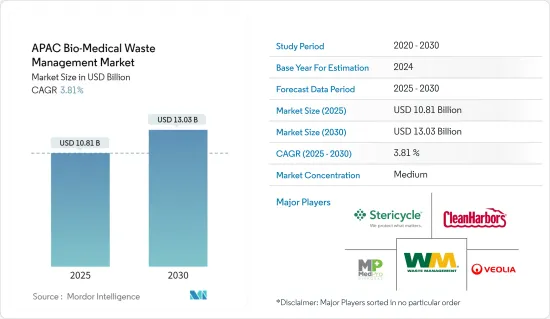

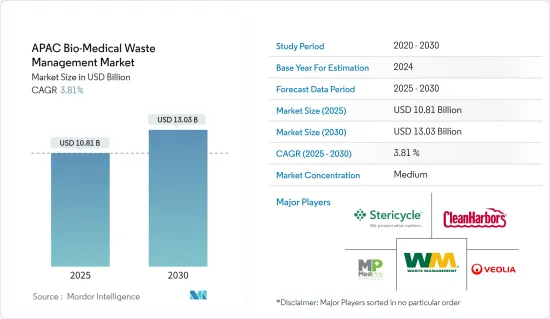

아시아태평양의 바이오 의료 폐기물 관리 시장 규모는 2025년에 108억 1,000만 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 3.81%로 전망되며, 2030년에는 130억 3,000만 달러에 달할 것으로 예측됩니다.

아시아태평양의 바이오 의료 폐기물 관리 시장은 병원, 클리닉, 연구소, 연구 기관 등의 건강 관리 시설에서 발생하는 폐기물의 수집, 처리 및 처분에 중점을 둡니다. 이 시장을 견인하는 것은 엄격한 정부 규제, 건강 관리 부문의 성장, 부적절한 바이오 의료 폐기물 처리가 환경에 미치는 영향에 대한 의식 증가입니다.

인도에서는 총 1,590 TPD의 처리 능력이 있음에도 불구하고 약 700 TPD의 바이오 의료 폐기물이 발생하고 640 TPD가 처리되고 있습니다. 소각 처리 능력은 857 TPD, 오토클레이브 처리 능력은 752 TPD로 보고되었습니다.

이러한 잉여 능력에도 불구하고 국내 20개 주에서는 CBWTF가 부족하여 캡티브 처리 수단과 깊은 구멍 매설에 의존하고 있습니다. 그러나 기존의 틈이나 누출을 다루지 않으면 폐기물 발생량 증가가 과제가 될 수 있습니다. 모든 SPCB는 갭 분석을 수행하고, 누출을 추정하고, 이 시나리오를 해결하기 위해 새로운 CBWTF를 전략적으로 계획하도록 요구됩니다.

13,500개 이상의 의료 시설이 있는 베트남에서는 매일 약 22톤의 플라스틱 폐기물이 발생합니다. 이 중 65% 이상이 감염성입니다. 감염성 플라스틱 폐기물이 만연하고 있는 주요 원인은 기구나 공구에서 점적 라인이나 주사기에 이르기까지 다양한 의료 용도로 플라스틱이 많이 사용되고 있다는 점입니다.

사태의 심각성을 인식한 CHERAD는 베트남의 여러 병원과 제휴하여 순환 경제 모델을 시험적으로 도입했습니다. '오염 감소' 프로젝트의 일환으로 칸토 중앙 종합 병원은 의료용 플라스틱 폐기물을 소독하는 오토 클레이브 시스템을 채택했습니다. 이 활동에는 폐기물 분류, 재활용 및 커뮤니티 참여를 강화하기 위한 교육 세션도 포함됩니다.

팬데믹 기간 동안 인도네시아에서는 하루 30%의 의료 폐기물이 급증했으며, 총량은 약 382톤으로 팬데믹 전 293톤에서 증가했습니다. 이 데이터는 전국 2,820개 병원과 9,884개 보건소에서 얻은 것입니다. 특히 자카르타에서는 수도에서 약 30km 떨어진 서부 자바 주 부카시의 블랑켄 매립지에서 의료 폐기물이 500%나 급증했습니다.

인도네시아는 많은 국가들과 마찬가지로 재활용 불가능하고 생분해성이 없는 플라스틱 폐기물의 과제를 다루고 있으며 매립지의 현저한 축적으로 이어지고 있습니다. 인도네시아 최대 자카르타에 위치한 반탈 게반 매립지에서는 매일 900대 이상의 트럭이 5,000톤 이상의 고형 폐기물을 내리고 있습니다. 이 긴급성을 인식한 인도네시아는 2025년까지 플라스틱 폐기물을 70% 줄이는 야심찬 목표를 세웠으며, 이 목표를 향해 매년 10억 달러를 기부하고 있습니다.

인도, 베트남, 인도네시아와 같은 국가들이 바이오 의료 폐기물 관리로 전진하고 있는 반면, 특히 도시와 농촌 지역 사이에는 격차가 존재합니다. 인도의 급성장은 신흥국이 폐기물 관리 시스템의 현저한 개선을 보이는 등 상황이 진화하고 있음을 뒷받침합니다.

결론적으로, 바이오 의료 폐기물 관리는 특히 폐기물 발생량 증가와 재활용 불가능한 물질이 야기하는 과제에 직면하는 많은 국가들에게 여전히 중요한 문제입니다.

특히 신흥국에서는 큰 진전을 볼 수 있는 것, 지속가능하고 효과적인 폐기물 관리를 실천하기 위해서는 지속적인 투자, 전략적 계획, 지역 사회의 관여가 분명히 필요합니다.

인도, 베트남, 인도네시아와 같은 국가의 노력은 바이오 의료 폐기물이 환경과 건강에 미치는 영향을 줄이기 위해 능력과 운영 과제를 다루는 것의 중요성을 강조합니다.

2022 회계년도 남아시아에서는 유해 폐기물 생산량이 급증하여 1,200만 톤을 넘어 거의 절반이 이용 가능하다고 간주되었습니다. Indian Journal of Pharmacy Practice의 보고서에 따르면, 의약품 수요의 급증은 의약품 폐기물 증가와 직결된다고 강조합니다.

인도 중앙공해관리위원회(Central Pollution Control Board)의 데이터에 따르면 인도의 의료 시설은 총 4,075톤 이상의 폐기물을 매일 배출하고 있습니다. WHO와 유니세프의 공동평가에 따르면 24개국의 의료시설 중 적절한 의약품 폐기물 관리 시스템을 도입하고 있는 것은 58%에 불과합니다.

이 보고서는 또한 의약품 폐기물의 처리에 화학 소독제를 사용하면 실수로 유해 화합물을 대기 중에 방출해 버릴 가능성이 있으며, 취급을 잘못하면 심각한 건강 피해를 초래한다고 경고하고 있습니다.

베트남에 초점을 맞추면, 이 나라는 13,500개가 넘는 의료 시설을 자랑하며, 총 매일 약 22톤의 플라스틱 폐기물을 배출하고 있으며, 감염성 폐기물은 이 양의 65% 이상을 차지하고 있습니다. 반면 중국은 2022년 100만 톤 이상의 유해산업 폐기물을 처리했습니다.

이 산업 폐기물은 고체, 반고체, 액체 및 미처리 상태로 방치되면 본질적으로 독성이 있으며 오염되어 위험합니다. 정화 방법에는 화학적, 생물학적 치료, 열이용, 고형화 등이 있습니다.

결론적으로 남아시아, 베트남, 중국의 유해 폐기물 생산량 증가는 효과적인 폐기물 관리 솔루션의 긴급한 필요성을 강조합니다. 이 데이터는 건강 위험과 환경 오염을 줄이기 위해 적절한 처리 및 처분 방법의 중요한 역할을 돋보이게 합니다.

의약품과 산업활동에 대한 수요가 계속 증가하고 있는 가운데 공중위생과 환경을 지키기 위해 견고한 폐기물 관리 방법의 도입이 점점 중요해지고 있습니다.

14억 명이 넘는 인구를 보유한 중국은 엄청난 의료 폐기물을 배출하는 거대한 건강 관리 시스템을 운영하고 있으며 견고한 폐기물 관리 솔루션이 필요합니다.

중국의 도시화와 경제 성장은 의료시설의 확대로 이어져 바이오 의료 폐기물의 발생이 상승하고 있습니다. 그럼에도 불구하고 중국의 의료비는 늘어나고 있지만 많은 고소득 국가에 비해 여전히 늦어지고 있습니다. 고령화와 부유층 증가로 인한 압력 증가를 예측하고, 정부는 향후 10년 동안 건강 관리 예산을 강화할 계획입니다.

게다가 사회적 지출은 중국의 의료 상황을 형성하는데 있어서 매우 중요한 역할을 하게 될 것으로 보입니다. China Merchants Securities의 수석 매크로 분석가인 Xie Yaxuan은 보험, 건강 보험료, 사회 의료 보조를 포함한 사회 및 상업 채널의 비율이 증가하는 건강 관리 자금의 변화를 강조했습니다.

중국 정부는 환경 및 공중 보건의 위험을 줄이기 위해 의료 폐기물의 적절한 처리를 보장하기 위해 엄격한 규제를 도입했습니다. 정부는 집중처리 시스템을 확립하고 소각과 같은 선진기술을 활용함으로써 효율성과 환경에 대한 친절함을 높였습니다.

바이오 메디컬 폐기물 관리에서 중국의 장점은 폐기물의 대량 발생으로 이어지는 엄청난 인구와 광범위한 건강 관리 시스템, 정부의 엄격한 감독, 첨단 기술에 대한 많은 투자, 지속적인 경제 성장, 환경 의식 증가 등 여러 요인으로 인해 발생합니다. 이러한 요소들이 함께 중국은 효과적인 바이오 의료 폐기물 관리의 전면 러너로서의 지위를 확고하게 하고 있습니다.

아시아태평양의 바이오 의료 폐기물 관리 시장은 주로 소수의 주요 기업이 주도하는 현저한 집중이 특징입니다. 이러한 이점은 엄청난 진입 장벽, 인프라 및 기술 투자에 대한 큰 수요, 대규모 기업이 소규모 경쟁사를 흡수하는 동향에 기인합니다.

이 상황에서 주목할만한 기업은 Stericycle Inc., Veolia Environmental Services, Waste Management Inc., Clean Harbors Inc., MedPro Disposal 등입니다. 그 결과, 시장 경쟁 구도는 계속 안정되고, 이러한 대기업은 시장 역학에 영향을 미치고 혁신을 추진할 것으로 예상됩니다.

The APAC Bio-Medical Waste Management Market size is estimated at USD 10.81 billion in 2025, and is expected to reach USD 13.03 billion by 2030, at a CAGR of 3.81% during the forecast period (2025-2030).

The APAC Bio-Medical Waste Management Market focuses on the collection, treatment, and disposal of waste generated from healthcare facilities like hospitals, clinics, laboratories, and research institutions. This market is driven by stringent government regulations, the growing healthcare sector, and increasing awareness about the environmental impact of improper biomedical waste disposal.

India generates approximately 700 TPD of biomedical waste, with 640 TPD being treated, despite a combined treatment capacity of 1,590 TPD. The reported incineration capacity of the country stands at 857 TPD while autoclaving capacity is 752 TPD.

Despite this surplus capacity, 20 states in the country resort to captive treatment measures and deep pit burials due to the lack of CBWTFs. However, the rising waste generation could pose challenges if existing gaps and leakages are not addressed. All SPCBs are urged to conduct gap analyses, estimate leakages, and strategically plan newer CBWTFs to tackle this scenario.

Vietnam, with over 13,500 medical facilities, generates roughly 22 tons of plastic waste daily. Of this, more than 65% is infectious. The prevalence of infectious plastic waste is primarily due to the extensive use of plastic in various medical applications, from equipment and tools to intravenous lines and syringes.

Recognizing the gravity of the situation, CHERAD partnered with multiple hospitals in Vietnam to pilot a circular economy model. As part of the "Reducing Pollution" project, Can Tho Central General Hospital adopted an autoclave system to disinfect medical plastic waste. This initiative includes training sessions to enhance waste separation, recycling, and community engagement.

During the pandemic, Indonesia witnessed a 30% surge in daily medical waste, totaling around 382 tonnes, up from pre-pandemic figures of 293 tonnes. This data was sourced from 2,820 hospitals and 9,884 health centers nationwide. Notably, Jakarta saw a 500% spike in medical waste at the Burangkeng landfill in Bekasi, West Java, around 30 kilometers from the capital.

Indonesia, like many nations, grapples with the challenge of non-recyclable and non-biodegradable plastic waste, leading to significant landfill accumulation. The Bantar Gebang landfill in Jakarta, Indonesia's largest, witnesses over 900 trucks daily, unloading more than 5,000 tonnes of solid waste. Recognizing the urgency, Indonesia has set an ambitious target of slashing plastic waste by 70% by 2025, with a commitment of USD 1 billion annually toward this goal.

While countries like India, Vietnam, and Indonesia are making strides in biomedical waste management, disparities exist, especially between urban and rural regions. India's rapid growth underscores the evolving landscape, with emerging economies showing marked improvements in their waste management systems.

In conclusion, the management of biomedical waste remains a critical issue for many countries, particularly in the face of increasing waste generation and the challenges posed by non-recyclable materials.

While significant progress has been made, especially in emerging economies, there is a clear need for continued investment, strategic planning, and community engagement to ensure sustainable and effective waste management practices.

The efforts of countries like India, Vietnam, and Indonesia highlight the importance of addressing both capacity and operational challenges to mitigate the environmental and health impacts of biomedical waste.

In the financial year 2022, South Asia saw a surge in hazardous waste production, exceeding 12 million metric tons, with almost half being deemed utilizable. A report from the Indian Journal of Pharmacy Practice highlighted that the upsurge in pharmaceutical demand directly correlates with increased drug wastage.

Data from India's Central Pollution Control Board revealed that healthcare facilities in the country collectively produce over 4,075 tons of waste daily. A joint assessment by WHO and UNICEF found that only 58% of healthcare facilities across 24 countries have proper pharmaceutical waste management systems in place.

The report also warns that using chemical disinfectants to treat pharmaceutical waste can inadvertently release harmful compounds into the atmosphere, posing significant health risks if mishandled.

Shifting focus to Vietnam, the nation boasts over 13,500 medical facilities, collectively generating approximately 22 tons of plastic waste each day, with infectious waste accounting for over 65% of this volume. Meanwhile, in 2022, China disposed of over one million metric tons of hazardous industrial waste.

This industrial waste, spanning solid, semi-solid, and liquid forms, is inherently toxic, polluting, and hazardous if left untreated. Remediation methods encompass chemical and biological treatments, heat applications, and solidification.

In conclusion, the escalating production of hazardous waste in South Asia, Vietnam, and China underscores the urgent need for effective waste management solutions. The data highlights the critical role of proper treatment and disposal methods to mitigate health risks and environmental pollution.

As the demand for pharmaceuticals and industrial activities continues to rise, implementing robust waste management practices becomes increasingly vital to safeguard public health and the environment.

With a population exceeding 1.4 billion, China operates a vast healthcare system that yields substantial volumes of medical waste, necessitating robust waste management solutions.

Urbanization and economic growth in China have led to the expansion of healthcare facilities, consequently escalating the generation of biomedical waste. Despite this, China's healthcare expenditure, while growing, still lags behind that of many high-income nations. Anticipating heightened pressure from an aging and increasingly affluent populace, the government plans to bolster healthcare budgets over the coming decade.

Furthermore, social expenditures are poised to be pivotal in shaping China's healthcare landscape. Xie Yaxuan, Chief Macro Analyst at China Merchants Securities, highlighted a shift in healthcare funding, with an increasing share coming from social and commercial channels, including insurance, health premiums, and social healthcare aid.

The Chinese government rolled out stringent regulations to ensure the proper disposal of medical waste, aiming to mitigate environmental and public health risks. The government established centralized disposal systems, leveraging advanced technologies like incineration, enhancing efficiency and eco-friendliness.

China's preeminence in biomedical waste management results from several factors, including its massive population and extensive healthcare system, leading to high waste generation, stringent government oversight, substantial investments in cutting-edge technologies, sustained economic growth, and increasing environmental consciousness. These elements collectively solidify China's position as a frontrunner in effective biomedical waste management.

The bio-medical waste management market in Asia-Pacific is characterized by significant concentration, primarily led by a handful of key players. This dominance results from formidable entry barriers, substantial demands for infrastructural and technological investments, and the trend of larger entities absorbing smaller competitors.

Notable players in this landscape encompass Stericycle Inc., Veolia Environmental Services, Waste Management Inc., Clean Harbors Inc., and MedPro Disposal. Consequently, the market's competitive landscape is expected to remain stable, with these major players continuing to influence market dynamics and drive innovation.