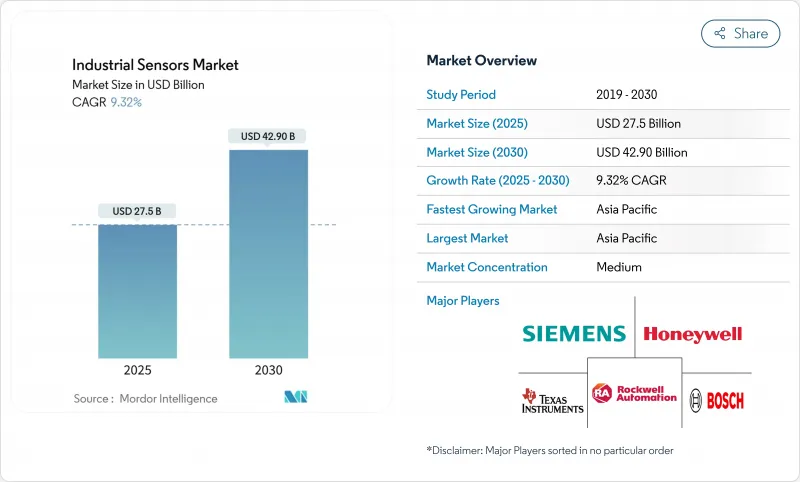

산업 센서 시장은 2025년에 275억 달러, 2030년에는 429억 달러에 이르고, CAGR은 9.3%를 나타낼 전망입니다.

왕성한 수요의 배경은 공장 디지털화의 진전, 에지 대응 장치의 보급, 시스템 통합을 간소화하는 오픈 통신 프로토콜의 보급이 있습니다. 제조업체는 고밀도 센서 네트워크를 자율 주행의 "눈과 귀"로 간주하고 모든 데이터를 클라우드로 라우팅하지 않고도 현장에서 신속한 의사 결정을 가능하게 합니다. 에너지 집약적인 섹터에서는 탈탄소화 지령의 강화에 대응하기 위해 세밀한 센싱을 도입하고 있는 한편, 브라운필드 공장에서는 자산의 건전성 데이터를 해방하기 위해 IO-Link의 개수를 가속화하고 있습니다. 기술적 측면에서 인센서 AI와 멀티 프로토콜 연결은 산업 센서 시장을 재정의하여 미션 크리티컬한 환경에서의 응답성과 탄력성을 강화하고 있습니다.

업무의 디지털화라는 경쟁압력에 노출되어 있는 제조업체가, 산업 센서 시장의 고조에 박차를 가하고 있습니다. 고밀도 센서 그리드는 온도, 압력, 유량과 같은 실시간 데이터를 수집하는 IIoT 아키텍처를 지원하여 이전에 분리된 기계를 지능형 자산으로 전환합니다. 엣지 컴퓨팅에 대한 지출은 플랜트가 애널리틱스를 프로세스에 가깝게 이동시키고 대기 시간을 줄이고 클라우드 대역폭에 대한 수요를 완화함에 따라 급증할 것으로 예측됩니다. 이 동향은 아시아태평양에서 두드러지며 중국의 스마트 팩토리 의무화와 일본의 자동화 주도가 센서 도입을 가속화하고 있습니다.

조기에 고장을 감지하면 비용이 많이 드는 가동 중지 시간을 줄일 수 있으므로 데이터 중심의 유지 보수 전략이 지원을 받고 있습니다. 진동, 열, 음향 센서와 에지 AI 모델을 결합한 설비를 도입함으로써 네트워크 트래픽을 줄이면서 90% 이상의 예측 정밀도를 달성하고 있습니다. 공정 산업은 엄격한 안전 요구 사항으로 인해 이러한 기능을 강조하지만 ROI 계산은 통합 작업과 조직 변경을 고려해야합니다.

중소기업에서는 네트워크 업그레이드, 미들웨어 및 통합 서비스를 포함하면 전체 프로젝트 비용이 BOM의 3배에서 4배가 되는 경우가 많습니다. 이기종 센서 출력을 수용하기 위해 레거시 MES 및 ERP 플랫폼을 개조하는 것은 구현을 장기화하고 전문 인력이 필요합니다.

레벨 센서는 2024년 매출의 18.4%를 차지하며 화학, 석유 및 수처리 사업에서 필수적인 재고 관리 기능으로 산업 센서 시장을 지원합니다. 한편, 이미지/비전 디바이스는 자동 결함 검출을 위해 인라인 머신 비전 시스템이 보급되어 CAGR은 11.2%로 예측되고 있습니다. 공장이 입증된 신뢰성을 중시하기 때문에 유선 아날로그 유형이 여전히 보급되고 있지만, 자기 진단 기능을 갖춘 디지털 유형도 급속히 진보하고 있습니다. 공급업체는 ESG 지침에 따른 에너지 모니터링 작업을 위해 MEMS 압력 센서와 유량 센서를 소형화합니다.

2차 동향으로서 광학과 초음파 기술을 결합한 하이브리드 센싱 플랫폼은 과제인 고체 재료 측정의 정확도를 높여줍니다. 컴팩트 카메라에 내장된 에지 AI는 대역폭에 부담을 주지 않고 장치에서 이상 감지를 가능하게 합니다. 이러한 역학을 통해 레벨 측정의 산업 센서 시장 규모는 신흥의 이미지 기술이 지출 증가를 획득하는 중에서도 압도적인 점유율을 유지할 것으로 예측됩니다.

2024년 산업 센서 시장 점유율의 31%는 이산 제조업이 차지합니다. 지속적인 설비 모니터링 수요가 왕성하기 때문에 공장은 진동, 온도, 위치 데이터를 동시에 획득하는 다기능 센서로 업그레이드를 계속하고 있습니다. 생명과학와 의약품은 2030년까지의 CAGR이 9.8%가 될 것으로 예측되며, 무균제조환경의 검증 프로토콜의 엄격화와 연속 제조 라인의 채택 확대가 돌풍이 됩니다.

화학 및 석유화학 제조업체는 수율 최적화를 위한 디지털 트윈 프레임워크에서 배출가스 모니터링을 위한 견고한 솔루션을 구축합니다. 광산업자는 고밀도 환경 감지에 따라 위험 지역을 탐색하는 스웜 로봇 시스템을 시도하고 있습니다. 송전망을 근대화하는 유틸리티자는 광섬유와 압전센서를 통합하여 재생가능에너지 발전 예측 및 설비자산관리를 개선하여 산업 센서 업계를 새로운 에너지 분야로 확대합니다.

산업 센서 시장은 센서 유형(유량, 압력, 기타), 최종 사용자 산업(화학제품 및 석유화학제품, 광업 및 금속, 전력 및 에너지, 식품 및 음료 등), 기술(유선/아날로그, 에지 AI/가상 센서 등), 통신 프로토콜(필드버스, 기타), 지역별로 분류되어 있습니다. 시장 규모와 예측은 모든 부문에 대해 금액(달러)으로 제공됩니다.

아시아태평양은 2024년 지출액의 44%를 차지하며 지속적인 정책 인센티브와 강력한 로봇 생태계를 반영합니다. 중국은 메이드 인 차이나 2025 프로그램에 힘입어 산업용 로봇의 세계 출하 대수의 52%를 차지하고 자동차와 가전 허브로서 센서 주문이 활발합니다. 일본은 최첨단 자동화 기술을 제공하고 한국은 정부의 공동투자를 통해 스마트 팩토리의 보급을 가속화하고 있습니다.

북미는 다품종 소량 생산과 에너지·인프라의 갱신에 있어서 계속해서 중요합니다. 공장에서는 엣지 AI 센서를 통합하여 예지보전을 진행하여 근로자의 안전성을 높이고 있습니다. 유럽 시장 성장은 지속적인 배출가스 감시를 의무화하는 탈탄소화 규칙과 보조를 맞추어 고정밀 유량 센서와 가스 분석 센서 수요를 자극하고 있습니다. 중동 및 아프리카, 남미 신흥국에서는 인프라 정비가 본격화되어 광업, 금속, 발전 프로젝트에 대한 수용성을 높이고 있습니다.

The industrial sensors market reached USD 27.5 billion in 2025 and is forecast to advance to USD 42.9 billion by 2030, delivering a 9.3% CAGR.

Strong demand stems from rising factory digitalization, deeper penetration of edge-ready devices, and wider availability of open communications protocols that simplify system integration. Manufacturers view dense sensor networks as the "eyes and ears" of automated operations, enabling faster decisions on the shop floor without routing all data to the cloud. Energy-intensive sectors now deploy granular sensing to comply with tightening decarbonization mandates, while brown-field plants accelerate IO-Link retrofits to unlock asset-health data. On the technology front, in-sensor AI and multi-protocol connectivity are redefining the industrial sensors market, enhancing responsiveness and resilience in mission-critical environments.

Manufacturers under competitive pressure to digitize operations keep fueling an upswing in the industrial sensors market. Dense sensor grids underpin IIoT architectures that collect real-time data on temperature, pressure, and flow, transforming previously disconnected machines into intelligent assets. Edge computing spend is projected to rise steeply as plants shift analytics closer to the process, trimming latency and easing cloud bandwidth demands. The trend is pronounced in Asia-Pacific where China's smart-factory mandates and Japan's automation leadership accelerate sensor uptake.

Data-driven maintenance strategies are gaining traction because early fault detection curbs costly downtime. Facilities deploying vibration, thermal, and acoustic sensors coupled with edge AI models achieve prediction accuracies above 90% while lowering network traffic. Process industries value these capabilities due to stringent safety requirements, yet ROI calculations must account for integration work and organizational change.

Small and mid-size enterprises often face total project costs three to four times higher than the bill of materials once network upgrades, middleware, and integration services are included. Retrofitting legacy MES and ERP platforms to accommodate heterogeneous sensor outputs prolongs implementation and demands specialist talent.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Level sensors accounted for 18.4% of 2024 revenue, anchoring the industrial sensors market with indispensable inventory-control functionality in chemicals, oil, and water-treatment operations. Image/vision devices, meanwhile, are forecast for an 11.2% CAGR as inline machine-vision systems proliferate for automated defect detection. Wired analog versions remain widespread because factories value proven reliability, but digital variants with self-diagnostics are advancing fast. Suppliers are miniaturizing MEMS pressure and flow sensors for energy-monitoring tasks aligned with ESG mandates.

Second-order trends point to hybrid sensing platforms that combine optical and ultrasonic techniques to boost accuracy for challenging solid-material measurements. Edge AI incorporated within compact cameras now enables on-device anomaly detection without bandwidth strain. These dynamics position the industrial sensors market size for level measurement to retain a commanding share even as emerging imaging technologies capture incremental spend.

Discrete manufacturing held 31% of the industrial sensors market share in 2024 due to persistent investments in automotive and electronics lines. Robust demand for continuous equipment monitoring keeps factories upgrading to multifunctional sensors that capture vibration, temperature, and positional data concurrently. Life sciences and pharmaceuticals are projected to achieve a 9.8% CAGR through 2030, benefitting from stricter validation protocols for sterile production environments and wider adoption of continuous-manufacturing lines.

Manufacturers in chemicals and petrochemicals deploy rugged solutions for emissions monitoring within digital-twin frameworks aimed at optimizing yield. Mining operators experiment with swarm-robotics systems that rely on dense environmental sensing to navigate hazardous zones. Utilities modernizing grids integrate fiber-optic and piezoelectric sensors to improve renewable-generation forecasting and equipment asset management, extending the industrial sensors industry into new energy verticals.

The Industrial Sensors Market is Segmented by Sensor Type (Flow, Pressure, and More), End-User Industry (Chemical & Petrochemicals, Mining & Metals, Power & Energy, Food & Beverage and More), Technology (Wired / Analog, Edge-AI / Virtual Sensors and More), Communication Protocol (Fieldbus and More), Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Segments.

Asia-Pacific captured 44% of 2024 spending, reflecting ongoing policy incentives and a strong robotics ecosystem. China dominates installations, propelled by the Made in China 2025 program and a 52% share of global industrial-robot shipments, translating into vigorous sensor orders across automotive and consumer-electronics hubs. Japan contributes cutting-edge automation technologies, while South Korea's government co-investment accelerates smart-factory penetration.

North America remains pivotal for high-mix, low-volume production and energy-infrastructure renewal. Plants integrate edge-AI sensors to advance predictive maintenance and enhance workforce safety. Europe's market growth aligns with decarbonization rules that require continuous emissions monitoring, stimulating demand for high-precision flow and gas-analysis sensors. Emerging economies in the Middle East, Africa, and South America increase uptake for mining, metals, and power-generation projects as infrastructure build-outs gather momentum.