해양지원선 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Offshore Support Vessels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1640663

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

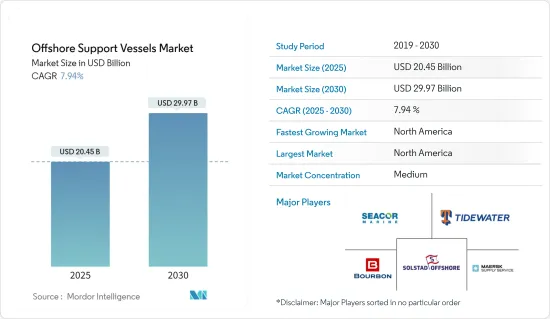

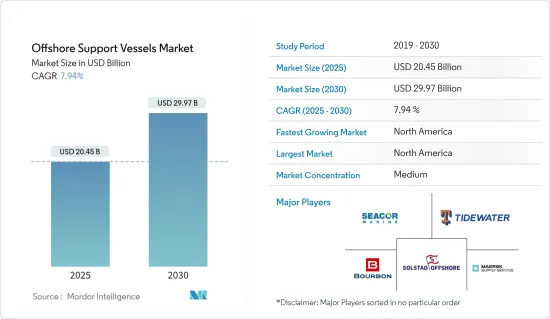

해양지원선 시장 규모는 2025년에 204억 5,000만 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 7.94%로 전망되며, 2030년에는 299억 7,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 투자 확대, 석유 및 가스의 해양 탐사 및 생산 활동, 해상 풍력 발전 설비 증가가 시장 수요를 견인할 것으로 예상됩니다.

한편, 채굴되는 상품의 가격 변동이 시장 성장을 억제할 것으로 예상됩니다.

해양 선박의 환경 문제를 해결하는 데 도움이 되는 새로운 기술은 시장에 많은 기회를 제공합니다. 예를 들어, Maersk Supply Service는 비이동선으로부터의 배출을 제거함으로써 해운산업에서 이산화탄소 배출량을 줄이기 위해 스틸스트렘 해양선박 충전 사업을 시작했습니다. 장기적으로는 화석 연료선을 꾸준히 폐지해 나갈 것으로 예상됩니다.

북미는 이 지역에서 최근 일어난 대규모 해양석유 및 가스의 발견에 의해 예측기간 중에 시장을 독점할 것으로 예측되고 있습니다.

해양지원선 시장 동향

PSV(플랫폼 공급선)가 시장을 독점할 전망

PSV(Platform Supply Vessels)는 해양 드릴링 장비와 생산 플랫폼에 장비, 소모품 및 드릴링 소모품을 공급하는 데 필수적입니다. 이러한 소모품에는 시멘트, 중정석, 벤토나이트 등의 건조 분말, 드릴수, 오일 또는 물 기반 액체 진흙, 메탄올, 특수 화학물질 등이 포함됩니다.

PSV는 육상 기지에서의 적재에서 작업을 시작합니다. 이중 바닥 탱크에서 액체화물을, 전용 공압 탱크로 드라이버 루크화물을 수송하고 선미의 오픈 데크로 장비와 드릴 파이프를 운반합니다. 리그와 플랫폼에 도착하면 리그 크레인이 갑판화물을 관리하는 동안 액체화물과 분말화물이 공압으로 압송되거나 운반됩니다.

많은 국가에서 세계 수준의 석유 및 가스 수요가 증가함에 따라 생산자는 심해에서 석유 및 가스 개발을 포함하여 더 많은 석유 자원을 탐험할 수 있습니다. 미국에서는 멕시코만(GoM) 연방 해양 지역의 원유 생산량이 2023년에는 일량 약 186만 5,000배럴에 이릅니다. 이러한 동향은 해양 석유 생산과 관련 서비스에 대한 수요를 보여줍니다.

플랫폼 보급선(PSV)은 석유 및 가스, 신재생 에너지 부문에서 해외 물류 지원 수요 증가에 견인되어 세계적으로 큰 성장을 이루고 있습니다. PSV는 드릴링 장비, 연료, 물과 같은 물품을 해상 플랫폼으로 운송하도록 설계된 특수 선박입니다. 이 선박은 해양 시설의 지속적인 운영을 보장하고 지속 가능하고 효율적인 공급망에 대한 요구 증가를 지원하는 데 매우 중요합니다.

기업은 배출량을 줄이고 운영 효율성을 최적화하고 시장은 세계적으로 친환경 솔루션으로 전환하고 있습니다. 그 두드러진 예는 2024년 1월 Kongsberg Maritime에서 첨단 에너지 저장 시스템 4개 인수를 발표한 SEACOR Marine Holdings Inc.입니다. 이 노력은 하이브리드 전력 솔루션을 4척의 SEACOR PSV(SEACOR 오하이오, SEACOR 알프스, SEACOR 안데스, SEACOR 아틀라스)에 통합하는 것으로, 설치는 2024년 12월에 시작되어 2025년 중반까지 완료될 예정입니다. 이러한 업그레이드는 배출을 최소화하고 선내 에너지 효율을 높이는 산업의 목표에 부합합니다.

게다가 플릿 용량의 확장은 몇몇 기업들에게 전략적 초점이 되고 있습니다. 2023년 3월 미국에 본사를 둔 Tidewater는 Solstad Offshore에서 37척의 PSV를 5억 7,700만 달러에 인수하고, 회사의 플릿을 228척(PSV 199척과 앵커 핸들링 태그 공급(AHTS) 선박 포함)으로 대폭 강화했습니다. Tidewater의 플릿은 평균 선령 11.3년과 세계적으로 가장 젊은 플릿의 하나로 되어 있으며, 이 분야의 증대하는 운용 요구와 지속가능성 기준에 대응하기 위한 자리를 잡고 있습니다.

전반적으로 플랫폼 공급선 수요는 예측 기간 동안 상당한 성장이 예상됩니다.

북미가 시장을 독점할 전망

미국은 해양지원선(OSV) 시장에서 뛰어난 진출기업이며, 그 주요 이유는 확립된 석유 및 가스 산업과 성장하는 해양 신재생 에너지 프로젝트입니다.

멕시코만을 중심으로 해외활동이 활발한 미국의 OSV 시장은 전통적인 화석연료 탐사와 신흥의 청정에너지원을 지원하는 데 필수적인 존재로 남아 있습니다. 이 다양한 시장은 지속 가능한 대체 에너지로 점진적으로 전환하면서 에너지 안보를 유지하는 미국의 약속을 반영합니다.

멕시코 만은 여전히 중요한 해양 석유 및 가스 허브입니다. 예를 들어, 2024년 9월, Talos Energy는 미국 멕시코만의 광구에서 상업용 석유 및 천연 가스를 대량으로 발견했다고 발표했습니다.

이러한 활동에는 탐사, 시추 및 생산을 지원하는 OSV의 지속적인 수요가 필요합니다. OSV는 물자의 수송, 리그의 안정화, 해저 검사의 지원에 필수적이며, 지속적인 석유 및 가스 조업에 빠뜨릴 수 없는 존재가 되고 있습니다.

국내 여러 기업이 해외 활동을 위한 OSV의 지속적인 수요를 지원하고 있습니다. 예를 들어, 2024년 8월, DOF는 미국 멕시코만에서 해저 계약을 획득했습니다. 이 계약은 물 주입 흐름 라인, 선체 배관, 관련 해저 인프라의 엔지니어링, 조달, 건설 및 해상 설치를 포함합니다.

해상 풍력 발전 용량의 확대를 추진하는 정부의 움직임은 건설, 승무원 이동, 유지 보수를 위한 서비스 운영 선박(SOV) 및 기타 OSV와 같은 특수 선박에 대한 수요를 부추기고 있습니다.

예를 들어 Hornbeck Offshore Services는 2024년 7월 동부 조선 그룹과 계약을 맺고 280피트의 해양지원선(OSV)을 서비스 운영 선박(SOV)으로 개조하여 미국 해양 풍력 발전 시장에서 급증하는 수요에 대응했습니다.

이 나라에서는 해안에 수많은 풍력 발전소가 설치되어 해상 풍력 발전 용량이 확대되고 있습니다. 예를 들어, 2024년 9월, 이베르드로라의 미국 자회사인 Avangrid가 미국에서 791MW의 뉴잉글랜드 윈드 1 해상 풍력 발전소 개발 계약을 획득했습니다. 해안을 따라 새로운 풍력 발전소가 개발됨에 따라 OSV는 이러한 신재생 에너지 프로젝트를 지원하기 위해 점점 더 필요합니다.

예를 들어 덴마크의 Maersk Supply Service는 2024년 9월 폴란드 CRIST에 DP3급 배터리 하이브리드 추진 다목적 해양 지원선(OSV)을 주문했습니다. ABS 클래스 기준으로 건설되는 110m의 OSV는 화이트 로즈 유전용 프로젝트 '시드래곤' 아래 MMC Ship Design & Marine Consulting이 995L SBC 선형 설계도를 바탕으로 설계했습니다. 마스크는 이 배를 캐나다 동부 뉴펀들랜드 래브라도 해안에 위치한 화이트 로즈 유전에 장기 배치할 계획으로 유전 오퍼레이터인 Cenovus Energy에 공급합니다.

이상으로부터 예측기간 동안 북아프리카가 해양지원선 시장을 독점할 것으로 예상됩니다.

해양지원선 산업 개요

해양지원선 시장은 세분화되어 있습니다. 이 시장의 주요 기업(순부동)에는 Tidewater Inc., Bourbon Corporation SA, Seacor Marine Holdings Inc., Maersk Supply Service A/S, Solstad Offshore ASA 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

서문

시장 규모 및 수요 예측(단위 : 10억 달러)(-2029년)

최근 동향 및 개발

정부의 규제 및 시책

시장 역학

성장 촉진요인

해상 풍력 발전 설비 증가

석유 및 가스 개발에 대한 투자 확대

억제요인

원유 가격의 높은 변동성

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

투자분석

제5장 시장 세분화

선종별

앵커 핸들링 태그 및 앵커 핸들링 예선 공급선(AHT/AHTSs)

플랫폼 공급선(PSV)

기타

지역별

북미

미국

캐나다

기타 북미

유럽

영국

프랑스

러시아

노르웨이

이탈리아

독일

기타 유럽

아시아태평양

중국

인도

한국

ASEAN 국가

기타 아시아태평양

남미 국가

브라질

아르헨티나

기타 남미 국가

중동 및 아프리카

사우디아라비아

카타르

아랍에미리트(UAE)

나이지리아

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

주요 기업의 전략

기업 프로파일

Bourbon Corporation SA

Maersk Supply Service AS

Seacor Marine Holdings Inc.

Edison Chouest Offshore LLC

Swire Pacific Limited

Tidewater Inc.

Harvey Gulf International Marine LLC

Solstad Offshore ASA

Hornbeck Offshore Services Inc.

PACC Offshore Services Holdings Ltd.

제7장 시장 기회 및 향후 동향

해외 선박의 환경 문제 대응을 지원하는 신기술

AJY

영문 목차

영문목차

The Offshore Support Vessels Market size is estimated at USD 20.45 billion in 2025, and is expected to reach USD 29.97 billion by 2030, at a CAGR of 7.94% during the forecast period (2025-2030).

Key Highlights

Over the medium term, growing investments, offshore oil and gas exploration and production activities, and rising offshore wind energy installations are expected to drive the market demand.

On the other hand, the volatility in the prices of extracted commodities is expected to restrain the market growth.

Nevertheless, new technologies that help offshore vessels deal with environmental problems open up many opportunities for the market. For example, Maersk Supply Service has started its Stillstrom offshore vessel-charging business to reduce carbon emissions in the shipping industry by eliminating emissions from non-moving ships. In the long run, it will steadily phase out fossil-fuel-based vessels.

North America is predicted to dominate the market during the forecast period due to major offshore oil and gas discoveries that happened in the region recently.

Offshore Support Vessels Market Trends

Platform Supply Vessels (PSVs) Expected to Dominate the Market

PSVs (Platform Supply Vessels) are essential for delivering equipment, supplies, and drilling consumables to offshore drilling rigs and production platforms. These consumables include dry powders like cement, baryte, and bentonite, drill water, oil or water-based liquid mud, methanol, and specialized chemicals.

PSVs begin their operations by loading at a shore base. They transport liquid cargo in double-bottom tanks, dry bulk cargoes in specialized pneumatic pressure tanks, and carry equipment and drill pipes on the open deck aft. Upon reaching the rig or platform, liquid and powder cargoes are pumped or transferred pneumatically while the rig crane manages the deck cargo.

The increase in oil and gas demand at the global level in many countries has prompted producers to explore more petroleum sources, such as deepwater oil and gas exploitation. In the United States, crude oil production from the Gulf of Mexico (GoM) Federal Offshore region reached around 1865 thousand barrels per day in 2023. Such growing trends indicate the demand for offshore petroleum production and related services.

Platform Supply Vessels (PSV) has witnessed a significant growth globally, driven by the increasing demand for offshore logistics support in the oil, gas, and renewable energy sectors. PSVs are specialized vessels designed to transport supplies like drilling equipment, fuel, water, and other materials to offshore platforms. These vessels are critical in ensuring continuous operations for offshore installations and supporting the growing need for sustainable and efficient supply chains.

The market globally is moving towards greener solutions as companies aim to reduce emissions and optimize operational efficiency. A notable example is SEACOR Marine Holdings Inc. which, in January 2024, announced the acquisition of four advanced energy storage systems from Kongsberg Maritime. This initiative will integrate hybrid power solutions into four SEACOR PSVs-SEACOR Ohio, SEACOR Alps, SEACOR Andes, and SEACOR Atlas-with installation expected to start in December 2024 and complete by mid-2025. These upgrades align with industry goals to minimize emissions and enhance energy efficiency on board.

Additionally, expanding fleet capacities has been a strategic focus for some companies. In March 2023, US-based Tidewater acquired 37 PSVs from Solstad Offshore in a USD 577 million deal, significantly boosting its fleet to 228 vessels, which includes 199 PSVs and anchor handling tug supply (AHTS) vessels. Tidewater's fleet is considered one of the youngest globally, with an average age of 11.3 years, positioning it to meet the sector's growing operational needs and sustainability standards.

Overall, the demand for platform supply vessels is expected to witness significant growth during the forecast period.

North America Expected to Dominate the Market

The United States is a prominent player in the Offshore Support Vessels (OSVs) market, largely due to its well-established oil and gas industry and growing offshore renewable energy projects.

With significant offshore activities, particularly in the Gulf of Mexico, the United States OSV market remains essential for supporting traditional fossil fuel exploration and emerging clean energy sources. This diverse market reflects the United States' commitment to maintaining energy security while gradually shifting towards sustainable alternatives.

The Gulf of Mexico remains a significant offshore oil and gas hub. For instance, in September 2024, Talos Energy announced a significant discovery of commercial oil and natural gas quantities in a block in the United States Gulf of Mexico.

These activities require a continuous demand for OSVs to support exploration, drilling, and production. OSVs are critical in transporting supplies, stabilizing rigs, and assisting with subsea inspections, making them essential for ongoing oil and gas operations.

Several companies in the country supported the continuous demand for OSVs for offshore activities. For instance, in August 2024, DOF secured a subsea contract in the US Gulf of Mexico. The contract encompasses engineering, procurement, construction, and offshore installation of a water injection flowline, hull piping, and related subsea infrastructure.

The government's push to expand offshore wind capacity has fueled demand for specialized vessels like Service Operation Vessels (SOVs) and other OSVs for construction, crew transfers, and maintenance.

For instance, in July 2024, Hornbeck Offshore Services contracted Eastern Shipbuilding Group to transform a 280-foot offshore supply vessel (OSV) into a service operation vessel (SOV), addressing the surging demand in the United States offshore wind market.

The country is expanding its offshore wind capacity with numerous wind farms established along its coasts. For instance, in September 2024, Iberdrola's US subsidiary, Avangrid, secured a contract to develop the 791 MW New England Wind 1 offshore wind farm in the United States. As new wind farms are developed along the coasts, OSVs are increasingly needed to support these renewable energy projects.

For instance, in September 2024, Maersk Supply Service from Denmark ordered a DP3-class, battery-hybrid propulsion multipurpose offshore support vessel (OSV) with Poland's CRIST. The 110-meter OSV, set to be built to ABS class standards, is designed on the 995L SBC hull blueprint by MMC Ship Design & Marine Consulting under the project Sea Dragon for the White Rose oilfield. Maersk plans to deploy this vessel for long-term service at the White Rose oilfield, located offshore Newfoundland and Labrador in eastern Canada, catering to field operator Cenovus Energy.

Thus, owing to above points, North Amrica is expected to dominate the offshore support vessels market during the forecast period.

Offshore Support Vessels Industry Overview

The offshore support vessel market is semi-fragmented. Some of the major players in the market (in no particular order) include Tidewater Inc., Bourbon Corporation SA, Seacor Marine Holdings Inc., Maersk Supply Service A/S, and Solstad Offshore ASA.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Rising Offshore Wind Energy Installations

4.5.1.2 Growing Investments In Offshore Oil & Gas Exploration And Production