ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

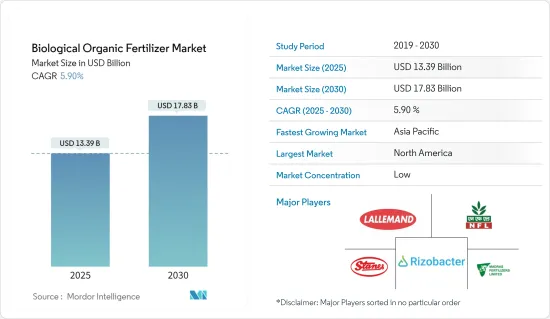

생물학적 유기 비료 시장 규모는 2025년에 133억 9,000만 달러에 달할 것으로 추정됩니다. 예측 기간(2025-2030년)의 CAGR은 5.9%를 나타낼 것으로 예상되고, 2030년에는 178억 3,000만 달러에 이를 것으로 전망됩니다.

주요 하이라이트

생물학적 유기 비료 시장의 성장을 지원하는 중요한 요소 중 하나는 유기 농업의 보급입니다. 지속 가능한 농업의 중요성과 제조업체에 대한 정부의 지원은 시장 개척을 증가시키는 또 다른 요인입니다.

또한 최근 바이오 유기질 비료가 곡물에 미치는 영향에 대한 연구 결과도 발표되고 있습니다. 벼의 양분 흡수와 식물 생육 촉진 등 다양한 특성을 보인 바이오 유기질 비료는 범람원, 테라스, 염분 토양에서 분리한 바실러스, 프로테우스, 페니바실러스 등 주로 식물 성장 촉진균(PGPB)의 생세포와 RP(5%), 바이오 숯(15%)을 함유한 유기농 기반 바이오 비료입니다. 방글라데시 라이스가 수행한 16건의 현장 실험과 18건의 농가 실증 시험 결과, PGPB를 첨가하면 생물학적 질소 고정을 통해 쌀 생산에 필요한 30%의 합성 N을 보충하고 식물 성장 기간 동안 가용화를 통해 암인산염의 가용 P를 완전히 보완하는 것으로 입증되었습니다. 생물학적 유기 비료의 생물 성분과 유기물의 결합 효과는 요소-N을 30% 절감하고 쌀 생산에 100% 삼중 과인산 비료 사용을 없애는 동시에 영양소 흡수, N, P 사용 효율, 쌀 수확량 및 토양 건강을 개선하여 결국 생물학적 유기 비료의 채택을 향상시켰습니다.

생물학적 유기 비료 시장 동향

유기농업 증가

유기농 제품과 소비의 인기가 높아짐에 따라 전 세계적으로 유기농업의 확대가 강요되고 있습니다. 그 후, 재생농업, 유기농업, 토양건강에 대한 최근의 관심이 높아짐에 따라 생물학적 유기 비료 시장은 극적으로 성장하고 있습니다. 천연 유기 비료는 특정 수준의 미생물(예 : 질소 고정 박테리아)을 포함합니다. 유기 비료는 유사하게 미생물을 포함하며 일반적으로 가축의 분뇨 및 작물 잔류물과 같은 유기 농업에 매우 적합한 동식물에서 유래합니다.

유기농업연구소에 따르면 유기농업의 재배면적은 2020년에 4.1% 증가했습니다. 또한, 선진국과 신흥 국가의 지역별 통계는 국내 유기농업의 성장을 묘사하고 있습니다. 예를 들어 인도 정부의 통계에 따르면 인도의 유기농업인증 프로세스 하의 면적은 2021년부터 2022년에 걸쳐 거의 두배로 증가하였으며, 유기농업에 대한 대처와 도입이 증가하고 있음을 보여주며 총 생산량은 20,540.63톤을 차지했습니다. 이처럼 유기농 면적이 증가하고 양질의 작물에 대한 수요가 높아짐에 따라 재배농가는 과도한 합성비료 대신 바이오로지컬 유기 비료를 사용할 것으로 예상되어 시장을 견인하고 있습니다.

아시아태평양이 가장 빠르게 성장하는 시장

아시아태평양의 유기 비료 시장은 다른 모든 지역에서 가장 빠르게 성장하고 있습니다. 아시아태평양에서의 유기 비료의 소비는 바이오 및 유기 잔류물 기반 비료의 장점에 대한 농부의 의식이 증가함에 따라 증가할 것으로 예상됩니다. 이 지역 수요는 중국, 인도, 태국, 인도네시아, 베트남 등 주요 농업 국가에 집중되어 있으며 중국과 인도가 시장 개척을 이끌고 있습니다.

게다가 이 지역의 여러 나라들은 비료 전반에 대해 독자적인 규제를 마련하고 있을 뿐만 아니라 생물·유기 비료에 대해서도 특정한 요건이나 규칙을 마련하고 있는 경우가 많습니다. 예를 들어, 인도네시아에서 유기 비료, 생물학적 비료, 토양개량등록에 관한 MOA 규정 No.1/2019는 MOA가 승인한 기관에 의한 품질시험에 합격할 것을 의무화함으로써 시장에 유통되는 비료제품의 품질을 확보하는 것을 목적으로 하고 있습니다.

또한 이 지역의 여러 나라에서 유기농업이 확대되고 유기농 제품에 대한 수요가 높아지고 있는 것도 이 지역 시장을 견인하고 있습니다. 또한 일부 아시아 국가에서는 유기 부문과 관련된 주요 정책 개발이 이루어지고 있습니다. 일본에서는 2030년까지 유기농가와 유기농지의 수를 3배로 늘리는 것을 목표로 하는 농업·경영 기본계획이 크게 진전되어 시장 성장을 뒷받침하고 있습니다.

생물학적 유기 비료 산업 개요

생물학적 유기 비료 시장은 국제 및 지역 유력 기업에 의해 단편화되었습니다. 정부 조직과의 협력, 시장 확대, 제품 혁신은 기업이 채택하는 전략의 일부입니다. Rizobacter Argentina SA, Lallemand, National Fertilizers Limited는 생물학적 유기 비료 시장의 주요 시장 기업의 일부입니다. 시장 규제가 없는 시나리오는 소규모 기업을 지원하고 시장을 단편화하고 있지만 곧 적절한 규제로 통합된 것으로 바뀔 수 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트·지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

시장 성장 촉진요인

시장 성장 억제요인

Porter's Five Forces 분석

공급기업의 협상력

구매자·소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업 간 경쟁 강도

제5장 시장 세분화

유형

미생물

리조비움

아조토박터

아조스피릴룸

남조류

인산염 가용화 박테리아

균근균

기타 미생물

유기 잔류물

풋거름

어분

골분

유분

기타

용도

곡물 및 곡류

맥류 및 유지종자

과일 및 야채

상업용 작물

잔디 및 관상용 작물

지역

북미

미국

캐나다

멕시코

기타 북미

유럽

독일

영국

프랑스

스페인

이탈리아

러시아

기타 유럽

아시아태평양

중국

일본

인도

호주

기타 아시아태평양

남미

브라질

아르헨티나

기타 남미

아프리카

남아프리카

기타 아프리카

제6장 경쟁 구도

Most Adopted Competitor Strategies

시장 점유율 분석

기업 프로파일

Rizobacter Argentina SA

Lallemand Inc.

National Fertilizers Limited

Madras Fertilizers Limited

T Stanes & Company Limited

Gujarat State Fertilizers & Chemicals Ltd

String Bio

Rashtriya Chemicals & Fertilizers Ltd

Agrinos

Biomax Naturals

Symborg(Corteva Agriscience)

Agri Life

Premier Tech

Biofosfatos do Brasil

Kiwa Bio-Tech Products Group Corporation

Protan AG

Mapleton Agri Biotech Pty Limited

Bio Nature Technology PTE Ltd.

Kribhco

Bio Ark Pte Ltd

Novozymes

Savio BIO Organic AND Fertilizers Private Limited

ACI Biolife

제7장 시장 기회와 앞으로의 동향

KTH

영문 목차

영문목차

The Biological Organic Fertilizer Market size is estimated at USD 13.39 billion in 2025, and is expected to reach USD 17.83 billion by 2030, at a CAGR of 5.9% during the forecast period (2025-2030).

Key Highlights

The increased practice of organic farming is one of the significant factors behind the growth of the biological organic fertilizer market. The emphasis on sustainable agriculture and government support to the manufacturers are the other factors that augment the development of the market.

Moreover, recent studies have shown the effect of bio-organic fertilizers on grains. Bio-organic fertilizer that exhibited various qualities, such as nutrient acquisition and plant growth promotion of rice, is an organic-based biofertilizer that contains RP (5%), biochar (15%), and the living cells of Plant Growth Promoting Bacteria (PGPB), mostly Bacillus, Proteus, and Paenibacillus spp., which were isolated from the floodplain, terrace, and saline soils. The results of 16 field experiments and 18 farmers' demonstration trials undertaken by Bangladesh Rice proved that added PGPB supplemented the 30% synthetic N requirement of rice production through biological nitrogen fixation and fully complemented available P from rock phosphate by solubilization during the plant growth period. The combined effect of living ingredients and organic matter of the bio-organic fertilizer saved 30% urea-N, eliminated 100% Triple Super Phosphate fertilizer use in rice production, and simultaneously improved nutrient uptake, N, P use efficiencies, rice yield, and soil health, eventually enhancing the adoption of biological organic fertilizers.

Biological Organic Fertilizer Market Trends

Increasing Organic Farming

The rising popularity of organic products and consumption has forced the expansion of organic farming across the globe. Subsequently, the market for biological organic fertilizers has grown dramatically in response to the recent surge in interest in regenerative agriculture, organic farming, and soil health. Natural organic fertilizers contain specific levels of microorganisms (such as nitrogen-fixing bacteria); organic fertilizers similarly contain microorganisms and typically come from animals and plants, such as livestock manure and crop residues, which are highly suitable for Organic Farming.

According to the Research Institute of Organic Agriculture, the area under organic farming increased by 4.1% in 2020. In addition, the regional statistics of both developed and developing countries have depicted the growth of organic agriculture in the country. For instance, according to the statistics by the government of India, the area under the organic farming certification process in India has almost doubled in 2021-2022, indicating the increasing initiatives and adoption of organic farming, with the full production accounting for 20,540.63 metric tons. Thus, owing to the rising organic area under cultivation and the increasing demand for good-quality crops, cultivators are anticipated to use biological organic fertilizers instead of excessive synthetic fertilizers, driving the market.

Asia Pacific is the fastest growing market

The organic fertilizer market in Asia-Pacific is the fastest-growing among all the other regions. The consumption of organic fertilizers in Asia-Pacific is anticipated to increase with rising awareness among farmers about the benefits of bio-based and organic residue-based fertilizers. The regional demand is concentrated among major agriculture-based countries like China, India, Thailand, Indonesia, and Vietnam while China and India are leading the market developments.

In addition, not only do different countries in the region have their own regulations for fertilizers in general, but they also often have specific requirements and rules for biological and organic fertilizers. For instance, the Regulation of the MOA No. 1/2019 concerning the Registration of Organic Fertilizers, Biological Fertilizers, and Soil Improvement in Indonesia aims to ensure the quality of fertilizer products circulating in the market by requiring them to pass a quality test by an MOA-approved institution.

Further, the growing organic farming in different countries under the region and the increasing demand for organic products drive the market in the region. Moreover, there have been major policy developments related to the organic sector in some Asian countries. In Japan, there was a major development in the Basic Plan for Agriculture and Management, aiming to triple the number of organic farmers and organic land by 2030, in turn boosting the growth of the market.

Biological Organic Fertilizer Industry Overview

The Biological organic fertilizer market is fragmented due to prominent international and regional players. Collaborations with government organizations and expansion in the market, along with product innovation, are some of the strategies adopted by the companies. Rizobacter Argentina S.A, Lallemand, and National Fertilizers Limited are some of the leading market players in the biological organic fertilizer market. The unregulated scenario in the market has sustained the small companies, making the market fragmented, which could be converted to a consolidated one with the proper regulations shortly.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.3 Market Restraints

4.4 Porter's Five Force Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Type

5.1.1 Microorganism

5.1.1.1 Rhizobium

5.1.1.2 Azotobacter

5.1.1.3 Azospirillum

5.1.1.4 Blue-green Algae

5.1.1.5 Phosphate Solubilizing Bacteria

5.1.1.6 Mycorrhiza

5.1.1.7 Other Microorganisms

5.1.2 Organic residues

5.1.2.1 Green Manure

5.1.2.2 Fish Meal

5.1.2.3 Bone Meal

5.1.2.4 Oil Cakes

5.1.2.5 Others

5.2 Application

5.2.1 Grains and Cereals

5.2.2 Pulses and Oilseeds

5.2.3 Fruits and Vegetables

5.2.4 Commercial Crops

5.2.5 Turf and Ornamentals

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Mexico

5.3.1.4 Rest of North America

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Spain

5.3.2.5 Italy

5.3.2.6 Russia

5.3.2.7 Rest of Europe

5.3.3 Asia Pacific

5.3.3.1 China

5.3.3.2 Japan

5.3.3.3 India

5.3.3.4 Australia

5.3.3.5 Rest of Asia-Pacific

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Africa

5.3.5.1 South Africa

5.3.5.2 Rest of Africa

6 COMPETITIVE LANDSCAPE

6.1 Most Adopted Competitor Strategies

6.2 Market Share Analysis

6.3 Company Profiles

6.3.1 Rizobacter Argentina S.A.

6.3.2 Lallemand Inc.

6.3.3 National Fertilizers Limited

6.3.4 Madras Fertilizers Limited

6.3.5 T Stanes & Company Limited

6.3.6 Gujarat State Fertilizers & Chemicals Ltd

6.3.7 String Bio

6.3.8 Rashtriya Chemicals & Fertilizers Ltd

6.3.9 Agrinos

6.3.10 Biomax Naturals

6.3.11 Symborg (Corteva Agriscience)

6.3.12 Agri Life

6.3.13 Premier Tech

6.3.14 Biofosfatos do Brasil

6.3.15 Kiwa Bio-Tech Products Group Corporation

6.3.16 Protan AG

6.3.17 Mapleton Agri Biotech Pty Limited

6.3.18 Bio Nature Technology PTE Ltd.

6.3.19 Kribhco

6.3.20 Bio Ark Pte Ltd

6.3.21 Novozymes

6.3.22 Savio BIO Organic AND Fertilizers Private Limited