North America Nematicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1683206

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

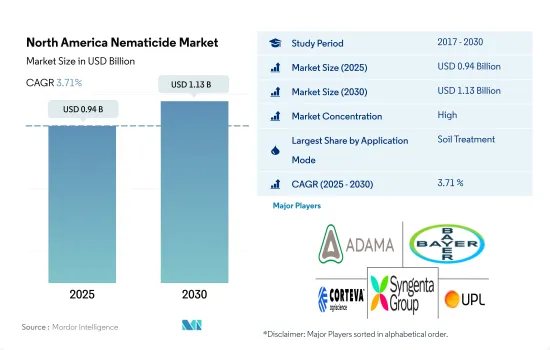

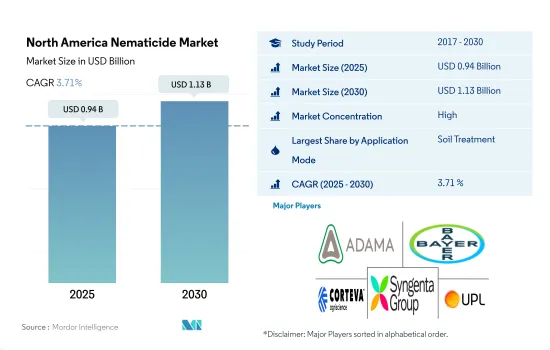

북미의 살선충제 시장 규모는 2025년에 9억 4,000만 달러로 추정되고, 2030년에는 11억 3,000만 달러에 이를 전망이며, 예측 기간 중 2025년부터 2030년까지 CAGR 3.71%로 성장할 것으로 예측됩니다.

토양 용도가 살선충제 시장을 독점

북미에서는 경제적으로 중요한 폭넓은 작물을 공격하는 다양한 유형의 선충이 존재하기 때문에 살선충제 수요가 증가하고 있습니다. 식물 기생성 선충은 단독으로 피해를 초래할 뿐만 아니라 다른 미생물과 병해 복합체를 형성하여 작물의 손실을 증대시키고 있습니다. 선충에 의한 연간 작물 손실은 미국에서 80억 달러로 추정됩니다. 살선충제는 해충 유형과 작물의 성장 단계에 따라 다양한 방법으로 살포할 수 있습니다.

엽면 살포(선충제를 식물의 잎에 직접 살포)와 같은 다른 살포 방법과 비교할 때, 선충의 토양 살포는 일반적으로 유익한 곤충 및 수분 매개체를 비롯한 비표적 유기체에 노출될 위험이 적습니다. 이 때문에 토양 시용이 70.7%의 점유율을 차지했으며, 2022년 시장 규모는 5억 9,870만 달러에 달했습니다.

엽면 살포는 2022년 북미 선충 시장의 10.9%를 차지했습니다. 잎 표면 살포의 주요 목적은 선충에 의한 화서와 잎의 침입을 제어하는 것입니다. 예를 들어, 국선 선충은 백미 수선병을 일으키는 엽면 선충이며, 사마크 림프 선충은 곡류의 춘계 위황병의 원인이 됩니다.

선충의 만연에 의한 작물의 손실은 해마다 증가하고 있으며, 농업 종사자에게 큰 우려가 되어 살선충제의 사용을 강요하고 있습니다. 따라서 이 시장은 예측 기간 동안 CAGR 3.2%를 나타낼 것으로 예측됩니다.

북미의 농업 종사자들은 작물의 건강과 수율을 극대화하기 위해 선충 관리에 중점을 두고 있으며, 이는 시장을 견인합니다.

북미에는 다양한 농업 부문이 있습니다. 선충은 곡물, 과일, 야채, 특수 작물과 같은 주요 작물을 포함한 광범위한 작물에 영향을 줄 수 있습니다. 그 결과, 선충의 개체수를 방제하고, 작물의 손실을 경감하기 위한 살선충제 수요가 높아지고 있습니다. 2022년 이 지역은 세계 살선충제 시장의 30.7% 시장 점유율을 차지했습니다.

미국은 살선충제의 주요 소비국입니다. 선충은 작물에 큰 피해를 주고 수확량의 손실과 경제적 영향을 미칩니다. 농업 종사자는 작물의 건강 상태를 최적으로 유지하고 수확량을 극대화하기 위해 선충 관리의 중요성을 인식하고 있습니다. 그 결과, 미국에서는 살선충제 수요가 왕성하고, 북미 시장에서의 주요 점유율에 공헌하고 있습니다.

멕시코의 살선충제 시장은 빠르게 성장하고 있습니다. 2023년부터 2029년까지 CAGR은 5.2%로 예측되고 있습니다. 멕시코는 이 지역의 주요 농산물 수출국 중 하나입니다. 멕시코는 국제 시장의 엄격한 품질 기준과 요구 사항을 충족하기 위해 농작물의 선충 개체 수를 효과적으로 관리해야 할 필요성이 커지고 있습니다. 멕시코산 농산물의 수출 수요 증가가 이 나라 살선충제 시장의 성장을 견인하고 있으며, 북미에서 가장 급성장하고 있는 시장의 하나가 되고 있습니다.

농업 종사자의 의식 고조, 농업 기술의 진보, 농업의 확대 등의 요인이 살선충제 시장의 성장에 기여하고 있습니다. 따라서 북미의 살선충제 시장은 예측기간 중 2023년부터 2029년까지 CAGR 3.9%를 나타낼 것으로 예측되고 있습니다.

북미의 살선충제 시장 동향

단작농과 불경기 재배는 선충 밀도를 증식시켜, 1헥타르당 살선충제 소비량 증가

최근 북미에서는 헥타르당 살선충제 소비량이 현저하게 증가하고 있습니다. 2022년에는 이 소비량이 2017년 기록된 수준에 비해 헥타르당 4g으로 크게 증가했습니다. 이 증가 추세의 주요 원동력은 선충을 치료하기 위해 살선충제에 대한 의존도가 증가하고 있다는 것입니다.

2022년에는 미국이 살선충제의 상당한 소비량으로 두드러졌으며, 헥타르당 82.9g에 달했고, 기타 국가를 크게 웃돌았습니다. 이 현저한 증가는 주로 선충의 개체수의 증식을 촉진하는 다양한 요인에 의해 살선충제 수요가 높아져 사용량이 증가한 것에 기인한다고 생각됩니다. 이 증가 경향의 요인 중 하나는 토양 교란을 줄이고 작물 잔여물의 유지를 높이는 불경기 재배의 채용입니다. 그러나 불경기 재배는 토양의 선충 수를 증가시키고 있습니다.

특히 밀(68%), 옥수수(76%), 면화(43%), 콩(74%) 등 주요 작물에서는 불경기 농법이 상당히 채용되어 살선충제의 필요성이 더욱 높아지고 있습니다. 이 나라의 열대 및 아열대 지역에서는 주로 단작농법이 채용되고 있으며, 이들 지역에서는 온난하고 습도가 높기 때문에 선충의 생육에 적합한 환경이 되고 있습니다. 따라서 헥타르당 살선충제 사용량이 증가하고 있습니다.

캐나다, 멕시코 및 기타 북미에서는 헥타르당 살선충제 사용량에 거의 변화가 없습니다. 기후 변화, 토양 조건 및 기타 농업 관행은 선충 증가의 이유이며, 헥타르당 살선충제 소비량을 더욱 증가시키고 있습니다.

플루엔술폰은 수요가 높기 때문에 다른 살선충제 중에서 가장 높은 가격이 되고 있습니다.

선충은 농작물에 큰 피해를 주고 수율 감소와 경제적 영향을 미칩니다. 농업 종사자는 작물의 건강 상태를 최적으로 유지하고 수확량을 극대화하기 위해 선충 관리의 중요성을 인식하고 있습니다. 미국은 이 지역에서 살선충제의 주요 소비국입니다.

플루엔술폰은 플루오로알킬계 화학물질로 분류되며, 식물 기생성 선충을 방제하기 위해 농업에서 사용됩니다. 플루엔술폰의 작용기전은 선충과 곤충의 신경계를 파괴하고 마비시켜 결국 죽음에 이르게 한다는 것입니다. 야채, 과일, 관상용 식물 등 다양한 작물에 사용되며, 이러한 해충에 의한 피해를 경감함으로써 작물의 수율과 품질을 향상시키고 있습니다. 플루엔술폰의 2022년 가격은 톤당 1만 9,100달러였습니다.

아바멕틴은 종자 처리에 이용되는 침투성 살선충제로, 뿌리 벌레 선충의 방제를 포함하여 선충에 의한 초기 성장기의 뿌리 감염을 최소화하는 효율적인 해결책을 기재하고 있습니다. 아바멕틴의 유효 성분 비용은 상승 경향이 있으며, 2022년에는 톤당 12.3달러에 달할 전망입니다.

옥사밀은 카르바마트계 살충 및 살선충제로, 다양한 선충의 구제에 자주 사용됩니다. 옥사밀은 야채, 과일, 관상용 식물 등의 작물에 살포되어 저작 및 흡입 곤충이나 식물의 뿌리를 공격하는 선충에 의한 피해로부터 작물을 지킵니다. 옥사밀은 이러한 해충의 신경계를 혼란시키고 마비시키고 궁극적으로 죽음에 이르게 함으로써 효과를 발휘합니다. 과립과 농축액 등 다양한 제제가 있으며, 대상이 되는 해충이나 작물에 따라 토양이나 잎에 살포됩니다. 옥사밀은 2022년 1톤당 8,600달러로 평가되었습니다.

북미의 살선충제 산업 개요

북미의 살선충제 시장은 상당히 통합되어 있으며 상위 5개사에서 89.63%를 차지하고 있습니다. 이 시장의 주요 기업은 ADAMA Agricultural Solutions Ltd, Bayer AG, Corteva Agriscience, Syngenta Group, Upl Limited입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

조사 전제조건 및 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

1헥타르당 농약 소비량

유효성분의 가격 분석

규제 프레임워크

캐나다

멕시코

미국

밸류체인 및 유통채널 분석

제5장 시장 세분화(시장 규모(단위 : 달러, 수량), 예측, 성장 전망 분석 포함)(-2030년)

용도 모드별

화학 관개

잎면 살포

훈증

종자 처리

토양 처리

작물 유형별

상업 작물

과일 및 야채

곡물

콩류 및 지방종자

잔디 및 관상용

국가별

캐나다

멕시코

미국

기타 북미

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

ADAMA Agricultural Solutions Ltd

Albaugh LLC

American Vanguard Corporation

Bayer AG

Corteva Agriscience

Syngenta Group

Tessenderlo Kerley Inc.(Novasource)

Upl Limited

Vive Crop Protection

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

AJY

영문 목차

영문목차

The North America Nematicide Market size is estimated at 0.94 billion USD in 2025, and is expected to reach 1.13 billion USD by 2030, growing at a CAGR of 3.71% during the forecast period (2025-2030).

Soil application dominated the nematicide market

The demand for nematicides has been increasing due to the presence of various nematode species attacking the wide range of economically important crops in North America. Plant parasitic nematodes cause damage individually and form disease complexes with other microorganisms, thereby increasing crop loss. Annual crop losses due to nematodes are estimated at USD 8.0 billion in the United States. Nematicides can be applied through different methods depending on the type of pest and growth stage of the crop.

Compared to other application methods, such as foliar application (spraying the nematicide directly onto the plant leaves), soil application of nematodes generally poses fewer risks of exposing non-target organisms, including beneficial insects and pollinators, as the nematicide remains primarily in the soil, where the target nematodes reside. Owing to this, soil application dominated the market with a share of 70.7%, valued at USD 598.7 million in 2022.

Foliar applications accounted for 10.9% of the North American nematicide market in 2022. The main purpose of foliar application is to control the infestation of inflorescence and leaves by the nematodes. For instance, chrysanthemum nematodes are foliar nematodes that cause white rice tip, and summer crimp nematodes cause spring dwarf diseases in cereal crops.

The crop losses due to nematode infestation are increasing every year, acting as a major concern for farmers and forcing them to use nematicides. Therefore, the market is anticipated to register a CAGR of 3.2% during the forecast period.

North American farmers' emphasis on nematode management for optimal crop health and yield maximization will drive the market

North America has a diverse agricultural sector. Nematodes can impact a wide range of crops, including major commodities like grains, fruits, vegetables, and specialty crops. As a result, there is a growing demand for nematicides to control nematode populations and mitigate crop losses. In 2022, the region accounted for 30.7% market share value of the global nematicide market.

The United States is a major consumer of nematicide products. Nematodes can cause substantial damage to crops, leading to yield losses and economic impact. The farmers recognize the importance of nematode management to ensure optimal crop health and maximize yields. As a result, there is a strong demand for nematicide products in the United States, contributing to its major share in the North American market.

Mexico is experiencing rapid growth in its nematicide market. It is anticipated to register a CAGR of 5.2% during 2023-2029. Mexico is one of the leading exporters of agricultural products in the region. As Mexico aims to meet the stringent quality standards and requirements of international markets, there is an increasing need to effectively manage nematode populations in crops. The rising export demand for Mexican agricultural products is driving the growth of the nematicide market in the country, making it one of the fastest-growing markets in North America.

Factors such as increasing awareness among farmers, advancements in agricultural technologies, and expansion of agriculture contribute to the growth of the nematicide market. Therefore, the North American nematicide market is expected to register a CAGR of 3.9% during the forecast period (2023-2029).

North America Nematicide Market Trends

Monoculture and no-tillage practices proliferate the nematode density, resulting in increased consumption of nematicides per ha

In recent years, there has been a notable growth in the consumption of nematicide per hectare in North America. In 2022, this consumption witnessed a considerable increase of 4 g per ha compared to the levels recorded in 2017. The primary driving force behind this upward trend is the growing dependency on nematicides to control nematodes.

In 2022, the United States stood out with a substantial consumption of nematicide, reaching 82.9 g per ha, which was significantly higher than other countries. This notable increase can be primarily attributed to various factors promoting the proliferation of nematode populations, leading to a higher demand for nematicides and increased usage levels. One of the contributing factors to this upward trend is the adoption of no-tillage practices, which reduce soil disturbance and increase the retention of crop residue. However, this practice also inadvertently results in a higher nematode population in the soil.

Notably, major crops like wheat (68%), corn (76%), cotton (43%), and soybeans (74%) have recorded considerable adoption of no-tillage methods, further intensifying the need for nematicides. The country's tropical and subtropical regions predominantly adopt monoculture agricultural practices, and the warm and humid conditions in these areas create favorable environments for nematode growth. Therefore, the utilization of nematicides per ha is growing.

There is a minimal change in the consumption of nematicides per ha in Canada, Mexico, and the Rest of North America. Climate changes, soil conditions, and other agricultural practices are reasons for nematodes' growth, further increasing the consumption of nematicides per ha.

Fluensulfone was priced highest among other nematicides due to the high demand

Nematodes can cause substantial damage to crops, leading to yield losses and economic impact. The farmers recognize the importance of nematode management to ensure optimal crop health and maximize yields. The United States is a major consumer of nematicide products in the region.

Fluensulfone falls under the fluoroalkyl chemical class and is used in agriculture to control plant-parasitic nematodes. Fluensulfone's mode of action involves disrupting the nervous systems of nematodes and insects, leading to their paralysis and eventual death. It is used in a variety of crops, including vegetables, fruits, and ornamental plants, to enhance crop yield and quality by reducing the damage caused by these pests. Fluensulfone was priced at USD 19.1 thousand per metric ton in 2022.

Abamectin is a systemic nematicide utilized for seed treatment, providing an efficient solution to minimize early-growth root infections caused by nematodes, including controlling root-knot nematode species. The cost of abamectin's active ingredient has been on the rise, reaching USD 12.3 per metric ton in 2022.

Oxamyl is a carbamate insecticide and nematicide that is commonly used to control a variety of nematodes. It is applied to crops like vegetables, fruits, and ornamental plants to protect them from damage caused by chewing and sucking insects, as well as nematodes that attack the plant roots. Oxamyl works by disrupting the nervous system of these pests, leading to paralysis and eventual death. It is available in various formulations, including granules and liquid concentrates, and is applied to the soil or foliage depending on the target pests and crops. Oxamyl was valued at USD 8.6 thousand per metric ton in 2022.

North America Nematicide Industry Overview

The North America Nematicide Market is fairly consolidated, with the top five companies occupying 89.63%. The major players in this market are ADAMA Agricultural Solutions Ltd, Bayer AG, Corteva Agriscience, Syngenta Group and Upl Limited (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Consumption Of Pesticide Per Hectare

4.2 Pricing Analysis For Active Ingredients

4.3 Regulatory Framework

4.3.1 Canada

4.3.2 Mexico

4.3.3 United States

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

5.1 Application Mode

5.1.1 Chemigation

5.1.2 Foliar

5.1.3 Fumigation

5.1.4 Seed Treatment

5.1.5 Soil Treatment

5.2 Crop Type

5.2.1 Commercial Crops

5.2.2 Fruits & Vegetables

5.2.3 Grains & Cereals

5.2.4 Pulses & Oilseeds

5.2.5 Turf & Ornamental

5.3 Country

5.3.1 Canada

5.3.2 Mexico

5.3.3 United States

5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

6.4.1 ADAMA Agricultural Solutions Ltd

6.4.2 Albaugh LLC

6.4.3 American Vanguard Corporation

6.4.4 Bayer AG

6.4.5 Corteva Agriscience

6.4.6 Syngenta Group

6.4.7 Tessenderlo Kerley Inc. (Novasource)

6.4.8 Upl Limited

6.4.9 Vive Crop Protection

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS