다이캐스팅 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Die Casting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1686552

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

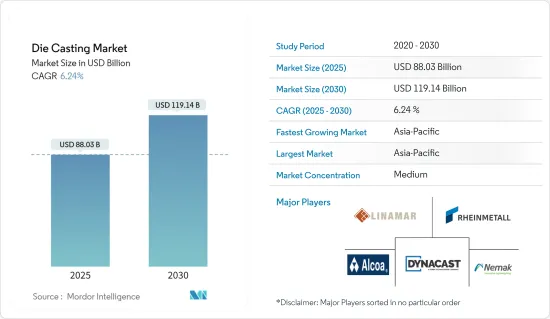

다이캐스팅 시장 규모는 2025년에 880억 3,000만 달러로 추정되고, 2030년에는 1,191억 4,000만 달러에 달할 것으로 예측되며, 예측 기간 중(2025-2030년)의 CAGR은 6.24%를 나타낼 전망입니다.

COVID-19의 발생은 제조업에 타격을 주었습니다. 세계 여러 주요 경제 국가가 봉쇄되면서 공급망에 차질이 생겼습니다. 경제가 회복되면서 소비자 선호도가 경량화 차량으로 바뀌면서 자동차 산업에서 다이캐스트 부품에 대한 수요가 크게 증가하면서 시장이 다시 활기를 되찾았습니다.

중기적으로 다이캐스팅 산업의 공급망 복잡성, 자동차 시장 확대, 산업 기계의 다이캐스팅 부품 보급률 증가, 건설 부문 성장, 전기 및 전자 분야의 알루미늄 주조 사용 등이 시장을 주도할 것으로 예상됩니다. 연비를 높이기 위한 CAFE 표준과 EPA 정책으로 인해 자동차 제조업체는 경량 비철금속을 사용하여 자동차 무게를 줄이려고 노력하고 있습니다.

높은 열전도율로 인해 전기 및 전자 산업에서 알루미늄 다이캐스팅 부품에 대한 수요가 증가함에 따라 예측 기간 동안 성장을 주도 할 가능성이 높습니다. 결과적으로 다이캐스트 부품을 경량화 전략으로 채택하는 것이 자동차 부문에서 이전 시장의 주요 동인으로 작용하고 있습니다. 그러나 원자재 공급 부족, 원자재 가격 변동성, 야금 산업의 배기가스 배출에 대한 환경 규제는 시장 성장의 주요 장벽으로 작용하고 있습니다.

아시아태평양은 중국과 인도와 같은 국가에서 자동차 수요가 증가하고 다양한 응용 분야에 알루미늄 다이캐스팅 사용이 증가함에 따라 다이캐스팅 시장에서 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.

다이캐스팅 시장 동향

다이캐스팅 공정에서 중요한 역할을 할 것으로 예상되는 알루미늄

알루미늄 고압 다이캐스팅 부품은 경량 부품을 제조하고 복잡한 형상을 위한 높은 유연성을 제공하기 때문에 수년 동안 다양한 산업 분야에서 수요가 증가하고 있습니다.

최근 몇 년 동안 자동차 부품은 신기술의 진화와 함께 발전과 혁신을 거듭해 왔습니다. 그중에서도 자동차 부품 제조에 경량 소재를 사용하는 것이 전국적으로 주목을 받고 있습니다.

이러한 인기의 중요한 이유 중 하나는 핵심 부품을 제조하는 경량 자동차 소재의 채택으로 자동차의 연비가 향상되었기 때문입니다.

또한 차량 경량화는 안전, 품질, 성능의 저하 없이 이루어져야 합니다.

또한, 시장 발전을 위해 주요 업체들의 인수 및 파트너십이 증가하고 있습니다.

2022년 8월, Wencan Group은 안후이성 육안경제기술 개발구에 신에너지 자동차(NEV)용 알루미늄 다이캐스트 부품 생산 기지를 건설할 계획이라고 발표했습니다.

2021년 10월, 다양한 락 장치, 전기, 전자, 기계, 자동차, 공업 부품의 제조 및 조립 사업을 실시하는 완전 자회사로서 Sandhar Engineering Private Limited를 설립했습니다.

2021년 4월 Jaya Hind Industries는 KS Huayu AlutechGmbH(KSATAG)와 자동차용 실린더 블록과 실린더 헤드의 제조에 관한 기술 제휴를 2027년까지 연장했습니다.

2021년 3월, Sandhar Technologies는 Unicast Autotech와 알루미늄 다이캐스팅 사업 인수를 위한 구속력 없는 양해각서를 체결했습니다.

알루미늄 다이캐스팅 시장의 성장은 자동차 및 비자동차 부문에서 경량 부품 및 고전도성 금속 부품에 대한 수요 증가를 충족하기 위해 예측 기간 동안 계속 증가 할 것으로 보입니다.

아시아태평양이 현저한 성장을 이룰 전망

아시아태평양은 예측 기간 동안 다이캐스팅 시장에서 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.

인도와 중국의 저렴한 노동력과 낮은 제조 비용은 아시아태평양 지역의 시장 성장을 더욱 가속화할 것으로 예상됩니다.

2022년 5월, Tamil Nadu Small Industries Development Corporation은 알루미늄 고압 다이캐스트용 공통 설비 센터를 설립하기 위해 5.8 칼로르 루피를 투자했습니다.

전국적으로 자동차 제조 산업이 확장됨에 따라 자동차 경량 소재에 대한 수요가 증가할 것으로 예상됩니다

2021년 2월, MG Motors는 구자라트 주 할롤 공장에서 생산 능력을 강화하기 위해 사업 확대와 현지화에 1,500캐롤 루피를 투자할 가능성이 있다고 발표했습니다.

인도 정부는 예측 기간 동안 인도에서 전기 자동차의 차량당 알루미늄 사용량을 29Kg에서 160Kg으로 늘릴 것을 제안했습니다.

또한 전기 자동차를 제조하는 회사들도 이러한 압력 다이캐스팅 기계를 적극적으로 조달하고 있으며, 증가하는 소비자 수요에 대비하기 위해 이 기술을 채택하고 있습니다.

몇몇 업체는 이 시장에서 경쟁력을 유지하기 위해 제조 용량 확대와 같은 성장 전략을 채택하고 있습니다.

2021년 7월, YIZUMI는 미국과 인도에 다이캐스트 기술 서비스 센터(TSC)를 설립하여 다이캐스트 셀, 금형, 다이캐스팅 공정 및 제품 디버깅을 위한 통합 솔루션을 제공하는 다이캐스팅 기술 서비스 센터(TSC)를 설립했습니다.

2021년 2월, Endurance Technologies는 타밀나두주 칸치푸람의 바다갈에 위치한 새 공장에서 상업 생산을 시작했습니다.

다이캐스트 산업 개요

다이 캐스팅 주조 시장은 다음과 같은 여러 주요 기업에 의해 지배되고 있습니다.

2022년 3월, Linamar Corporation은 GF Casting Solutions(GF)의 주식 50%를 취득했습니다.

2022년 1월, Gibbs Die Casting의 자회사인 Koch Enterprises, Inc.는 Amprod Holdings, LLC를 인수했습니다.

2022년 1월 Sandhar Auto Electric Solutions Private Limited를 완전 자회사로 설립하여 e-모빌리티 사업과 첨단 기술 솔루션의 제공을 시작했습니다.

2021년 8월, Linamar Corporation은 네덜란드의 Innovative Mechatronic Systems BV(IMSystems)와의 제휴를 발표했습니다.

2021년 4월, Aludyne은 Shiloh Industries CastLight 부문을 인수했다고 발표했습니다.

2021년 2월, Endurance Technologies는 인도 타밀 나두 주 칸체프람의 신공장에서 상업 생산을 개시했다고 발표했습니다.

2020년 4월, Endurance Technologies는 이탈리아 트렌티노를 거점으로 하는 Adler SpA의 주식 99%를 취득했습니다.

The Die Casting Market size is estimated at USD 88.03 billion in 2025, and is expected to reach USD 119.14 billion by 2030, at a CAGR of 6.24% during the forecast period (2025-2030).

The COVID-19 outbreak hit the manufacturing industry adversely. The disruptions were caused in the supply chain as several major economies of the world were in lockdown. All the manufacturing units and OEM plants were forced to halt production and operations during this period. With the recovery of economies, the demand returned to the market witnessing huge demand for die-cast parts in the automotive industry as the consumer preference changed to lightweight vehicles. The trend is expected to continue and drive market growth.

Over the medium term, the market studied is largely driven by supply chain complexities in the die-casting industry, expanding automotive market, increasing penetration of die-casting parts in industrial machinery, growing constructional sector, and employing aluminum casts in electrical and electronics. CAFE standards and EPA policies to cut down automobile emissions and increase fuel efficiency are driving the automakers to reduce the weight of the automobile by employing lightweight non-ferrous metals. Subsequently, employing die-cast parts as a weight reduction strategy is acting as a major driver for the former market in the automotive segment.

Rising demand for aluminum die-casting parts in the electrical and electronics industry owing to its high thermal conductivity is likely to drive growth during the forecast period. Subsequently, employing die-cast parts as a weight reduction strategy is acting as a major driver for the former market in the automotive segment. However, a crunch in raw material supply, volatility in raw material prices, and environmental regulations on emissions for the metallurgy industries are acting as major barriers to market growth.

The Asia-Pacific region is anticipated to hold the largest market share in the die-casting market due to the rise in demand for automobiles in countries such as China and India and the rise in the use of aluminum die-casting for various applications. North America is also expected to witness significant growth in the aluminum die-casting market due to growing output from the construction and automotive sectors.

Die Casting Market Trends

Aluminum Anticipated to Play Key Role in Die Casting Process

The demand for aluminum high-pressure die-casting parts has been increasing across numerous industrial applications over the years, as the process manufactures lightweight parts and provides high flexibility for complex shapes.

In recent years, automotive parts have witnessed advancements and innovations with the evolution of new technologies. Among them, the use of lightweight materials for the manufacturing of auto components has been gaining attention across the country.

One of the important reasons for this popularity is the enhanced fuel economy of automobiles with the adoption of lightweight automotive materials manufacturing crucial parts.

Additionally, the lightweight of vehicles must be done without compromising on safety, quality, and performance. Aluminum die-cast parts are durable and can be endlessly recycled therefore, aluminum is most preferred by manufacturers due to its varied advantages.

Moreover, there is a rising number of acquisitions and partnerships by the major players to further enhance development in the market. For instance,

In August 2022, Wencan Group Co., Ltd. announced that it intends to build a production base of aluminum die-cast parts for New Energy Vehicles (NEVs) in Lu'an Economic and Technological Development Zone, Anhui Province.

In October 2021, Sandhar Engineering Private Limited was incorporated as a wholly owned Subsidiary Company for carrying out the business of manufacturers, and assembling various Locking Devices, Electrical, Electronics, Mechanical, Automobile, and Industrial parts.

In April 2021, Jaya Hind Industries extended its technical partnership with KS Huayu AlutechGmbH (KSATAG) for the manufacturing of automotive cylinder blocks and cylinder heads till 2027. The scope of the agreement has also been expanded to cover new parts from Sunrise Industries, such as Electric Vehicles, Structural parts for Chassis, etc.

In March 2021, Sandhar Technologies entered a non-binding Memorandum of Understanding with Unicast Autotech to acquire its aluminum die-casting business

The growth of the aluminum die-casting market is likely to continue to increase during the forecast period to meet the increasing demand for lightweight components and high-conductivity metal parts from the automotive and non-automotive sectors.

Asia-Pacific Region Likely to Witness Significant Growth

The Asia-Pacific region is anticipated to hold the largest market share in the die-casting market during the forecast period. The growing automobile industry, demand from the industrial sector, and increased scope of application in windmills and telecommunications are expected to drive the die-casting market at a faster pace in the Asia-Pacific region.

Cheaper labor and low manufacturing costs in India and China are expected to further accelerate the market growth in the Asia-Pacific region. In addition, increased demand for electric and hybrid vehicles has turned automakers' focus to using lightweight materials like aluminum as a substitute for heavier steel and iron in all types of vehicles. For instance,

In May 2022, Tamil Nadu Small Industries Development Corporation invested an amount of INR 5.8 Crore to establish a common facility center for aluminum high-pressure die casting.

The growing expansion of automotive manufacturing industries across the country is likely to increase the demand for lightweight materials for automotive applications. For instance,

In February 2021, MG Motors announced that INR 1,500 crore may be invested in the expansion and localization of its business to increase its production capacity at the Halol plant in Gujarat.

The government of India has proposed the use of aluminum per vehicle in India from 29 Kg to 160 Kg for the electric vehicle during the forecast period.

In addition, the companies manufacturing electric vehicles are also actively procuring these pressure diecasting machines and are adopting this technology to make themselves ready for growing consumer demand.

Several players adopt growth strategies, such as manufacturing capacity expansion, to stay competitive in this market. For instance,

In July 2021, YIZUMI established the Die Casting Technical Service Center (TSC) in the United States and India that offers integrated solutions for die casting cells, dies, die casting process, and product debugging.

In February 2021, Endurance Technologies commenced commercial production at its new plant in Vallam, Vadagal, Kancheepuram, Tamil Nadu. The plant manufactures aluminum die-castings and carries out the integration of disc brake components with control brake modulators for supplying machined aluminum castings to Hyundai, Kia, and Royal Enfield.

Die Casting Industry Overview

The Die Casting market is dominated by several key players such as Neamk, Alcoa Corporation, Linamar Corporation, Dynacast, and many others. These key players in the market are focusing on expanding their presence globally through various mergers, partnerships, joint ventures, and acquisitions. For instance,

In March 2022, Linamar Corporation acquired a 50% interest in GF Casting Solutions (GF). Through this acquisition, Linamar Corporation enhanced its product portfolio in automotive applications.

In January 2022, Koch Enterprises, Inc., a subsidiary of Gibbs Die Casting acquired Amprod Holdings, LLC. Through this acquisition, the company expanded its product portfolio across the United States.

In January 2022, Sandhar Auto Electric Solutions Private Limited was incorporated as a wholly owned Subsidiary Company to undertake e-mobility business and to provide Advanced Technology Solutions. Sandhar Auto Electric Solutions Private Limited is primarily involved in the business of manufacturing parts/components for Battery Electric Vehicles, Hydrogen Fuel Cell Vehicles, Biofuel based technology Vehicle, All Terrain Vehicles (ATVs), and any other Advanced Automotive Technology Vehicles.

In August 2021, Linamar Corporation announced the partnership with Netherlands-based Innovative Mechatronic Systems B.V. (IMSystems). The partnership focuses on bringing the Archimedes Drive transmission system to market.

In April 2021, Aludyne announced that it had acquired Shiloh Industries CastLight division. This division manufactures aluminum die-casting parts.

In February 2021, Endurance Technologies announced that it had started commercial production at the new plant in Kancheepuram, Tamil Nadu, India. The plant will manufacture aluminum die-castings and integration of disc brake components for two and four-wheelers.

In April 2020, Endurance Technologies acquired a controlling equity stake of 99% in Adler SpA, based out of Trentino, Italy. The acquisition is expected to improve the company's reach across Europe, with the aid of ten manufacturing plants combined in Italy and Germany.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Drivers

4.2 Market Restraints

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Threat of New Entrants

4.3.2 Bargaining Power of Buyers/Consumers

4.3.3 Bargaining Power of Suppliers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Billion)

5.1 By Application

5.1.1 Automotive

5.1.2 Electrical and Electronics

5.1.3 Industrial

5.1.4 Other Applications

5.2 By Process

5.2.1 Pressure Die Casting

5.2.2 Vacuum Die Casting

5.2.3 Squeeze Die Casting

5.2.4 Other Processes

5.3 By Raw Material

5.3.1 Aluminum

5.3.2 Maginesium

5.3.3 Zinc

5.4 Geography

5.4.1 North America

5.4.1.1 United States

5.4.1.2 Canada

5.4.1.3 Rest of North America

5.4.2 Europe

5.4.2.1 United Kingdom

5.4.2.2 France

5.4.2.3 Germany

5.4.2.4 Italy

5.4.2.5 Russia

5.4.2.6 Rest of Europe

5.4.3 Asia-Pacific

5.4.3.1 China

5.4.3.2 India

5.4.3.3 Japan

5.4.3.4 Australia

5.4.3.5 Thailand

5.4.3.6 Malaysia

5.4.3.7 Indonesia

5.4.3.8 South Korea

5.4.3.9 Rest of Asia-Pacific

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Rest of South America

5.4.5 Middle-East and Africa

5.4.5.1 South Africa

5.4.5.2 Turkey

5.4.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Vendor Market Share

6.2 Company Profiles

6.2.1 Form Technologies Inc. (Dynacast)

6.2.2 Nemak

6.2.3 Endurance Technologies Limited

6.2.4 Sundaram Clayton Ltd

6.2.5 Shiloh Industries

6.2.6 Georg Fischer Limited

6.2.7 Koch Enterprises (Gibbs Die Casting Group)

6.2.8 Bocar Group

6.2.9 Engtek Group

6.2.10 Rheinmetall AG (Rheinmetall Automotive, formerly KSPG AG)