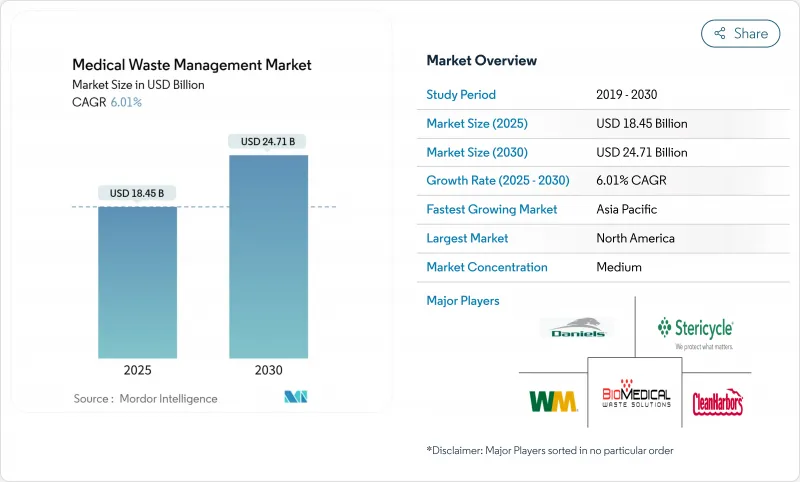

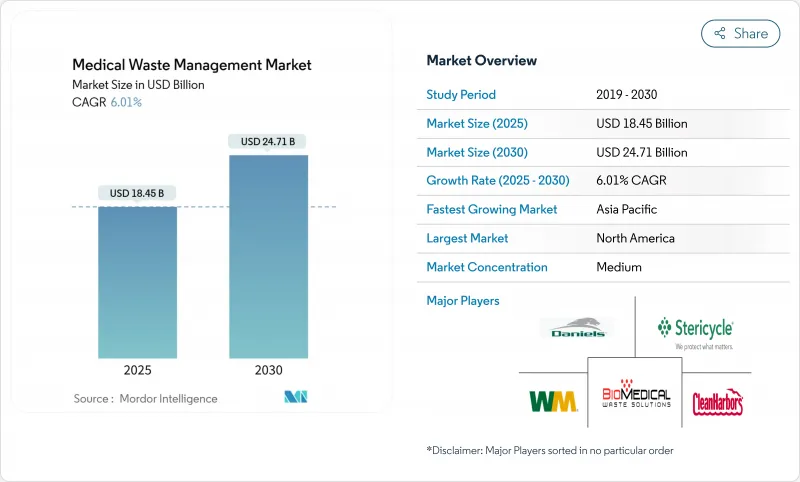

의료 폐기물 관리 시장 규모는 2025년 184억 5,000만 달러로 추정되며, 시장 추정 및 예측 기간(2025-2030년) 동안 6.01%의 연평균 복합 성장률(CAGR)로 2030년에는 247억 1,000만 달러에 달할 것으로 예측됩니다.

빠른 성장은 팬데믹 이후 역량 구축, 원격 의료의 보급, 안전한 폐기를 위한 기술 수준을 높이는 여러 지역의 규제 강화에 기인합니다. 열처리는 여전히 선도적 지위를 유지하고 있지만, 현장 모듈식 시스템, 데이터 기반 분리수거, 순환경제형 회수 서비스는 병원, 진료소, 재택의료 채널에서 빠르게 확대되고 있습니다. 자동화 및 배출 감소 기술과 컴플라이언스 전문성을 결합한 서비스 제공업체는 지불자와 규제 당국이 환경적 성과와 상환을 연계하고 있기 때문에 프리미엄 계약을 체결할 수 있습니다. 동시에 염소계 화학물질의 세계 공급 제약과 소각로 허가 규정의 변화로 인해 사업자들은 처리 포트폴리오를 다양화하고, 특히 급성장하는 아시아 및 중남미 시장에서 규제 리스크를 헤지해야 할 필요성이 대두되고 있습니다.

연방, 주 및 초국가적 프로그램은 지속 가능한 폐기물 인프라에 새로운 자본을 투입하고 있습니다. 미국 환경보호청(EPA)은 2024년 5,800만 달러를 '재활용을 위한 고형폐기물 인프라 보조금'으로 지급하고, 의료폐기물 분리수거 시설과 소외된 지역사회에 대한 접근에 자금을 배정했습니다. 마찬가지로, 2025년 HHS 예산안은 간접적으로 시설 추적 및 감사 시스템에 자금을 지원하는 환경 보건 이니셔티브에 11억 달러를 요구하고 있습니다. 이러한 자금 투입은 장비 업그레이드를 촉진하고, 지역 치료 파일럿을 촉진하며, 배출량 감소와 공정한 서비스 이용을 증명할 수 있는 공급업체를 우선적으로 선정할 수 있도록 합니다. 환경정의 지표와 검증 가능한 지역사회 건강 성과와 일치하는 제안서를 제출하는 업체는 공공 입찰에서 우선 공급업체 지위를 얻게 됩니다.

재택수액, 자가주사, 원격진단의 보급으로 케어의 연속성이 확대되고, 규제 대상인 날카로운 물건이나 감염성 폐기물이 지자체 운반업체가 관리할 수 없는 주택 내 흐름에 놓이게 되었습니다. 의료 네트워크는 현재 안전한 회수를 위해 분산형 회수, 환자 교육 이니셔티브, 공급망 재설계를 병행하고 있습니다. 정액제 샤프 우편 수거, IoT 지원 충전 레벨 센서, 변조 방지 용기를 제공하는 업체들은 특히 공동주택이 밀집되어 격리를 복잡하게 만드는 혼잡한 도시 지역에서 빠르게 규모를 확장하고 있습니다. 분산형 폐기물 모델은 책임 추궁의 대상을 확대하기 때문에 추적성 소프트웨어와 디지털 매니페스토는 병원 그룹에 있어 중요한 구매 기준이 되고 있습니다.

스텔리사이클의 네바다 공장이 2024년에 보여준 것처럼, 차세대 시설에서는 배기가스 스크러버, 에너지 회수 터빈, AI를 활용한 원료 제어가 필요하며, 프로젝트 예산은 1억 달러가 넘을 수 있습니다. 운전비용은 숙련공의 할증임금과 지속적인 배출가스 모니터링으로 인해 더욱 상승합니다. 따라서 소규모 발전사업자는 제3의 전문업체에 위탁하고 있으며, 이들 업체는 노후화된 설비를 일몰시키는 허가증으로 업그레이드에 필요한 자금을 조달해야 합니다. 투자 부담을 분산하기 위해 리스 컨소시엄이나 그린본드를 통한 자금 조달이 부상하고 있지만, 금리 변동으로 인해 수익률이 낮은 지역에서는 도입이 늦어질 수 있습니다.

보고서에서 분석된 기타 촉진 및 억제요인은 다음과 같습니다.

유해 폐기물의 물량 점유율은 17.44%에 불과하지만, 높은 가격 책정, 7.75%의 연평균 복합 성장률(CAGR)을 나타내고, 의료 폐기물 관리 시장의 핵심 수익 동력이 되고 있습니다. 의약품, 화학요법, 방사성 폐기물의 경우 분자 수준의 파괴, 안전한 운송, 장기적인 기록관리가 필요하기 때문에 소규모 운송업체는 거의 돌파할 수 없는 장벽이 있습니다. 반대로 비유해 폐기물의 흐름은 대량 처리와 표준화된 멸균 방법으로 82.56%의 점유율을 유지하고 있습니다. 이러한 패턴을 종합하면, 미래의 승자는 일상적인 수집에서 규모를 활용하면서 카테고리별 차별화를 마스터하게 될 것입니다.

감염 및 병리학적인 하위 스트림은 여전히 가장 큰 위험 조각으로, 소각 또는 고압 증기 오토클레이브 사이클이 필요합니다. 원격 의료가 확대됨에 따라 샤프의 양이 급증하고, 역물류 네트워크와 무단개봉 방지 메일백 키트가 필요하게 될 것입니다. 화학물질과 세포독의 폐기는 정확한 적합성 프로파일에 의존하고 있으며, 실험실급 분류 소프트웨어의 채택을 촉진하고 있습니다. 방사성 동위원소 붕괴 저장은 저장 시간을 연장하고 연간 처리량을 줄이면서도 높은 마진을 제공합니다. 풀스펙트럼 핸들링을 제공하는 사업자는 고객 집착도를 높이고, 감사 서비스 및 교육에서 교차 판매 기회를 창출할 수 있습니다.

열 방식은 현재 매출의 59.83%를 차지하고 있으며, 검증된 소각로 용량과 업그레이드된 오토클레이브 제품군이 의료폐기물 관리 시장을 뒷받침하고 있습니다. 에너지 회수 개보수는 순 연료 사용량을 10-12% 절감하여 ESG 목표에 부합하고, 화석연료 가격 변동에도 불구하고 운영비용을 안정적으로 유지하고 있습니다. 재에서 폴리머와 금속을 재생하면 폐기물 흐름을 더욱 수익화할 수 있습니다. 그러나 마이크로파, 플라즈마, 산화 증기 시스템은 빠르게 규모를 확장하여 병원을 더 작은 환경 발자국을 가진 마이크로 처리 허브로 바꾸고 있습니다.

전자 레인지 장비는 5분 이내에 6-log 감소를 달성할 수 있으며, 공간 제약이 있는 진료소에 적합합니다. 플라즈마 가스화는 염소 시약을 사용하지 않고 화학독소를 중화합니다. 국내에서 개발된 고온증기 시스템은 국내 의료폐기물의 30%를 처리하고, 전국에 도입될 경우 연간 5,400만 달러의 비용을 절감할 수 있습니다. 경쟁사와의 차별화는 기술 구성, 원격 모니터링, 실시간 원료 데이터에 맞춘 가공 레시피에 점점 더 의존하고 있습니다.

의료폐기물 관리 시장 보고서는 폐기물 유형(비유해 폐기물 등), 처리 기술(열, 화학 및 생물학적 등), 서비스 유형(수집, 운송, 보관 등), 처리 장소, 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)으로 업계를 분류하고 있습니다. 시장 예측은 금액(USD)으로 제공됩니다.

북미는 2024년 매출 점유율 39.86%를 차지하며 규제와 기술의 벤치마크가 되었습니다. 연방 규정은 전자 매니페스토를 의무화하고 있으며, 상호 운용 가능한 컴플라이언스 플랫폼에 대한 IT 투자를 촉진하고 있습니다. 여러 주에 걸쳐 있는 대규모 병원 체인은 그 규모를 활용하여 플라스틱 재활용 및 에너지 회수 기술을 기타 국가보다 더 빨리 도입하고 있습니다. 웨이스트 매니지먼트의 스테리사이클 인수에 따른 통합으로 일반 폐기물과 규제 폐기물의 흐름을 아우르는 통합 서비스가 제공되며, 장비 임대 협상에서 조달력을 확보할 수 있게 되었습니다.

아시아태평양의 의료폐기물 관리 시장은 병원 건설, 보편적 의료보험 도입, 규제 강화에 힘입어 연평균 7.18% 성장할 것으로 예측됩니다. 중국의 '폐기물 제로 도시' 시범사업은 치료 인프라를 공유하는 지자체와 병원의 파트너십의 선구자 역할을 합니다. 일본의 밀집된 도시지역은 소각처리에 의존하고 있지만, 재활용 의무화로 인해 플라스틱의 분리수거와 화학적 해중합법 도입이 진행될 것으로 보입니다. 기술 선택의 유연성 및 현지 언어 직원 인증은 다국적 제공업체에게 우위를 제공합니다.

유럽은 지속가능성의 문턱을 계속 높이는 조화로운 법적 프레임워크를 따르고 있습니다. 2026년에 예정된 확대된 생산자책임제도는 재활용이 불가능한 헬스케어 포장재에 직접 비용을 부과하여 재활용을 위한 설계를 장려하고 재료 회수 서비스에 대한 수요를 증가시킬 것입니다. 배출량 규제는 소각로의 이익 폭을 좁히고, 특히 허가 경로가 짧은 소규모 미국 회원국의 경우 마이크로파 및 플라즈마 장비에 대한 투자에 박차를 가합니다.

중동 및 아프리카는 걸프협력회의 국가들의 높은 1인당 의료비 지출과 사하라 사막 이남 아프리카의 인프라 구축 증가를 동시에 가지고 있습니다. 인구 증가와 감염병 확산으로 폐기물 발생량이 가속화되고 있지만, 규제 가이드라인이 늦어지고 있어 턴키 솔루션의 공백이 발생하고 있습니다. 남미에서는 브라질과 칠레가 분산형 오토클레이브 네트워크를 시범적으로 도입하는 등 환율 변동에도 불구하고 병원 현대화 투자가 견조하게 진행되고 있습니다. 이러한 신흥 지역 전체에서 기부자가 자금을 지원하는 그린병원 이니셔티브는 ESG 보고와 현지 기술 이전을 중시하는 의료기관에 대한 진입장벽을 마련하고 있습니다.

The Medical Waste Management Market size is estimated at USD 18.45 billion in 2025, and is expected to reach USD 24.71 billion by 2030, at a CAGR of 6.01% during the forecast period (2025-2030).

Rapid growth stems from post-pandemic capacity building, wider tele-health adoption, and stricter multi-region regulations that raise the technical bar for safe disposal. Thermal treatment retains a leadership position, yet on-site modular systems, data-driven segregation, and circular-economy recovery services are scaling quickly across hospitals, clinics, and home-care channels. Service providers that blend compliance expertise with automation and emissions-cutting technologies are capturing premium contracts as payers and regulators tie reimbursement to environmental performance. At the same time, global supply constraints for chlorine-based chemicals and shifting incinerator permitting rules compel operators to diversify treatment portfolios and hedge regulatory risk especially in fast-growing Asian and Latin American markets.

Federal, state, and supranational programs are injecting new capital into sustainable waste infrastructure. The U.S. EPA awarded USD 58 million in 2024 under its Solid Waste Infrastructure for Recycling Grants, earmarking funds for medical waste segregation equipment and disadvantaged-community access. Similarly, the FY 2025 HHS budget requests USD 1.1 billion for environmental health initiatives that indirectly finance facility tracking and audit systems. These injections accelerate equipment upgrades, spur local treatment pilots, and prioritize vendors able to document emissions cuts and equitable service access. Providers that align proposals with environmental justice metrics and verifiable community health outcomes gain preferred-supplier status across public tenders.

The care continuum is widening as home infusions, self-injectables, and remote diagnostics proliferate, placing regulated sharps and infectious waste in residential streams that municipal haulers are ill-equipped to manage. Health networks now juggle decentralized pick-ups, patient-education initiatives, and supply-chain redesigns for safe retrieval. Vendors offering subscription-based sharps mail-backs, IoT-enabled fill-level sensors, and tamper-proof containers are scaling quickly, especially in congested urban corridors where multi-unit dwellings complicate segregation. The distributed waste model also magnifies liability exposure, making traceability software and digital manifests a critical purchase criterion for hospital groups.

Next-generation facilities require flue-gas scrubbers, energy-recovery turbines, and AI-driven feedstock controls that can push project budgets past USD 100 million, as Stericycle's Nevada plant illustrated in 2024. Operating costs climb further with skilled-labor premiums and continuous emissions monitoring. Smaller generators therefore outsource to third-party specialists, but those providers still must finance upgrades as permits sunset older units. Leasing consortia and green-bond financing are emerging to spread the investment burden, yet interest-rate volatility may slow deployments in lower-margin geographies.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hazardous waste captures a modest 17.44% volume share yet commands higher pricing and posts a 7.75% CAGR, making it the core profit engine of the medical waste management market. Pharmaceutical, chemotherapy, and radioactive categories require molecular-level destruction, secure transport, and long-term recordkeeping, creating barriers small haulers rarely breach. Conversely, non-hazardous streams maintain the bulk 82.56% share through high procedure volumes and standardized sterilization practices. Combined, these patterns signal that future winners will master categorical differentiation while leveraging scale in routine collections.

Infectious and pathological sub-streams remain the largest hazardous slice, demanding incineration or high-pressure steam autoclave cycles. Sharps volumes balloon as tele-health expands, necessitating reverse-logistics networks and tamper-proof mail-back kits. Chemical and cytotoxic disposals hinge on precise compatibility profiles, driving adoption of lab-grade segregation software. Radioactive isotope decay storage extends holding times, reducing annual throughput yet offering premium margins. Operators that offer full-spectrum handling deepen client stickiness and unlock cross-selling opportunities in audit services and training.

Thermal methods account for 59.83% revenue today, anchoring the medical waste management market via proven incinerator capacity and upgraded autoclave fleets. Energy-recovery retrofits are cutting net fuel use 10-12%, aligning with ESG goals and stabilizing operating costs as fossil-fuel prices fluctuate. Polymer and metals reclamation from ash further monetize waste streams. However, microwave, plasma, and oxidative-steam systems are scaling rapidly, turning hospitals into micro-treatment hubs with smaller environmental footprints.

Microwave units achieve 6-log reductions within five minutes and suit space-constrained clinics. Plasma gasification neutralizes chemical toxins without chlorine reagents, appealing where chemical shortages or emissions caps bite hardest. High-temperature steam systems developed in Korea process 30% of national medical waste, promising USD 54 million in annual savings if adopted nationwide. Competitive differentiation increasingly hinges on technology mix, remote monitoring, and adaptive processing recipes tuned to real-time feedstock data.

The Medical Waste Management Market Report Segments the Industry Into by Waste Type (Non-Hazardous Waste and More), Treatment Technology (Thermal, Chemical and Biological, and More), Service Type (Collection, Transportation, and Storage, and More), Treatment Site, and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America, with a 39.86% revenue share in 2024, remains the benchmark for regulation and technology. Federal rules now require e-manifests, driving IT spend on interoperable compliance platforms. Large multistate hospital chains leverage scale to adopt plastics recycling and energy-recovery technologies faster than peers elsewhere. Consolidation following Waste Management's acquisition of Stericycle produces integrated offerings spanning municipal and regulated waste streams and creates procurement clout when negotiating equipment leases.

The Asia-Pacific medical waste management market is forecast to grow 7.18% annually, fueled by hospital construction, universal health-coverage rollouts, and tightening rules. China's Zero-Waste City pilots pioneer municipal-hospital partnerships that share treatment infrastructure, while India's under-segregation rates invite foreign expertise packaged with robust training and digital tracking. Japan's dense urban clusters rely on incineration, yet recycling mandates will push adoption of plastics sorting and chemical depolymerization. Flexibility in technology choice and local-language staff certification give multinational providers an edge.

Europe follows a harmonized legal framework that continues to elevate sustainability thresholds. Extended Producer Responsibility schemes coming in 2026 place direct cost on non-recyclable healthcare packaging, incentivizing design-for-recycling and boosting demand for material recovery services. Emissions caps narrow incinerator margins, spurring investment in microwave and plasma units, especially in smaller EU member states where permitting pathways are shorter.

Middle East & Africa combine high per-capita healthcare spending in Gulf Cooperation Council states with rising infrastructure builds in Sub-Saharan Africa. Population growth and infectious-disease burdens accelerate waste volumes, yet regulatory guidelines lag, creating white-space for turnkey solutions. South America witnesses resilient investment in hospital modernization amid currency volatility, with Brazil and Chile piloting decentralized autoclave networks. Across these emerging regions, donor-funded green-hospital initiatives create entry doors for providers that emphasize ESG reporting and local-skills transfer.