인도의 전기자동차용 전지 제조 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

India Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636466

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

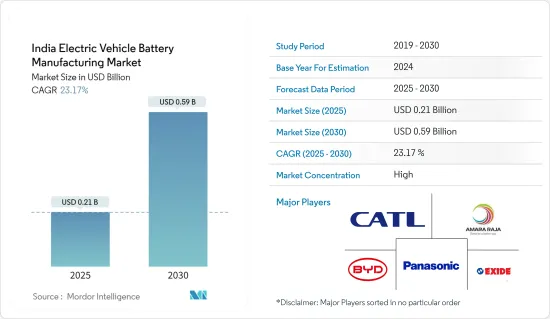

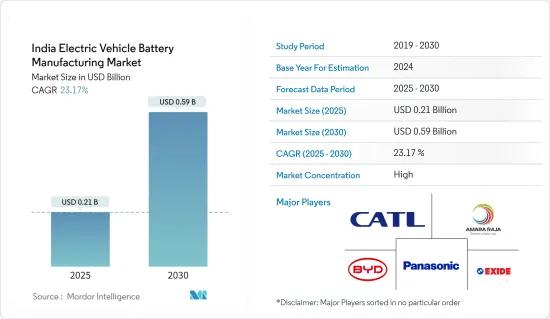

인도 전기자동차 전지 제조 시장 규모는 2025년 2억 1,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 23.17%로, 2030년에는 5억 9,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

장기적으로는 전지 생산 능력 강화를 위한 투자나 전지 원료 비용의 저하 등의 요인이 예측 기간 동안 인도의 전기자동차용 전지 제조 시장의 가장 큰 촉진요인 중 하나가 될 것으로 예상됩니다.

반면 원료 공급망과 관련된 문제는 예측 기간 동안 시장 성장을 방해할 것으로 예상됩니다.

전기자동차 분야의 장기적인 목표는 향후 시장에 기회를 가져올 것으로 기대됩니다.

인도 전기자동차 전지 제조 시장 동향

리튬 이온 전지 유형이 시장을 독점

인도의 전기자동차(EV)용 전지 제조 시장은 주로 리튬 이온(Li-ion) 전지의 우위성에 의해 대폭적인 성장이 전망되고 있습니다. 리튬 이온 전지는 에너지 밀도가 높고 수명이 길며 성능이 높은 것으로 알려져 있어 신뢰성이 높고 효율적인 자동차를 제공하는 데 중점을 둔 EV 제조업체에게 최적의 선택이 되고 있습니다.

EV의 보급을 촉진하고 EV용 전지의 현지 생산을 활성화하기 위해 인도 정부는 일련의 이니셔티브를 시행하고 있습니다. 하이브리드 자동차 및 전기자동차의 신속한 도입 및 제조(FAME) 체계는 EV 제조업체와 구매자 모두에게 금전적 인센티브를 제공합니다. 이를 보완하는 PLI(Production Linked Incentive) 체계는 첨단 화학 셀(ACC) 축전지를 대상으로 하고 있으며, 자국 내에서 견고한 제조 생태계를 육성하는 것을 목표로 하고 있습니다.

인도의 EV 추진은 이산화탄소 배출을 억제하고 지속 가능한 에너지를 도입하는 보다 광범위한 노력과 발을 맞추고 있습니다. 정부의 엄격한 배출규제와 시책은 내연기관에서 전기차로의 전환을 유도하고 있습니다. 세계 최대의 잠재적 EV 시장인 인도에서는 도시화, 연료 가격 상승, 환경 의식 증가 등을 배경으로 EV 수요가 급증하고 있습니다. 이러한 수요 증가는 자국산 전지의 필요성을 강조하고 시장을 성장시킵니다.

2024년 7월 축전지 대기업인 Exide Industries는 벵갈루루에 건설 중인 대규모 12기가와트급 리튬 이온 전지 제조 공장의 첫 단계가 회계 연도 말까지 완성될 예정이라고 발표했습니다. 한편, 콜카타에 본사를 둔 Exide의 자회사인 Exide Energy Solutions(EESL)는 리튬 이온 전지 제조 프로젝트의 막바지에 다다르고 있습니다. EESL은 인도 EV 시장의 급속한 확대를 인식하고, 자동차 대기업 현대 자동차 및 기아 자동차와 양해각서(MOU)를 체결하여 전략적 협력 관계를 맺고 있습니다.

EV의 보급을 촉진하기 위해 전국적인 충전 인프라 개발에 대규모 투자가 이루어지고 있습니다. 급증하는 인프라는 전기자동차의 보급을 지원할 뿐만 아니라 자국산 전지 수요를 높입니다. 인도 기업은 R&D 투자를 확대하고 있으며 전지 기술의 개선과 비용 절감을 목표로 하고 있습니다. 국제 기술 공급자 및 연구 기관과의 제휴는 전지 제조에서 혁신의 기폭제가 되고 있습니다.

2024년 7월 LICO는 벵갈루루에 최첨단 시설을 건설하여 인도 최대 규모의 리튬 이온 전지 재활용 공장으로 사업을 확대할 것을 발표했습니다. 2024년 10월까지 운영을 시작하는 LICO의 시설은 2026년까지 연간 2만 5,000톤의 처리 능력을 목표로 하고 있습니다. 전략적으로는 운송 리스크와 비용을 줄이기 위해 허브 앤 스포크형 조업 모델을 채택하여 지역적 처리를 중시합니다. EV의 보급이 가속화되고 있는 가운데, 인도는 사용 전지를 효율적으로 관리하고 미래를 대비한 인프라를 확보하기 위한 준비를 진행하고 있습니다.

인도의 리튬 이온 전지(LiB) 제조 분야는 상승 기조에 있으며, 대기업은 급성장하는 EV 시장에 대응하기 위해 새로운 설비에 전략적 투자를 하고 있습니다. PLI 체계 하에서 Ola Electric, Reliance, Rajesh Export와 같은 선도 기업은 셀 제조를 위한 우대 정책을 보장받아 2024년 생산을 예정하고 있습니다. 게다가 많은 기업들이 LiB 전지 공장을 계획적으로 확대하고 국내외 시장에 대응할 수 있는 체제를 정비하고 있습니다.

이러한 개발로 동지역은 EV용 전지의 생산이 급증하고 이에 따라 리튬 이온 전지 수요도 향후 수년간 증가할 전망입니다.

전지 생산 능력 증대를 위한 투자

인도에서는 전기자동차(EV) 수요 급증에 대응하기 위해 전지 제조능력을 높이고 있습니다. 첨단화학전지(ACC) 축전지의 생산연계 인센티브(PLI) 제도와 같은 대처를 통해 정부는 투자를 유치하여 현지 생산을 강화하려고 하고 있습니다. 이러한 전략적 움직임은 수입 의존성을 억제하고 견고한 자국 내 전지 제조 환경을 육성하는 데 매우 중요합니다.

급성장하는 EV 시장에 대응하기 위해 새로운 전지 생산 공장이 인도 전역에 세워지고 있으며 Exide Industries, Amara Raja, Tata Chemicals와 같은 산업 선도 업체들은 최첨단 장비에 대한 투자를 추진하고 있습니다. 이 공장은 내수를 충족하고, 혁신을 촉진하며, 고용을 창출하는데 중요한 역할을 하고 있으며, 인도 EV 전지 제조 부문의 성장을 뒷받침하고 있습니다.

전지 제조의 야망을 강화하기 위해 인도는 최고급 리튬 이온 전지 제조에 필수적인 슬러리 믹서를 포함한 고급 설비 입찰을 실시했습니다. 이러한 입찰은 효율성과 생산량을 향상시키는 최첨단 기술을 대상으로 합니다. 인도는 제조 공정을 현대화함으로써 EV용 전지 생산 경쟁 벤치마킹 및 품질 향상을 달성하고 세계적 수준에 맞추는 것을 목표로 하고 있습니다.

예를 들어, 2024년 7월에는 전동 이륜차와 스마트 모빌리티 부문에서 유명한 대만 Ahamani EV Technology가 인도의 EV 시장에 많은 투자를 할 예정입니다. 동사는 인도에 메가와트 규모의 전지 제조 유닛을 설립할 계획으로 인도의 주요 자동차 관련 기업과 전략적 기술 이전 제휴를 모색하고 있으며 이미 3-4사의 대기업 EV 기업과 협상을 진행하고 있습니다. 정부의 지원 시책과 환경 친화적인 수송 수단에 대한 소비자 수요의 급증에 의해 인도에서는 전기 이동성이 중시되고 있습니다. 현지에 건설 예정인 전지 시설은 EV 밸류 체인에서 인도의 자급률 향상을 목표로 할 뿐만 아니라 고용 창출과 경제 활성화를 보장합니다.

인도 정부는 세금 혜택, 제조업체 및 소비자 보조금, 충전 인프라 투자 등 다양한 이니셔티브를 통해 EV 부문을 적극적으로 지원하고 있습니다. 이러한 조치는 EV의 구매 편의성과 편의성을 향상시키고, 보급률을 높이고, 나아가서는 전지 재료 수요 상승을 목적으로 하고 있습니다. 전지 기술의 혁신도 시장 역학에 영향을 미치고 있습니다. 예를 들어, BYD는 인산철 리튬(LFP) 전지와 같은 기존의 리튬 이온 전지에 비해 에너지 밀도는 약간 낮지만 안전하고 비용 효율적인 새로운 전지화학 분야를 개척하고 있으며, 이러한 돌파구는 EV를 더 많은 사람들이 이용하는 데 중요한 역할을 합니다.

2024년 8월, Amara Raja Advanced Cell Technologies(ARACT)는 인도에서 EV 기술을 추진하기 위해 Piaggio Vehicles Private Limited와 각서를 체결하였습니다. 이 제휴는 Piaggio의 전동 삼륜차와 향후 출시될 이륜차에 맞춘 리튬 이온 셀, 전지 팩, 충전기의 제조 및 공급을 중심으로 이루어집니다.

인도는 세계 동향에 맞추어 2029년까지 전기자동차(EV)의 야심찬 판매 목표를 내걸고 있습니다. 인도 정부는 EV에 대한 요구를 높이기 위해 자국 내 생산, 특히 전지 생산을 중시하고 있습니다. '30@30' 구상 및 기타 예측에 따르면 인도에서는 2023년에 42.5GWh의 누적 전지용량이 필요하며, 2029년에는 577.8GWh로 급증할 전망입니다. 이러한 급증은 인도의 연간 전지 필요량이 전 세계 생산량의 17%에서 26%를 차지할 수 있음을 의미합니다. 또한 이러한 수요에 부응할 뿐만 아니라 비용을 낮추고 EV 시장 경쟁을 높이기 위해서는 생산 확대가 필수적입니다. 확고한 자국 내 생산 기반을 확립하는 것은 일본에게 큰 경제적 이점을 가져다줍니다.

결론적으로 이러한 노력과 투자는 인도의 전지 생산 능력을 크게 향상시킬 것입니다.

인도 전기자동차 전지 제조 산업 개요

인도 전기자동차 전지 제조 시장은 어느정도 집중되어 있습니다. 동시장의 주요 기업(순서부동)에는 BYD, Contemporary Amperex Technology Co.Ltd., Panasonic Corporation, Exide Industries, Amara Raja Batteries Ltd. 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

서문

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

촉진요인

전지 생산 능력 향상을 위한 투자

전지 원료 비용 저하

억제요인

원료 매장량 부족

공급망 분석

PESTLE 분석

투자 분석

제5장 시장 세분화

전지

리튬 이온

납축전지

니켈 수소 전지

기타

전지 형태

각형

파우치형

원통형

차량

승용차

상용차

기타

추진

전지 전기자동차

하이브리드 전기자동차

플러그인 하이브리드 전기자동차

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 개요

BYD Co. Ltd

Contemporary Amperex Technology Co. Limited

EnerSys

GS Yuasa Corporation

LG Chem Ltd

Exide Industries

Panasonic Corporation

Amara Raja Batteries Ltd.

Tata Chemicals

HBL Power Systems Ltd.

기타 유력 기업 목록

시장 순위 분석

제7장 시장 기회와 앞으로의 동향

전기차 장기 목표

CSM

영문 목차

영문목차

The India Electric Vehicle Battery Manufacturing Market size is estimated at USD 0.21 billion in 2025, and is expected to reach USD 0.59 billion by 2030, at a CAGR of 23.17% during the forecast period (2025-2030).

Key Highlights

Over the long term, factors such as Investments to enhance battery production capacity and the decline in the cost of battery raw materials are expected to be among the most significant drivers for the India Electric Vehicle Battery Manufacturing Market during the forecast period.

On the other hand, challenges associated with the raw material supply chain are expected to hinder market growth during the forecast period.

Nevertheless, long-term ambitious targets for electric vehicles are expected to create opportunities for the market in the future.

India Electric Vehicle Battery Manufacturing Market Trends

Lithium-ion Battery Type to Dominate the Market

India's electric vehicle (EV) battery manufacturing market is set for substantial growth, primarily fueled by the supremacy of lithium-ion (Li-ion) batteries. Li-ion batteries, known for their superior energy density, extended life cycles, and enhanced performance, have become the go-to choice for EV manufacturers focused on delivering reliable and efficient vehicles.

To bolster EV adoption and stimulate local EV battery manufacturing, the Indian government has rolled out a series of initiatives. The Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme offers financial incentives to both EV manufacturers and buyers. Complementing this, the Production Linked Incentive (PLI) scheme targets advanced chemistry cell (ACC) battery storage, aiming to cultivate a robust manufacturing ecosystem within the country.

India's push for EVs resonates with its broader commitment to curbing carbon emissions and embracing sustainable energy. The government's stringent emission norms and policies advocate a transition from internal combustion engines to electric vehicles. As the world's largest potential EV market, India's demand for EVs is surging, driven by urbanization, escalating fuel prices, and heightened environmental consciousness. This burgeoning demand underscores the necessity for domestically produced batteries, propelling the market forward.

In July 2024, Exide Industries, a leading storage battery firm, announced that the first phase of its ambitious 12-gigawatt lithium-ion cell manufacturing plant in Bengaluru is on track for completion by the financial year's end. Meanwhile, Exide's Kolkata-based subsidiary, Exide Energy Solutions (EESL), is nearing the finish line with its lithium-ion cell manufacturing project. Recognizing the rapid expansion of India's EV market, EESL has inked a non-binding memorandum of understanding (MOU) with automotive giants Hyundai Motor and Kia Corporation, signaling a strategic collaboration.

Massive investments are being funneled into the development of charging infrastructure nationwide, a move that bolsters EV adoption. This burgeoning infrastructure not only supports the widespread use of electric vehicles but also amplifies the demand for locally produced batteries. Indian firms are ramping up investments in research and development, aiming to refine battery technologies and curtail costs. Collaborations with international tech providers and research institutions are catalyzing innovations in battery manufacturing.

In July 2024, LICO announced its operational expansion with a state-of-the-art facility in Bangalore, poised to be one of India's largest lithium-ion battery recyclers. Set to commence operations by October 2024, LICO's facility aims for an ambitious processing capacity of 25,000 tonnes annually by 2026. Strategically, the plant will emphasize regional processing to mitigate transportation risks and costs, adopting a hub-and-spoke operational model. As EV adoption accelerates, India is gearing up to efficiently manage end-of-life batteries, ensuring a future-ready infrastructure.

India's Lithium-ion Battery (LiB) manufacturing sector is on an upward trajectory, with major players making strategic investments in new facilities to cater to the burgeoning EV market. Under the PLI scheme, industry stalwarts like Ola Electric, Reliance, and Rajesh Export have secured incentives for cell manufacturing, with production slated for 2024. In addition, numerous companies are methodically scaling up their LiB battery plants, positioning themselves to cater to both domestic and international markets.

Given these developments, the region is poised for a surge in EV battery production, with a corresponding uptick in demand for lithium-ion batteries in the coming years.

Investments to Enhance the Battery Production Capacity

India is ramping up its battery manufacturing capabilities to satisfy the surging demand for electric vehicles (EVs). Through initiatives like the Production Linked Incentive (PLI) scheme for advanced chemistry cell (ACC) battery storage, the government seeks to draw in investments and bolster local production. This strategic move is pivotal for curbing import reliance and nurturing a robust domestic battery manufacturing landscape.

New battery production plants are emerging across India, catering to the burgeoning EV market. Industry giants such as Exide Industries, Amara Raja, and Tata Chemicals are channeling investments into cutting-edge facilities. These plants play a crucial role in satiating domestic demand, spurring innovation, and generating employment, thus propelling the growth of India's EV battery manufacturing sector.

To bolster its battery manufacturing ambitions, India is issuing tenders for advanced equipment, including slurry mixers, vital for producing top-tier lithium-ion batteries. These tenders target state-of-the-art technology to boost efficiency and output. By modernizing its manufacturing processes, India aims to elevate the competitiveness and quality of its EV battery production, aligning it with global benchmarks.

For example, in July 2024, Ahamani EV Technology Co., Ltd., a prominent Taiwanese player in electric two-wheelers and smart mobility, is set to make a substantial investment in India's EV landscape. The firm plans to set up a megawatt-scale battery manufacturing unit in India and is on the lookout for strategic technology transfer collaborations with major Indian automotive entities. Talks are already in progress with 3-4 leading EV firms. Given India's heightened emphasis on electric mobility, bolstered by supportive government policies and a surge in consumer demand for eco-friendly transport, Ahamani sees a golden opportunity. The envisioned local battery facility not only aims to bolster India's self-sufficiency in the EV value chain but also promises job creation and economic stimulation.

India's government is actively backing the EV sector through a range of initiatives, including tax breaks, subsidies for manufacturers and consumers alike, and investments in charging infrastructure. These measures aim to enhance the affordability and convenience of EVs, driving up adoption rates and, in turn, boosting the demand for battery materials. Battery technology innovations are also influencing the market dynamics. For instance, BYD is pioneering new battery chemistries, like lithium iron phosphate (LFP) batteries, which, while being safer and more cost-effective, have a marginally lower energy density compared to conventional lithium-ion batteries. Such breakthroughs are instrumental in making EVs more accessible to the broader public.

In August 2024, Amara Raja Advanced Cell Technologies (ARACT) inked a Memorandum of Understanding (MoU) with Piaggio Vehicles Private Limited, aiming to propel EV technology in India. This collaboration centers on crafting and supplying lithium-ion cells, battery packs, and chargers tailored for Piaggio's electric three-wheelers and upcoming two-wheelers.

India is setting its sights on ambitious electric vehicle (EV) sales targets by 2029, in line with global trends. The government is emphasizing domestic manufacturing, especially in battery production, to fuel India's EV aspirations. Under the "30@30" initiative and other bold projections, India needed a cumulative battery capacity of 42.5 GWh in 2023, with expectations to skyrocket to 577.8 GWh by 2029. This surge means India's annual battery requirements could represent 17% to 26% of global production. Moreover, ramping up production is crucial not only to meet these demands but also to drive down costs, enhancing the market competitiveness of EVs. Establishing a solid domestic manufacturing foundation promises substantial economic advantages for the country.

In conclusion, these initiatives and investments are set to significantly bolster India's battery production capabilities.

India Electric Vehicle Battery Manufacturing Industry Overview

The India Electric Vehicle Battery Manufacturing Market is semi-concentrated. Some of the key players in this market (in no particular order) are BYD Co. Ltd., Contemporary Amperex Technology Co. Limited, Panasonic Corporation, Exide Industries, and Amara Raja Batteries Ltd.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Investments to Enhance the battery production capacity

4.5.1.2 Decline in cost of battery raw materials

4.5.2 Restraints

4.5.2.1 Lack of Raw Material Reserves

4.6 Supply Chain Analysis

4.7 PESTLE ANALYSIS

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery

5.1.1 Lithium-ion

5.1.2 Lead-Acid

5.1.3 Nickel Metal Hydride Battery

5.1.4 Others

5.2 Battery Form

5.2.1 Prismatic

5.2.2 Pouch

5.2.3 Cylindrical

5.3 Vehicle

5.3.1 Passenger Cars

5.3.2 Commercial Vehicles

5.3.3 Others

5.4 Propulsion

5.4.1 Battery Electric Vehicle

5.4.2 Hybrid Electric Vehicle

5.4.3 Plug-in Hybrid Electric Vehicle

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 BYD Co. Ltd

6.3.2 Contemporary Amperex Technology Co. Limited

6.3.3 EnerSys

6.3.4 GS Yuasa Corporation

6.3.5 LG Chem Ltd

6.3.6 Exide Industries

6.3.7 Panasonic Corporation

6.3.8 Amara Raja Batteries Ltd.

6.3.9 Tata Chemicals

6.3.10 HBL Power Systems Ltd.

6.4 List of Other Prominent Companies

6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Long-term ambitious targets for electric vehicles