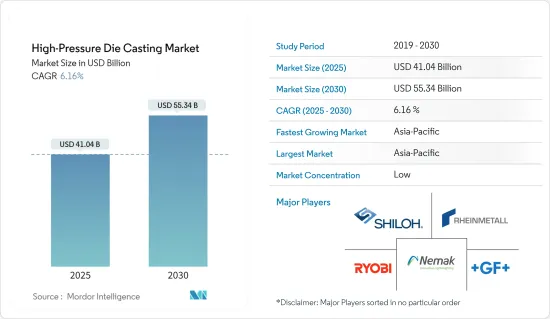

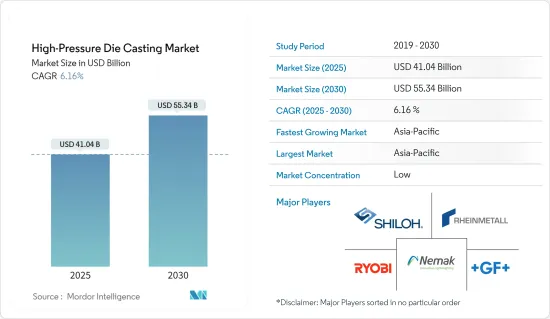

고압 다이캐스트(HPDC) 시장 규모는 2025년에 410억 4,000만 달러, 2030년에는 553억 4,000만 달러에 달할 것으로 예측됩니다. 예측기간(2025-2030년)의 CAGR은 6.16%를 나타낼 전망입니다.

세계 전기자동차로의 전환과 연비 기준의 엄격화로 인해 경량이고 내구성 있는 자동차 부품에 대한 수요가 증가하고 있는 것이 고압 다이캐스트(HPDC) 시장을 견인하고 있습니다. 자동차 제조업체가 자동차의 항속거리를 연장하고 배출가스를 줄이기 위해, HPDC는 높은 치수 정밀도와 우수한 표면 마감으로 복잡한 형상을 생산할 수 있기 때문에 지지되어 가볍고 구조적으로 견고한 부품 제조에 이상적입니다.

이러한 요구는 자동차 업계가 전동화로의 전환을 추진하고 있는 것으로 더욱 높아지고 있으며, 배터리 프레임이나 모터 하우징 등 전동 파워트레인 특유의 요구에 견디는 부품의 개발이 필요해지고 있습니다. 그 결과 HPDC 시장은 엄청난 성장을 이루고 있으며 각 제조업체는 이러한 진화하는 요구 사항을 충족하기 위해 신기술에 대한 투자와 생산 능력을 확대하고 있습니다.

고압 다이캐스팅 산업은 특히 전기자동차의 경량적이고 구조적으로 효율적인 부품에 대한 수요가 증가함에 따라 기술에 대한 투자와 생산 능력의 확대라는 중요한 동향을 경험하고 있습니다. 자동차 산업이 전동화로 전환함에 따라 HPDC 시장의 기업은 부품의 성능과 중량 효율을 높이는 혁신에 주력하고 있습니다. 이러한 추세는 지속가능성과 연료 효율성 향상을 목표로 하는 광범위한 산업의 움직임을 반영합니다.

자동차 산업은 고압 다이캐스팅(HPDC) 시장에서 주요 부문이며, 주로 알루미늄 사용량의 급증과 EV 생산의 급증에 의해 견인되고 있습니다. 경량 소재로의 이동은 주로 연비와 배기가스 규제의 엄격화에 대응할 필요성 때문에 자동차 산업에서 중요한 원동력이 되고 있습니다.

이러한 경향은 기존의 내연 엔진 차량보다 알루미늄을 많이 사용하는 전기자동차의 생산에서 특히 두드러집니다. 자동차의 알루미늄 사용량 증가는 복잡하고 완성도가 높은 부품의 효율적이고 지속 가능한 생산을 가능하게 하는 HPDC에 대한 자동차 산업의 요구와 일치합니다. 게다가 EV 생산의 급증은 자동차 산업에서 HPDC의 중요성을 더욱 두드러뜨리고 있습니다.

이러한 EV 생산 증가로 인해 HPDC 부품이 더 많이 필요합니다. 특히 차량 성능을 저하시키지 않고 배터리의 중량 증가에 대응하는 경량 구조 부품이 필요하기 때문입니다.

아시아태평양은 세계의 고압 다이캐스트 시장을 독점하고 예측 기간 동안 가장 빠른 성장률을 보여줄 것으로 기대됩니다. 아시아태평양에서는 중국, 인도, 일본 등의 국가들이 시장에서 중요한 역할을 할 것으로 보입니다.

저연비 차량의 인기 증가와 다이캐스트 기술의 최신 발전은 시장 개척에 더욱 기여할 것으로 예상됩니다. 이러한 장점으로 인해 이 지역의 자동차 제조업체는 원재료의 지속적인 공급과 공장 확장 등을 위해 장기 계약을 맺고 있습니다.

소비자의 선호와 국제 기준을 충족하는 제품을 생산하기 위해 주조는 기술 혁신의 개선에 중점을 두고 시장 기업에게 새로운 기회를 제공합니다. 주조 기업은 아시아태평양 고압 다이캐스트 시장의 주요 시장 성장 촉진요인인 기술 품질과 브랜드 지향에 주력하고 있습니다. 이러한 개발과 사례는 아시아태평양 국가의 전체 시장 개척에 기여할 것으로 보입니다.

고압 다이 캐스팅 시장은 매우 세분화되어 있으며 세계에 많은 지역 및 국제 기업이 있습니다. 최근의 동향에서는 신흥국으로부터 많은 중소규모의 기업이 시장에 진입해, 사업을 확대하고 있기 때문에 시장 경쟁은 격화하고 있습니다. 시장에서 인정받는 기업으로는 Nemak, Georg Fischer Automotive, Ryobi Die Casting, Rheinmetall AG, Form Technologies Inc.(Dynacast), Shiloh Industries 등이 있습니다. 기타 주요 기업으로는 Koch Enterprise, Linamar Corporation, Bocar Group 등이 있습니다.

HPDC 시장의 주요 기업은 기술적 진보, 업무 효율성 개선, 전략적 확장에 적극적으로 노력하고 있으며, 제품 제공을 강화하고, 특히 전기자동차로의 전환에 따라 진화하는 자동차 시장에서의 지위를 높이고 있습니다. 이러한 전략적 움직임은 전통적인 자동차와 전기자동차 모두에서 고품질의 정밀 부품에 대한 수요 증가에 대응하여 시장 점유율을 높이는 것을 목표로합니다.

The High-Pressure Die Casting Market size is estimated at USD 41.04 billion in 2025, and is expected to reach USD 55.34 billion by 2030, at a CAGR of 6.16% during the forecast period (2025-2030).

Increasing demand for lightweight yet durable automotive components, driven by a global shift toward electric vehicles and more stringent fuel efficiency standards, is driving the high-pressure die casting (HPDC) market. As automotive manufacturers aim to extend the range and reduce the emissions of their vehicles, HPDC is favored for its ability to produce complex shapes with high dimensional accuracy and excellent surface finish, making it ideal for creating components that are both lightweight and structurally robust.

This need is further amplified by the automotive industry's ongoing transition to electrification, which necessitates the development of components that can withstand the unique demands of electric powertrains, such as battery frames and motor housings. As a result, the HPDC market is experiencing substantial growth, with manufacturers investing in new technologies and expanding capacity to meet these evolving requirements.

The high-pressure die-casting industry is experiencing a key trend with increased investments in technology and capacity expansion, driven by the growing demand for lightweight and structurally efficient components, especially in electric vehicles. As the automotive industry shifts toward electrification, companies within the HPDC market are focusing on innovations that enhance the performance and weight efficiency of their components. This trend is reflective of a broader industry movement toward sustainability and increased fuel efficiency. For instance,

The automotive industry is the predominant segment within the high-pressure die casting (HPDC) market, primarily driven by the surge in aluminum usage and the escalating production of EVs. The shift toward lightweight materials is a critical driver in the automotive industry, primarily due to the need to meet stricter fuel economy and emissions standards.

This trend is particularly pronounced in the production of electric vehicles, which are more aluminum-intensive than traditional combustion engine vehicles. The increased aluminum usage in vehicles aligns with the automotive industry's needs for HPDC as it allows for the efficient and sustainable production of complex, high-integrity parts. Furthermore, the surge in EV production further underscores the importance of HPDC in the automotive industry.

This increase in EV production necessitates more HPDC parts, particularly because of the need for lightweight structural components that accommodate the additional weight of batteries without compromising vehicle performance.

The Asia-Pacific region is expected to dominate the global high-pressure die-casting market, and it is also expected to witness the fastest growth rate during the forecast period. In the Asia-Pacific region, countries like China, India, and Japan are likely to play a key role in the market.

The increasing popularity of fuel-efficient vehicles and the latest advancements in die-casting techniques are expected to further contribute to the market's development. Thus, due to such benefits, automakers in the region are entering long-term deals for uninterrupted supply of raw materials, expansion of plants, etc.

The growing focus of foundries on improving innovation to produce products that meet consumer preferences and international standards offers new opportunities for players in the market. Foundries are focusing on technical quality and brand orientation, which are considered major growth drivers for the Asia-Pacific high-pressure die-casting market. Such developments and instances are likely to contribute to the overall development of the market across Asia-Pacific countries.

The high-pressure die-casting market is highly fragmented, with the presence of many regional and international players worldwide. Competition in the market has increased, as many small- and medium-scale players from developing countries have entered and expanded their business in the market over recent years. Some of the recognized players in the market are Nemak, Georg Fischer Automotive, Ryobi Die Casting, Rheinmetall AG, Form Technologies Inc. (Dynacast), and Shiloh Industries. Some other notable players include Koch Enterprise, Linamar Corporation, and Bocar Group.

Major players in the HPDC market are actively engaging in technological advancements, operational efficiency improvements, and strategic expansions to enhance their product offerings and better position themselves in the evolving automotive market, especially with the shift toward electric vehicles. These strategic moves are aimed at capturing a larger share of the market by meeting the increasing demands for high-quality, precision components in both conventional and electric vehicles.