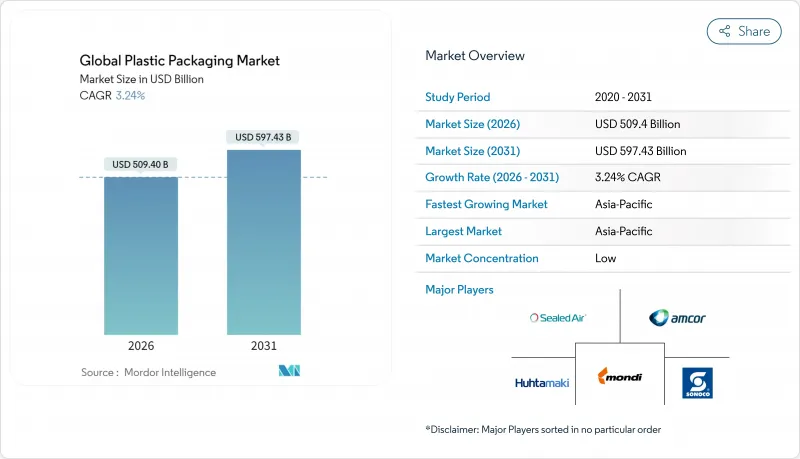

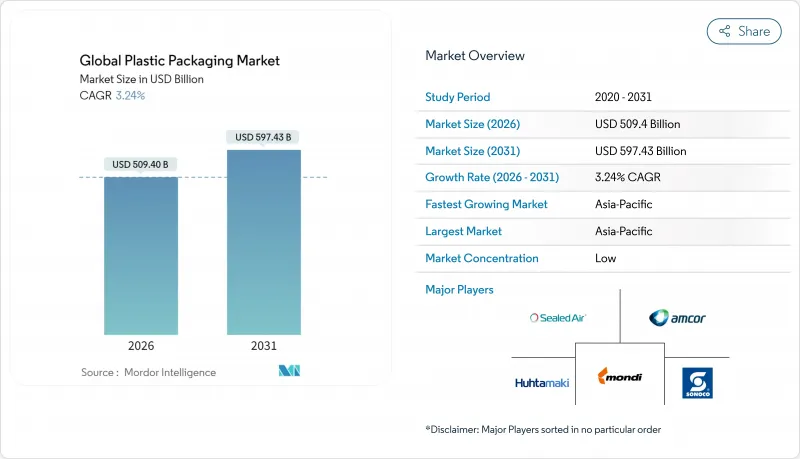

플라스틱 포장 시장 규모는 2026년에는 5,094억 달러에 달할 것으로 예측되며, 2025년 4,934억 2,000만 달러에서 성장한 수치입니다. 2031년에는 5,974억 3,000만 달러에 이르고, 2026년부터 2031년에 걸쳐 CAGR 3.24%로 성장할 전망입니다.

규제 감시가 강화되는 가운데 견고한 전자상거래 활동, 편리성 식품 소비 증가, 대체 소재에 대한 비용 경쟁력 등 요소가 지속적인 수요를 지지하고 있습니다. 화학적 리사이클 라인 투자, 캡 고정 규제에 대응한 포장 재설계, 고리사이클율 기준 달성이 가능한 기존 기업은 경쟁 우위를 확보할 수 있는 반면, 중소 컨버터는 컴플라이언스 비용 증가에 직면하고 있습니다. 동시에 물류 비용 상승으로 운송비를 절감하는 경량이고 연포장 형태의 가치 제안이 높아져 전자상거래, 식품, 의료 분야에서 공급업체 계약이 강화되고 있습니다. 첨단적인 연구개발과 폐쇄 루프 공급계약의 자금조달에는 규모가 필수조건이 되기 때문에 업계 재편이 가속화되고 있습니다.

라스트마일 배송 모델에서는 포장물이 다수의 취급 공정과 용적 중량 과금에 노출되므로 브랜드 소유자는 경질 포장재에 비해 최대 75%의 공극을 줄일 수 있는 필름, 파우치, 메일러를 선호합니다. 아마존의 '프라스트레이션 프리 포장' 프로토콜(현재 30만 SKU 이상을 커버)은 사실상 업계 규격을 형성하여 중소기업 판매자를 준거한 폴리에틸렌 및 폴리프로필렌 솔루션으로 이끌고 있습니다. 자동 분류 라인에서는 광학 검출을 견디는 단일 소재 구조가 필수이며, 혼합 소재의 포장은 거부나 고비용의 재작업 작업의 리스크가 있습니다. 포장 체적을 15% 삭감하면 운송비가 12% 낮아져 고성능 플렉서블 필름의 8-10%의 재료 비용 증가를 충분히 상쇄합니다. 배리어 코팅된 연포장은 전자기기나 온도 관리가 필요한 의약품에 대한 보호도 확대하여 식품 이외의 분야로의 전개를 가능하게 하고 있습니다.

도시화, 가구 규모의 축소, 노동 시간의 연장이 단품 포장의 상온 보존 가능 식품에 대한 수요를 촉진하고 있습니다. 2024년에는 도시 소비자의 가공식품 구매량이 전년대비 8.2% 증가하여 과거 최고 성장률을 기록했습니다. 산소 및 습기 배리어성과 전자레인지 대응성을 겸비한 다층 연포장은 보존 기간과 안전성의 면에서 종이 포장을 웃도고 있습니다. 음료 제조업체는 규제 위반에 의한 벌칙 회피를 위해, 제조 코스트를 1 단위당 0.02-0.04 유로 추가해, 고정식 캡이나 부정 개봉 방지 기능을 추가하고 있습니다. 장기 보존 가능한 포장에 의해 유제품이나 주스 브랜드는 냉장 유통망이 정비되어 있지 않은 지방 시장에도 진출 가능하게 되어, 신흥 시장에 있어서의 연포장의 우위성이 한층 더 견고한 것이 되고 있습니다.

캘리포니아의 비닐 봉지 금지, 영국의 습식 티슈 금지, 남호주의 발포 스티롤 규제로 인해 제품 카테고리 전체가 사실상 밤새 사라졌습니다. 수입제한과 고액벌금을 포함한 집행조치는 긴급한 제품개선과 설비투자를 촉구하고 있습니다. 가나의 비닐봉지금지안에 관한 학술연구에서는 주당 34만 달러의 세수감소가 시산되어 광범위한 경제파급효과가 부각되었습니다. 다국적 기업은 각 관할 구역마다 다른 "일회용" 정의에 직면하여 세계 SKU의 통합이 복잡해지고 있습니다. 입법자가 명백한 일회용 제품 이외의 대상 범위를 확대함에 따라 외식산업용 포장이나 2차 포장 형식에서도 추가적인 판매 수량 리스크가 발생하고 있습니다.

연포장은 2025년 매출의 54.10%를 차지하며, 2031년까지 연률 4.41%의 성장이 전망되고 있어 플라스틱 포장 시장에서 경질 포장을 크게 웃도는 확대 페이스를 나타내고 있습니다. 연료비 인플레이션과 체중 중량 운임 제도는 출하 물류 비용을 줄이는 파우치, 메일 봉투, 랩 필름으로의 구조적 전환을 뒷받침하고 있습니다. 필름 및 랩은 보존 기간을 손상시키지 않고 EPR(확대 생산자 책임) 프레임워크를 충족하는 단일 소재 옵션을 컨버터가 채택함에 따라 더욱 보급되고 있습니다. 구조와 고급스러운 진열이 최우선으로 되는 분야에서는 경질병, 항아리, 트레이의 필요성은 여전히 높은 것, 재밀봉 가능한 지퍼, 돌출부, 스탠드업 형식이 역사적 특징의 장점을 잠식함에 따라 점유율이 점차 감소하고 있습니다. 두 형식을 모두 제공하는 통합 공급업체는 브랜드 소유자가 벤더 기반을 간소화하면서 더 높은 지갑 공유를 보장합니다.

수지 가격의 급등이 전가 능력을 능가하는 경우, 경질 포장 하위 부문은 이익률의 압박에 직면합니다. 반면, 연질 포장은 단위당 그램 중량을 줄여 위험을 줄입니다. 유리나 금속의 대체품은 음료나 통조림 식품에 한정된 틈새 시장에 머물러 있습니다. 트레이 제조업체는 오븐 대응과 전자레인지 대응 등 고부가가치 기능이 요구되는 외식산업 채널에서 존재감을 유지합니다. 전반적으로, 연질 포장은 수량과 성장률의 양면에서 주도적 입장을 확립하여 예측 기간 동안 플라스틱 포장 시장을 견인하는 핵심 역할을 확고히 합니다.

2025년 시점에서 폴리에틸렌이 플라스틱 포장 시장의 41.85%를 차지하는 한편, 폴리프로필렌은 5.55%라는 뛰어난 CAGR에 의해 가장 급속하게 성장하는 수지 패밀리로서의 지위를 확립하고 있습니다. 폴리프로필렌의 높은 내열성, 뛰어난 투명성, 우수한 밀봉성은 재활용 가능성 요구 사항을 충족하면서 식품 안전을 보장하는 단일 소재 솔루션을 제공합니다. PET는 확립된 병에서 병으로의 재활용 루프를 통해 음료 분야에서 견고한 지위를 유지하지만, 기계적 재활용의 한계는 높은 비용의 화학적 재활용 능력을 추가하지 않으면 재생재 함량의 향상을 제한합니다. PVC, 폴리스티렌 및 기타 스티렌 수지는 엄격한 환경 규제와 브랜드 소유자의 선택을 벗어나 바이오 수지 및 특수 공중 합체의 틈새 시장에 기회가 탄생했습니다.

화학적 재활용의 경제성은 안정한 탈중합 경로를 갖는 수지를 더욱 유리하게 만듭니다. 따라서 PET와 PP는 더 많은 설비 투자를 모으는 반면, PS와 PVC 프로젝트는 투자 장벽을 지우는 데 어려움을 겪고 있습니다. 수지 공급업체는 재료 전환 시 컨버터를 지도하는 용도 엔지니어링 팀을 통해 차별화를 도모하고 있으며, 이 서비스는 진화하는 EPR(확대 생산자 책임) 틀과 FDA의 식품 접촉 규칙 중에서 높은 평가를 받고 있습니다.

아시아태평양은 2025년 세계 수익의 40.80%를 차지하고 6.78%의 연평균 복합 성장률(CAGR)로 확대되어 플라스틱 포장 시장 성장의 확고한 견인 역할을 하고 있습니다. 중국이 가장 큰 점유율을 차지하고 있지만 폐기물 수입 규제 강화와 탄소 중립 목표로 현지 제조업체는 재활용 능력에 대한 투자를 촉구하고 있습니다. 인도, 베트남, 인도네시아에서는 조직화된 소매업 및 전자상거래의 침투가 진행되어 2자리 수량 증가를 기록하고 있습니다. 통화 변동과 지정학적 요인으로 인해 다국적 브랜드 소유자는 조달 대상을 ASEAN 국가에 분산시키고 특정 국가에 대한 과도한 의존성을 줄이는 움직임을 볼 수 있습니다.

북미에서는 의약품 수요, 신선식품물류, 고도재활용 거점의 정비를 배경으로 안정된 1자리대 중반의 성장을 보여주고 있습니다. 주 수준의 플라스틱 폐기물 규제는 복잡성을 증가시키는 반면, 재활용 플라스틱 및 단일 소재 기술 개발 기업에 새로운 기회를 제공합니다. 캐나다에서 도입 예정인 전국적인 EPR(확대생산자책임)제도는 재활용 가능한 포장재로의 이행을 가속시켜 국경을 넘은 연계를 촉진할 전망입니다.

EPR(확대생산자 책임)과 캡고정의무의 중심지인 유럽은 가치 성장은 완만하면서도 세계 설계 기준에 큰 영향력을 미치고 있습니다. 높은 노동 및 에너지 비용이 공정 자동화와 수지 경량화를 촉진하는 한편, 규제 당국이 리사이클 함유율의 기준치를 인상함으로써 화학적 리사이클 투자가 가속되고 있습니다. 동유럽의 컨버터 기업은 서유럽 수준의 비용 기반을 피하면서 지역적인 근접성을 요구하는 브랜드 기업의 리쇼어링 안건을 모아 폴란드나 헝가리로의 자본 유입을 촉진하고 있습니다.

라틴 아메리카와 중동 및 아프리카의 점유율은 비슷하지만 빠른 성장세를 보이고 있습니다. 브라질은 장벽 포장이 필요한 농산물 수출의 혜택을 누리고 있으며, GCC 국가들은 석유화학 통합을 활용하여 경쟁력 있는 가격의 수지를 수출하고 있습니다. 아프리카 시장에서는 일회용 금지법의 제정이 시작되고 있어 저그램 중량으로 높은 배리어성을 갖춘 솔루션을 저렴한 가격으로 제공할 수 있는 연포장 제조업체에게 유망한 시장이 되고 있습니다.

plastic packaging market size in 2026 is estimated at USD 509.4 billion, growing from 2025 value of USD 493.42 billion with 2031 projections showing USD 597.43 billion, growing at 3.24% CAGR over 2026-2031.

Robust e-commerce activity, rising convenience-food consumption, and cost-competitive advantages over alternate substrates underpin sustained demand even as regulatory scrutiny intensifies. Incumbents able to fund chemical-recycling lines, redesign packs for tethered-cap rules, and meet high recycled-content thresholds secure competitive insulation while smaller converters confront escalating compliance costs. Concurrently, logistics inflation elevates the value proposition of lightweight flexible formats that trim freight bills, strengthening supplier contracts in e-commerce, food, and healthcare channels. Consolidation accelerates as scale becomes prerequisite for funding advanced R&D and closed-loop supply agreements.

Last-mile delivery models expose packages to multiple handling events and dimensional weight billing, prompting brand owners to favor films, pouches, and mailers that shrink void space by up to 75% versus rigid alternatives. Amazon's frustration-free packaging protocol, now covering more than 300,000 SKUs, shapes de facto industry specifications and pushes SME sellers toward compliant polyethylene and polypropylene solutions. Automated sortation lines require mono-material constructions that withstand optical detection; mixed-material packs risk rejection and costly rework. A 15% reduction in package volume translates to 12% lower freight expenditure, more than offsetting the 8-10% material premium for high-performance flexible films. Barrier-coated flexibles also extend protection to electronics and temperature-sensitive pharmaceuticals, broadening addressable segments beyond food.

Urbanization, smaller household sizes, and longer working hours spur demand for single-portion, shelf-stable meals. Processed-food uptake among urban consumers rose 8.2% year-on-year in 2024, the fastest climb on record.Multilayer flexibles combining oxygen and moisture barriers plus microwave compatibility outperform paper-based options on shelf-life and safety. Beverage innovators add tethered closures and tamper-evident features, absorbing EUR 0.02-0.04 extra per unit in manufacturing cost to avoid regulatory penalties. Extended shelf-life packs enable dairy and juice brands to reach rural areas lacking cold chains, further cementing flexible dominance in emerging markets.

California's bag prohibitions, the UK's wet-wipe ban, and South Australia's EPS restrictions remove entire product categories virtually overnight. Enforcement includes import restrictions and stiff fines, driving emergency reformulations and CapEx outlays. Academic work on Ghana's proposed bag bans estimates weekly tax-revenue losses of USD 0.34 million, underscoring broader economic spillovers. Multinationals grapple with divergent definitions of "single-use" across jurisdictions, complicating global SKU harmonization. As legislators widen scope beyond obvious disposable items, additional volume risks emerge for food-service and secondary-packaging formats.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Flexible formats commanded 54.10% of 2025 sales and are forecast to grow at 4.41% annually through 2031, expanding the plastic packaging market far faster than rigid alternatives. Fuel cost inflation and dimensional-weight freight tariffs reinforce a structural migration toward pouches, mailers, and wrap films that cut outbound logistics charges. Films and wraps gain further traction as converters deploy mono-material options that satisfy EPR frameworks without compromising shelf life. Rigid bottles, jars, and trays retain indispensability where structure or premium shelf presence is paramount, yet their share gradually declines as resealable zippers, spouts, and stand-up formats erode historical feature advantages. Integrated suppliers offering both formats secure higher wallet share as brand owners streamline vendor bases.

Rigid-package sub-segments confront margin pressure when resin spikes outpace pass-through ability, whereas flexible peers mitigate exposure through lighter gram-weight per unit. Glass and metal replacements remain niche, limited to beverages and canned foods. Tray makers preserve relevance in food-service channels where oven-safe or microwave-ready features command price premium. Overall, flexibles' dual leadership in volume and growth cements their central role in driving the plastic packaging market over the forecast horizon.

Although polyethylene held 41.85% plastic packaging market share in 2025, polypropylene's superior 5.55% CAGR positions it as the fastest-advancing resin family. PP's higher heat resistance, improved clarity, and better seal integrity facilitate mono-material solutions that meet recyclability mandates while safeguarding food safety. PET protects its beverage stronghold owing to established bottle-to-bottle recycling loops, yet mechanical-recycling limitations cap recycled content without costly chemical-recycling capacity additions. PVC, polystyrene, and other styrenics retreat under stricter environmental rules and brand-owner deselection, opening space for bio-based and specialty co-polymer niches.

Chemical-recycling economics further favor resins with stable depolymerization pathways; hence PET and PP attract greater capex, while PS and PVC projects struggle to clear investment hurdles. Resin suppliers differentiate through application engineering teams that guide converters during material transitions, a service highly prized amid evolving EPR frameworks and FDA food-contact rules.

The Plastic Packaging Market Report is Segmented by Packaging Type (Rigid Packaging Type, Flexible Packaging Type), Material (Polyethylene, PET, Polypropylene, Polystyrene and EPS, PVC, Others), End-User Industry (Food, Beverage, Healthcare and Pharmaceuticals, and More), Distribution Channel (Direct Sales, Indirect Sales), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific controlled 40.80% of global revenue in 2025 and is expanding at 6.78% CAGR, making it the undisputed engine of plastic packaging market growth. China accounts for the lion's share, though stricter waste-import rules and carbon-neutrality pledges compel local producers to invest in recycling capacity. India, Vietnam, and Indonesia record double-digit volume gains as organized retail and e-commerce penetration deepens. Currency volatility and geopolitics prompt multinational brand owners to diversify sourcing into ASEAN nations, reducing overreliance on any single country.

North America manifests steady mid-single-digit expansion underpinned by pharmaceutical demand, fresh-produce logistics, and the build-out of advanced-recycling hubs. State-level plastic-waste legislation adds complexity, yet it simultaneously opens opportunities for recycled and mono-material innovators. Canada's forthcoming nationwide EPR framework accelerates shift toward recyclable packs, encouraging cross-border partnerships.

Europe, the epicenter of EPR and tethered-cap mandates, experiences modest value growth but exerts outsized influence on global design standards. High labor and energy costs incentivize process automation and resin lightweighting, while regulators push recycled-content thresholds that drive chemical-recycling investments. Eastern European converters attract reshoring projects as brands seek regional proximity without Western Europe's cost base, spurring capital inflows into Poland and Hungary.

Latin America and the Middle East & Africa trail in share but register pockets of rapid expansion. Brazil benefits from agrifood exports that require barrier packaging, whereas GCC nations leverage petrochemical integration to export competitively priced resin. African markets begin to legislate single-use bans, creating fertile terrain for flexible producers that can deliver low-gram-weight, high-barrier solutions at affordable price points.