ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

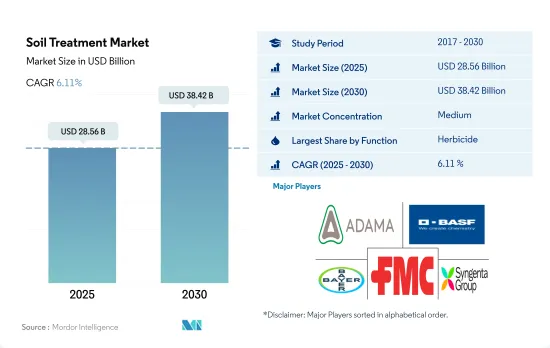

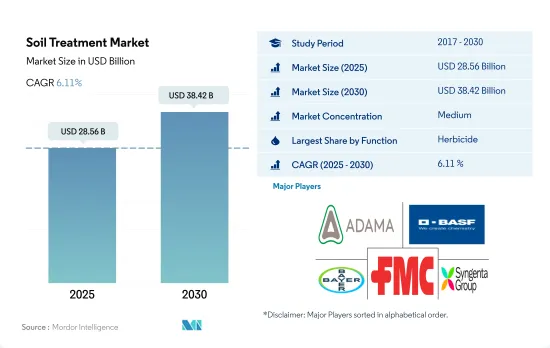

토양 처리 시장 규모는 2025년에 285억 6,000만 달러로 추정되고, 2030년에는 384억 2,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR은 6.11%를 나타낼 전망입니다.

제초제는 토양 처리 방법을 통한 효과로 시장을 지배

제초제는 2022년 토양 처리 방법의 활용도에서 72.8%로 가장 높은 점유율을 차지했습니다.

무경운 및 최소 경운 농법을 포함한 현대식 농법을 채택하는 추세가 증가하고 있습니다.

살충제는 2022년 전 세계의 토양 처리 시장에서 12.8%의 점유율을 차지할 것으로 예상됩니다.

토양 처리 살균제의 활용은 주로 곡물과 곡류에 집중되어 있으며, 시장에서 45.4%의 가장 큰 점유율을 차지하고 있습니다.

알디카브, 페나미포스, 옥사밀과 같은 선충제의 토양 처리는 다양한 작물에서 상당한 손실을 유발하는 것으로 알려진 멜로이도진 인코그니타, 프라틸렌쿠스 브라치유러스 같은 미세 선충을 효과적으로 방제하는 데 사용될 수 있습니다.

앞서 언급한 요인으로 인해 토양 처리 시장은 성장할 것으로 예상됩니다.

주요 국가에서 해충으로 인한 수확량 손실이 증가함에 따라 토양 처리의 사용이 증가

토양 매개 해충은 전 세계적으로 농업과 생태계에 큰 영향을 미칠 수 있습니다. 이러한 해충에는 토양에 서식하며 농작물에 피해를 주고 수확량을 감소시키며 생태계를 교란하는 선충, 곰팡이, 박테리아, 곤충 등이 포함됩니다. 해충을 효과적으로 관리하는 것은 식량 안보를 보장하고 안정적인 식량 공급을 유지하는 데 필수적입니다.

2022년 남미의 토양 처리 부문은 전 세계 시장에서 34.2%의 상당한 점유율을 차지할 것으로 예상됩니다. 재배자들은 일반적으로 토양 처리를 위해 토양 관주, 살포, 고랑 살포 기술을 사용합니다. 이러한 방법을 통해 토양 매개성 질병과 해충의 방제를 강화하면 작물 수확량이 향상됩니다. 토양 건강 보존에 대한 중요성이 강조되면서 농부들은 이러한 토양 처리 방법을 채택하게 되었습니다.

북미는 전 세계 시장 점유율 29.6%를 차지하며 두 번째로 큰 국가입니다. 토양 매개성 질병은 농작물 생산의 주요 제약 요인으로 꼽힙니다. 토양 매개 식물 병원균인 리족토니아(Rhizoctonia spp.), 푸사리움(Fusarium spp.), 버티실리움(Verticillium spp.), 스클로티니아(Sclerotinia spp.), 피튬(Pythium spp.), 피토포라(Phytophthora spp.) 등은 밀, 면화, 옥수수, 채소, 과일, 관상용 등 많은 작물에 50-75%의 수확량 손실을 유발할 수 있습니다.

따라서 세계의 토양처리 시장가치는 2023년과 2029년 사이에 CAGR 5.0%로 성장할 것으로 예상되며 기후 변화와 해충 침입으로 인한 작물 손실 증가로 인해 모든 작물 유형에서 상당한 성장을 목격 할 것으로 예상됩니다.

세계의 토양 처리 시장 동향

토양 매개 해충, 질병 및 잡초의 감염이 증가함에 따라 농약의 토양 처리 헥타르당 소비량은 전 세계적으로 증가 할 가능성이 높습니다.

토양 살포 방식을 통한 작물보호제의 전 세계 평균 소비량은 2022년 농경지 1ha당 2,345.0g으로 2017년 1ha당 2,065.0g에 비해 13.6% 증가했습니다.

무경운 및 최소 경운 농법을 포함한 현대식 농법의 채택이 증가함에 따라 토양 내 해충 개체수가 증가하여 해충, 잡초 및 토양 매개 질병을 방제하기 위한 농약의 토양 살포가 필요해졌습니다.

제초제, 특히 전착성 제초제는 일반적으로 잡초 종자를 표적으로 삼아 작물을 파종하기 전에도 발아를 방해하기 때문에 토양에 살포됩니다. 이 접근 방식은 잡초 개체군을 사전에 선제적으로 관리하여 작물의 생육과 전반적인 잡초 방제를 개선할 수 있다는 점에서 인기를 얻고 있습니다.

흰 땅벌레의 침입은 대두의 경우 뿌리 시스템을 약 25%, 옥수수의 경우 64% 감소시켰습니다. 브라질과 같은 남미 국가에서는 필로파가 카필라타와 에곱시스 볼보세리두스가 모든 평가 변수를 손상시켜 전체 대두 생산성을 58.62%, 옥수수 생산성을 59.76% 감소시키는 것으로 관찰되었습니다. 이러한 모든 토양 매개 해충은 살충제를 토양에 살포하면 효과적으로 방제할 수 있습니다.

마찬가지로 Meloidogyne incognita와 Pratylenchus brachyurus와 같은 선충은 과일과 채소 작물에 상당한 손실을 초래합니다. 예를 들어 당근은 평균 20.0%에 달하는 상당한 손실을 입기 쉽습니다.

토양 매개 질병 방제의 필요성에 따라 토양 처리 살충제 사용량이 증가

농약 시장의 역동적인 환경 속에서 토양 처리 농약은 중요한 구성 요소로 주목받고 있습니다.

사이퍼메트린은 토양 처리용 살충제로 사용할 수 있는 피레스로이드계 살충제입니다. 토양에 적용하면 흰개미와 뿌리 구더기를 비롯한 다양한 토양 매개 해충을 효과적으로 방제할 수 있습니다. 사이퍼메트린의 작용 방식은 해충과 접촉하면 해충의 신경계를 표적으로 삼아 마비를 일으켜 결국 사망에 이르게 하는 것입니다.

말라티온은 농경지 및 비농경지에서 다양한 해충을 방제하기 위해 토양 처리제로 사용되는 유기인계 살충제입니다. 농작물 및 기타 식물에 피해를 줄 수 있는 날벌레와 기는 벌레를 모두 방제하는 데 효과적입니다.

만코제브는 댐핑오프, 마름병, 노균병 등 다양한 곰팡이병을 방제하는 데 사용되는 살균제이자 토양 처리제입니다.

토양 처리 산업 개요

토양 처리 시장은 적당히 통합되어 상위 5개사에서 44.67%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. ADAMA Agricultural Solutions Ltd, BASF SE, Bayer AG, FMC Corporation, Syngenta Group (알파벳 순)

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

1헥타르당 농약 소비량

유효성분의 가격 분석

규제 프레임워크

아르헨티나

호주

브라질

캐나다

칠레

중국

프랑스

독일

인도

인도네시아

이탈리아

일본

멕시코

미얀마

네덜란드

파키스탄

필리핀

러시아

남아프리카

스페인

태국

우크라이나

영국

미국

베트남

밸류체인과 유통채널 분석

제5장 시장 세분화

기능

살균제

제초제

살충제

연체 동물 살충제

선충제

작물 유형

상업용 작물

과일 및 채소

곡물

콩류 및 유지 종자

잔디 및 관상용

지역

아프리카

국가별

남아프리카

기타 아프리카

아시아태평양

국가별

호주

중국

인도

인도네시아

일본

미얀마

파키스탄

필리핀

태국

베트남

기타 아시아태평양

유럽

국가별

프랑스

독일

이탈리아

네덜란드

러시아

스페인

우크라이나

영국

기타 유럽

북미

국가별

캐나다

멕시코

미국

기타 북미

남미

국가별

아르헨티나

브라질

칠레

기타 남미 국가

제6장 경쟁 구도

주요 전략적 움직임

시장 점유율 분석

기업 상황

기업 프로파일

ADAMA Agricultural Solutions Ltd

American Vanguard Corporation

BASF SE

Bayer AG

FMC Corporation

Nufarm Ltd

PI Industries

Rallis India Ltd

Syngenta Group

UPL Limited

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

출처 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

HBR

영문 목차

영문목차

The Soil Treatment Market size is estimated at 28.56 billion USD in 2025, and is expected to reach 38.42 billion USD by 2030, growing at a CAGR of 6.11% during the forecast period (2025-2030).

Herbicides dominate the market due to their effectiveness through soil treatment methods

Herbicides accounted for the highest share of 72.8% in the utilization of soil treatment methods in 2022. These herbicides specifically target weed seeds, impeding their germination even prior to crop sowing. This approach has gained popularity due to its ability to proactively manage weed populations proactively, ensuring better crop establishment and overall weed control.

There is a growing trend toward adopting modern farming practices, including no-till and minimum-till farming. Herbicides may be applied through the soil treatment method with precision, targeting specific areas in the field where weed pressure is high, thereby optimizing herbicide use and reducing costs. These factors are driving the adoption of soil treatment for herbicide applications.

Insecticides accounted for a share of 12.8% of the global soil treatment market in 2022. Although the pupae and eggs in the soil are not affected by the normal doses of pesticides, larval and adult stages may be controlled by soil treatment. Pests like white grubs, wireworms, fungus gnats, and soil mealybugs may effectively be managed by soil application.

The utilization of soil treatment fungicides was predominantly focused on grains and cereals, representing the largest value share of 45.4% in the market. This preference is driven by the effectiveness of fungicides in protecting the quality of grains and cereals, as they help prevent or reduce fungal infections.

The soil treatment of nematicides like aldicarb, fenamiphos, and oxamyl may effectively be employed in controlling microscopic nematodes like Meloidogyne incognita and Pratylenchus brachyurus that are known to cause significant losses in various crops.

Owing to the aforementioned factors, the market for soil treatment is anticipated to grow.

The rise in yield losses in major countries due to pests is driving the use of soil treatment

Soil-borne pests may have a significant global impact on agriculture and ecosystems. These pests include nematodes, fungi, bacteria, and insects that live in the soil and can damage crops, reduce yields, and disrupt ecosystems. Managing pests effectively is essential for ensuring food security and maintaining a stable food supply.

In 2022, the soil treatment segment in South America held a substantial 34.2% share of the global market. From 2017 to 2022, the region witnessed a noteworthy increase in market value, accounting for USD 8,568.9 million in 2022. Growers commonly employ soil drenching, broadcast, and furrow application techniques for soil treatment. Enhancing the control of soil-borne diseases and pests through these methods improves crop yields. The growing emphasis on preserving soil health has prompted farmers to embrace these soil treatment approaches.

North America is the second leading country, holding a substantial 29.6% global market share. Soil-borne diseases are considered a major limitation of crop production. Soil-borne plant pathogens such as Rhizoctonia spp., Fusarium spp., Verticillium spp., Sclerotinia spp., Pythium spp., and Phytophthora spp. can cause 50% to 75% yield loss for many crops such as wheat, cotton, maize, vegetables, fruits, and ornamentals.

Therefore, the global soil treatment market value is expected to register a CAGR of 5.0% during 2023-2029 and is anticipated to witness significant growth in all crop types due to the changing climate and rising crop losses due to pest infestation.

Global Soil Treatment Market Trends

The increasing infestation of soil borne pest, diseases, and weeds, the per hectare consumption of soil treatment of pesticides is likely to increase globally

The global average consumption of crop protection chemicals through soil application mode was recorded as 2,345.0 g per ha of agricultural land in 2022, which increased by 13.6% compared to 2017, which was 2,065.0 g per ha.

The growing trend toward the adoption of modern farming practices, including no-till and minimum-till farming, is increasing the pest population in the soil, necessitating the soil application of pesticides to control pests, weeds, and soil-borne diseases.

Herbicides, specifically pre-emergent herbicides, are generally applied to soil as they specifically target weed seeds, impeding their germination even prior to crop sowing. This approach has gained popularity due to its ability to proactively manage weed populations proactively, ensuring better crop establishment and overall weed control.

The white grub infestation reduced the root system by approximately 25% in soybeans and 64% in maize. It was observed that Phyllophaga capillata and Aegopsis bolboceridus damaged all evaluated variables, reducing overall soybean productivity by 58.62% and maize productivity by 59.76% in South American countries like Brazil. All these soil-borne pests may effectively be controlled by soil application of insecticides.

Similarly, nematodes like Meloidogyne incognita and Pratylenchus brachyurus cause significant losses in fruit and vegetable crops. For instance, carrots are susceptible to considerable losses, averaging up to 20.0%. As these parasitic nematodes are soil-dwelling organisms, it is important to treat the soil with nematicides to kill these organisms.

Soil treatment pesticide usage is increasing with the need for controlling soil-borne diseases

Amid the dynamic landscape of the pesticide market, soil treatment pesticides stand out as crucial components. These specialized chemicals play a pivotal role in fostering healthy crop growth, effective pest and disease control, and sustainable agricultural practices.

Cypermethrin is a pyrethroid insecticide that may be used as a soil treatment pesticide. When applied to the soil, it provides effective control against a variety of soil-borne pests, including termites and root maggots. Cypermethrin's mode of action involves targeting the nervous system of the pests upon contact, leading to paralysis and eventual death. It was priced at USD 21.0 thousand per metric ton in 2022.

Atrazine is an herbicide commonly used as a soil treatment to control various broadleaf and grassy weeds in agricultural fields and non-crop areas. It is particularly effective in managing weed populations that compete with crops for nutrients, water, and sunlight. In 2022, it was priced at USD 13.8 thousand per metric ton.

Malathion is an organophosphate insecticide used as a soil treatment to control a variety of insect pests in agricultural fields and non-crop areas. It is effective in managing both flying and crawling insects that may cause damage to crops and other plants. Malathion was priced at USD 12.5 thousand per metric ton.

Mancozeb is a fungicide and soil treatment used to control various fungal diseases such as damping-off, blight, and downy mildew. It belongs to the class of dithiocarbamates and is known for its broad-spectrum activity against a wide range of plant pathogens. In 2022, it was priced at USD 7.8 thousand per metric ton.

Soil Treatment Industry Overview

The Soil Treatment Market is moderately consolidated, with the top five companies occupying 44.67%. The major players in this market are ADAMA Agricultural Solutions Ltd, BASF SE, Bayer AG, FMC Corporation and Syngenta Group (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Consumption Of Pesticide Per Hectare

4.2 Pricing Analysis For Active Ingredients

4.3 Regulatory Framework

4.3.1 Argentina

4.3.2 Australia

4.3.3 Brazil

4.3.4 Canada

4.3.5 Chile

4.3.6 China

4.3.7 France

4.3.8 Germany

4.3.9 India

4.3.10 Indonesia

4.3.11 Italy

4.3.12 Japan

4.3.13 Mexico

4.3.14 Myanmar

4.3.15 Netherlands

4.3.16 Pakistan

4.3.17 Philippines

4.3.18 Russia

4.3.19 South Africa

4.3.20 Spain

4.3.21 Thailand

4.3.22 Ukraine

4.3.23 United Kingdom

4.3.24 United States

4.3.25 Vietnam

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

5.1 Function

5.1.1 Fungicide

5.1.2 Herbicide

5.1.3 Insecticide

5.1.4 Molluscicide

5.1.5 Nematicide

5.2 Crop Type

5.2.1 Commercial Crops

5.2.2 Fruits & Vegetables

5.2.3 Grains & Cereals

5.2.4 Pulses & Oilseeds

5.2.5 Turf & Ornamental

5.3 Region

5.3.1 Africa

5.3.1.1 By Country

5.3.1.1.1 South Africa

5.3.1.1.2 Rest of Africa

5.3.2 Asia-Pacific

5.3.2.1 By Country

5.3.2.1.1 Australia

5.3.2.1.2 China

5.3.2.1.3 India

5.3.2.1.4 Indonesia

5.3.2.1.5 Japan

5.3.2.1.6 Myanmar

5.3.2.1.7 Pakistan

5.3.2.1.8 Philippines

5.3.2.1.9 Thailand

5.3.2.1.10 Vietnam

5.3.2.1.11 Rest of Asia-Pacific

5.3.3 Europe

5.3.3.1 By Country

5.3.3.1.1 France

5.3.3.1.2 Germany

5.3.3.1.3 Italy

5.3.3.1.4 Netherlands

5.3.3.1.5 Russia

5.3.3.1.6 Spain

5.3.3.1.7 Ukraine

5.3.3.1.8 United Kingdom

5.3.3.1.9 Rest of Europe

5.3.4 North America

5.3.4.1 By Country

5.3.4.1.1 Canada

5.3.4.1.2 Mexico

5.3.4.1.3 United States

5.3.4.1.4 Rest of North America

5.3.5 South America

5.3.5.1 By Country

5.3.5.1.1 Argentina

5.3.5.1.2 Brazil

5.3.5.1.3 Chile

5.3.5.1.4 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

6.4.1 ADAMA Agricultural Solutions Ltd

6.4.2 American Vanguard Corporation

6.4.3 BASF SE

6.4.4 Bayer AG

6.4.5 FMC Corporation

6.4.6 Nufarm Ltd

6.4.7 PI Industries

6.4.8 Rallis India Ltd

6.4.9 Syngenta Group

6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS