아시아태평양의 살선충제 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Asia Pacific Nematicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1683205

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

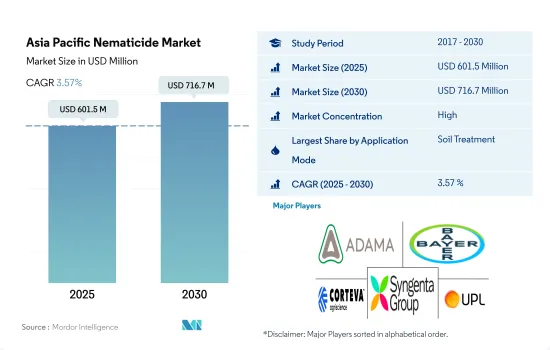

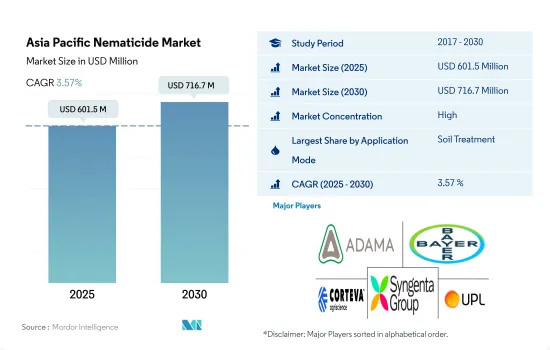

아시아태평양의 살선충제 시장 규모는 2025년에는 6억 150만 달러로 추정되고, 2030년에는 7억 1,670만 달러에 이를 것으로 예측되며, 예측 기간 중 2025년부터 2030년까지 CAGR은 3.57%로 성장할 것으로 예측됩니다.

비표적 생물에 대한 노출 위험이 적기 때문에 토양 적용형 살선충제가 시장을 석권

식물의 일부를 식해하는 선충을 식물 기생 선충(PPN)이라고 합니다. 살선충제는 잎 표면 살포, 화학 살포, 토양 처리와 같은 다양한 살포 방법을 통해 이러한 선충을 방제하는 데 사용됩니다.

잎 표면 살포와 같은 다른 살포 방법과 비교할 때, 일반적으로 선충제의 토양 살포는 유익한 곤충과 꽃가루 매개자를 포함한 비표적 생물에 노출될 위험이 적습니다. 왜냐하면 살선충제는 주로 토양에 머물며 표적 선충이 서식하고 있기 때문입니다. 이 때문에 토양 시용이 2022년에는 69.3%의 점유율을 차지하였고 시장을 독점했습니다.

엽면 살포는 2022년에 아시아태평양 살선충제 시장의 12.8%를 차지했습니다. 잎 표면 살포의 주요 목적은 밀과 같은 곡류의 원인 선충으로도 알려진 Anguina tritici와 같은 선충에 의한 화서에 대한 침입과 잎으로의 침입을 방제하는 것입니다. 잎 표면 살포는 메틸 브로마이드, 옥사밀, 팔라티온과 같은 활성 성분을 사용하기 때문에 선충에 효과적입니다.

화학 관개는 2022년 아시아태평양 선충제 시장의 8.0%를 차지했습니다. 중국은 화학 관개 부문에서 36.2% 시장 점유율을 차지했으며, 2022년 시장 규모는 1,640만 달러였습니다. 곡물 시스트 선충 Heterodera avenae는 중국의 청해 티베트 고원과 황하 지역의 주요 선충 해충 중 하나로 밀과 같은 주요 작물에서 10-90%의 수율 손실을 일으키는 것으로 보고되었습니다.

선충의 침입으로 인한 농작물의 손실은 해마다 증가하고 있으며, 농업 종사자에게 큰 문제가 되고 있습니다.

식량 수요 증가로 인한 농작물 보호의 필요성이 시장 성장의 원동력이 되고 있습니다.

농업이 번성하고 음식 수요가 증가하고 있는 아시아태평양에서는 선충의 침입으로부터 작물을 보호하기 위해 살선충제의 사용이 증가하고 있습니다. 2022년에 이 지역은 금액 기준으로 세계 작물 보호 시장의 19.8%를 차지했습니다.

이 지역은 농업이 번성하고 중국, 인도, 일본, 호주 등이 주요 공헌국입니다. 농업 종사자는 수요 증가에 대응하고, 작물의 품질을 확보하기 위해, 선충으로부터 작물을 보호하는 대책을 채용하고 있으며, 시장의 성장을 가속하고 있습니다.

이 시장은 2023년부터 2029년까지 1억 3,890만 달러의 성장이 전망되고 있습니다. 농업 종사자는 선충이 작물의 수율에 미치는 부정적인 영향에 대한 인식을 깊게 하고 있습니다. 선충의 만연은 생산성 저하, 성장 저해, 심지어 부작용으로 이어질 수 있습니다. 이러한 인식에서 농업 종사자는 작물을 보호하기 위해 살선충제에 투자합니다.

특히 인도네시아, 태국, 중국, 인도 등 국가에서는 상업적 농업 확대가 살선충제 수요를 끌어올리고 있습니다. 대규모 농업 경영에서는 제한된 장소에 작물이 집중되기 때문에 선충의 침입을 받기 쉽습니다. 따라서 영리 목적의 농업 종사자는 작물을 보호하고 높은 수율을 보장하기 위해 종종 살선충제에 의존합니다.

아시아태평양의 살선충제 시장은 농산물 수요 증가, 선충에 의한 농작물 손실에 대한 의식 증가, 상업적 농업 확대로 예측 기간 중(2023-2029년) 금액 기준으로 CAGR 3.8%를 나타낼 것으로 예측됩니다. 이 지역의 농업이 더욱 발전하고 선충의 만연이 초래하는 과제에 대처함에 따라 이러한 동향은 앞으로도 계속될 것으로 예상됩니다.

아시아태평양 선충제 시장 동향

선충 구제의 중요성에 대한 농업 종사자의 의식 증가가 살선충제의 살포를 증가시키고 있습니다.

일본은 1헥타르당 살선충제 소비량이 최대이며 2022년 농지 1헥타르당 평균 소비량은 478.7그램입니다. 그러나 일본은 이 지역 농지 전체의 0.45%를 차지할 뿐, 2022년에는 불과 290만 헥타르에 불과했습니다. 일본에서는 하우스 재배나 단작 등의 집약적 농법이 보급되고 있습니다. 이러한 농법은 생산성을 극대화한다는 이점이 있는 한편, 선충과 같은 토양 전염성 해충에 대한 작물의 취약성을 높이기 위해 일본의 농업 종사자는 작물을 지키기 위해 살선충제에 의존하게 됩니다.

호주는 헥타르당 살선충제 소비량이 두 번째로 많으며 2022년에는 헥타르당 63.6g을 소비했습니다. 이것은 호주 생산자와 잔디 관리자에게 식물 기생 선충이 초래하는 막대한 숨겨진 비용으로 인한 것입니다. 호주에서는 최대 1,900만 헥타르의 경작지와 어메니티 잔디가 기생선충의 악영향을 받고 연간 3억 달러의 손실을 입은 것으로 추정됩니다.

호주에 이어지는 것은 필리핀과 베트남으로, 2022년 살선충제 사용량은 각각 헥타르당 46.3g과 41.1g입니다. 필리핀에서는 뿌리 벌레 선충이 큰 문제가 되고 있습니다. 특히 토마토와 같은 야채 작물에서는 재배 품종과 지역에 따라 다르지만 20%에서 85%의 손실을 초래하는 것으로 알려져 있습니다.

중국, 태국, 미얀마, 인도는 이 지역에서 살선충제를 대량으로 소비하는 기타 국가이며 선충의 만연이 증가하고 있기 때문입니다. 그러나 농업 종사자의 의식이 높아지고 농작물을 보호할 필요성이 높아짐에 따라 살선충제의 사용량이 증가하고 있습니다.

선충의 침입으로 인한 농작물의 손실은 해마다 증가하고 있으며, 살선충제의 가격에도 영향을 미치고 있습니다.

식물 기생 선충(PPN)은 식량 안보와 식물 건강에 가장 악명 높고 과소 평가된 위협 중 하나입니다. 예를 들어 인도에서는 주요 식물 기생 선충에 의한 연간 작물 손실은 19.6%, 2,421억 루피로 추정됩니다. 야채 재배에서 식물 기생 선충은 주요 해충 중 하나로 알려져 있습니다. 플루엔술폰, 아바멕틴, 옥사밀은 아시아태평양에서 일반적으로 사용되는 살선충제입니다.

플루엔술폰은 2022년 1톤당 미화 1만 9,000달러로 평가되었습니다. 플루엔술폰은 뿌리 딱정벌레 선충(Meloidogyne spp.), 감자시스트 선충, 침선충, 피침선충, 자선충, 왜성 근선충(Trichodorus spp. 및 Paratrichodorus spp.), 병반선충 등의 선충을 억제하는데 사용됩니다.

아바멕틴은 뿌리병선충(Pratylenchus penetrans), 신장선충(Rotylenchulus reniformis), 뿌리즙 선충(Meloidogyne incognita), 시스트선충(Heterodera schachtii) 등 여러 식물 기생선충에 대해 살선충 활성이 있는 것으로 알려져 있습니다. 아바멕틴은 2022년 1톤당 미화 12,200달러로 평가되었습니다.

옥사밀은 카르바마트계 살선충제로 액체와 입상으로 제조되고 있습니다. Oxamyl은 아래로 이동하는 전신 활동을 가진 유일한 살선충제이기 때문에 Pratylenchus 선충의 감소에 도움이되는 엽면 살선충 용도가 있습니다. 옥사밀은 2022년 1톤당 8,700달러로 평가되었습니다.

선충의 침입으로 인한 농작물의 손실은 해마다 증가하고 있으며, 농업 종사자에게 큰 우려 사항이 되어 농작물을 보호하기 위해 살선충제를 사용할 수 밖에 없게 되고 있습니다. 이 요인은 살선충제의 가격에 영향을 미칠 것으로 예상됩니다.

아시아태평양의 살선충제 산업 개요

아시아태평양의 살선충제 시장은 상당히 통합되어 있으며 상위 5개사에서 86.26%를 차지하고 있습니다. 이 시장의 주요 기업은 ADAMA Agricultural Solutions Ltd, Bayer AG, Corteva Agriscience, Syngenta Group, UPL Limited입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

조사 전제조건 및 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

1헥타르당 농약 소비량

유효성분의 가격 분석

규제 프레임워크

호주

중국

인도

인도네시아

일본

미얀마

파키스탄

필리핀

태국

베트남

밸류체인 및 유통채널 분석

제5장 시장 세분화

용도 모드별

화학 관개

잎면 살포

훈증

종자 처리

토양 처리

작물 유형별

상업 작물

과일 및 야채

곡물

콩류 및 지방종자

잔디 및 관상용

국가별

호주

중국

인도

인도네시아

일본

미얀마

파키스탄

필리핀

태국

베트남

기타 아시아태평양

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

ADAMA Agricultural Solutions Ltd

American Vanguard Corporation

Bayer AG

Corteva Agriscience

Syngenta Group

UPL Limited

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

AJY

영문 목차

영문목차

The Asia Pacific Nematicide Market size is estimated at 601.5 million USD in 2025, and is expected to reach 716.7 million USD by 2030, growing at a CAGR of 3.57% during the forecast period (2025-2030).

Soil application of nematicides dominated the market owing to fewer risks of exposing non-target organisms

Nematodes that feed on plant parts are called plant parasitic nematodes (PPN). Nematicides are used to control these nematodes through various application methods like foliar application, chemigation, and soil treatment.

Compared to other application methods, such as foliar application, soil application of nematicides generally poses fewer risks of exposing non-target organisms, including beneficial insects and pollinators. This is because the nematicide remains primarily in the soil, where the target nematodes reside. Owing to this, soil application dominated the market with a share of 69.3% in 2022.

Foliar applications accounted for 12.8% of the Asia-Pacific nematicide market in 2022. The main purpose of the foliar application is to control the infestation of inflorescence and the infestation of leaves by nematodes such as the Anguina tritici (seed gall nematode), also known as seed gall disease-causing nematodes, which are present in cereals such as wheat. Foliar application is effective against nematodes due to the use of active ingredients like methyl bromide, Oxamyl, and parathion.

Chemigation accounted for 8.0% of the Asia-Pacific nematicide market in 2022. China dominated the chemigation segment with a market share of 36.2%, valued at USD 16.4 million in 2022. The cereal cyst nematode, Heterodera avenae, is one of the major nematode pests in the Qinghai-Tibetan Plateau and Yellow River regions of China; it is reported to cause 10-90% yield losses in major crops like wheat.

Crop losses due to nematode infestation are increasing every year and are acting as a major concern for farmers, forcing them to use nematicides in order to protect the crops.

The need to protect the crops due to rising food demand is driving the growth of the market

Asia-Pacific, with its large agricultural industry and increasing demand for food, has witnessed a rise in the use of nematicides to protect crops from nematode infestations. In 2022, the region accounted for 19.8% of the global crop protection market by value.

The region has a substantial agricultural industry, with countries like China, India, Japan, and Australia being major contributors. Farmers are adopting measures to protect their crops from nematodes to meet the growing demand and ensure the quality of crops, thus driving the market's growth.

The market is expected to grow by USD 138.9 million during 2023-2029. Farmers are becoming more aware of the detrimental effects of nematodes on crop yields. Nematode infestations can lead to reduced productivity, stunted growth, and even crop failure. This awareness has prompted farmers to invest in nematicides to protect their crops.

The expansion of commercial farming, particularly in countries like Indonesia, Thailand, China, and India, has driven the demand for nematicides. Large-scale farming operations are more susceptible to nematode infestations due to the concentration of crops in a confined area. Therefore, commercial farmers often rely on nematicides to protect their crops and ensure higher yields.

The Asia-Pacific nematicide market is projected to register a CAGR of 3.8% by value during the forecast period (2023-2029) due to the increasing demand for agricultural products, rising awareness about nematode-related crop losses, and expansion of commercial farming. These trends are expected to continue as the region's agricultural industry further develops and addresses the challenges posed by nematode infestations.

Asia Pacific Nematicide Market Trends

Growing awareness among farmers about the importance of nematode control is increasing the application of nematicides

Japan is the largest consumer of nematicides per hectare, with an average consumption of 478.7 grams per hectare of agricultural land in 2022. However, Japan only accounted for 0.45% of the total agricultural land in the region, with just 2.9 million hectares in 2022. Intensive farming practices, such as greenhouse cultivation and monocropping, are prevalent in Japan. While these practices have their advantages in maximizing productivity, they also increase the vulnerability of crops to soil-borne pests like nematodes, leading the farmers in Japan to rely on nematicides to safeguard their crops.

Australia is the second-highest consumer of nematicides per hectare, with a consumption of 63.6 grams per hectare in 2022. This could be attributed to the huge hidden cost posed by plant parasitic nematodes to Australian producers and turf managers. It has been estimated that up to 19 million hectares of cultivated land and amenity turf are negatively impacted by parasitic nematodes in Australia, resulting in annual losses of USD 300 million.

Australia is closely followed by the Philippines and Vietnam, with nematicide consumptions of 46.3 and 41.1 grams per hectare, respectively, in 2022. Root-knot nematode is a major problem in the Philippines. It is known to cause losses between 20% and 85%, especially in vegetable crops like tomatoes, based on the cultivar and region grown.

China, Thailand, Myanmar, and India are other countries in the region that consume significant amounts of nematicides, owing to the increasing incidences of nematode infestation, which are often neglected by the farmers because of their hidden nature. However, the usage of nematicides is increasing with growing awareness among farmers and the need to protect the crops.

Crop losses due to nematode infestation are increasing every year, influencing the prices of nematicides

Plant parasitic nematodes (PPNs) are among the most notorious and underrated threats to food security and plant health. For instance, in India, the annual crop losses due to major plant parasitic nematodes are estimated to be 19.6%, valued at INR 242.1 billion. In vegetable cultivation, plant parasitic nematodes are considered among the major pests. Fluensulfone, Abamectin, and Oxamyl are commonly used nematicides in Asia-Pacific.

Fluensulfone was valued at USD 19.0 thousand per metric ton in 2022. It can be used to suppress nematodes, including root-knot nematodes (Meloidogyne spp.), potato cyst nematodes, needle nematodes, lance nematodes, sting nematodes, stubby root nematodes (Trichodorus and Paratrichodorus spp.), and lesion nematodes.

Abamectin is known to have nematicidal activity against some plant parasitic nematodes, including the root lesion nematode (Pratylenchus penetrans), the reniform nematode (Rotylenchulus reniformis), the root-knot nematode (Meloidogyne incognita), and the cyst nematode (Heterodera schachtii). Abamectin was valued at USD 12.2 thousand per metric ton in 2022.

Oxamyl is a carbamate nematicide that is manufactured in liquid and granular forms. Oxamyl is the only nematicide with downward-moving systemic activity; thus, it has foliar nematicidal applications that help to reduce Pratylenchus nematodes. Oxamyl was valued at USD 8.7 thousand per metric ton in 2022.

Crop losses due to nematode infestation are increasing every year and are acting as a major concern for farmers, forcing them to use nematicides in order to protect the crops. This factor is expected to influence the prices of nematicides.

Asia Pacific Nematicide Industry Overview

The Asia Pacific Nematicide Market is fairly consolidated, with the top five companies occupying 86.26%. The major players in this market are ADAMA Agricultural Solutions Ltd, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Consumption Of Pesticide Per Hectare

4.2 Pricing Analysis For Active Ingredients

4.3 Regulatory Framework

4.3.1 Australia

4.3.2 China

4.3.3 India

4.3.4 Indonesia

4.3.5 Japan

4.3.6 Myanmar

4.3.7 Pakistan

4.3.8 Philippines

4.3.9 Thailand

4.3.10 Vietnam

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

5.1 Application Mode

5.1.1 Chemigation

5.1.2 Foliar

5.1.3 Fumigation

5.1.4 Seed Treatment

5.1.5 Soil Treatment

5.2 Crop Type

5.2.1 Commercial Crops

5.2.2 Fruits & Vegetables

5.2.3 Grains & Cereals

5.2.4 Pulses & Oilseeds

5.2.5 Turf & Ornamental

5.3 Country

5.3.1 Australia

5.3.2 China

5.3.3 India

5.3.4 Indonesia

5.3.5 Japan

5.3.6 Myanmar

5.3.7 Pakistan

5.3.8 Philippines

5.3.9 Thailand

5.3.10 Vietnam

5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

6.4.1 ADAMA Agricultural Solutions Ltd

6.4.2 American Vanguard Corporation

6.4.3 Bayer AG

6.4.4 Corteva Agriscience

6.4.5 Syngenta Group

6.4.6 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS