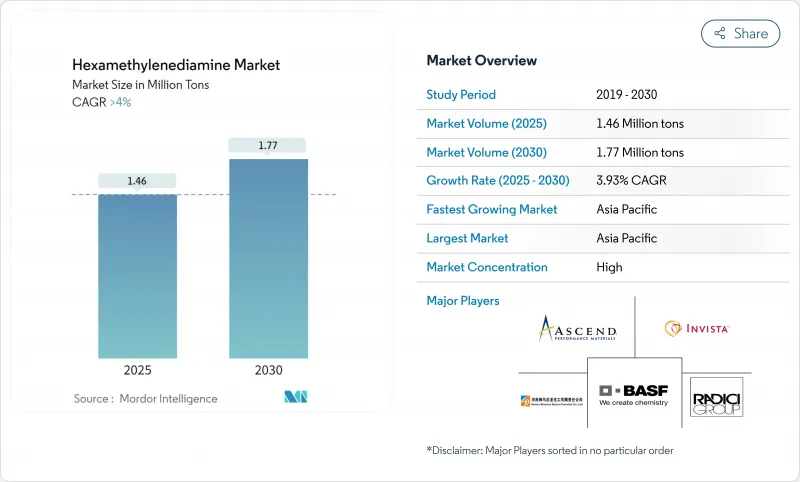

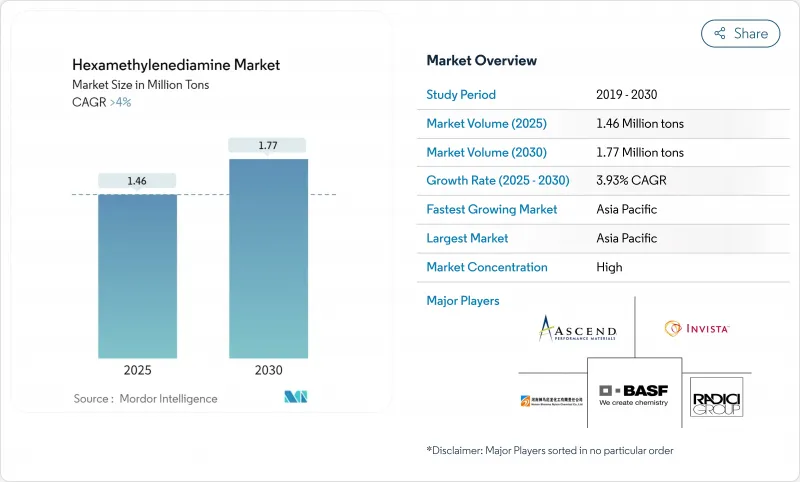

헥사메틸렌디아민 시장 규모는 2025년에 146만 톤으로 추정되며 예측 기간(2025-2030년)의 CAGR은 4%를 나타내 2030년에는 177만 톤에 달할 것으로 예상됩니다.

수요의 힘은 나일론 6,6의 생산에 뿌리를두고 있는 반면, 아디포니트릴에서 헥사메틸렌디아민으로의 연쇄에 있어서 생산 능력의 제약이, 아시아태평양, 북미, 유럽에서의 새로운 투자의 방아쇠가 되고 있습니다. 경량 자동차 부품에 대한 전략적 주력, 팬데믹 후의 테크니컬 텍스타일의 부활, 에폭시 경화제 등의 특수 용도의 꾸준한 보급이 생산량의 확대를 지지하고 있습니다. 생산자는 수직 통합을 가속화하고 저비용과 배출량 감소를 약속하는 바이오 원료를 시험적으로 도입함으로써 최근 공급 충격에 대응해 왔습니다. 동시에 원유에 연동한 원료의 불안정성, REACH 주도의 아민 배출 제한, 바이올루트의 스케일 업 리스크 등이 선행 전망을 약화시키고 있습니다.

자동차의 경량화 목표가 나일론 66의 채용을 가속하고 있어, 강하에의 침투가 헥사메틸렌디아민 시장을 밀어 올리고 있습니다. 자동차 제조업체는 폴리아미드의 강도 대 중량비, 내열성, 재활용성을 높게 평가하고 있으며, 특히 질량이 항속 거리에 직접 영향을 주는 전지식 전기자동차에서는 그 경향이 현저합니다. 아시아태평양의 OEM은 폴리아미드의 생산 능력 증대와 병행하여 나일론의 흡기 매니폴드와 구조 부재의 사용을 확대하고, 지역 간의 균형을 강화하고, 종합 공급업체에게 보상을 줍니다. 북미에서는 Tier 1공급업체가 터보차징의 열 부하에 대응하기 위해 나일론 6,6을 중심으로 엔진 베이 부품을 재설계하고 있습니다. 따라서 재료의 대체 동향은 단순한 순환 수요 증가가 아니라 구조적 수요 증가를 초래합니다.

2024년 공급 충격은 소수의 아디포니트릴 유닛에 대한 의존성을 드러냈습니다. 생산자는 중국, 멕시코 걸프, 서유럽에서 아디포니트릴루 헥사메틸렌디아민의 생산 능력을 향상시키기 위해 병목 현상을 제거하고 유리 뿌리 라인을 추진함으로써 대응했습니다. 인비스타의 메이틀랜드 재가동과 어센드의 앨라배마에서의 연산 90톤의 증설은 이 동향을 상징하고 있습니다. 이 물결은 원료의 급박을 완화시키는 반면 단기적인 공급 과잉과 지역적인 가격 변동을 가속시킬 위험도 있습니다. 그럼에도 불구하고 대부분의 운영자들은 강하의 나일론 경제성을 보호하고 아시아 중심의 최종 용도 클러스터에서 근접 우위를 얻기 위해 자본 투자가 정당화된다고 생각합니다.

아디포니트릴은 원유와 나프타의 스프레드에 연동하기 때문에 업스트림 가격 변동은 헥사메틸렌디아민의 계약 결제에 신속하게 전달되어 통합되지 않은 기업을 압박합니다. 2015년 중국 공장 사고는 집중 위험을 부각시켰고, 그 후 정유소의 운영 중단은 스팟 프리미엄의 폭을 넓혔습니다. 수입이 많은 유럽은 변동을 가장 민감하게 느끼고 나일론 방적의 전업 제조업체에 마진 압력을 강화하고 있습니다. 유로화안은 달러화 원료를 급등시켜 경쟁력을 더욱 저하시킵니다. 이러한 요인은 백 통합 프로젝트에 박차를 가하고 원유 변동에서 비용을 분리하는 바이오 루트에 대한 관심을 강화하고 있습니다.

2024년 헥사메틸렌디아민 시장에서는 나일론 생산이 78.19%의 점유율을 차지했습니다. 이 부문의 생산량은 114만 톤으로 자동차 보닛 하부 부품과 카펫 섬유에 의해 지원됩니다. 이 풀은 예측 기간 중 최대 절대 수요 증가를 지원하지만 CAGR은 3.68%에 그칩니다. 대조적으로, 에폭시 경화제나 살생물제 중간체 등의 특수 용도는 5.05%의 페이스로 확대되어 헥사메틸렌디아민 시장 규모에서 차지하는 점유율을 2025년의 25만톤에서 2030년에는 32만톤으로 끌어올립니다.

이익률이 높은 틈새 분야로의 다각화는 나일론 가격주기에 대한 수익 노출을 줄여줍니다. 생산자는 제형화 가능한 등급을 제공하여 고객의 인증 시간을 단축하고 스위칭 비용을 향상시킵니다. 또한, 이 접근법은 기존의 정제 트레인을 활용하므로 추가적인 설비 투자액은 수익에 비해 낮게 억제됩니다. 그 결과, 특수 등급의 보급은 모든 지역에서 베이스 폴리머의 성장을 능가할 것으로 예측됩니다.

헥사메틸렌디아민 시장 보고서는 용도(나일론 생산, 코팅용 중간체, 살생물제, 기타 용도(경화제, 윤활제 등)), 최종 사용자 산업(섬유, 플라스틱, 자동차, 기타 최종 사용자 산업(페인트 및 코팅, 석유화학 등)), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)으로 구분됩니다.

아시아태평양의 헥사메틸렌디아민 시장 점유율 52.06%는 중국 정화에서 나일론까지 일관된 생태계와이 지역의 자동차 및 섬유 부문의 확대를 반영합니다. 이 지역 수요는 CAGR 4.96%를 나타내, 2025년 76만톤에서 2030년에는 97만톤 근처까지 증가합니다. 정부는 첨단 재료 클러스터를 추진하고 있으며, 아디프산 원료에 근접하고 있기 때문에 공급 라인이 단축됩니다. 상하이에서 인비스타의 17억 5,000만 위안의 생산능력 배증과 같은 투자는 현지 공급망을 강화하고 경쟁력을 강화합니다.

북미 점유율은 셰일 오일에 유리한 원료와 자동차 수지에 대한 수요에 의해 지원됩니다. 하지만 수입품과의 비용 경쟁과 최근 선도적인 생산자의 파산 절차는 가격 주기에 취약성을 부각시키고 있습니다. 생산자는 고순도 등급과 바이오 등급을 중시하고, 마진을 확보하고, 전자 기기 및 의료용 OEM에서 인수를 보장합니다.

유럽은 지속가능성과 특수 틈새 시장에 주력하고 있습니다. BASF의 연산 260km의 새로운 프랑스 공장은 첨단 정제와 에너지 효율적인 반응기를 통합하고 강화되는 탈탄소 지령에 대응하고 있습니다. 아민 배출에 관한 REACH 규제는 다른 지역보다 엄격하고 컴플라이언스 비용을 인상하고 있지만, 현지 생산에 가격 경쟁력이 없는 해자를 제공합니다.

남미와 중동 및 아프리카의 두 지역은 경쟁력있는 가스 경제와 확대되는 하류 플라스틱 수요를 활용합니다. 브라질의 자동차 생산 회복과 사우디아라비아의 화학 다각화 이니셔티브는 소규모 기반이지만,이 지역의 HMD 유닛에 활로를 엽니다. 정치적·물류적 리스크에 의해 아시아태평양에 비하면 성장은 완만하지만, 국경을 넘은 합작투자가 이러한 프론티어의 생산량을 개척하려고 하고 있습니다.

The Hexamethylenediamine Market size is estimated at 1.46 million tons in 2025, and is expected to reach 1.77 million tons by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

Demand strength is rooted in nylon 6,6 production, while capacity constraints in the adiponitrile-to-hexamethylenediamine chain are triggering fresh investment across Asia-Pacific, North America and Europe. Strategic focus on lightweight vehicle parts, the post-pandemic revival of technical textiles and the steady uptake of specialty applications such as epoxy curing agents underpin volume expansion. Producers have responded to recent supply shocks by accelerating vertical integration and by piloting bio-based feedstocks that promise lower cost and reduced emissions. At the same time, crude-linked feedstock volatility, REACH-driven amine-emission limits and scale-up risk for bio routes temper the outlook.

Automotive light-weighting targets are accelerating nylon 6,6 adoption, and the downstream pull-through is boosting the hexamethylenediamine market. Vehicle makers value polyamide's strength-to-weight ratio, heat resistance and recyclability, particularly for battery-electric models where mass directly affects range. Asia-Pacific OEMs are ramping nylon intake manifold and structural-member usage alongside regional polyamide capacity additions, tightening regional balances and rewarding integrated suppliers. In North America, Tier-1 suppliers are redesigning engine-bay components around nylon 6,6 to cope with turbo-charging heat loads. The material substitution trend is therefore driving a structural, rather than merely cyclical, uplift in hexamethylenediamine demand.

Supply shocks in 2024 exposed reliance on a handful of adiponitrile units. Producers reacted by green-lighting de-bottlenecks and grass-roots lines that push integrated adiponitrile-hexamethylenediamine capacities higher in China, the Gulf Coast and Western Europe. INVISTA's Maitland restart and Ascend's 90 kt/y Alabama build-out epitomize the trend. While the wave will ease feedstock tightness, it also risks short-term oversupply and sharper regional price swings. Still, most operators deem the capex justified to safeguard downstream nylon economics and capture proximity advantages in Asia-centric end-use clusters.

Because adiponitrile tracks crude-naphtha spreads, upstream price shifts transmit quickly to hexamethylenediamine contract settlements, squeezing unintegrated players. The 2015 China plant accident underscored concentration risk, and subsequent refinery outages kept spot premiums wide. Import-heavy Europe feels swings most acutely, amplifying margin pressure on captive nylon spinners. Currency movement adds another layer: a weak euro inflates dollar-indexed feedstocks, further eroding competitiveness. These factors spur back-integration projects and intensify interest in bio-routes that decouple cost from oil volatility.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Nylon production retained a commanding 78.19% slice of the hexamethylenediamine market in 2024. The segment's volume translates to 1.14 million tons, supported by automotive under-the-hood parts and carpet fibers. This pool underpins the largest absolute demand increment over the forecast horizon, but its CAGR trails at 3.68%. In contrast, specialty uses such as epoxy curing agents and biocide intermediates are expanding at a 5.05% pace, lifting their share of the hexamethylenediamine market size from 0.25 million tons in 2025 toward 0.32 million tons in 2030.

Diversification into higher-margin niches mitigates revenue exposure to nylon price cycles. Producers supply formulation-ready grades that shorten customer qualification time, reinforcing switching costs. The approach also leverages existing purification trains, so incremental capex stays low relative to returns. As a result, specialty penetration is expected to continue outpacing base-polymer growth across all regions.

The Hexamethylenediamine Market Report is Segmented by the Application (Nylon Production, Intermediate for Coatings, Biocides, and Other Applications (Curing Agents, Lubricants, Etc. )), End-User Industry (Textile, Plastics, Automotive, and Other End-User Industries (Paints and Coatings, Petrochemicals, Etc. )), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Asia-Pacific's 52.06% stake in the hexamethylenediamine market reflects China's integrated refinery-to-nylon ecosystem and the region's outsized automotive and textile sectors. Regional demand rises at a 4.96% CAGR, lifting volume from 0.76 million tons in 2025 to nearly 0.97 million tons by 2030. Governments promote advanced materials clusters, and proximity to adipic-acid feedstock shortens supply lines. Investments such as INVISTA's RMB 1.75 billion capacity doubling in Shanghai anchor the local supply chain and strengthen competitiveness.

North America's share is underpinned by shale-advantaged feedstocks and captive automotive resin demand. Yet, cost competition from imports and recent bankruptcy proceedings at a major producer underscore vulnerability to price cycles. Producers emphasize high-purity and bio-based grades to defend margins and secure offtake from electronics and medical OEMs.

Europe is focusing on sustainability and specialty niches. BASF's new 260 kt/y French plant integrates advanced purification and energy-efficient reactors that align with tightening decarbonization directives. REACH restrictions on amine emissions are stricter than other regions, raising compliance costs yet providing a non-price competitive moat for local output.

South America plus the Middle East and Africa both regions leverage competitive gas economics and expanding downstream plastics demand. Brazil's automotive-production rebound and Saudi Arabia's chemicals diversification initiatives open windows for regional HMD units, albeit from a small base. Political and logistical risk keeps growth moderate compared with Asia-Pacific, but cross-border joint ventures are positioning to tap these frontier volumes.