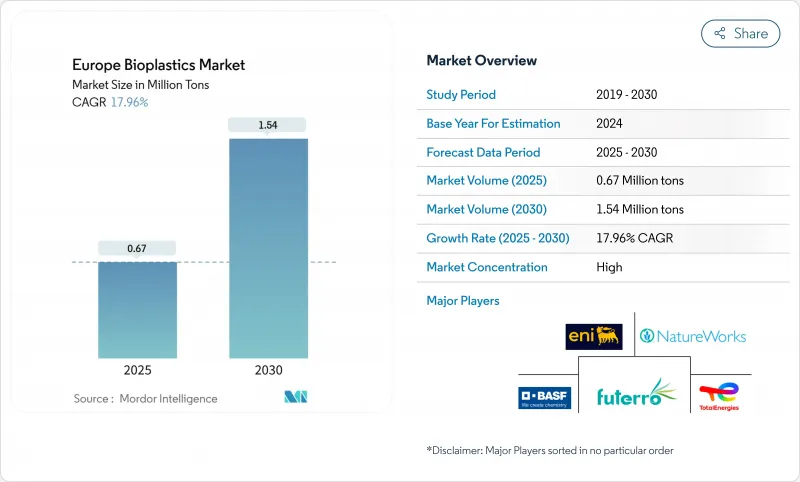

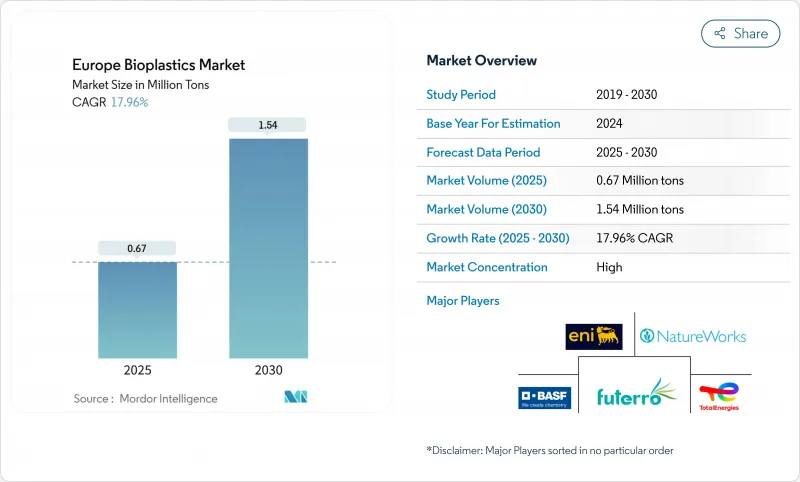

유럽의 바이오플라스틱 시장은 2025년에 현재 67만톤으로 평가되었고, 2030년에 154만톤에 이를 것으로 예측되며, 2025-2030년에 걸친 CAGR은 17.96%를 나타낼 전망입니다.

EU 전역의 정책 입안자들이 화석 기반 폴리머에 대한 규제를 강화함에 따라, 제조업체들은 바이오 기반 대안을 선택적 업그레이드가 아닌 필수 업그레이드로 간주하고 있습니다. 이러한 변화는 식품, 소매, 자동차, 소비재 가치 사슬의 조달 부서까지 확산되고 있습니다.

이 지침의 단계적 금지 조치와 재생 소재 사용 의무는 커피 캡슐, 농산물 포장백, 패스트푸드 용기 등에 사용되는 퇴비화 가능 바이오폴리머에 대한 구조적 수요를 창출하고 있습니다. 해당 법률이 브랜드명 대신 소재 성능 기준을 적용함에 따라, 생산자들은 PLA, PHA 또는 전분 혼합물을 규정 준수 경로로 포지셔닝할 수 있으며 이는 탄소 집약도 개선 효과까지 가져옵니다. 회원국별 시행 일정이 상이하여, 모듈식 생산 레시피를 보유한 기업들은 조기 시행 시장에서 선점적 점유율을 확보하고 있습니다. 특히 폴란드와 아일랜드의 차별화된 부과금 구조는 운송 탄소발자국 감축을 위한 재생 가능 원료의 현지 조달을 촉진하며, 공급망을 지역화 허브로 은연중 전환시키고 있습니다.

연포장은 이미 유럽의 바이오플라스틱 시장의 43% 점유율을 차지하며 연평균 23% 가까운 성장률을 보이고 있습니다. 필름 및 파우치 제조사들은 전체 충전 라인을 개조하지 않고도 단일 레이어를 대체할 수 있기 때문입니다. 브랜드 소유자들은 화석 PE에서 바이오 PE 또는 퇴비화 가능 라미네이트로 전환 시 발생하는 소폭의 가격 프리미엄을 상쇄하는 마케팅 효과를 보고합니다. 따라서 영업팀은 이러한 소재를 순수한 비용 항목이 아닌 수익 보호 수단으로 제안합니다. 몬디의 플렉스스튜디오(FlexStudios) 같은 혁신 허브는 고객과의 공동 개발이 리드 타임을 단축하고 기존 수지와 동등한 라인 속도를 구현하는 방법을 보여줍니다. 암묵적인 교훈은 압출 및 차단 코팅 노하우를 모두 숙달한 변환업체가 다국적 식품 기업과의 협상에서 교섭력을 확보한다는 점입니다.

EU 지역 중 극소수만이 인증된 산업용 퇴비화 시설을 운영하고 있어, 퇴비화 가능 포장재가 매립지로 보내지거나 기계적 재활용 흐름을 오염시키는 경우가 발생합니다. 이에 생산자들은 재활용과 산업용 퇴비화를 동시에 인증받은 이중 인증 등급을 출시하여 폐기 경로 간 위험을 분산시키고 있습니다. 폐기물 관리 지도를 분석하는 투자자들은 남유럽의 관광지 밀집 지역과 처리 능력 격차가 겹친다는 점을 주목하며, 신규 퇴비화 시설이 호텔 폐기물에서 안정적인 계절별 원료를 확보할 수 있을 것임을 시사합니다. 여기서 도출되는 결론은 인프라 병목 현상이 폴리머 선택뿐만 아니라 신규 바이오플라스틱 시설의 입지 결정에도 영향을 미칠 것이라는 점입니다.

바이오 기반 생분해성 소재는 2024년 유럽의 바이오플라스틱 시장 점유율 49%를 차지하며, 2030년까지 연평균 22.56%의 성장률을 기록할 것으로 예상되어 선도적 위치를 공고히 할 전망입니다. PLA 및 신흥 PHA 등급을 생산하는 고생산성 라인은 유리한 원료 조달과 특허 기술로 생산량 증가에 따라 생산 비용을 절감합니다. 생분해성 식기를 도입한 패스트푸드 체인의 초기 증거에 따르면, 기능성이 석유 기반 제품과 동등할 때 제품 품질 인식이 개선되어 재주문과 예측 가능한 규모 확대로 이어집니다. 화석 원료 가격 상승이 예상보다 빠르게 격차를 좁히면서 비용 균등화가 우려했던 것보다 조기에 달성 가능하다는 점이 시사됩니다.

바이오 기반 비생분해성 소재는 유럽의 바이오플라스틱 시장 규모에서 차지하는 비중은 작지만, 기존 PET 및 PE 재활용 흐름과 드롭인 호환성을 제공하여 역물류 시스템 변경을 꺼리는 음료 브랜드의 관심을 끌고 있습니다. 식물 기반 PET에 대한 투자 발표는 수요 주저보다는 공급 제약이 여전히 성장의 한계 요소임을 확인시켜 줍니다.

2024년 유럽의 바이오플라스틱 시장 원료별 점유율에서 사탕수수는 약 44%를 차지합니다. 브라질과 태국의 산업용 발효기가 세계적 규모로 가동되며 통합 물류를 통해 유럽에 공급되기 때문입니다. 안정적인 자당 수율과 확립된 인증 체계로 조달 리스크가 낮아 구매자들은 다년 계약을 체결합니다. 임업 및 볏짚에서 발생하는 셀룰로오스 잔여물은 현재 기반은 작지만, 도시 하수 슬러지를 PHA 중간체로 전환하는 DEEP PURPLE 프로젝트 등이 실현 가능성을 입증함에 따라 22.3%의 높은 연평균 성장률(CAGR)로 확장 중입니다. 현재 시장 분석에 따르면 셀룰로오스 기반 경로는 지정학적 공급원을 다각화하여 설탕 주기와 연계된 가격 변동성을 완화할 것으로 예상됩니다.

유럽의 바이오플라스틱 시장 보고서는 업계를 유형별(바이오 기반 생분해성, 바이오 기반 비생분해성), 원료별(사탕수수/사탕무, 옥수수, 기타), 가공 기술별(압출 성형, 사출 성형, 블로우 성형, 기타), 용도별(연포장, 경질 포장, 자동차 및 조립 작업, 기타), 국가별(독일)로 분류합니다.

The European bioplastics market is currently 0.67 million tons in 2025 and is on track to reach 1.54 million tons by 2030, supported by a forecast compound annual growth rate (CAGR) of 17.96% between 2025 and 2030.

Policymakers across the EU are tightening rules on fossil-based polymers, so manufacturers are treating bio-based alternatives as an essential rather than optional upgrade, a shift that is filtering through procurement departments in food, retail, automotive, and consumer-goods value chains.

The Directive's phased bans and recycled-content quotas are creating structural pull for compostable biopolymers in items such as coffee caps, produce bags, and quick-service trays. Since the law uses material performance criteria rather than brand names, producers can position PLA, PHA, or starch blends as compliant pathways that also score carbon-intensity gains. Member-state timelines differ, so companies with modular production recipes are capturing early share in markets that front-load enforcement. An immediate observation is that differing fee structures, especially in Poland and Ireland, encourage local sourcing of renewable feedstocks to cut transport footprints, subtly tilting supply chains toward regionalised hubs.

Flexible packaging already holds 43% European bioplastics market share and is growing at nearly 23% CAGR, because film and pouch makers can often substitute a single layer without overhauling entire filling lines. Brand owners report that switching from fossil PE to bio-PE or to a compostable laminate yields marketing benefits that offset modest price premiums, so sales teams pitch these materials as revenue protectors rather than pure cost items. Innovation hubs such as Mondi's FlexStudios demonstrate how co-development with customers cuts lead times and unlocks line-speed parity with incumbent resins. The implicit takeaway is that converters who master both extrusion and barrier-coating know-how gain bargaining power in negotiations with multinational food companies.

Only a fraction of EU regions operate certified industrial composting sites, so compostable packaging sometimes ends up in landfills or contaminates mechanical recycling streams. Producers respond by launching dual-certified grades that are both recyclable and industrially compostable, spreading risk across disposal pathways. Investors studying waste-management maps notice that capacity gaps overlap with high tourism regions in Southern Europe, suggesting that new composting plants could tap steady seasonal feedstock from hospitality waste. The inference here is that infrastructure bottlenecks will influence not just polymer selection but also plant-location decisions for new bioplastics facilities.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Bio-based biodegradables command 49% Europe Bioplastics market share in 2024 and are forecast to post a 22.56% CAGR through 2030, reinforcing their leadership position. High throughput lines producing PLA and emerging PHA grades use advantaged feedstock sourcing and license plate technologies that compress production costs as volumes ramp. Early-stage evidence from fast-food chains adopting compostable cutlery shows that product-quality perception improves when functionality matches petro-based equivalents, leading to repeat orders and predictable scale-up. A telling inference is that cost-parity looks achievable earlier than once feared because rising fossil feedstock prices narrow the gap faster than forecast.

Bio-based non-biodegradables, while representing a smaller slice of Europe's Bioplastics market size, provide drop-in compatibility with existing PET and PE recycling streams, which appeals to beverage brands reluctant to alter reverse-logistics systems. Announced investments in plant-based PET confirm that supply constraints, rather than demand hesitation, remain the growth limiter.

Sugarcane accounts for roughly 44% Europe Bioplastics market share by feedstock in 2024 because industrial fermenters in Brazil and Thailand run at world-scale and supply Europe via integrated logistics. Stable sucrose yields and established certification schemes keep procurement risks low, so buyers lock multi-year contracts. Cellulosic residues from forestry and straw hold a smaller base today but expand at a rapid 22.3% CAGR as projects such as DEEP PURPLE demonstrate the feasibility of turning municipal wastewater sludge into PHA intermediates. A current market inference is that cellulosic routes will diversify geopolitical supply, dampening price volatility linked to sugar cycles.

The Europe Bioplastics Market Report Segments the Industry by Type (Bio-Based Biodegradables, Bio-Based Non-Biodegradables), Feedstock (Sugarcane/Sugar Beet, Corn, and More), Processing Technology (Extrusion, Injection Molding, Blow Molding, and More), Application (Flexible Packaging, Rigid Packaging, Automotive and Assembly Operations, and More), and Country (Germany, United Kingdom, Italy, France, Netherlands, and More).