ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

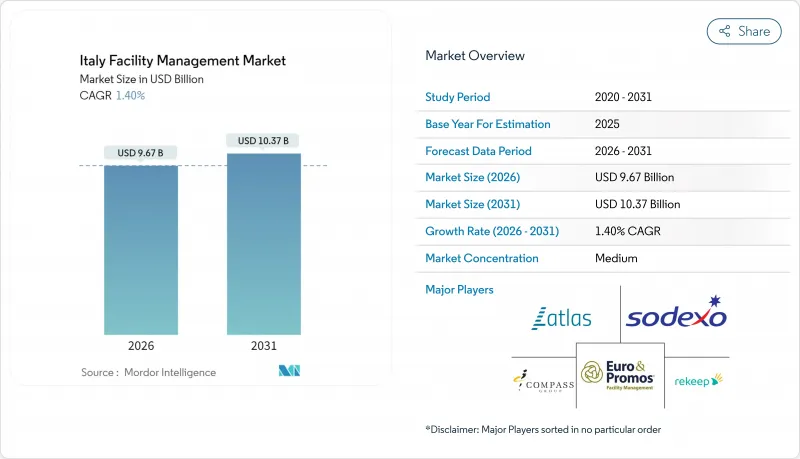

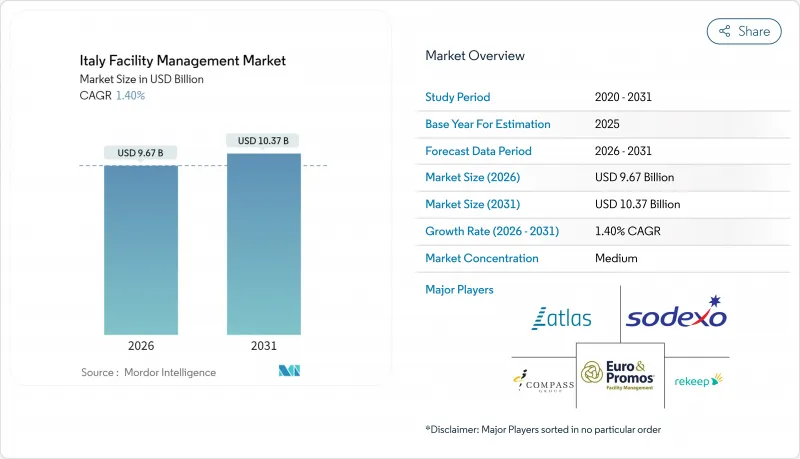

이탈리아의 시설 관리 시장은 2025년 95억 4,000만 달러에서 2026년에는 96억 7,000만 달러에 이를 것으로 예측됩니다. 2026-2031년에 걸쳐 CAGR 1.4%로 성장을 지속하여 2031년까지 103억 7,000만 달러에 이를 전망입니다.

측정된 성장은 국가 회복 및 회복력 계획, 상업용 부동산의 점진적 반등, 전기 및 가스 가격 상승에도 불구하고 통합 계약에 대한 수요 증가로 거슬러 올라간다. 예측 유지보수의 확산, 자산 소유자의 강화된 ESG 감시, 새로운 공공 조달 규정이 모두 이탈리아의 시설 관리 시장의 경쟁 논리를 형성했으며, 기술 지출은 IoT 기반 HVAC 최적화와 원격 자산 모니터링으로 계속 전환되었습니다. 이탈리아의 시설 관리 시장의 핵심인 하드 서비스는 2024년에도 견고한 기반을 유지했으나, 관광업이 호텔 및 고급 리조트로의 자본 유입을 주도하면서 소프트 서비스 수요가 가속화되었습니다. 북부 지역의 노동력 부족으로 공급업체 마진이 압박을 받으면서, 보수를 측정 가능한 건물 성능 지표에 연계하는 자동화 및 성과 기반 계약 모델로의 전환이 촉진되었습니다.

이탈리아의 시설 관리 시장 동향 및 인사이트

공공 부문 기관의 아웃소싱 동향으로 FM 시장 확대

지방자치단체 예산 축소로 인해 공공 조달 규정(D.Lgs. 36/2023)이 입찰 절차를 간소화한 후 비핵심 업무 아웃소싱이 가속화되었으며, 이는 지자체가 성과 기반 계약 하에 여러 서비스를 묶어 발주할 수 있게 했습니다. 예를 들어 토스카나 지역은 38개 박물관에 대한 관리 책임을 단일 공급자에게 부여함으로써 조정 비용을 절감하면서도 서비스 일관성을 개선하는 확장 가능한 문화유산 아웃소싱 모델을 입증했습니다. 대규모 프레임워크는 통합 디지털 플랫폼과 IoT 도입을 촉진하여 이탈리아 시설 관리 시장에 지속적인 성장 동력을 제공했습니다.

이탈리아의 관광 및 호스피탈리티 산업의 성장이 소프트 FM 서비스 수요 촉진

2024년 호텔 투자액은 21억 유로(24억 달러)를 초과하며 10년 평균 대비 30% 증가, 로마 및 베니스 및 밀라노 리조트들은 하우스키핑 및 컨시어지 및 케이터링 등 고집중 서비스에 집중. 일일 평균 요금은 4% 상승했으며, 방문객 수는 6,450만 명을 기록했습니다. 이는 계절적 변동에 따라 유연하게 대응할 수 있는 공급업체를 촉진했습니다. 지속가능성 인증과 에너지 효율적인 백오피스 운영이 핵심 선정 기준으로 부상하면서 기술 기반 소프트 서비스 제공이 더욱 가속화되었고, 이는 이탈리아 시설 관리 시장의 단기적 확장을 뒷받침했습니다.

이탈리아 지역별 분산된 규제 체계로 인한 준수 비용 복잡화

이탈리아의 20개 주는 D.Lgs. 81/2008(노동안전보건법)에 근거한 직장안전의 집행 권한을 보유하고 있으며, 검사 스케줄과 서류 형식에 차이가 발생하고 있습니다. 2025년 5월 국가-지역 협정을 통한 교육 표준화 노력은 불균등하게 진행되어 다지역 FM 제공업체들이 맞춤형 규정 준수 팀을 유지하도록 강요하고 국경 간 규모의 경제 효과를 저해했습니다. 이러한 비용은 결국 이탈리아 시설 관리 시장의 영업 마진 증가분 일부를 상쇄합니다.

부문 분석

2025년 현재 하드 서비스는 이탈리아의 시설 관리 시장 점유율의 58.85%를 차지했습니다. 의무화된 방화검사, MEP 설비의 업그레이드, 공조설비의 개수가 이 우위성을 지원했습니다. 특히 병원시설에서는 연간 FM 지출이 평균 161.58유로/㎡에 달하고 있습니다. 하드 서비스 부문 이탈리아 시설관리 시장 규모는 재량적 지출이 위축된 상황에서도 규정 준수 주도 투자가 물량을 완충하며 소폭 성장했습니다.

그러나 소프트 서비스는 2031년까지 연평균 복합 성장률(CAGR) 2.38%의 전망을 보였습니다. 이것은 고급 관광의 회복과 위생 및 케이터링 및 보안 기준을 향상시킨 직장 프로토콜의 진화에 뒷받침된 것입니다. 의료 및 호텔 고객사가 감염 관리 절차를 강화함에 따라 청소 서비스가 특히 큰 성장세를 보였습니다. 라치오 지역 본부에서 진행된 디지털 트윈 시범 운영은 공간 최적화 분석이 환경 품질과 입주자 경험 간의 연계성을 강화하여 소프트 서비스 제공업체에게 고수익 자문 역할을 부여하는 방식을 보여주었습니다.

이탈리아의 시설 관리 시장은 서비스 유형(하드 서비스, 소프트 서비스), 제공 형태(사내 제공, 아웃소싱), 최종 사용자 업계(상업(IT 및 통신, 소매 및 창고), 호스피탈리티(호텔, 음식점, 대규모 레스토랑), 공공 및 공공 인프라(정부, 교육, 교통)) 등에 의해 구분되고 있습니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

Euro & Promos Facility Management SPA(EURO & PROMOS)

Rekeep SpA

Olly Services SRL

NAZCA

Elmet SRL

Apleona GmbH

SGI Srl

CNS Consorzio Nazionale Servizi

Siram SpA

BumaQ Srl

Ares Facility Management

P&P Spa

제7장 시장 기회와 장래의 전망

HBR

영문 목차

영문목차

The Italy facility management market is expected to grow from USD 9.54 billion in 2025 to USD 9.67 billion in 2026 and is forecast to reach USD 10.37 billion by 2031 at 1.4% CAGR over 2026-2031.

The measured expansion traced back to the National Recovery and Resilience Plan, the gradual rebound of commercial real estate, and stepped-up demand for integrated contracts despite rising electricity and gas prices. Growing adoption of predictive maintenance, heightened ESG scrutiny from asset owners, and new public-procurement rules all shaped the competitive logic of the Italy facility management market, while technology spending continued to shift toward IoT-enabled HVAC optimisation and remote asset monitoring. The hard-services core of the Italy facility management market retained a strong base in 2024, yet soft-services demand accelerated as tourism led capital inflows back into hotels and luxury resorts. Provider margins came under pressure from labour shortages in northern regions, prompting a shift towards automation and outcome-based contracting models that tie remuneration to measurable building-performance metrics.

Italy Facility Management Market Trends and Insights

Outsourcing Trend Among Public Sector Entities Expanding FM Market

Reduced municipal budgets intensified the outsourcing of non-core activities after the Public Procurement Code (D.Lgs. 36/2023) simplified tendering, enabling municipalities to bundle multiple services under performance-based contracts. The Tuscany region, for instance, awarded a single provider responsibility for 38 museums, demonstrating scalable cultural heritage outsourcing models that trim coordination costs while improving service consistency. Larger frameworks encouraged unified digital platforms and IoT adoption, creating sustained momentum for the Italy facility management market.

Growth of Italy's Tourism and Hospitality Sector Boosts Demand for Soft FM Services

Hotel investments exceeded EUR 2.1 billion(USD 2.4 billion) in 2024-30% above the decade average-prompting resorts in Rome, Venice, and Milan to sharpen focus on high-presence services such as housekeeping, concierge and catering. Average daily rates rose 4% alongside 64.5 million visitor arrivals, spurring providers that could flex capacity with seasonal volatility. Sustainability labels and energy-efficient back-of-house operations emerged as core selection criteria, further propelling technology-driven soft-service offerings and underpinning near-term expansion of the Italy facility management market.

Fragmented Regulatory Framework Across Italian Regions Complicates Compliance Costs

Italy's 20 regions retained discretion over workplace-safety enforcement under D.Lgs. 81/2008, leading to divergent inspection schedules and documentation formats. Efforts to harmonise training through the May 2025 State-Regions agreement progressed unevenly, forcing multi-region FM providers to maintain bespoke compliance teams and dampening cross-border economies of scale. These costs ultimately offset a portion of operating-margin gains in the Italy facility management market.

Other drivers and restraints analyzed in the detailed report include:

Increasing Adoption of Integrated Facility Management Contracts for Cost Optimization

Aging Building Stock Requiring Predictive Maintenance and Retrofit Services

Rising Costs of Skilled Technical Labor Squeeze FM Provider Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard services held 58.85% of the Italy facility management market share in 2025. Mandatory fire-safety inspections, MEP upgrades, and HVAC retrofits underpinned this dominance, especially within hospital estates that averaged EUR 161.58 per m2 in annual FM outlay. The Italy facility management market size for hard services advanced modestly as compliance-led investment cushioned volume even when discretionary spending softened.

Soft services nonetheless registered a 2.38% CAGR outlook through 2031, buoyed by the revival of luxury tourism and evolving workplace protocols that elevated hygiene, catering, and security standards. Cleaning services captured outsized gains as healthcare and hospitality clients enforced stricter infection-control routines. Digital Twin pilots at the Lazio Region headquarters illustrated how space-optimisation analytics tightened the linkage between environmental quality and occupant experience, giving soft-service providers higher-margin advisory roles.

Italy Facility Management Market is Segmented by Service Type (Hard Service, Soft Service), Offering Type (In-House, Outsourced), End-User Industry (Commercial (IT and Telecom, Retail and Warehouses), Hospitality (Hotels, Eateries and Large-Scale Restaurants), Institutional and Public Infrastructure (Government, Education, Transportation)) and More. The Market Forecasts are Provided in Terms of Value (USD).

5.3.3 Institutional and Public Infrastructure (Government, Education, Transportation)

5.3.4 Healthcare (Public and Private Facilities)

5.3.5 Industrial and Process (Manufacturing, Energy, Mining)

5.3.6 Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure)

6 COMPETITIVE LANDSCAPE

6.1 Market Concentration

6.2 Strategic Moves and Partnerships

6.3 Market Share Analysis

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)