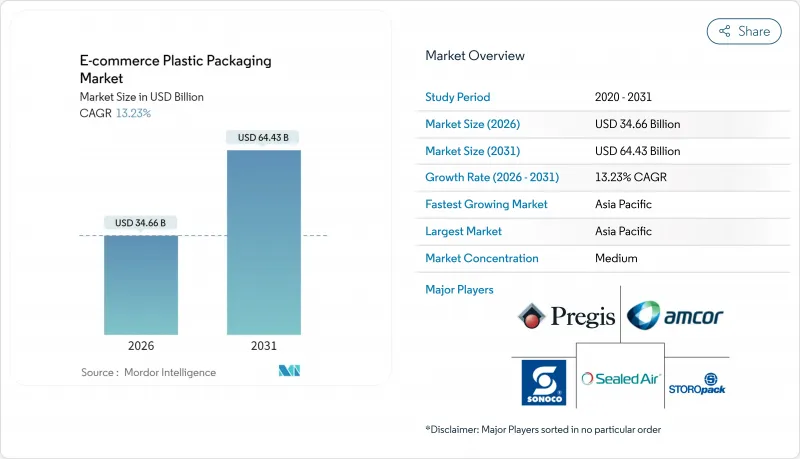

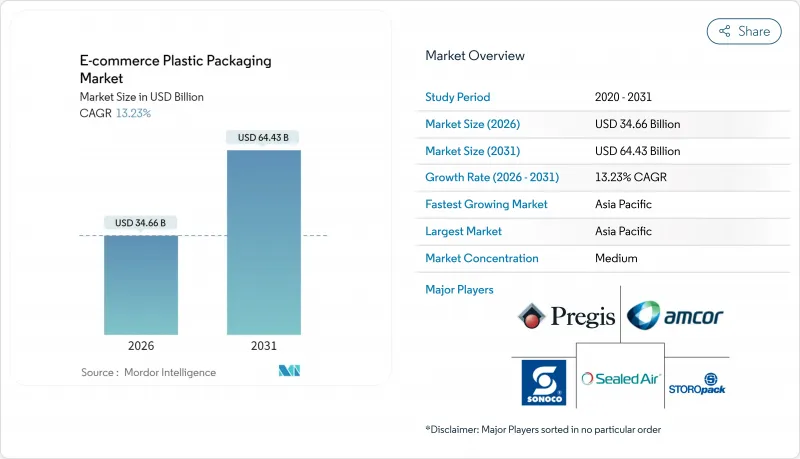

2026년 전자상거래 플라스틱 포장 시장 규모는 346억 6,000만 달러로 추정되며, 2025년 306억 달러에서 성장할 전망입니다. 2031년 예측은 644억 3,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 13.23%를 나타낼 것으로 예상됩니다.

온라인 소매의 급속한 성장, 프리미엄 개봉 경험에 대한 소비자 기대 증가, 지속가능성에 대한 규제 강화가 단기부터 중기적인 시장 전망을 형성하고 있습니다. 가볍고 유연한 필름, 단일 소재의 장벽 구조, 디자인성이 뛰어난 기재는 브랜드가 운송 비용을 줄이고, 재활용 규칙을 준수하며, 시각적 매력을 높이는 데 도움이 됩니다. 제조업체는 밀집한 도시 지역의 배송 네트워크를 통해 운송되는 식료품 및 화장품을 보호하는 스마트 라벨, 자동 충전 라인 및 온도 관리 솔루션의 기회를 포착합니다. 통합 컨버터가 틈새 전문 기업을 인수하고 신규 수지 특허를 취득하고 공급 안전성을 보장하는 화학적 재활용을 확대함에 따라 경쟁이 치열해지고 있습니다.

전자상거래의 지속적인 성장은 자동 분류, 복합 운송 및 소비자에게 직접 개봉을 견디는 포장 수요를 견인하고 있습니다. 일본의 정기 미용 서비스는 프리미엄 디자인과 변조 방지 씰이 매장 체험을 대체하는 사례를 보여줍니다. 소포량 증가로 창고는 로봇 처리 능력과 보관 밀도를 극대화하는 표준 포장 크기를 채용하고 있습니다.

메탈로센 폴리에틸렌 필름은 두께를 30% 삭감하면서도 -40℃에서 120℃의 범위에서 씰 성능을 유지하여 운송 시의 배출량과 원재료비를 삭감합니다. 나노첨가제는 장벽강도를 높여 전자기기용 파우치의 박육화를 실현합니다. 가공업자는 경질 인서트를 팽창식 완충재로 대체하여 체적 중량을 대폭 삭감하고, 단일 소재 재활용 규제에의 적합을 도모하고 있습니다.

캘리포니아주 SB54 법안은 2032년까지 65%의 재활용 소재 사용을 의무화하고 EU의 신규 규제에서는 순환형 설계가 요구됩니다. 컴플라이언스 부담은 높은 비용의 라인 업데이트와 제품 포트폴리오의 합리화를 강요하는 한편, 사용 후 플라스틱 회수를 효율화하는 단일 소재 라미네이트의 기술 혁신이 촉진되고 있습니다. 브랜드 각사는 가이드라인이 안정될 때까지 제품 투입을 늦추지만, 조기 도입 기업은 환경 배려형 브랜드로서의 우위성을 확보하고 있습니다.

폴리에틸렌은 2025년 전자상거래 플라스틱 포장 시장 점유율의 42.12%를 차지한 뛰어난 밀봉성과 자동화된 성형·충전·씰 라인에서의 높은 처리량성을 배경으로 했습니다. 메탈로센 등급은 내천자성을 손상시키지 않고 운송 중량을 억제하는 적극적인 박육화를 가능하게 합니다. 폴리에틸렌 유래의 전자상거래 플라스틱 포장 시장 규모는 대중용 메일 변기 봉투나 스트레치 슬리브를 배경으로 꾸준히 확대될 것으로 예측됩니다. 폴리에틸렌 테레프탈레이트(PET)는 14.42%의 연평균 복합 성장률(CAGR)로 확대되어 뛰어난 산소·습기 배리어성이 수지 비용의 높이를 웃도는 온도 관리가 필요한 식료품 포장으로 지지되고 있습니다. 화학적 재활용은 식품 접촉 승인을 유지한 100% 소비 후 원료 유래 PET를 제공합니다. 폴리프로필렌(PP)은 재사용 가능한 토트백과 힌지 뚜껑 상자로 수요를 확보하고, 바이오플라스틱은 퇴비화 가능성이 강력한 브랜드 가치를 가진 고급 화장품 분야에서 발판을 굳히고 있습니다.

폴리에틸렌 혁신의 제2파는 금속화층을 배제하면서 동등한 향기 유지성을 실현하는 단일 소재 구조에 초점을 맞추어 재활용 공정의 원활화를 도모하고 있습니다. PET 필름에서는 나노클레이 분산체가 산소 투과량을 15-20% 삭감하고, 얇은 라미네이트를 가능하게 함으로써 소포 수송 시의 부피를 저감합니다. 이러한 소재의 진보는 고성능으로 지속 가능한 폴리머의 실증장으로서 전자상거래 플라스틱 포장 시장을 강화하고 있습니다.

파우치 및 가방은 의류, 가정용품 및 퍼스널케어 제품의 운송에 있어서 다용도로 2025년 수익의 37.95%를 차지했습니다. 그러나 팽창식 쿠션과 성형 펄 플라이너를 포함한 보호 포장은 깨지기 쉬운 소비자용 전자기기의 출하량 증가에 따라 2031년까지 14.55%라는 가장 빠른 CAGR을 나타낼 전망입니다. VTT사의 종이접기 기술을 이용한 판지 패드는 플라스틱 기포 완충재에 필적하는 충격 흡수 공동을 형성하면서 폐기물을 삭감합니다. 수축 필름과 연신 필름은 지역 배송 센터의 팔레트 보호에 필수적이지만 성장률은 부문 리더에 뒤쳐져 있습니다. 식료품 EC 사업자가 인증된 콜드체인 대응을 요구하는 가운데 특수 단열 메일 봉투가 틈새 성장을 개척하고 있습니다.

보호 솔루션에는 현재 산업 퇴비 처리로 분해되는 동안 낙하 및 진동으로부터 제품을 보호하는 바이오 열가소성 수지 함침 부직포가 통합되어 있습니다. 이러한 진보는 유럽의 플라스틱 세금 제도와 기업의 넷 제로 공약에 따른 것으로 지속 가능한 완충재가 프리미엄 추가 판매가 아닌 표준이 되는 것을 보증합니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 14.75%로 성장을 견인할 전망입니다. 중국의 성숙한 온라인 소매 생태계가 고급 포장 기준을 지역 전체에 퍼뜨리고 있기 때문입니다. 현지의 컨버터는 고속 구분 벨트에 대응한 경량 메일 봉투를 양산해, 저비용과 단 사이클을 실현하고 있습니다. 일본의 정기구매 문화는 습도가 높은 여름과 빙점 아래 겨울에 화장품을 보호하는 고급 배리어 라미네이트 수요를 견인하고 있습니다. 한국의 모바일 커머스는 택배 로커에 맞는 컴팩트하고 브랜드성을 중시한 포장을 선호합니다. 한편, 급성장하는 인도 시장에서는 난폭한 취급에도 견디면서 비용 효율을 유지하는 초경제적인 단층봉투가 주류가 되고 있습니다.

북미에서는 고급 창고 로봇 기술과 특히 미용·전자기기 분야에서 프리미엄 개봉 체험을 요구하는 문화가 대량 유통을 지지하고 있습니다. 캘리포니아의 재생재 사용 의무화로 화학재생 PET제 메일봉투의 조기 도입이 촉진되고 있습니다. 캐나다에서는 몬디사가 힌튼 공장을 500만 달러로 인수함으로써 새로운 크래프트 종이 생산 능력을 획득하여 섬유와 폴리머를 융합한 하이브리드형 EC 솔루션의 가능성이 넓어지고 있습니다. 멕시코의 니어 쇼어 공장은 리드 타임 단축을 요구하는 미국 소매 업체를 위해 폴리 메일을 제공합니다.

유럽에서는 엄격한 일회용 규제가 기조가 되고, 컨버터는 단일 소재나 종이 베이스의 대체품으로 이행하고 있습니다. 독일의 재활용 업체는 높은 PET 회수율을 달성하여 병에서 가방으로 순환 공급을 실현. 영국은 브렉지트 후에 독자적인 틀을 구축하면서도 EU의 재활용재 목표를 반영하여 버진 수지 사용에 대한 압력을 유지하고 있습니다. 몬디사의 종이 메일 봉투 도입은 섬유 기재가 배송시의 내구성 기준을 충족시키면서 플라스틱 삭감 목표를 달성할 수 있음을 나타내고 있습니다.

E-commerce plastic packaging market size in 2026 is estimated at USD 34.66 billion, growing from 2025 value of USD 30.60 billion with 2031 projections showing USD 64.43 billion, growing at 13.23% CAGR over 2026-2031.

Rapid online retail growth, rising consumer expectations for premium unboxing and mounting sustainability mandates shape the near-to-mid-term outlook. Lightweight flexible films, mono-material barrier constructions and design-rich substrates help brands cut freight costs, comply with recycling rules and enhance visual appeal. Manufacturers seize opportunities in smart labels, automated filling lines and temperature-controlled solutions that protect groceries and cosmetics shipped through dense urban fulfillment networks. Competitive intensity grows as integrated converters acquire niche specialists, patent novel resins and scale chemical recycling that safeguards supply security.

Uninterrupted growth in e-commerce drives demand for packaging that endures automated sortation, multi-modal transport and direct-to-consumer unboxing. Subscription beauty services in Japan highlight how premium designs and tamper-evident seals substitute for in-store experience. Higher parcel volumes push warehouses to adopt standard pack dimensions that maximize robotic throughput and storage density.

Metallocene polyethylene films cut thickness by 30% yet keep seals intact between -40 °C and 120 °C, reducing freight emissions and raw-material spend. Nano-additives bolster barrier strength, enabling thinner walls for electronics pouches. Converters replace rigid inserts with inflatable cushioning to slash dimensional weight and comply with mono-material recycling rules.

California SB 54 demands 65% recycled content by 2032 while forthcoming EU rules insist on circular design. The compliance burden triggers costly line upgrades and portfolio rationalization, yet it spurs innovation in mono-material laminates that streamline post-consumer recovery. Brands delay launches until guidelines stabilize, though early adopters secure green-branding advantages.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Polyethylene contributed 42.12% to the e-commerce plastic packaging market share in 2025, supported by favorable sealability and high throughput on automated form-fill-seal lines. Metallocene grades permit aggressive downgauging that curbs shipping mass without compromising puncture resistance. The e-commerce plastic packaging market size derived from polyethylene is projected to climb steadily on the back of mass accessible mailers and stretch sleeves. Polyethylene terephthalate, expanding at 14.42% CAGR, finds favor in temperature-sensitive grocery packs where superior oxygen and moisture barriers outweigh higher resin cost. Chemical recycling yields PET with 100% post-consumer content that retains food-contact clearance. Polypropylene secures demand in reusable totes and hingelid boxes, while bioplastics gain a foothold in premium cosmetics where compostability carries strong brand equity.

A second wave of polyethylene innovation centers on mono-material structures that eliminate metallized layers yet deliver equal aroma retention, smoothing passage through recycling streams. In PET films, nano-clay dispersions cut oxygen ingress by 15-20% and permit thinner laminates that reduce cube size during parcel transit. Such material advances reinforce the e-commerce plastic packaging market as a proving ground for high-performance sustainable polymers.

Pouches and bags controlled 37.95% of 2025 revenue thanks to versatility across apparel, home and personal care shipments. Yet protective packaging, including inflatable cushions and molded pulp liners, will record the fastest 14.55% CAGR through 2031 as fragile consumer electronics volumes swell. Origami-engineered paperboard pads from VTT create shock-absorbing hollows that rival plastic bubble wrap while trimming waste. Shrink and stretch films stay essential for pallet integrity within regional fulfillment centers, though gains trail segment leaders. Specialty thermal mailers carve niche growth as grocery e-tailers demand certified cold-chain compliance.

Protective solutions now integrate bio-based thermoplastic-impregnated nonwovens that break down in industrial composters yet shield products from drops and vibration. Such advances align with European plastic-tax regimes and corporate net-zero pledges, ensuring sustainable cushioning becomes a standard rather than a premium upsell.

The E-Commerce Plastic Packaging Market Report is Segmented by Material Type (Polyethylene, Polypropylene, and More), Product Type (Pouches and Bags, Mailers and Envelopes, and More), End-User Industry (Consumer Electronics and Media, Food and Beverage, and More), Packaging Function (Primary, Secondary, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific leads growth with a 14.75% CAGR to 2031 as China's mature online retail ecosystem spreads sophisticated packaging standards across the region. Domestic converters mass-produce lightweight mailers tailored to high-speed sortation belts, keeping costs low and cycle times short. Japan's subscription culture drives demand for premium barrier laminates that preserve cosmetics in humid summers and sub-zero winters. South Korea's handheld commerce favors compact, brand-heavy packs that fit parcel lockers, while India's burgeoning volume tilts toward ultra-economical mono-layer bags that tolerate rough handling yet remain cost effective.

North America sustains large volumes through advanced warehouse robotics and a culture of premium unboxing, particularly in beauty and electronics. California's recycled-content mandate boosts early adoption of chemically recycled PET mailers. Canada benefits from new kraft paper capacity after Mondi's USD 5 million Hinton mill purchase, opening opportunities to blend fiber and polymer in hybrid e-commerce solutions. Mexico's near-shore plants supply poly mailers to U.S. retailers seeking shorter lead times.

Europe sets regulatory tone with stringent single-use rules, pushing converters toward mono-material and paper-based alternatives. German recyclers achieve high PET recovery rates that feed bottle-to-pouch loops. The United Kingdom shapes an independent framework after Brexit, yet still mirrors EU recyclate targets, keeping pressure on virgin resin use. Mondi's paper mailer launch shows how fiber substrates can meet durability thresholds for parcel journeys while satisfying plastic-reduction targets.