and bottled water, boosts the demand for plastic caps. Data from the USDA highlights Japan's growing preference for US non-alcoholic beverages, especially mineral water and juices. Concurrently, Japanese consumers are leaning towards healthier drinks and non-alcoholic beers, further fueling the need for plastic caps and closures.

Japanese manufacturers focus on product differentiation, channeling investments into sustainable, high-quality, and competitively priced offerings to cater to evolving consumer demands. Companies like Nippon Closures Co. Ltd. are pioneering research in recyclable plastic caps, even introducing caps with 30% biomass content to reduce environmental footprints, bolstering market growth.

However, Japan's plastic market faces challenges. Fluctuating plastic prices, driven by demand-supply imbalances, directly impact the production costs of plastic caps and closures, potentially hindering market growth. Additionally, the country's mounting plastic waste poses a dual challenge, constraining the demand for plastic packaging solutions.

Japan Plastic Caps and Closures Market Trends

Threaded Caps Segment to Have the Highest Share

Threaded caps find extensive applications across various sectors, including food, beverages, cosmetics, and pharmaceuticals, due to their airtight sealing properties, which are crucial for preventing leaks and maintaining product integrity, especially in Japan.

Japanese manufacturers craft these caps predominantly from resin materials like HDPE, LDPE, and polypropylene, offering variations in thread types, from continuous to non-continuous closures. These caps, especially popular for beverage bottles, enhance packaging aesthetics and play a pivotal role in preserving the product's flavor and quality, thus amplifying their demand across a spectrum of applications.

Key players such as Amcor Group GmbH and Aptar Group Inc. lead the market, customizing their threaded caps to cater to various end-users. For instance, Amcor's 13/415 mm threaded ribbed linerless cap is specifically tailored to pharmaceutical and personal care end-use. The versatility and benefits of these caps have propelled their adoption, transcending industries from food and beverages to home care, pet care, and nutraceuticals.

In Japan, the utilization of Polyethylene (PE), Polypropylene (PP), and other resins for crafting threaded caps are on the rise, bolstering product demand. This surge is largely propelled by Japan's escalating consumption of raw material plastics, primarily for packaging solutions. Recent figures from the Ministry of Economy, Trade, and Industry (METI) reveal that in April 2024, Polyethylene (PE) consumption stood at 84.03 Metric Tons, while Polypropylene (PP) consumption reached 105.75 Metric Tons.

Food Segment Expected to Dominate the Market

Advancements in food manufacturing have led to a notable shift in the Japanese diet, transitioning from traditional fresh produce to mass-produced and processed foods. This change has seen a rise in pre-processed ingredients and ready-to-eat meals, especially favored by Japan's younger generation and dual-income households, driving substantial market growth.

According to the United States Department of Agriculture (USDA), Japan's aging demographic increasingly values protein-rich and nutritious foods. The surging demand for plastic caps and closures in food packaging directly responds to Japan's heightened appetite for processed meat products, necessitating a corresponding rise in plastic lid and closure production.

In Japan, jams, pickles, spices, and nuts are typically found in bottles or containers with airtight plastic closures. These closures prevent contamination and tampering and are engineered for convenient opening and dispensing. Their pivotal role in extending product shelf life, safeguarding against external elements, and managing oxygen levels within the packaging underscores their significance in driving market growth.

Japan's reliance on the United States for imports, spanning processed meat, dairy, bakery items, and vegetables, is largely steered by the robust food retail sector. Japan Customs data reveals that the U.S. supplies Japan with 26% of its meat products, 12% of processed vegetables, 6% of fresh fruits, and 4% of processed fruits, further fueling the demand for plastic caps and closures in the Japanese market.

Japan Plastic Caps and Closures Industry Overview

The Japanese plastic caps and closures market is moderately consolidated, with domestic players such as Nippon Closures Co. Ltd, Toyo Seiken Group Holdings Ltd, and International players including Amcor Group GmbH, Aptar Group Inc., and Tetra Pak. To solidify their footprint in the market, the players focus on new product development, partnerships, mergers and acquisitions, and collaborations.

April 2024: Aptar Group Inc., a United States-based company in Japan, unveiled its latest product, the Future Disc Top closure. This innovative closure, designed for the beauty and personal care sector, is crafted exclusively from Polyethylene (PE), making it entirely recyclable. Its secure locking ring is noteworthy, a feature that enhances its transit reliability, ultimately resulting in a premium experience for end-users.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Buyers

4.3.2 Bargaining Power of Suppliers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitutes Products

4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Rising Food and Beverage Sector in the Country

5.1.2 Increased Demand for Innovative Products in the Market

5.2 Market Challenge

5.2.1 Volatility in Plastic Prices in Japan

6 INDUSTRY REGULATION, POLICY AND STANDARDS

7 MARKET SEGMENTATION

7.1 By Resin

7.1.1 Polyethylene (PE)

7.1.2 Polyethylene Terephthalate (PET)

7.1.3 Polypropylene (PP)

7.1.4 Other Plastic Materials (Polystyrene, PVC, Polycarbonate, etc.)