ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

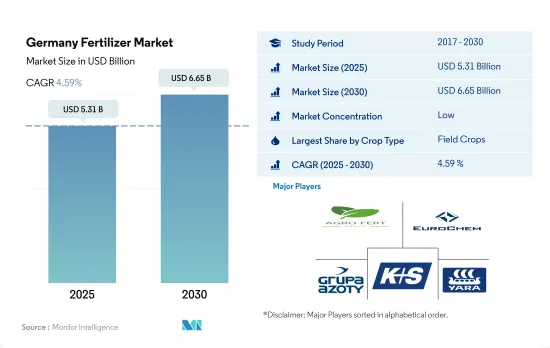

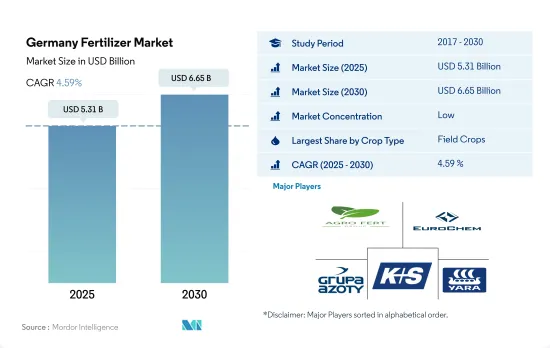

독일의 비료 시장 규모는 2025년에 53억 1,000만 달러로 추정되며, 2030년에는 66억 5,000만 달러에 달할 것으로 예상되며, 예측 기간(2025-2030년) 동안 4.59%의 CAGR로 성장할 것으로 예상됩니다.

집약적 농법이 비료 소비를 증가시키고 있습니다.

독일은 유럽에서 4번째로 큰 농업 국가로 국토의 57% 이상을 농업이 차지하고 있으며, 1헥타르당 평균 61헥타르의 소규모 농가가 27만 6,000여 가구에 달합니다. 토양의 종류가 다양하기 때문에 농부들은 영양 부족에 대처하고 작물의 성장과 품질을 최적화하기 위해 비료의 사용량을 조정하고 있습니다.

최근 몇 년 동안 독일에서는 비료 사용량이 눈에 띄게 증가하여 2022년 비료 사용량이 전년 대비 2.9% 증가했는데, 이는 독일의 기후 조건이 크게 영향을 미쳤습니다. 농부들은 가뭄과 폭염에 시달리고 식량 안보를 지키기 위해 비료와 작물 보호 제품에 크게 의존했습니다.

2022년에는 밭작물이 56.4%를 차지하여 비료 소비의 대부분을 차지했습니다. 이는 주로 경작 면적의 확대, 집약적인 농법, 지속적인 경작으로 인한 영양 부족을 해결해야 할 필요성에 기인합니다. 밀, 보리, 유채, 콩이 주요 작물로서 선두를 달리고 있습니다. 독일은 재배면적 확대를 통해 국내 콩과 작물 생산에 중점을 두고 있으며, 2023년부터 2030년까지 CAGR 3.7%로 예측되어 밭작물 시장을 견인할 것으로 보입니다.

잔디 및 관상용 작물 분야는 독일에서 두 번째로 큰 시장 점유율을 차지하고 있으며, 2022년에는 35.9%에 달했습니다. 이러한 작물은 다양한 용도로 수요가 증가하고 있습니다. 이에 따라 농부들은 작물의 성장과 품질을 보장하기 위해 작물 영양에 대한 의존도를 높이고 있습니다. 이러한 수요 증가는 향후 몇 년 동안 시장을 주도할 것으로 예상됩니다.

독일의 비료 시장 동향

가뭄과 폭염이 밭작물 재배에 미치는 영향

2022년에는 밭작물이 독일 재배면적의 78.2%를 차지했습니다. 이러한 우위는 식량 안보를 보장하고 농업 부문에 경제적으로 중요한 작물로서의 역할을 수행하는 이중적 의미에서 비롯됩니다. 조사 기간 동안 밭작물 재배 면적은 크게 감소하여 2017년 밭작물 재배 면적은 735만 헥타르였으나 2022년에는 161만 헥타르가 감소한 574만 헥타르가 되었습니다. 이처럼 밭작물 재배 면적이 눈에 띄게 감소한 것은 최근 몇 년간의 가뭄과 폭염의 악영향으로 수확량이 크게 감소했기 때문입니다. 그 결과, 농부들은 이러한 가혹한 기후 조건에 대응하기 위해 재배 면적을 줄이는 것을 선택했습니다. 밀, 유채, 옥수수, 콩이 주요 재배 작물입니다.

밀은 가장 광범위하게 재배되는 작물로서 주도권을 쥐고 있으며, 이 지역의 두 번째 생산자이며, 2022년 밀의 경작 면적은 전체 경작지의 49.8%를 차지했습니다. 이러한 우위는 국내 시장과 국제 시장에서 밀에 대한 수요가 증가하고 있는 것이 주요 원인입니다. 2022년 밀 재배 면적은 2017년 대비 약 7% 감소하여 298만 헥타르에 이르렀으며, 이는 주로 건조하고 더운 기후 조건으로 인해 여름 밀의 수확 면적이 45% 감소하고 겨울 밀의 수확 면적이 1.4% 감소했기 때문입니다.

콩과 작물의 재배 면적은 2022년 46.3% 증가했지만, 이는 주로 국내 생산에 대한 의존도가 높기 때문입니다.

질소는 밭작물이 소비하는 주요 영양소입니다.

2022년 독일의 밭작물 평균 양분 시용량은 1헥타르당 177.2kg이었습니다. 특히 옥수수, 쌀, 밀, 밀, 사탕수수, 콩, 유채, 면화는 주요 밭작물이며, 이들 작물은 생육을 지원하기 위해 높은 영양소 수준을 요구합니다. 집약적인 농법과 밀과 같은 주요 작물의 지속적인 재배로 인한 영양분 부족은 영양분 시용의 증가를 필요로 합니다. 이러한 상황에서는 토양의 비옥도를 유지하기 위해 더 많은 양분 투입이 필요합니다.

질소는 모든 주요 양분 중에서 밭작물이 소비하는 주요 양분으로 눈에 띕니다. 질소의 평균 양분 시용량은 1헥타르당 274.7kg입니다. 이 나라의 토양은 높은 pH 수준, 모래 토양 구성, 반복되는 가뭄으로 인한 지속적인 건조 상태로 인해 질소 결핍에 시달리고 있습니다. 이러한 요인들이 복합적으로 작용하여 질소 영양소에 대한 수요가 증가하고 있습니다. 칼륨은 두 번째로 많이 소비되는 1차 영양소이며, 헥타르당 평균 영양소 사용량은 142.9kg, 인의 소비량은 114.1kg입니다.

중국은 역내에서도 유채 생산량이 가장 많은 국가입니다. 유채의 평균 양분 시용량은 1헥타르당 290.5킬로그램에 달해 가장 많습니다. 유채는 질소에 크게 의존하고 있습니다. 중요한 영양소인 질소의 평균 시용량은 1헥타르당 393.7킬로그램에 달합니다. 이 작물은 양분 이용 효율이 낮기 때문에 질소 시비에 크게 의존하여 단백질 함량을 높입니다.

독일의 비료 산업 개요

독일의 비료 시장은 세분화되어 있으며, 상위 5개 기업이 32.74%를 점유하고 있습니다. 이 시장의 주요 업체는 다음과 같습니다. AGROFERT, EuroChem Group, Grupa Azoty S.A.(Compo Expert), K+S Aktiengesellschaft 및 Yara International ASA(알파벳 순으로 정렬).

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 오퍼

제3장 소개

조사 가정과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

주요 작물작부면적

밭작물

원예작물

평균 양분시용율

미량영양소

밭작물

원예작물

1차 영양소

밭작물

원예작물

2차 다량 영양소

밭작물

원예작물

관개 농지

규제 프레임워크

밸류체인과 유통 채널 분석

제5장 시장 세분화

유형

복합형

스트레이트

미량영양소

붕소

구리

철

망간

몰리브덴

아연

기타

질소

요소

기타

인산

DAP

MAP

SSP

TSP

인산염

MoP

SoP

2차 영양소

칼슘

마그네슘

유황

형태

기존

특수

CRF

액체 비료

SRF

수용성

시비 방법

시비

엽면 살포

토양

작물 유형

밭작물

원예작물

잔디·관상용

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 개요

AGLUKON Spezialduenger GmbH & Co.

AGROFERT

EuroChem Group

Grupa Azoty S.A.(Compo Expert)

ICL Group Ltd

K+S Aktiengesellschaft

Nouryon

PhosAgro Group of Companies

Sociedad Quimica y Minera de Chile SA

Yara International ASA

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보 출처와 참고문헌

도표

주요 인사이트

데이터팩

용어집

ksm

영문 목차

영문목차

The Germany Fertilizer Market size is estimated at 5.31 billion USD in 2025, and is expected to reach 6.65 billion USD by 2030, growing at a CAGR of 4.59% during the forecast period (2025-2030).

Intensive agricultural practices are increasing fertilizer consumption

Germany ranks as the fourth largest agricultural nation in the European region, with agriculture occupying over 57% of its land. The country boasts nearly 276,000 small farms, averaging 61 hectares each. Given the diverse soil types, farmers tailor their fertilizer usage to address nutrient deficiencies and optimize crop growth and quality.

In recent years, Germany has seen a notable surge in fertilizer utilization. In 2022, fertilizer usage rose by 2.9% compared to the previous year, largely influenced by the country's climatic conditions. Farmers struggled with droughts and heatwaves and relied heavily on fertilizers and crop protection products to safeguard food security.

In 2022, field crops dominated fertilizer consumption, accounting for 56.4%. This is primarily due to their expansive cultivation areas, intensive agricultural practices, and the need to address nutrient deficiencies resulting from continuous cultivation. Wheat, barley, rapeseed, and soybean take the lead as major crops. Germany's emphasis on domestic legume production, achieved through expanding cultivation areas, is set to drive the field crops market with a projected CAGR of 3.7% from 2023 to 2030.

The turf and ornamental crop segment claims the second-largest market share in Germany, standing at 35.9% in 2022. These crops are witnessing heightened demand across various applications. Farmers, in response, are increasingly relying on crop nutrition to ensure robust growth and quality. This rising demand is poised to propel the market in the coming years.

Germany Fertilizer Market Trends

Droughts and heat waves impacted the cultivation of field crops

In 2022, field crops dominated Germany's cultivation area, accounting for 78.2%. This prominence can be attributed to their dual significance in guaranteeing food security and serving as economically vital crops for the agricultural sector. A substantial decline in the cultivation area of field crops was observed during the study period. In 2017, the total cultivation area dedicated to field crops accounted for 7.35 million hectares, but by 2022, it had reduced by 1.61 million hectares and reached 5.74 million hectares. This noteworthy reduction in the country's field crop acreage can be attributed to the adverse impacts of recent droughts and persistent heat waves, which led to significant yield losses. Consequently, farmers opted to reduce their cultivation areas in response to these challenging climatic conditions. Wheat, rapeseed, corn, and soybean are major cultivating crops.

Wheat takes the lead as the most extensively cultivated crop and is the region's second-largest producer. In 2022, the wheat cultivation area comprised a substantial 49.8% of the total cultivated land. This predominance can be majorly attributed to the escalating demand for wheat both within the domestic market and on the international market. The wheat cultivation area reduced drastically by approximately 7% compared to the year 2017. In 2022, it accounted for 2.98 million hectares, which is majorly due to a reduction in summer wheat harvesting area, down by 45%, and winter wheat harvesting area by 1.4%, due to dry and hot climatic conditions.

The legume crop cultivation area increased in 2022 by 46.3%, which was majorly due to the country's dependence on domestic production.

Nitrogen is the main primary nutrient consumed by the field crops

In the year 2022, the average nutrient application rate of field crops stood at 177.2 kg per hectare in Germany. Notably, corn, rice, wheat, sorghum, soybean, rapeseed, and cotton represent the primary field crops cultivated, and they demand higher nutrient levels to support their growth. The nutrient deficiency arising from intensive agricultural practices and the continuous cultivation of major crops, such as wheat, necessitates an increased application of nutrients. This situation calls for higher nutrient input to maintain soil fertility.

Nitrogen stands out as the predominant nutrient consumed by field crops among all the primary nutrients. The average nutrient application rate for nitrogen is a substantial 274.7 kg per hectare. The country's soils experience nitrogen deficiency due to its high pH levels, sandy soil composition, and persistent dry conditions resulting from recurrent droughts. These factors collectively drive an increased demand for nitrogen nutrients in the country's agricultural practices. Potash is the second most consumed primary nutrient, with an average nutrient application rate of 142.9 kg per hectare, and phosphorus consumption accounts for 114.1 kg per hectare.

The country holds a prominent position as a leading producer of oil rapeseed within the region. The rapeseed crop exhibits the highest average nutrient application rate, reaching 290.5 kilograms per hectare. The oil rapeseed crop relies heavily on nitrogen. It is notable that the average nutrient application rate for this crucial nutrient stands at 393.7 kilograms per hectare. This crop heavily depends on nitrogen fertilization due to its lower nutrient use efficiency, and while this enhances protein content.

Germany Fertilizer Industry Overview

The Germany Fertilizer Market is fragmented, with the top five companies occupying 32.74%. The major players in this market are AGROFERT, EuroChem Group, Grupa Azoty S.A. (Compo Expert), K+S Aktiengesellschaft and Yara International ASA (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Acreage Of Major Crop Types

4.1.1 Field Crops

4.1.2 Horticultural Crops

4.2 Average Nutrient Application Rates

4.2.1 Micronutrients

4.2.1.1 Field Crops

4.2.1.2 Horticultural Crops

4.2.2 Primary Nutrients

4.2.2.1 Field Crops

4.2.2.2 Horticultural Crops

4.2.3 Secondary Macronutrients

4.2.3.1 Field Crops

4.2.3.2 Horticultural Crops

4.3 Agricultural Land Equipped For Irrigation

4.4 Regulatory Framework

4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)