ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

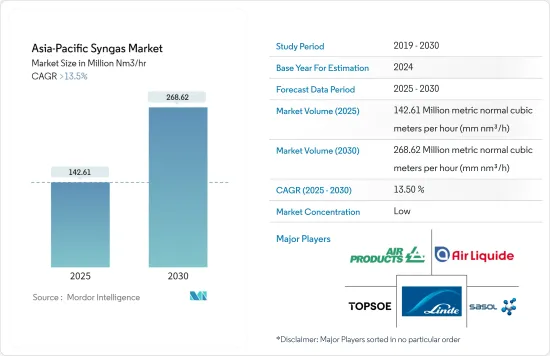

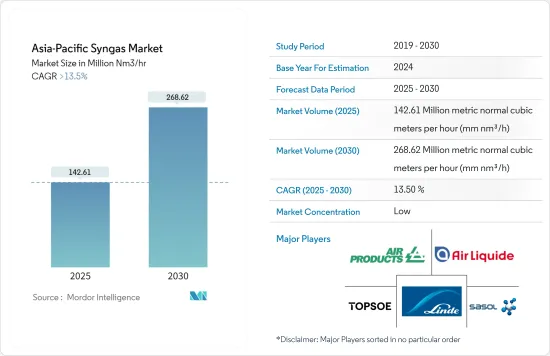

아시아태평양의 합성가스 시장 규모는 2025년에는 1억 4,261만mmnm3/h로 추정되고, 2030년에는 2억 6,862만mmnm3/h에 이를 것으로 예측되며, 예측기간 중(2025-2030년) 연평균 성장율(CAGR)은 13.5%로 전망됩니다.

주요 하이라이트

아시아태평양의 합성가스 시장은 COVID-19 팬데믹의 악영향을 받았습니다. 중국은 이 지역에서 코로나19 팬데믹으로 인해 가장 큰 타격을 받았습니다. 팬데믹으로 인해 인도와 중국과 같은 국가에서 화학 생산 공장이 폐쇄되면서 합성가스 시장에 영향을 미쳤습니다. 그러나 제한이 해제된 후 시장은 빠르게 회복되었습니다. 발전 및 화학 산업에서 합성가스 소비가 증가하면서 시장이 크게 회복되었습니다.

전력 및 화학 산업의 합성가스 수요 증가, 재생 연료 사용에 대한 환경 인식 및 정부 규제 강화, 비료용 수소 수요 증가가 시장 성장을 견인할 것으로 예상됩니다.

합성가스 생산 플랜트 설치에는 막대한 자본 투자와 자금이 필요하기 때문에 시장 성장을 저해할 것으로 예상됩니다.

지하 석탄 가스화 기술의 개발은 향후 기회가 될 것으로 예상됩니다.

발전 및 화학 산업에서 합성가스 수요가 증가함에 따라 중국이 시장을 장악할 것으로 예상됩니다. 또한 예측 기간 동안 가장 높은 CAGR을 기록 할 것으로 예상됩니다.

아시아태평양의 합성가스 시장 동향

시장을 독점하는 암모니아 응용 분야

합성 가스는 암모니아와 비료의 산업적 합성의 부산물입니다. 이 과정에서 메탄(천연 가스에서 추출)은 물과 반응하여 일산화탄소를 생성하고 수소(천연 가스에서 추출)는 물과 반응하여 일산화탄소와 수소를 생성합니다. 가스화 공정은 탄소 함유 물질을 더 긴 탄화수소 사슬로 변환하는 데 사용됩니다.

하버보쉬 공정을 통해 합성 가스는 비료의 표준 성분인 암모니아로 전환될 수 있습니다. 이 과정에서 공기 중의 질소가 합성 가스의 수소와 혼합되어 암모니아가 만들어지고, 이 암모니아는 다양한 종류의 비료를 만드는 데 사용될 수 있습니다.

비료를 만들기 위한 원료로 합성 가스를 사용하면 여러 가지 장점이 있습니다. 예를 들어, 합성가스는 다양한 원료로 만들 수 있으므로 기업에게 더 많은 옵션을 제공하고 단일 원료에 대한 의존도를 낮출 수 있습니다. 또한 바이오매스를 가스화하여 합성가스를 만들면 화석 연료로 비료를 만드는 것보다 온실가스 배출량을 줄일 수 있습니다.

중국은 전 세계 농업 면적의 약 7%를 차지하며, 전 세계 인구의 22%를 먹여 살리고 있습니다. 중국은 쌀, 면화, 감자 등 다양한 농작물의 최대 생산국입니다. 따라서 대규모 농업 활동으로 인해 비료로 사용되는 암모니아에 대한 수요가 빠르게 증가하고 있습니다.

중국은 세계에서 가장 큰 암모니아 생산국이자 소비국입니다. 미국 지질조사국(USGS)에 따르면 중국은 2022년에 4,200만 톤의 암모니아를 생산할 것으로 예상됩니다. 중국의 암모니아 수요는 비료, 섬유, 제약 및 광업과 같은 농업 산업에서의 응용 분야 증가로 인해 증가하고 있습니다.

마찬가지로 인도에서도 농업, 섬유, 화학 산업에서 암모니아에 대한 수요가 증가하고 있습니다. 따라서 다양한 기업들이 인도에서 암모니아 생산 능력을 늘리고 있습니다. 예를 들어, 2023년 5월, 디팍 비료 및 석유화학 회사(DFPC)는 5억 2,250만 달러 규모의 신규 암모니아 공장을 시운전하고 올해 하반기부터 생산을 시작한다고 발표했습니다. 이 회사는 마하라슈트라 주 탈로자에 연간 5,00,000만 톤(MTPA)의 생산 능력을 추가하여 총 암모니아 생산 능력을 6,28,700 MTPA로 늘릴 계획입니다.

따라서 암모니아에 대한 수요 증가는 예측 기간 동안이 지역의 합성 가스 수요를 주도 할 것으로 예상됩니다.

아시아태평양시장을 독점하는 중국

아시아태평양에서는 중국이 GDP에서 가장 큰 경제 강국입니다. 중국은 가장 빠르게 성장하는 경제국 중 하나이며 오늘날 세계 최대 생산국 중 하나입니다. 이 나라의 제조 부문은 이 나라의 경제에 크게 기여하고 있습니다.

중국에서는 발전, 화학 및 비료, 액체 연료 및 기체 연료 응용 분야에서 합성 가스에 대한 수요가 증가하고 있습니다. 이에 따라 다양한 기업들이 중국 내 합성가스 생산 능력을 늘리며 시장을 주도하고 있습니다.

중국에서는 Air Products가 중국 후허하오터에 위치한 Jiutai New Material의 고가치 모노에틸렌 글리콜 프로젝트에 합성 가스를 공급하는 장기 현장 계약을 획득했습니다. 이 시설은 매시 50만 Nm3 이상의 합성가스를 생산하도록 설계되어 있으며, 5기의 가스화로, 합성가스의 정제 및 처리를 실시하는 매시 약 10만 Nm3의 공기분리장치(ASU) 2기, 관련 인프라와 유틸리티으로 구성되어 있습니다.

중국은 비료, 특히 암모니아 기반 비료의 주요 생산국이자 수출국입니다. 중국에는 비료 제조를 전문으로 하는 여러 주요 화학 기업이 있으며, 암모니아 기반 비료는 국내 및 국제적으로 수요가 높습니다.

화학 산업에서 합성 가스는 화학 물질과 연료를 만드는 데 사용됩니다. 합성가스를 만들기 위해 석탄, 석유 코크스, 바이오매스를 가스로 전환합니다. 화학 사업에서 합성 가스는 메탄올, 암모니아, 수소를 만드는 데 사용됩니다. “가스-액체"(GTL) 공정을 통해 일산화탄소와 수소가 반응하여 합성가스를 메탄올로 전환합니다. 메탄올은 포름알데히드, 아세트산 등을 만드는 데 사용할 수 있습니다.

합성 가스는 연료이자 원료입니다. 화학 공장의 보일러와 열교환기를 가열하거나 기타 고온 산업용으로 사용할 수 있습니다. 바스프 화학 전망 보고서에 따르면 2022년 중국의 화학 생산 능력은 전년도 성장률인 6.6%에 비해 7.7% 증가할 것으로 예상됩니다. 따라서 화학 산업의 성장은 중국 내 합성 가스 수요를 견인할 것으로 예상됩니다.

중국의 발전량 증가는 합성가스 수요를 증가시키고 있습니다. 중국전력위원회(CEC)에 따르면 2022년 중국의 발전 용량은 2559.4기가와트로 전년도 2376.1기가와트의 발전 용량에 비해 증가했습니다. 따라서 발전 용량의 증가는 국가의 성가 수요를 주도 할 것으로 예상됩니다.

이와 같이 화학, 비료, 발전산업의 성장이 이 나라의 합성가스 시장을 견인할 것으로 예상됩니다.

아시아태평양의 합성 가스 산업 개요

아시아태평양의 합성 가스 시장은 그 특성상 단편적입니다. 이 시장의 주요 기업에는 Air Products and Chemicals, Inc., Air Liquide, Haldor Topsoe A/S, Linde plc, Sasol 등이 포함됩니다(특정한 순서 없음).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

합성가스 생산에 있어서의 원료의 유연성

전력 및 화학 산업에서 수요 증가

비료용 수소 수요 증가

억제요인

고액의 설비투자와 자금조달

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 진입업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(수량 기준 시장 규모)

원료

석탄

천연가스

석유

반려동물 코크스

바이오매스

기술

수증기 개질

부분 산화

자동 열 개질

복합 또는 2단계 개질

바이오매스 가스화

가스화로 유형

고정층

엔트레인 플로우

유동층

용도

발전

화학

메탄올

암모니아

옥소화학

n-부탄올

수소

디메틸에테르

액체 연료

가스 연료

지역

중국

인도

일본

한국

호주 및 뉴질랜드

기타 아시아태평양

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율, 랭킹 분석

주요 기업의 전략

기업 프로파일

Air Products and Chemicals, Inc.

Air Liquide

BASF SE

BP plc

DuPont

General Electric

Haldor Topsoe A/S

KBR Inc

Linde plc

Royal Dutch Shell plc

Sasol

Siemens

SynGas Technology LLC

TechnipFMC plc

제7장 시장 기회와 앞으로의 동향

바이오매스와 도시폐기물의 이용

지하석탄가스화기술 개발

HBR

영문 목차

영문목차

The Asia-Pacific Syngas Market size is estimated at 142.61 million metric normal cubic meters per hour (mm nm3/h) in 2025, and is expected to reach 268.62 million metric normal cubic meters per hour (mm nm3/h) by 2030, at a CAGR of greater than 13.5% during the forecast period (2025-2030).

Key Highlights

The Asia-Pacific Sngas market was negatively affected by the COVID-19 pandemic. China was worst hit by the COVID pandemic in the region. The pandemic resulted in the closure of chemical production plants in countries like India and China, thereby affecting the market for syngas. However, the market recovered well after the restrictions were lifted. The market recovered significantly, owing to the rise in consumption of syngas in power generation and chemical industries.

The growing demand for syngas from the electricity and chemical industry, increasing environmental awareness and government regulations on renewable fuel use, and increasing hydrogen demand for fertilizers are expected to drive the growth of the market.

The syngas production plant setup requires high capital investment and funding, which is expected to hinder market growth.

The development of underground coal gasification technology is likely to act as an opportunity in the future.

China is expected to dominate the market due to the rising demand for syngas in the power generation and chemical industries. It is also expected to register the highest CAGR during the forecast period.

Asia Pacific Syngas Market Trends

Ammonia Application Segment to Dominate the Market

Syngas is a byproduct of the industrial synthesis of ammonia and fertilizer. Throughout this process, methane (from natural gas) reacts with water to produce carbon monoxide, and hydrogen (from natural gas) reacts with water to produce carbon monoxide and hydrogen. The gasification process is used to transform any carbon-containing substance into longer hydrocarbon chains.

Through the Haber-Bosch process, syngas can be turned into ammonia, which is a standard part of fertilizers. During this process, nitrogen from the air is mixed with hydrogen from the syngas to make ammonia, which can then be used to make different kinds of fertilizers.

Using syngas as a source of raw materials to make fertilizer has a number of advantages. For example, syngas can be made from a number of different materials, which gives companies more options and makes them less reliant on a single raw material. Also, making syngas from biomass by gasifying it can help cut down on greenhouse gas emissions compared to making fertilizer from fossil fuels.

China accounts for approximately 7% of the overall agricultural acreage globally, thus feeding 22% of the world's population. The country is the largest producer of various crops, including rice, cotton, potatoes, and others. Hence, the demand for ammonia, which is used as a fertilizer, is rapidly increasing owing to the large-scale agricultural activities in the country.

China is the largest producer and consumer of ammonia in the world. According to the US Geological Survey (USGS), the country produced 42 million metric tons in 2022. The demand for ammonia in the country is rising due to increasing applications in the agriculture industry, such as fertilizers, textiles, pharmaceuticals, and mining.

Similarly, in India, the demand for ammonia is increasing in the agriculture, textile, and chemical industries. Thus, various companies are increasing their ammonia production capacity in the country. For instance, in May 2023, Deepak Fertilisers and Petrochemicals Corporation (DFPC) announced that it would be commissioning a new USD 522.5 Million ammonia plant and start production by the start of the second half of this year. The company is adding a capacity of 5,00,000 million tonnes per annum (MTPA) at Taloja in Maharashtra, which would take the total ammonia capacity to 6,28,700 MTPA.

Thus, the increasing demand for ammonia is expected to drive the demand for syngas in the region during the forecast period.

China to Dominate the Asia-Pacific Market

In the Asia-Pacific region, China is the largest economy in terms of GDP. China is one of the fastest emerging economies and has become one of the biggest production houses in the world today. The country's manufacturing sector is one of the significant contributors to the country's economy.

In China, the demand for syngas is increasing from power generation, chemicals and fertilizers, liquid fuels, and gaseous fuel applications. Thus, various companies are increasing the production capacity of syngas in the country, thereby driving the market.

In China, Air Products was awarded a long-term onsite contract to supply syngas to Jiutai New Material Co. Ltd for its high-value mono-ethylene glycol project in Hohhot, China. The facility is designed to produce over 500,000 Nm3/hr of syngas, comprised of five gasifiers, two approximately 100,000 Nm3/hr air separation units (ASU) with syngas purification and processing, and associated infrastructure and utilities.

China is a significant producer and exporter of fertilizers, particularly ammonia-based fertilizers. The country is home to several significant chemical businesses that specialize in fertilizer manufacture, and its ammonia-based fertilizers are in high demand both domestically and internationally.

In the chemical industry, syngas is used to make chemicals and fuels. To make syngas, coal, petroleum coke, and biomass are turned into gas. In the chemical business, syngas is used to make methanol, ammonia, and hydrogen. Through the "gas-to-liquids" (GTL) process, carbon monoxide and hydrogen react to turn syngas into methanol. Methanol can be used to make formaldehyde, acetic acid, and other things.

Syngas is both a fuel and a raw material. It can be used to heat boilers and heat exchangers in chemical plants and for other high-temperature industrial uses. According to the BASF chemical outlook report, the chemical production capacity in China will increase by 7.7% in 2022 as compared to the growth rate of 6.6% during the previous year. Thus the growth in the chemical industry is expected to drive the demand for syngas in the country.

Increasing power generation in the country is boosting the demand for syngas. According to the China Electricity Council (CEC), in 2022, the power generation capacity in the country is registered at 2559.4 gigawatts, as compared to 2376.1 gigawatts of power generation capacity in the previous year. Thus, the increasing power generation capacity is expected to drive the demand for sungas in the country.

Thus, the growth in chemical, fertilizer, and power generation industries is expected to drive the market for syngas in the country.

Asia Pacific Syngas Industry Overview

The Asia-Pacific Syngas Market is fragmented in nature. Some of the major players in the market include (not in any particular order) include Air Products and Chemicals, Inc., Air Liquide, Haldor Topsoe A/S, Linde plc, and Sasol, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Feedstock Flexibility for Syngas Production

4.1.2 Growing Demand in the Electricity and Chemical Industries

4.1.3 Increasing Hydrogen Demand for Fertilizers

4.2 Restraints

4.2.1 High Capital Investment and Funding

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Feedstock

5.1.1 Coal

5.1.2 Natural Gas

5.1.3 Petroleum

5.1.4 Pet Coke

5.1.5 Biomass

5.2 Technology

5.2.1 Steam Reforming

5.2.2 Partial Oxidation

5.2.3 Auto-thermal Reforming

5.2.4 Combined or Two-step Reforming

5.2.5 Biomass Gasification

5.3 Gasifier Type

5.3.1 Fixed Bed

5.3.2 Entrained Flow

5.3.3 Fluidized Bed

5.4 Application

5.4.1 Power Generation

5.4.2 Chemicals

5.4.2.1 Methanol

5.4.2.2 Ammonia

5.4.2.3 Oxo Chemicals

5.4.2.4 n-Butanol

5.4.2.5 Hydrogen

5.4.2.6 Dimethyl Ether

5.4.3 Liquid Fuels

5.4.4 Gaseous Fuels

5.5 Geography

5.5.1 China

5.5.2 India

5.5.3 Japan

5.5.4 South Korea

5.5.5 Australia & New Zealand

5.5.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Air Products and Chemicals, Inc.

6.4.2 Air Liquide

6.4.3 BASF SE

6.4.4 BP p.l.c.

6.4.5 DuPont

6.4.6 General Electric

6.4.7 Haldor Topsoe A/S

6.4.8 KBR Inc

6.4.9 Linde plc

6.4.10 Royal Dutch Shell plc

6.4.11 Sasol

6.4.12 Siemens

6.4.13 SynGas Technology LLC

6.4.14 TechnipFMC plc

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Utilization of Biomass and Municipal Waste

7.2 Development of Underground Coal Gasification Technology