ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

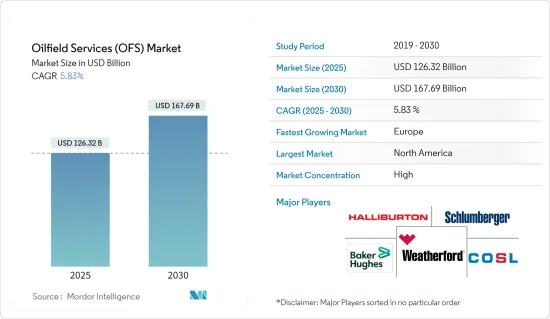

유전 서비스(OFS) 시장 규모는 2025년에 1,263억 2,000만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 5.83%로 성장할 전망이며, 2030년에는 1,676억 9,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 가스 매장량의 개발 증가 및 첨단 기술, 툴, 설비 등의 요인이 예측 기간 중의 유전 서비스 시장을 견인할 것으로 예상됩니다.

한편, 수급 격차, 지정학, 기타 몇개의 요인에 기인하는 최근의 기간에 있어서 불안정한 원유 가격이, 유전 서비스 시장 수요 증가를 억제하고 있습니다.

그러나 탄화수소의 생산비용을 최적화하기 위한 신기술 및 수법에 대한 주목은 예측 기간 중 유전 서비스 시장에 몇 가지 기회를 만들어낼 것으로 예상됩니다.

북미는 셰일 유전에서의 시추 및 생산 활동이 활발하기 때문에 예측 기간 중 최대 시장이 될 것으로 예상됩니다.

유전 서비스 시장 동향

시추 서비스가 시장을 독점할 전망

세계 경제는 석유 수요의 대폭적인 증가를 뒷받침할 것으로 예상됩니다. 호조를 보이는 경제는 더 많은 석유를 소비할 것으로 예상되며, 그 수요는 오랜 기간에 걸쳐 크게 증가할 것으로 예상됩니다. 인도와 중국은 2024년까지 세계 석유 수요의 약 50%를 차지한 것으로 평가됩니다.

석유수출국기구(OPEC)의 통계에 따르면, 2023년 세계의 원유 수요는 일량 약 1억 221만 배럴로, 2022년의 9,957만 배럴로부터 증가했습니다. 원유 수요의 증가는 전 세계적으로 시추 서비스의 수요를 증가시키고 있습니다.

2023년 4월, 해양 드릴링 회사인 Seadrill Limited가 Aquadrill LLC의 인수에 성공했다고 발표했습니다. 9억 5,800만 달러 상당의 전 주식 취득에 의해, 12기의 플로터, 3기의 가혹 환경 리그, 4기의 양성 잭 업, 3기의 입찰 지원 리그로 구성되는 고사양 플리트가 탄생했습니다.

2024년 2월 중동 최대의 국영 시추 회사인 ADNOC Drilling은 오만에서의 리그 공급 입찰 자격을 취득하고 사우디아라비아와 쿠웨이트에서의 입찰 참가 승인을 요구하고 있습니다. 2024년 말까지 이 회사는 아랍에미리트 이외에 배치할 수 있는 만큼의 리그를 보유하게 됩니다.

그 때문에 석유 및 가스 대기업 회사는 증산과 에너지 수요 증가에 대응할 필요에 강요되고 있습니다. 그 결과 재래형 유전이 성숙의 조짐을 보이기 시작하면서 몇몇 사업회사들은 비재래형 매장량 개발에 중점을 옮기고 있습니다.

2023년 10월, Transocean은 육상 시추 리그 3기의 새로운 연장 계약을 획득했다고 발표했습니다. Industries와의 계약에 따라 일당 33만 달러로 인도에 배치되어 있습니다. 계약은 2025년 10월까지 갱신되어 일당은 34만 8,000달러로 증액되었습니다. 2023년 12월 현행 계약 종료 후 리그는 45일간의 준비 기간을 거쳐 새로운 계약을 시작합니다.

따라서, 상기의 점으로부터, 예측 기간 중 시추 서비스가 유전 서비스 시장을 독점할 것으로 예상됩니다.

북미가 시장을 독점하는 전망

북미는 세계적으로 가장 발달한 해양 석유 및 가스 산업 중 하나이며, 주요 중점 지역은 멕시코 만과 알래스카 해안 지역의 방대한 매장량입니다. 폭이 증가하여 이 지역의 해외 석유 및 가스 부문에 대한 투자를 유치했습니다. 시추 심도가 해마다 깊어짐에 따라, 기술적으로 회수 가능한 매장량은 큰폭으로 증가해, 이 지역의 오프쇼어 석유 및 가스 부문에의 투자를 유치했습니다. 상기의 요인에 의해, 이 지역은 유전 서비스 시장의 세계의 핫스팟이기도 하며, 그 점유율의 대부분은 미국이 차지하고 있습니다.

미국이 석유 및 가스 생산 능력의 확대에 다액의 투자를 실시했기 때문에 멕시코만은 해양 시추 리그 서비스의 중요한 핫스팟이 되었습니다. 멕시코만은 석유 및 가스를 포함한 이 지역의 풍부한 천연자원을 담당하고 있습니다.

미국은 주로 셰일층이나 타이트한 매장량으로 시추 및 수압 파쇄되는 갱정의 수가 증가하고 있기 때문에 유전 서비스의 최대 시장 중 하나가 될 것으로 예상됩니다. 이 분지의 손익분기 가격의 낮은 수준이 이를 뒷받침하고 있습니다. 최근 셰일 플레이, 수평 굴착, 프래킹 개발로 이 지역의 유전 서비스 수요는 크게 증가하고 있습니다.

미국은 항상 최첨단을 달리고 있으며, 예측 기간 동안에도 북미의 석유 및 가스 시장을 계속 독점할 것으로 예상됩니다. 미국은 세계적으로 주요 석유 및 천연가스 생산국이며, 향후 수년간은 세계 석유 수요의 약 60%를 커버할 것으로 예상되고 있습니다. 그러나 러시아-우크라이나 전쟁의 악영향으로 미국은 러시아로부터의 석유 및 석유 정제품, 천연 가스 및 석탄의 수입 제한을 부과했습니다. 이 결과 미국 전역에서 가스 가격이 상승하고 인플레이션 압력이 높아졌기 때문에 2022년에는 자본 예산과 지출이 감소하고 생산이 억제되며 사업회사에 의한 굴착 리그 수가 감소했습니다.

그러나 이 시나리오는 2023년에는 회복되었습니다. 예를 들어, Baker Hughes의 리그 카운트에 따르면 2024년 2월, 미국의 가동 중인 로터리 리그는 626기로, 그 중 20기가 오프쇼어링 리그, 606기가 온쇼어링 리그였습니다. 2022년 말 가동 리그 수가 15기였던 것에 비해 오프쇼어링 리그 수는 증가를 기록했습니다. 이러한 동향은 이 나라의 시추 서비스의 성장을 지지하고 유전 서비스 시장의 성장을 한층 더 촉진할 것으로 생각됩니다.

마찬가지로 캐나다는 베네수엘라, 사우디아라비아에 이어 세계 3위의 원유 매장량을 자랑하며, 그 중 96%는 오일샌드 매장량입니다. 이 나라에서 채굴 가능한 원유는 밀도가 높고 모래 입자의 함유량도 많습니다. 이 때문에 유정의 저혈에서 지표까지 석유를 수송하기 위해서는 높은 압력과 갱정에의 개입이 필요해, 이 나라에 있어서 유전 서비스의 수요가 높아지고 있습니다.

따라서, 상기의 점으로부터, 예측 기간중, 북미가 유전 서비스 시장을 독점할 것으로 예상됩니다.

유전 서비스 산업 개요

유전 서비스 시장은 세분화되어 있습니다. 이 시장의 주요 기업에는 Schlumberger Limited, Baker Hughes Company, Halliburton Company, Weatherford International PLC, China Oilfield Services Limited 등이 있습니다.(순부동)

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

서문

시장 규모 및 수요 예측(단위 : 10억 달러)2029년)

석유 및 천연가스 생산량 예측(-2029년)

육상 및 해상 리그 가동수(-2023년)

최근 동향 및 개발

정부의 규제 및 시책

시장 역학

성장 촉진요인

가스 매장량의 개발 및 첨단 기술, 툴, 설비 증가

세계 유전 서비스 투자 증가

성장 억제요인

수급 격차에 기인하는 최근 기간 원유 가격의 변동

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

제5장 시장 세분화

서비스 유형별

시추 서비스

완성 서비스

생산 및 개입 서비스

기타

배치 장소별

온쇼어

오프쇼어

시장 분석 : 지역별 시장 규모 및 수요 예측(-2028년)

북미

미국

캐나다

기타 북미

유럽

독일

프랑스

영국

이탈리아

러시아

스페인

노르딕

튀르키예

기타 유럽

아시아태평양

중국

인도

일본

한국

말레이시아

태국

베트남

기타 아시아태평양

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

남아프리카

나이지리아

카타르

이집트

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

주요 기업의 전략

기업 프로파일

Schlumberger Limited

Weatherford International PLC

Baker Hughes Company

Halliburton Company

Transocean Ltd

Valaris PLC

China Oilfield Services Limited

Nabors Industries Inc.

Basic Energy Services Inc.

OiLSERV

Expro Group

시장 랭킹 및 공유(%) 분석

제7장 시장 기회 및 향후 동향

탄화수소 생산비용을 최적화하는 신기술 및 새로운 방법에 대한 주목 고조

AJY

영문 목차

영문목차

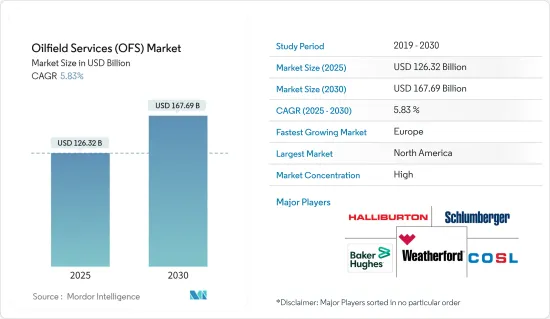

The Oilfield Services Market size is estimated at USD 126.32 billion in 2025, and is expected to reach USD 167.69 billion by 2030, at a CAGR of 5.83% during the forecast period (2025-2030).

Key Highlights

Over the medium term, factors such as the increasing development of gas reserves and advanced technology, tools, and equipment are expected to drive the oilfield services market during the forecast period.

On the other hand, the volatile oil prices over the recent period, owing to the supply-demand gap, geopolitics, and several other factors, have been restraining the growth in the demand for the oilfield services market.

However, the focus on new technologies and methods to optimize the production cost of hydrocarbons is expected to create several opportunities for the oilfield services (OFS) market during the forecast period.

North America is expected to be the largest market during the forecast period, owing to high drilling and production activity in shale fields.

Oilfield Services (OFS) Market Trends

Drilling Services Are Expected to Dominate the Market

The global economy is expected to underpin a substantial increase in oil demand. Strong economies are anticipated to consume more oil, and the demand is expected to grow significantly over the years. India and China will contribute around 50% of the global oil demand by 2024.

According to the Organization of the Petroleum Exporting Countries (OPEC) statistics, the worldwide crude oil demand was around 102.21 million barrels per day in 2023, up from 99.57 million barrels in 2022. The rising demand for crude oil increases the demand for drilling services worldwide.

In April 2023, Seadrill Limited, an offshore drilling company, announced acquiring Aquadrill LLC successfully. The all-stock acquisition, valued at USD 958 million, creates a high-spec fleet comprised of 12 floaters, three harsh environment rigs, four benign jack-ups, and three tender-assisted rigs.

In February 2024, ADNOC Drilling, the largest national drilling company in the Middle East, was qualified to bid to supply rigs in Oman and is seeking approvals to participate in tenders in Saudi Arabia and Kuwait. By the end of 2024, the company will have enough rigs to deploy outside the United Arab Emirates.

Hence, the top oil and gas operating companies are under increasing pressure to increase production and meet the increasing energy demand. As a result, several operating companies have shifted their focus toward exploiting unconventional reserves, as the conventional fields have started showing signs of maturity.

In October 2023, Transocean announced that it secured a new extension contract for three of its onshore drilling rigs. One of those rigs is deployed in India under contract with Reliance Industries Limited at a day rate of USD 330,000. The agreement was renewed until October 2025 with an increased day rate of USD 348,000. Following completion of the current contract in December 2023, the rig will undergo a 45-day preparation period before commencing the new contract.

Therefore, owing to the above points, drilling services are expected to dominate the oilfield services (OFS) market during the forecast period.

North America is Expected to Dominate the Market

North America has one of the most well-developed offshore oil and gas industries globally, with the primary areas of focus being the vast reserves in the Gulf of Mexico and offshore Alaska region. As drilling depths increased over the years, the volume of technically recoverable reserves increased significantly, attracting investments in the region's offshore oil & gas sector. Due to the factors mentioned above, the region is also a global hotspot for the oilfield services market, with most of the share from the United States.

As the United States invested heavily in expanding its oil & gas production capacity, the Gulf of Mexico has become a key hotspot for offshore drilling rig services. The Gulf of Mexico is responsible for the region's rich natural resources, including oil and gas.

The United States is expected to be one of the largest markets for oilfield services, mainly due to the increasing number of wells being drilled and fracked in shale and tight reserves. The basins' low breakeven price supports this. The recent development of shale plays, horizontal drilling, and fracking has resulted in a massive increase in demand for oilfield services in the region.

The United States has always been at the forefront and is expected to continue dominating North America's oil and gas market during the forecast period. The United States is a major crude oil and natural gas producer globally, and it is expected to cover around 60% of the world's oil demand in the coming years. However, owing to the negative impact of the Russia-Ukraine War, the United States imposed restrictions on importing oil, refined petroleum products, natural gas, and coal from Russia. This led to higher gas prices and increased inflation pressure across the United States, leading to a decline in the capital budget and expenditure, curtailed production, and reduced drilling rig count by the operating companies in 2022.

However, this scenario recovered in 2023. For instance, according to the Baker Hughes Rig Count, in February 2024, the United States had 626 active rotary rigs, of which 20 were offshore rigs and 606 onshore rigs. This recorded a rise in the offshore rig counts compared to the 15 active rigs at the end of 2022. These trends will likely support the growth of the country's drilling services and further promote the growth of the oilfield services market.

Similarly, Canada has the world's third-largest crude oil reserves, after Venezuela and Saudi Arabia, of which 96% are oil sand reserves. The oil available in the country is high-density and has a high sand particle content. Due to this, oil transport from the bottom hole of the oil well to the surface requires high pressure and wellbore intervention, thus increasing the demand for oilfield services in the country.

Therefore, owing to the above points, North America is expected to dominate the oilfield services (OFS) market during the forecast period.

Oilfield Services (OFS) Industry Overview

The oilfield services market is fragmented. Some of the major players in the market (in no particular order) include Schlumberger Limited, Baker Hughes Company, Halliburton Company, Weatherford International PLC, and China Oilfield Services Limited.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2029

4.3 Crude Oil and Natural Gas Production and Forecast, till 2029

4.4 Onshore and Offshore Active Rig Count, till 2023

4.5 Recent Trends and Developments

4.6 Government Policies and Regulations

4.7 Market Dynamics

4.7.1 Drivers

4.7.1.1 Increasing Development of Gas Reserves and Advanced Technology, Tools, and Equipment

4.7.1.2 Increasing Investment in the Oilfield Services across World

4.7.2 Restraints

4.7.2.1 The Volatile Oil Prices Over the Recent Period, Owing to the Supply-Demand Gap

4.8 Supply Chain Analysis

4.9 Porter's Five Forces Analysis

4.9.1 Bargaining Power of Suppliers

4.9.2 Bargaining Power of Consumers

4.9.3 Threat of New Entrants

4.9.4 Threat of Substitutes Products and Services

4.9.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Service Type

5.1.1 Drilling Services

5.1.2 Completion Services

5.1.3 Production and Intervention Services

5.1.4 Other Services

5.2 Location of Deployment

5.2.1 Onshore

5.2.2 Offshore

5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Rest of North America

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 France

5.3.2.3 United Kingdom

5.3.2.4 Italy

5.3.2.5 Russia

5.3.2.6 Spain

5.3.2.7 NORDIC

5.3.2.8 Turkey

5.3.2.9 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 India

5.3.3.3 Japan

5.3.3.4 South Korea

5.3.3.5 Malaysia

5.3.3.6 Thailand

5.3.3.7 Vietnam

5.3.3.8 Rest of Asia-Pacific

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 United Arab Emirates

5.3.5.3 South Africa

5.3.5.4 Nigeria

5.3.5.5 Qatar

5.3.5.6 Egypt

5.3.5.7 Rest of the Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Schlumberger Limited

6.3.2 Weatherford International PLC

6.3.3 Baker Hughes Company

6.3.4 Halliburton Company

6.3.5 Transocean Ltd

6.3.6 Valaris PLC

6.3.7 China Oilfield Services Limited

6.3.8 Nabors Industries Inc.

6.3.9 Basic Energy Services Inc.

6.3.10 OiLSERV

6.3.11 Expro Group

6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Focus on New Technologies and Methods to Optimize its Production Cost of Hydrocarbons