인도네시아의 플라스틱 포장 시장 전망 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Indonesia Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1639534

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

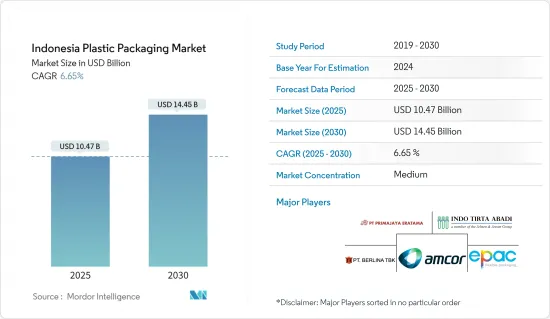

인도네시아의 플라스틱 포장 시장 규모는 2025년에 104억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 연평균 성장율(CAGR)은 6.65%로, 2030년에는 144억 5,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

기술 발전과 최종 사용자 산업 포장 용도의 확대는 인도네시아 포장 시장의 성장을 이끄는 핵심 요소입니다. 인도네시아의 인구 증가와 1인당 포장 소비량 증가가 이러한 추세에 크게 기여하고 있습니다. 편의용품에 대한 수요 증가, 기존 포장재의 대안으로 플라스틱 채택 증가 등 소비자 행동 변화는 시장 확대를 더욱 촉진하고 있습니다.

플라스틱 포장은 포장 산업에 새로운 방식을 도입했습니다. 내구성이 뛰어나고 가볍고 편안한 포장 솔루션은 아태지역 전역에서 포장재로 플라스틱의 사용을 확대했습니다.

인인도네시아의 경제 성장과 이동 중에도 먹을 수 있는 일회용 편의 식품에 대한 수요로 인해 연포장 생산이 증가했습니다. 연포장 제품 유형 중 파우치는 바쁜 라이프스타일과 많은 근로 인구로 인해 인도네시아의 즉석조리식품(RTE) 시장이 증가함에 따라 상당한 점유율을 차지할 것으로 예상됩니다. 연구 대상 시장은 액체 및 음료 포장에 대한 저렴한 대안을 선택할 것으로 예상되며, 따라서 다른 유형의 포장재보다 저렴하기 때문에 연포장재가 널리 사용될 것으로 예상됩니다.

이 지역에서는 LDPE 포장재 가격이 저렴하기 때문에 이 소재를 사용하는 데 드는 추가 비용이 판매자에게 미치는 영향은 미미할 것으로 보입니다. 폴리프로필렌, 폴리이소프렌, 폴리우레탄으로 만든 수술용 마스크에 대한 수요도 증가했습니다.

플라스틱 오염은 생태계에 미치는 해로운 영향을 강조하는 수많은 연구 결과와 함께 전 세계적인 환경 문제로 떠올랐습니다. 이에 따라 인도네시아는 플라스틱 사용을 억제하기 위한 규제를 시행하고 있습니다. 인도네시아 플라스틱 포장재 시장은 현재 플라스틱 수지 가격 상승으로 인해 상당한 어려움에 직면해 있습니다. 이러한 추세로 인해 현지 제조업체들은 수지 가격 상승에 따른 비용 회수가 지연되고 수익성이 감소하고 있습니다.

인도네시아의 플라스틱 포장 시장 동향

폴리에틸렌 테레프탈레이트(PET)가 가장 큰 시장 점유율을 차지

가볍고 내구성이 뛰어난 페트병은 유리병을 점점 더 많이 대체하고 있습니다. 이러한 변화는 생수 및 기타 음료를 보다 비용 효율적으로 운송할 수 있게 해줍니다. PET의 투명성과 고유한 CO2 차단 특성은 다양한 용도에 적합합니다. 이 소재는 병이나 다른 모양으로 쉽게 성형할 수 있으며 착색제, 자외선 차단제, 산소 차단제와 같은 첨가제를 사용하여 특정 브랜드 요구 사항을 충족하도록 특성을 강화할 수 있습니다.

경질 패키징에서 PET는 청량음료, 물, 주스, 스포츠 음료, 맥주, 조미료, 식품 용기 등 다양한 제품을 위한 전자레인지용 식품 트레이와 병을 생산합니다. PET 병에 대한 수요는 홈 케어, 음료, 퍼스널 케어 등 여러 분야에서 증가하고 있습니다. 이러한 성장은 주로 소비자 선호도와 가벼운 특성 및 높은 재활용성 등 PET의 주요 특성에 의해 주도되고 있습니다.

우유에 대한 수요가 증가하면 더 많은 포장재 생산이 필요하게 됩니다. 이러한 성장은 새로운 제조 시설에 대한 투자, 생산 능력 확대, PET 포장의 기술 발전으로 이어질 수 있습니다.

경제협력개발기구는 인도네시아의 생유제품 소비량이 향후 수년간 증가할 것으로 예측했습니다. 경제협력개발기구는 인도네시아의 생유 소비량은 향후 수년간 증가할 것으로 예측하고 있으며, 국민 1인당 연간 평균 성장률은 약 1kg(24.88%)로, 2031년에는 국민 1인당 소비량이 5.01kg에 달할 것으로 예측했습니다.

이와 같이 예상되는 신선한 유제품 소비 증가는 인도네시아의 PET 병 포장 시장에 긍정적인 영향을 미칠 것으로 예상됩니다. PET 병은 유제품을 포함한 다양한 제품의 포장에 자주 사용되는 소재입니다.

현저한 성장을 보이는 식품 부문

급속한 도시화와 슈퍼마켓, 대형 마트, 식료품점, 편의점, 쇼핑 센터의 증가로 파우치 및 가방 시장이 커지고 있습니다. 식음료 산업의 성장도 시장에 긍정적인 영향을 미칩니다. 또한 친환경 제품에 대한 소비자 선호도가 변화하면서 생분해성 플라스틱 파우치와 가방에 대한 수요도 증가하고 있습니다.

미국 농무부(USDA)는 인도네시아가 식품 가공 산업의 원자재 수요를 충족하기 위해 미국 원료 공급업체에게 상당한 기회를 제공한다고 보고했습니다. 미국은 인도네시아에서 세 번째로 큰 농산물 공급국으로, 11%의 시장 점유율을 차지하고 있습니다. 2023년 대두와 유제품은 미국 전체 대인도네시아 농산물 수출의 약 절반을 차지했습니다.

2024년 10월 17일부터 인도네시아의 수많은 식품, 식재료, 첨가물 및 모든 가공식품에 대해 할랄 인증이 의무화될 예정입니다.

할랄 인증 식품에 대한 수요가 증가함에 따라 할랄 기준을 충족하는 포장재에 대한 수요도 함께 증가할 것입니다. 이는 할랄 인증을 받았거나 할랄 제품을 취급하도록 특별히 설계된 플라스틱 포장재에 대한 수요 증가로 이어질 수 있습니다.

유기농 식품 부문은 종종 지속 가능성과 환경적 책임을 강조합니다. 이러한 추세는 생분해성 또는 재활용 가능한 플라스틱과 같은 보다 친환경적인 플라스틱 포장 솔루션의 개발과 채택을 촉진할 수 있습니다. 기업들은 유기농 시장의 가치에 부합하는 포장재를 만드는 데 투자할 가능성이 높습니다.

유기농 무역협회에 따르면 2022년 인도네시아에서 유기농 포장 식품의 소비 가치는 약 1,570만 달러에 달했습니다. 이 가치는 2025년에 1,900만 달러로 증가할 것으로 예상됩니다.

인도네시아의 플라스틱 포장 산업 개요

이 시장은 반통합 시장으로 몇몇 주요 업체들이 주도하고 있습니다. Amcor Group, Prima Jaya Eratama, PT ePac Flexibles Indonesia, PT Berlina Tbk, PT Indo Tirta Abadi는 포장 솔루션의 급증하는 수요를 해결하는 데 매우 중요합니다. 이 기업들은 기존의 플라스틱 포장재에서 벗어나고 있을 뿐만 아니라 지속 가능한 플라스틱 대체재에 대한 소비자의 선호도가 높아지는 추세에 발맞추고 있습니다. 이들 기업은 시장 입지를 강화하기 위해 전략을 세밀하게 조정하고, 제품군을 확대하며, 지속 가능성에 중점을 두고 협업과 인수를 적극적으로 모색하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

산업 밸류체인 분석

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

제5장 시장 역학

시장 성장 촉진요인

경량 포장 방식의 채용 증가

친환경 포장 및 재생 플라스틱 증가

시장의 과제

원재료(플라스틱 수지) 가격 상승

정부의 규제와 환경 문제

제6장 시장 세분화

경질 플라스틱 포장

재료 유형

폴리에틸렌(PE)

폴리에틸렌테레프탈레이트(PET)

폴리프로필렌(PP)

폴리스티렌(PS) 및 발포 폴리스티렌(EPS)

폴리염화비닐(PVC)

기타 재료

제품 유형

병과 항아리

트레이와 용기

기타 제품 유형

연질 플라스틱 포장

재료 유형

폴리에틸렌(PE)

2축 연신 폴리프로필렌(BOPP)

캐스트 폴리프로필렌(CPP)

폴리염화비닐(PVC)

에틸렌비닐알코올(EVOH)

기타 재료

제품 유형

파우치

가방

필름, 랩

기타 제품 유형

최종 사용자 산업

식품

음료

헬스케어

화장품, 퍼스널케어

기타 최종 사용자 산업

제7장 경쟁 구도

기업 프로파일

Amcor Group

Prima Jaya Eratama

PT ePac Flexibles Indonesia

PT Berlina Tbk

PT Indo Tirta Abadi

Sonoco Products Company

PT Solusi Prima Packaging

PT Hasil Raya Industries

PT Indonesia Toppan Printing

제8장 투자 분석

제9장 시장의 미래

HBR

영문 목차

영문목차

The Indonesia Plastic Packaging Market size is estimated at USD 10.47 billion in 2025, and is expected to reach USD 14.45 billion by 2030, at a CAGR of 6.65% during the forecast period (2025-2030).

Key Highlights

Technological advancements and expanding end-user industry packaging applications are key factors driving the growth of Indonesia's packaging market. The country's increasing population and rising per capita packaging consumption contribute significantly to this trend. Consumer behavior shifts, including the growing demand for convenience products and the increased adoption of plastic as an alternative to traditional packaging materials, further propel market expansion.

Plastic packaging has implemented new ways for the packaging industry to function. Durable, lightweight, and comfortable packaging solutions have augmented the use of plastics as a packaging material across the region.

Economic growth and the need for single-serve, on-the-go convenience foods in Indonesia have increased flexible packaging production. Among flexible packaging product types, pouches are expected to hold a significant share due to the country's increasing market for Ready-to-Eat (RTE) foods, owing to the busy lifestyle and many working populations. The studied market is anticipated to opt for a low-cost alternative for liquid and beverage packaging and hence see wide usage of flexible packaging as it is cheaper than other types of packaging.

The price of LDPE packaging is currently low in the region, which means that the additional cost of using the material will have minimal impact on sellers. The demand for surgical masks made of polypropylene, polyisoprene, and polyurethane has also increased.

Plastic pollution has emerged as a global environmental concern, with numerous studies highlighting its detrimental effects on ecosystems. In response, Indonesia has implemented regulations to curb plastic usage. The Indonesian plastic packaging market now faces significant challenges due to rising plastic resin prices. This trend has resulted in delays in recovering increased resin costs and diminished profitability for established local manufacturers.

Indonesia Plastic Packaging Market Trends

Polyethylene Terephthalate (PET) Occupies the Largest Market Share

Due to their lightweight and durable nature, PET bottles are increasingly replacing glass bottles. This shift allows for more cost-effective transportation of mineral water and other beverages. PET's transparency and inherent CO2 barrier properties suit it for various applications. The material can be easily moulded into bottles or other shapes, and its properties can be enhanced with additives such as colourants, UV blockers, and oxygen barriers to meet specific brand requirements.

In rigid packaging, PET produces microwavable food trays and bottles for various products, including soft drinks, water, juices, sports drinks, beer, condiments, and food containers. The demand for PET bottles is growing across multiple sectors, including home care, beverages, and personal care. This growth is primarily driven by consumer preferences and PET's key attributes, such as its lightweight nature and high recyclability.

Increased demand for milk will necessitate more packaging production. This growth can lead to investment in new manufacturing facilities, expanded production capabilities, and technological advancements in PET packaging.

The Organisation for Economic Cooperation and Development forecasts that Indonesia's consumption of fresh milk products will increase over the coming years. They project a compound annual growth rate of approximately one kilogram per capita (+24.88%) and estimate that by 2031, the consumption per capita will reach 5.01 kg.

This anticipated rise in fresh dairy product consumption is expected to impact Indonesia's PET bottle packaging market positively. PET bottles are a commonly used material for packaging various products, including dairy items.

Food Segment to Show Significant Growth

Rapid urbanization and the growing number of supermarkets, hypermarkets, grocery stores, convenience stores, and shopping centers increase the market for pouches and bags. The growth of the food and beverage industry also positively impacts the market. Futhermore, the changing consumer preferences towards eco-friendly products also drive the need for non-biodegradable plastic pouches and bags.

The United States Department of Agriculture (USDA) reports that Indonesia presents substantial opportunities for United States ingredient suppliers to meet the raw material needs of its food processing industry. The United States ranks as the third-largest agricultural supplier to Indonesia, holding an 11% market share. In 2023, soybeans and dairy products constituted approximately half of all US agricultural exports to Indonesia.

Starting October 17, 2024, halal certification will become mandatory for numerous foods, ingredients, additives, and all processed food products in Indonesia.

As the demand for halal-certified food products rises, there will be a parallel need for packaging that meets halal standards. This could lead to increased demand for plastic packaging that is certified or specifically designed to handle halal products.

The organic food sector often emphasizes sustainability and environmental responsibility. This trend can drive the development and adoption of more eco-friendly plastic packaging solutions, such as biodegradable or recyclable plastics. Companies will likely invest in creating packaging that aligns with the organic market's values.

According to the Organic Trade Association, in 2022, the consumption value of organic packaged food in Indonesia amounted to around USD 15.7 million. The value was forecast to increase to USD 19 million in 2025.

Indonesia Plastic Packaging Industry Overview

The market is semi-consolidated and driven by several key players. Amcor Group, Prima Jaya Eratama, PT ePac Flexibles Indonesia, PT Berlina Tbk, and PT Indo Tirta Abadi are pivotal in addressing the surging demand for packaging solutions. These companies are not only moving away from conventional plastic packaging but are also aligning with the growing consumer preference for sustainable plastic alternatives. To bolster their market presence, these firms are fine-tuning their strategies, broadening their product offerings, and actively seeking collaborations and acquisitions, with a pronounced focus on sustainability.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Consumers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Adoption of Lightweight Packaging Methods

5.1.2 Increased Eco-friendly Packaging and Recycled Plastic

5.2 Market Challenges

5.2.1 High Price of Raw Material (Plastic Resin)

5.2.2 Government Regulations and Environmental Concerns

6 MARKET SEGMENTATION

6.1 Rigid Plastic Packaging

6.1.1 Material Type

6.1.1.1 Polyethylene (PE)

6.1.1.2 Polyethylene terephthalate (PET)

6.1.1.3 Polypropylene (PP)

6.1.1.4 Polystyrene (PS) and Expanded polystyrene (EPS)