아프리카의 플라스틱 포장 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)

Africa Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1683827

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

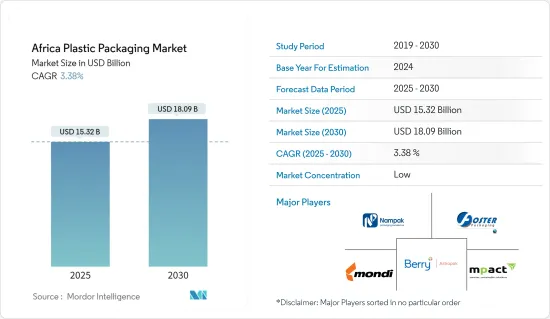

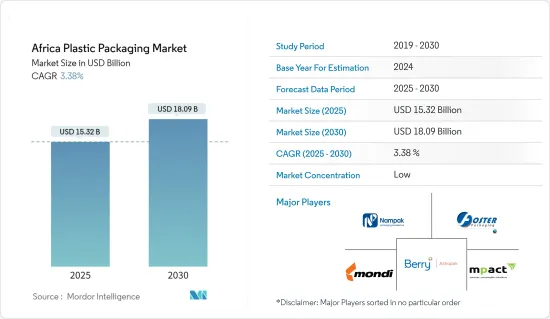

아프리카의 플라스틱 포장 시장 규모는 2025년에 153억 2,000만 달러에 이를 것으로 예상됩니다. 예측 기간(2025-2030년)의 CAGR은 3.38%을 나타내고, 2030년에는 180억 9,000만 달러에 달할 것으로 전망됩니다.

아프리카에서는 최근 몇 년 동안 급속한 인구 증가와 도시화가 진행되고 있습니다. 인구가 증가하고 도시로 이주하는 사람들이 증가함에 따라 포장된 상품에 대한 수요가 증가하고 플라스틱 포장 제품에 대한 요구가 탄생하고 있습니다. 게다가 경제 성장으로 중산계급이 확대되었고 이 지역의 여러 나라에서 가처분소득이 증가했습니다. 사람들의 구매력이 높아짐에 따라 포장 상품 수요도 높아지고 플라스틱 포장 업계의 성장을 이끌고 있습니다.

주요 하이라이트

이 지역의 많은 국가들은 경제 발전을 위해 산업화와 제조업에 주력하고 있으며, 여기에는 식품, 음식, 의약품, 퍼스널케어 제품 등 다양한 산업용 공장 설립이 포함됩니다. 플라스틱 포장은 이러한 산업에 있어서 다용도로 편리한 솔루션이기 때문에 이 지역에서는 그 수요가 지속적으로 성장하고 있습니다.

인구가 증가함에 따라 아프리카 국가에서는 음식 및 음료 수요가 지속적으로 증가하고 있습니다. 세계은행에 따르면 아프리카 식품 산업의 총액은 2030년까지 1조 달러(약 8,415억 유로)로 증가할 수 있습니다.

이 시장은 주로 환경 문제에 대한 관심 증가로 인한 규제 기준의 동적 변화로 인해 어려운 문제에 직면할 것으로 예상됩니다. 이 지역의 각국 정부는 플라스틱 포장 폐기물에 관한 국민의 우려에 대응하고, 환경 폐기물을 최소화하고, 폐기물 관리 프로세스를 개선하기 위한 규제를 실시했습니다.

국제 식품 제조 기업은 제품 수요가 증가함에 따라 아프리카에서 사업을 확대하고 있습니다. 2022년 10월, 쿠키 제조업체인 Britannia Industries Ltd는 아프리카에서의 사업 확대 계획의 일환으로 케냐에서의 사업에 관한 계약을 체결했습니다.

이 시장은 주로 환경 문제에 대한 관심이 높아짐에 따라 규제 기준의 동적 변화로 인해 과제가 예상됩니다. 이 지역의 각국 정부는 플라스틱 포장 폐기물에 관한 국민의 우려에 대응하고, 환경 폐기물을 최소화하고, 폐기물 관리 프로세스를 개선하기 위한 규제를 실시했습니다.

아프리카의 플라스틱 포장 시장 동향

식품산업이 경질·연질 플라스틱 포장 시장의 주요 점유율을 차지

플라스틱 식품 보존 용기는 효과적인 밀봉에 의해 보존 중인 식품의 보존과 신선도 유지에 도움이 됩니다. 이 콘테이너는 카페, 식료품 가게 또는 모든 식품 사업에서 사용하기에 적합합니다. 포장은 서 아프리카의 중요한 시장입니다. 이 산업은 주로 농업과 식품 산업의 성장에 대응하여 하위 지역에서 발전해 왔습니다. 나이지리아, 남아프리카, 케냐는 이 지역의 플라스틱 포장 시장에서 상당한 점유율을 차지합니다.

동부·남부 아프리카의 식품부문은 2050년까지 800%의 성장이 예상되어 가공식품의 거래는 최대 90% 증가할 것으로 전망됩니다. 아프리카 전체에서는 2030년까지 1조 달러의 식품 산업이 될 것으로 예상되고 있으며, 도시 지역의 소비가 더 많은 제품에 대한 수요를 견인하고 있습니다. 식품 포장은 아프리카에서 가장 중요한 최종 사용자 및 플라스틱 산업 중 하나입니다. 식품 업계에서는 경질 플라스틱 포장이 증가하고 있습니다. 이 산업은 경량으로 비용 절감이 가능하다는 특성에서 이것을 사용하고 있습니다.

단단한 플라스틱과 일회용 용기는 테이크 아웃, 후드 체인 및 레스토랑에 필수적입니다. 그러나 이 지역 전체에는 환경에 대한 우려가 있습니다. 이 지역 전체에서 여러 식품 체인이 개방됨에 따라 아프리카에서는 플라스틱 포장 수요가 급증하고 있습니다. 2022년 5월 두바이에 본사를 둔 하랄 패스트 푸드 체인인 ChicKing은 향후 5년간 케냐에 30개 매장을 오픈할 의향을 발표했습니다.

전형적인 유연한 식품 포장의 용도로는 치즈, 고기, 빵, 야채와 같은 식품을 포장하는 필름과 파우치가 있습니다. 대부분의 경우, 연포장은 1차 포장으로 사용되지만, 경우에 따라 2차 포장으로 사용될 수도 있습니다.

이 필름은 라미네이션 처리되지 않았으며 냉동고와 같은 가혹한 환경에도 견딜 수 있습니다. 그 충격 강도, 인열 강도, 내굴곡 균열성, 우수한 밀봉성은 식품 용도로 널리 사용됩니다. 이러한 요인이 아프리카의 연포장 시장을 견인하고 있습니다.

아프리카에서는 도시화가 진행되고 있기 때문에 도시에 사는 사람이 늘어나 신선한 농산물을 얻을 기회가 줄어들고 있습니다. 게다가 소비자의 지속가능성에 대한 관심 증가는 재활용이 용이한 재활용 재료로 만들어진 포장으로 이어져 연포장 수요를 뒷받침합니다.

남아프리카가 큰 시장 점유율을 차지

도시락의 인기가 높아지고, 레스토랑과 슈퍼마켓의 수가 늘어나고, 병 식수와 음료 소비량이 증가하는 것은 모두 나라 시장 확대의 주요 요인입니다.

남아프리카의 홈 케어 제품 시장은 보다 건강한 라이프 스타일을 유지하려는 개인의 동향 증가로 최근 몇 년 동안 상당한 성장을 이루고 있습니다. 이로 인해 음료병, 화장실병, 비닐봉지 등의 제품에 대한 수요가 높아져, 이 지역의 플라스틱 포장 시장의 성장을 높이고 있습니다.

이 나라의 플라스틱 쓰레기의 양은 엄청나기 때문에 정부 동향과 소비자의 강한 의식으로 재활용 추세가 건전한 속도로 확대되고 있습니다. 또한 남아프리카의 코카콜라와 같은 기업들은 국내에서 생산되는 것보다 더 많은 PET를 회수하고 재활용하고 있습니다.

수요 측면에서 모바일 연결의 발달로 남아프리카 고객은 전자상거래로 전환하고 있습니다. 이 추세는 COVID-19의 대유행과 국내 비접촉 거래에 대한 관심 증가로 가속화되고 있습니다. 이로 인해 여러 시장 인수가 가능해졌습니다. 예를 들어, 2021년 7월, 오스트리아의 플라스틱 포장 회사인 ALPLA 그룹은 남부 아프리카에서 발자국을 확대하기 위해 남아프리카의 포장 제조업체 Verigreen Packaging을 인수했습니다.

외국 경제변동 요인의 영향에도 불구하고 전반적으로 이 나라의 음료 소비량은 빠르게 증가하고 있습니다. 청량 음료 소비는 기후 조건의 결과로 나라에서 증가하고 있으며, 사람들은 더 많은 탄산 음료를 마시고 있습니다. 지난 2년간의 심각한 물 부족으로 인해 병 식수 사용량도 극적으로 증가하고 있습니다. 플라스틱병은 시장의 주류가 되고 플라스틱병 수요도 증가하고 있습니다. 따라서 이러한 요인들은 이 나라의 플라스틱 포장 시장의 성장을 가속하고 있습니다.

아프리카의 플라스틱 포장 산업 개요

아프리카의 플라스틱 포장 시장은 매우 단편화되어 있으며, 몬디, 남팩, 베리 아스트라팩 등 시장의 기존 기업과 여러 지역의 포장 회사로 구성되어 있습니다. 환경에 대한 우려가 각국에서 높아지고 있는 가운데, 대기업은 환경 문제에 임해, 플라스틱 병을 보다 안전하게 하기 위해, 연구개발에 대한 투자를 강화하고 있습니다.

2023년 1월, 파티사는 케냐와 나이지리아의 자회사를 통해 사하라 이남 아프리카에서 인쇄·포장 사업을 전개하고, 식품 및 식품 부문에 강한 익스포저를 보유한 MHL International Holdings의 상당한 소수 주주 지분 취득을 발표했습니다.

2022년 8월 알프라는 OTC 포장 제조 기술을 확대했습니다. ALPLA 그룹의 의약품 포장 사업인 Alplapharma는 OTC 병 제조 기술을 확장하고 유연한 압출 블로우 성형(EBM)을 도입하여 이 분야에서 지속가능하고 고객 특화된 포장 솔루션을 실현했습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트·지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

생태계 분석

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

제5장 시장 역학

시장 성장 촉진요인

페트병 수요 증가가 동지역의 경질 포장의 수요를 촉진할 전망

음료용 포장은 향후 수년에 견인력을 늘릴 전망

시장의 과제

원재료 가격 변동

COVID-19와 최근의 지정학적 변화가 아프리카의 포장 산업 성장에 미치는 영향

아프리카의 주요 신흥 시장 분석

관련 HS 코드에 근거한 아프리카의 주요 원료 수입 분석

플라스틱 포장 시장의 기술 혁신

포장 산업에서 광범위한 ROI 대책 분석

제6장 시장 세분화

경질 포장

재료

폴리에틸렌(PE)

폴리에틸렌 테레프탈레이트(PET)

폴리프로필렌(PP)

폴리스티렌(PS) 및 발포 폴리스티렌(EPS)

폴리염화비닐(PVC)

기타 재료

최종 사용자

식품

음료

헬스케어 및 의약품

퍼스널케어 및 화장품

기타 최종 사용자

연포장

재료

폴리에틸렌(PE)

양방향 폴리프로필렌(BOPP)

주조 폴리프로필렌(CPP)

폴리염화비닐(PVC)

에틸렌 비닐 알콜(EVOH)

기타 재료

최종 사용자

식품

음료

퍼스널케어 및 화장품

기타 최종 사용자

국가명

남아프리카

나이지리아

이집트

케냐

모로코

가나

에티오피아

탄자니아

잠비아

제7장 경쟁 구도

기업 프로파일

Berry Astrapak(Berry Global Group Inc.)

Nampak Ltd

Mondi PLC

Mpact Pty Ltd

Foster International Packaging

Constantia Flexibles

Tetra Pak SA

Amcor PLC

LIQUIBOX(Sealed Air Corporation)

Sonoco Products Company

Toppan Inc.

Huhtamaki Oyj

ALPLA Group

Plastipak Holdings Inc.

Polyoak Packaging

제8장 아프리카 국가별 주요 공급업체리스트

남아프리카

나이지리아

이집트

케냐

모로코

가나

에티오피아

탄자니아

잠비아

제9장 시장 전망

제10장 투자 분석

KTH

영문 목차

영문목차

The Africa Plastic Packaging Market size is estimated at USD 15.32 billion in 2025, and is expected to reach USD 18.09 billion by 2030, at a CAGR of 3.38% during the forecast period (2025-2030).

Africa has experienced rapid population growth and urbanization in recent years. As the population increases and more people move to cities, there is a rising demand for packaged goods, creating the need for plastic packaging products. Furthermore, economic growth resulted in an expansion of the middle class and increased disposable income in various countries of the region. As purchasing power of people increases, the demand for packaged goods also rises, driving the growth of the plastic packaging industry.

Key Highlights

Many countries in the region are focusing on industrialization and manufacturing for their economic development, which includes the establishment of factories for various industries, such as food, beverage, pharmaceuticals, personal care products, and more. As plastic packaging is a convenient solution for these industries in multiple applications, its demand is growing continuously in the region.

With a growing population, demand for food and beverages is continuously increasing in the countries of Africa. According to World Bank, the total value of the African food industry could rise to USD one trillion (approx. EUR 841.5 billion) by 2030.

The market is expected to be challenged owing to dynamic changes in regulatory standards, primarily due to increasing environmental concerns. Governments across the region have been responding to public concerns regarding plastic packaging waste and implementing regulations to minimize environmental waste and improve waste management processes.

International food manufacturing companies are expanding their operations in Africa due to rising product demand. In October 2022, cookie manufacturer Britannia Industries Ltd finalized a deal for operations in Kenya as part of its plan to expand in Africa.

The market is expected to be challenged owing to dynamic changes in regulatory standards, primarily due to increasing environmental concerns. Governments across the region have been responding to public concerns regarding plastic packaging waste and implementing regulations to minimize environmental waste and improve waste management processes.

Africa Plastic Packaging Market Trends

Food Industry to Hold Major Share in Both Rigid and Flexible Plastic Packaging Markets

Plastic food storage containers help preserve food during storage or keep them fresh by effective sealing. These containers are suitable for use in cafes, grocery shops, or any food business. Packaging is an important market in West Africa. This industry has developed in the sub-region largely in response to farming and the growth of the food industry. Nigeria, South Africa, and Kenya have a substantial share of the plastic packaging market in the region.

The food sector in Eastern and Southern Africa is expected to grow by 800% by 2050, with trade in processed foods increasing by up to 90%. Africa as a whole is anticipated to be a USD 1 trillion food industry by 2030, with urban consumption driving demand for more products. Food packaging is one of Africa's most significant end-user plastic industries. Rigid plastic packaging is increasing in the food industry. The industry uses it for its properties, such as lightweight and reduced cost.

Rigid plastic and disposable containers are integral to takeouts, food chains, and restaurants. However, there are environmental concerns across the region. The opening of several food chains across the region has spiked the demand for plastic packaging in Africa. In May 2022, the Dubai-based halal fast-food chain ChicKing announced its intentions to open 30 outlets in Kenya over the next five years.

Typical flexible food packaging applications include films and pouches to package food products like cheeses, meats, bread, and vegetables, among others. In most cases, flexible packaging is used as the primary packaging, but it can also be used as the secondary packaging in some cases.

These films can be laminated or nonlaminated and withstand harsh environments like freezers. Their impact strength, tear strength, flex-crack resistance, and excellent sealing properties are extensively used in food applications. Such factors are driving the flexible packaging market in the country.

Due to increasing urbanization in Africa, more people are living in cities and having less access to fresh produce, which is driving the demand for flexible packaging. Additionally, the growing focus of consumers toward sustainability is leading to packaging made from recycled materials that can be easily recycled, hence supporting the demand for flexible packaging.

South Africa to Hold Significant Market Share

The rising popularity of packed meals, the expanding number of restaurants and supermarkets, and rising bottled water and beverage consumption are all key drivers of the country's market expansion.

The South African home care products market has seen considerable growth in recent years owing to a growing trend among individuals to maintain a healthier lifestyle. This has driven demand for products like beverage bottles, toiletry bottles, plastic bags, and others, thereby increasing the growth of the region's plastic packaging market.

With the country's enormous volume of plastic garbage, the recycling trend is expanding at a healthy rate, owing to government restrictions and strong consumer awareness. Moreover, companies like Coca-Cola in South Africa collected and recycled more PET than was produced within the country.

On the demand side, customers in South Africa are migrating to e-commerce as mobile connectivity develops. This tendency has accelerated as a result of the COVID-19 pandemic as well as a spike in interest in contactless transactions inside the country. This has permitted several market acquisitions. For instance, in July 2021, Austrian plastic packaging firm ALPLA Group purchased South African packaging producer Verigreen Packaging to extend its footprint in southern Africa.

Overall, beverage consumption in the country is increasing rapidly, despite the impact of external economic variables. Soft drink consumption is increasing in the country as a result of climatic conditions, with people drinking more carbonated beverages. Due to severe water scarcity in the country over the previous two years, the usage of bottled water has also increased dramatically. With PET bottles becoming the market norm, the demand for plastic bottles has also increased. Therefore, these factors are driving the growth of the plastic packaging market in the country.

Africa Plastic Packaging Industry Overview

The African plastic packaging market is highly fragmented, comprising market incumbents such as Mondi, Nampak, and Berry Astrapak and several regional packaging firms. With environmental concerns rising across countries, major players have boosted their investments in research and development to tackle environmental concerns and make plastic bottles safer.

In January 2023, Phatisa announced the acquisition of a significant minority stake in MHL International Holdings, a printing and packaging provider operating in Sub-Saharan Africa through subsidiaries in Kenya and Nigeria with strong exposure to the food and beverage sector.

In August 2022, ALPLA expanded its OTC packaging manufacturing technology. Alplapharma, the pharma packaging business of the ALPLA group, accomplished this by expanding its manufacturing technology for OTC bottles with the inclusion of flexible extrusion blow molding (EBM), which allows for sustainable and customer-specific packaging solutions in this field.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Ecosystem Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Buyers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitutes Products

4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Rising Demand for Pet Bottles is Expected to Drive the Need for Rigid Packaging in the Region

5.1.2 Beverage Packaging is Expected to Gain Traction over the Coming Years

5.2 Market Challenges

5.2.1 Fluctuating Raw Material Prices

5.3 Impact of COVID -19 and the Recent Geopolitical Changes on the Growth of the African Packaging Industry

5.4 Analysis of the Key Emerging Markets in Africa

5.5 Analysis of the Key Raw Material Imports into Africa Based on Relevant HS Codes

5.6 Technological Innovations in the Plastic Packaging Market

5.7 Analysis of the Broader ROI Measures within the Packaging Industry

6 MARKET SEGMENTATION

6.1 Rigid Packaging

6.1.1 Material

6.1.1.1 Polyethylene (PE)

6.1.1.2 Polyethylene Terephthalate (PET)

6.1.1.3 Polypropylene (PP)

6.1.1.4 Polystyrene (PS) and Expanded Polystyrene (EPS)