ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

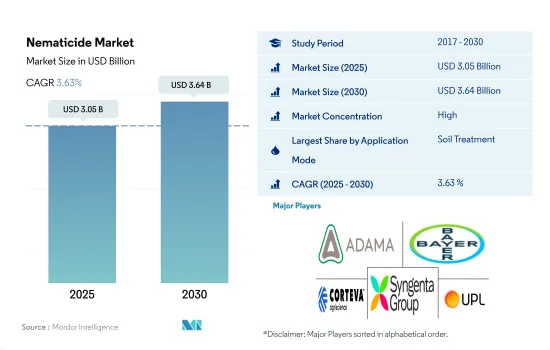

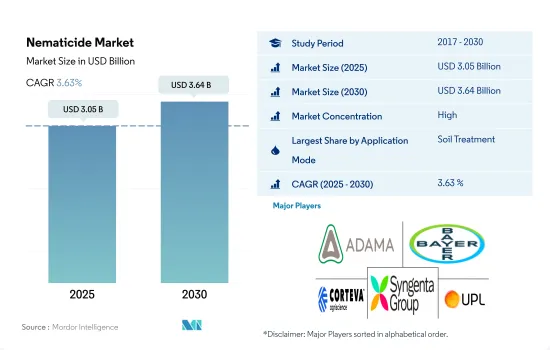

선충제 시장 규모는 2025년에 30억 5,000만 달러로 예측되고, 2030년에는 36억 4,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR은 3.63%를 나타낼 전망입니다.

토양 매개 선충에 의한 작물 초기 생육 피해 증가로 선충제의 토양 처리 적용 모드 증가

농업에서 선충의 성장은 가뭄, 폭염, 따뜻하고 습한 환경과 같은 기후 변화에 의해 촉진됩니다. 단일 재배 관행, 무경운, 모래 토양도 선충의 성장에 유리합니다.

토양 처리를 통한 선충제 살포는 2022년 70.3%의 시장 점유율을 차지했는데, 이는 이 방법이 토양 매개 선충 개체수를 줄이고 작물 생산성을 향상시키는 데 효과적이기 때문입니다. 이 방법은 작물을 심기 전과 심은 후 토양 관주를 통해 적용할 수 있으며, 작물의 발아를 빠르게 하는 데 도움이 됩니다.

선충제 살포의 엽면 살포 방법은 다음으로 가장 많이 사용되는 살포 모드이자 가장 빠르게 성장하는 부문으로, 예측 기간 동안 3.4 %의 CAGR을 기록 할 것으로 예상됩니다. 엽면 선충제 살포는 식물의 잎을 먹이로 하는 엽면 선충을 효과적으로 관리하여 식량 작물의 수확량을 감소시킵니다. 드론 애플리케이션 및 기타 기술 및 디지털 개선과 같은 발전으로 엽면 살포 모드의 활용도가 높아지고 있습니다.

2022년 8.5%의 시장 점유율을 차지한 화학 처리 모드를 통해 물과 선충제 양을 효과적으로 관리할 수 있습니다. 관개 시스템이 발전하고 물 부족이 증가하면 화학 처리 채택률이 높아져 선충제 살포가 증가할 것입니다.

모든 살포 모드는 선충 감염을 줄이고 작물 생산성을 높이는 것을 목표로 하며, 이는 시장을 주도할 것으로 예상됩니다.

선충 감염 증가와 선충제 채택 증가로 두드러진 위치에 서게 된 남미

선충은 기후 변화와 기타 해충 및 질병 외에도 전 세계 농업 부문에 심각한 피해를 입히고 있습니다. 4100종 이상의 식물 기생 선충이 확인되어 전 세계의 다양한 작물에 피해를 입히고 있습니다.

미국 식물병리학회에 따르면 선충은 매년 전 세계 농작물 손실의 약 14%를 유발하며, 이는 약 1,250억 달러의 경제적 손실과 맞먹는 수치입니다. 다양한 선충류 중에서도 뿌리혹선충(Meloidogyne spp.), 시스트 선충(Heterodera spp., Globodera spp.), 뿌리 콩나물 선충(Pratylenchus spp., Hirschmanniella spp 및 Radopholus spp.), 줄기 선충(Ditylenchus spp. spp.)는 물과 양분의 흡수에 영향을 주어 작물의 성장과 생산성에 큰 피해를줍니다.

재배에 사용되는 선충제 소비는 주로 남미가 주도하고 있으며, 2022년 전 세계 선충제 시장의 37.4%를 차지할 것으로 예상됩니다. 이는 선충으로 인한 농작물 손실이 매년 약 65억 달러에 달하는 데 주로 기인합니다. 대두는 주요 재배 작물이며, 남미는 전 세계 대두 생산량의 50% 이상을 생산합니다. 선충은 이 지역에서 30억 달러에 달하는 수확량 손실의 약 30%를 유발합니다. 2023년부터 2029년 사이에 1만 100톤 이상 증가할 것으로 예상되고 있습니다. 이는 남미 농업 산업에서 선충제의 필요성을 강조합니다.

세계의 선충제 시장은 예측 기간중(2023년-2029년)에 CAGR 3.7%로 성장할 것으로 예측되며, 이는 전 세계적으로 다양한 선충으로부터 작물을 보호하기 위한 선충제 채택이 증가함에 따라 주도될 것입니다.

세계의 선충제 시장 동향

집약적인 농업 관행으로 선충제 살포의 필요성 증가

2022년의 화학선충제의 세계 평균 소비량은 농지 1헥타르당 2.1kg이었습니다. 이러한 방식은 생산성을 향상시키지만 선충과 같은 토양 매개 해충에 대한 작물의 취약성을 높입니다. 따라서 농부들은 농작물을 보호하기 위해 선충제에 의존하는 경우가 많습니다.

유럽은 2022년에는 1헥타르당 591.7그램의 선충제를 사용하여 헥타르당 소비량이 2번째로 많아졌습니다. 유럽 국가들은 선충 피해에 더 취약한 채소, 과일, 관상용 작물 등 고부가가치 작물 재배를 확대하고 있습니다. 식물 기생 선충은 유럽 국가에서 연간 21.3%의 수확량 손실을 유발하며, 이는 15억 8,000만 달러에 달합니다.

남미는 2022년에 헥타르당 570.14그램으로 세 번째로 많은 선충제를 소비한 지역입니다. 뿌리혹선충은 이 지역의 토마토, 감자, 당근을 비롯한 다양한 식물의 뿌리와 괴경을 공격합니다. 당근은 평균 20.0%까지 상당한 손실을 입기 쉽고, 감자는 이 선충 종에 의한 감염으로 인해 최대 33.0%까지 더 높은 손실을 경험할 수 있습니다.

변화하는 기후 조건과 선충 감염에 미치는 영향은 선충제 수요와 가격을 동시에 상승

선충제는 식물 기생 선충을 효과적으로 방제하고, 뿌리 손상으로부터 작물을 보호하며, 최적의 수확량과 생산성을 보장함으로써 농업에서 중요한 역할을 합니다.

플루펜설폰은 아릴설포네이트 계열의 화학 물질에 속하는 선충제입니다. 다양한 농작물에서 뿌리혹선충, 낭종선충, 병변선충, 단검선충과 같은 식물 기생 선충을 방제하는 데 사용됩니다. 플루펜설폰의 작용 방식은 선충의 신경계를 방해하여 마비 및 사망에 이르게 하는 것입니다. 플루펜설폰은 선충을 표적으로 삼아 선충의 개체 수를 줄이고 작물에 미칠 수 있는 피해를 최소화하는 데 도움이 됩니다.

선충제 산업 개요

선충제 시장은 상당히 통합되어 있으며 상위 5개사에서 85.65%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

1헥타르당 농약 소비량

유효성분의 가격 분석

규제 프레임워크

호주

캐나다

중국

프랑스

독일

인도

인도네시아

이탈리아

일본

멕시코

미얀마

네덜란드

파키스탄

필리핀

러시아

남아프리카

스페인

태국

우크라이나

영국

미국

베트남

밸류체인과 유통채널 분석

제5장 시장 세분화

적용 모드

화학 처리

엽면 살포

훈증

종자 처리

토양 처리

작물 유형

상업용 작물

과일 및 채소

곡물

콩류 및 유지 종자

잔디 및 관상용

지역

아프리카

국가별

남아프리카

기타 아프리카

아시아태평양

국가별

호주

중국

인도

인도네시아

일본

미얀마

파키스탄

필리핀

태국

베트남

기타 아시아태평양

유럽

국가별

프랑스

독일

이탈리아

네덜란드

러시아

스페인

우크라이나

영국

기타 유럽

북미

국가별

캐나다

멕시코

미국

기타 북미

남미

국가별

아르헨티나

브라질

칠레

기타 남미 국가

제6장 경쟁 구도

주요 전략적 움직임

시장 점유율 분석

기업 상황

기업 프로파일

ADAMA Agricultural Solutions Ltd.

Albaugh LLC

American Vanguard Corporation

Bayer AG

Corteva Agriscience

Syngenta Group

Tessenderlo Kerley Inc.(Novasource)

Upl Limited

Vive Crop Protection

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

출처 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

HBR

영문 목차

영문목차

The Nematicide Market size is estimated at 3.05 billion USD in 2025, and is expected to reach 3.64 billion USD by 2030, growing at a CAGR of 3.63% during the forecast period (2025-2030).

Increasing early crop growth damage by soil-borne nematodes raises the soil treatment application mode of nematicides

The growth of nematodes in agriculture is favored by changing climates like drought, heat waves, and warm and humid conditions. Monoculture practices, no-tillage, and sandy soils also favor their growth. Based on the types of nematodes, regions, and crops, farmers implement various nematicide application modes for better nematode management and enhancing crop production.

Nematicide application via soil treatment held a majority market share of 70.3% in 2022, which was majorly attributed to the effectiveness of this method in reducing soil-borne nematode populations and improving crop productivity. These can be applied prior to planting and after planting by soil drenching, which helps in faster crop germination. The soil treatment mode of nematicide application is expected to increase by around 17.3 thousand metric ton during 2023-2029.

The foliar method of nematicide application was the next most used application mode and fastest-growing segment, which is anticipated to register a CAGR of 3.4% during the forecast period. The foliar nematicide application effectively manages the foliar nematodes that feed on the foliage of the plant and reduces the yield of food crops. Advancements in foliar mode, like drone applications and other technical and digital improvements, raise the foliar mode of application.

Effective management of water and nematicide quantity can be achieved through the chemigation mode, which occupied the market share of 8.5% in 2022. Advanced irrigation systems and increased water scarcity will raise the chemigation adoption rate, increasing the nematicide application.

All the application modes aim to reduce nematode infestations and increase crop productivity, which is expected to drive the market.

Increased nematode infestations and the growing adoption of nematicides stood South America in prominent position

Apart from climate changes and other pests and diseases, nematodes cause significant damage to the agriculture sector worldwide. More than 4100 plant parasitic nematodes were identified, causing damage to various crops across the world.

According to the American Society of Phytopathology, nematodes cause around 14% of the global crop loss annually, which is equal to an economic loss of almost USD 125 billion. Among various nematode species root-knot nematodes (Meloidogyne spp.), cyst nematodes (Heterodera spp., Globodera spp.), root-lesion nematodes (Pratylenchus spp., Hirschmanniella spp., and Radopholus spp.), stem nematodes (Ditylenchus spp.), and pine wood nematodes (Bursaphlenchus spp.) majorly damage the crop growth and productivity by effecting the water and nutrients absorption.

The consumption of nematicides in its cultivation is majorly dominated by South America, which represented 37.4% of the global nematicide market in 2022. This is majorly attributed to the crop losses by nematodes, which are recorded at around USD 6.5 billion every year. Soybean is the major crop grown, and South America produces more than 50% of the soybeans produced in the world. Nematodes cause around 30% of yield loss worth USD 3 billion in the region. During the historical period, the consumption of nematicides increased by around 7.6 thousand metric ton between 2017 and 2022, which is further expected to increase by more than 10.1 thousand metric ton between 2023-2029. This emphasized the nematicide's necessity in the South American agriculture industry.

The global nematicide market is anticipated to grow during the forecast period (2023-2029) with an estimated CAGR of 3.7%, which will be driven by the growing adoption of nematicides for crop protection from various nematodes globally.

Global Nematicide Market Trends

Intensive agricultural practices have increased the need for nematicide application

The average global consumption of chemical nematicides was 2.1 kg per hectare of agricultural land in 2022. Asia-Pacific was the largest consumer of nematicides, with a per-hectare consumption of 737.02 grams in 2022. Asian countries, including Japan, commonly adopt intensive farming practices like greenhouse cultivation and monocropping. Although these methods enhance productivity, they also heighten crop vulnerability to soil-borne pests like nematodes. Consequently, farmers frequently resort to nematicides to protect their crops.

Europe was the second largest per-hectare consumer of nematicides, with 591.7 grams per hectare in 2022. European countries are expanding the cultivation of high-value crops, including vegetables, fruits, and ornamentals, which tend to be more susceptible to nematode damage. The plant-parasitic nematodes cause an annual yield loss of 21.3%, amounting to USD 1.58 billion in European countries. As a result, the use of nematicides becomes necessary to effectively manage and control these infestations in Europe.

South America was the third largest per-hectare consumer of nematicides, with 570.14 grams per hectare in 2022. Root-knot nematodes attack the roots and tubers of various plants, including tomatoes, potatoes, and carrots in the region. Carrots are susceptible to considerable losses, averaging up to 20.0%, while potatoes can experience even higher losses of up to 33.0% due to infestations caused by these nematode species. The nematode population in North American countries is increasing with the increasing adoption of no-tillage practices, which reduce soil disturbance and increase the retention of crop residue. These circumstances are leading to the application of nematicides globally.

Changing climatic conditions and their effect on nematode infestations may raise the demand for nematicides and their prices simultaneously

Nematicides play a crucial role in agriculture by effectively controlling plant-parasitic nematodes, protecting crops from root damage, and ensuring optimal yield and productivity.

Flufensulfone is a nematicide belonging to the chemical class of arylsulfonates. It is used to control plant-parasitic nematodes, such as root-knot nematodes, cyst nematodes, lesion nematodes, and dagger nematodes in various agricultural crops. The mode of action of flufensulfone involves interfering with the nervous systems of nematodes, leading to paralysis and death. By targeting nematodes, flufensulfone helps reduce their populations and minimize the damage they can cause to crops. Flufensulfone was priced at USD 19.0 thousand metric ton in 2022.

Abamectin is known for its nematocidal activity against several plant-parasitic nematodes, including the root lesion nematode (Pratylenchus penetrans), the reniform nematode (Rotylenchus reniformis), the root-knot nematode (Meloidogyne incognita), and the cyst nematodes (Heterodera schachtii). Its efficacy in controlling these nematodes makes it a valuable tool for nematode management in agricultural crops. As of 2022, the market value of abamectin was approximately USD 12.2 thousand per metric ton.

Oxamyl is a widely used insecticide and nematicide belonging to the chemical class of carbamates. It is primarily used to control a variety of plant-parasitic nematodes in agricultural crops. Oxamyl's mode of action as an insecticide and nematicide involves inhibiting the activity of acetylcholinesterase, an enzyme essential for nerve function in insects and nematodes. By disrupting this enzyme, oxamyl causes nerve overstimulation, leading to paralysis and eventual death of the pests. It was priced at USD 8.8 thousand per metric ton in 2022.

Nematicide Industry Overview

The Nematicide Market is fairly consolidated, with the top five companies occupying 85.65%. The major players in this market are ADAMA Agricultural Solutions Ltd., Bayer AG, Corteva Agriscience, Syngenta Group and Upl Limited (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Consumption Of Pesticide Per Hectare

4.2 Pricing Analysis For Active Ingredients

4.3 Regulatory Framework

4.3.1 Australia

4.3.2 Canada

4.3.3 China

4.3.4 France

4.3.5 Germany

4.3.6 India

4.3.7 Indonesia

4.3.8 Italy

4.3.9 Japan

4.3.10 Mexico

4.3.11 Myanmar

4.3.12 Netherlands

4.3.13 Pakistan

4.3.14 Philippines

4.3.15 Russia

4.3.16 South Africa

4.3.17 Spain

4.3.18 Thailand

4.3.19 Ukraine

4.3.20 United Kingdom

4.3.21 United States

4.3.22 Vietnam

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

5.1 Application Mode

5.1.1 Chemigation

5.1.2 Foliar

5.1.3 Fumigation

5.1.4 Seed Treatment

5.1.5 Soil Treatment

5.2 Crop Type

5.2.1 Commercial Crops

5.2.2 Fruits & Vegetables

5.2.3 Grains & Cereals

5.2.4 Pulses & Oilseeds

5.2.5 Turf & Ornamental

5.3 Region

5.3.1 Africa

5.3.1.1 By Country

5.3.1.1.1 South Africa

5.3.1.1.2 Rest of Africa

5.3.2 Asia-Pacific

5.3.2.1 By Country

5.3.2.1.1 Australia

5.3.2.1.2 China

5.3.2.1.3 India

5.3.2.1.4 Indonesia

5.3.2.1.5 Japan

5.3.2.1.6 Myanmar

5.3.2.1.7 Pakistan

5.3.2.1.8 Philippines

5.3.2.1.9 Thailand

5.3.2.1.10 Vietnam

5.3.2.1.11 Rest of Asia-Pacific

5.3.3 Europe

5.3.3.1 By Country

5.3.3.1.1 France

5.3.3.1.2 Germany

5.3.3.1.3 Italy

5.3.3.1.4 Netherlands

5.3.3.1.5 Russia

5.3.3.1.6 Spain

5.3.3.1.7 Ukraine

5.3.3.1.8 United Kingdom

5.3.3.1.9 Rest of Europe

5.3.4 North America

5.3.4.1 By Country

5.3.4.1.1 Canada

5.3.4.1.2 Mexico

5.3.4.1.3 United States

5.3.4.1.4 Rest of North America

5.3.5 South America

5.3.5.1 By Country

5.3.5.1.1 Argentina

5.3.5.1.2 Brazil

5.3.5.1.3 Chile

5.3.5.1.4 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

6.4.1 ADAMA Agricultural Solutions Ltd.

6.4.2 Albaugh LLC

6.4.3 American Vanguard Corporation

6.4.4 Bayer AG

6.4.5 Corteva Agriscience

6.4.6 Syngenta Group

6.4.7 Tessenderlo Kerley Inc. (Novasource)

6.4.8 Upl Limited

6.4.9 Vive Crop Protection

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS