남미의 전기자동차용 전지 제조 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

South America Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636473

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

남미의 전기자동차용 전지 제조 시장 규모는 2025년에 59만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 16.25%로, 2030년에는 126만 달러에 이를 것으로 예측됩니다.

주요 하이라이트

중기적으로는 동지역의 전기자동차 보급 확대와 풍부한 원료 등의 요인이 예측 기간 중 남미의 전기자동차 전지 제조시장의 가장 중요한 촉진요인 중 하나가 될 것으로 예상됩니다.

반면 아시아태평양과 같은 기존 전지 시장과의 경쟁은 예측 기간 동안 남미의 전기자동차 전지 제조 시장에 위협이 될 것입니다.

남미 국가 간의 협력 관계와 파트너십을 구축하기 위한 지속적인 노력은 향후 시장에 여러 기회를 창출할 것으로 예상됩니다.

브라질은 전지 제조 확립을 위한 정부의 이니셔티브가 활발해지고 있으며 전기자동차의 보급이 진행되고 있기 때문에 시장을 독점하고 예측 기간 동안 가장 높은 성장을 기록할 것으로 예상됩니다.

남미의 전기자동차 전지 제조 시장 동향

리튬 이온 전지가 현저한 성장을 이루

리튬 이온 전지 부문은 남미의 전기자동차(EV)용 전지 제조 시장의 핵심이며 동지역의 풍부한 천연 자원, 진화하는 산업 능력, 지속가능성에 대한 노력 증가가 그 원동력이 되고 있습니다. 남미에는 브라질, 칠레, 아르헨티나를 포함한 '리튬 트라이앵글'이 있으며 이들 국가들은 세계의 리튬 매장량의 대부분을 차지하고 있습니다.

예를 들어, Energy Institute Statistical Review of World Energy는 2023년 남미의 리튬 매장량이 7만 1,030톤을 초과한다고 보고했습니다. 이는 2022년 대비 22.82%의 대폭적인 성장으로, 남미는 세계적으로 가장 급성장하고 있는 지역 중 하나로 자리잡고 있습니다. 또다른 주목할 점은 2018-2023년에 걸쳐, 남미는 38.1% 이상의 CAGR을 자랑해 동지역의 리튬 매장량과 생산 능력 향상을 뒷받침하고 있다는 점입니다.

이 전략적 이점을 통해 동지역은 세계 리튬 이온 전지 공급망에서 중요한 진출기업으로 자리매김하고 있습니다. 리튬 이온 전지는 에너지 밀도가 높고 수명이 길며 자가방전율이 상대적으로 낮기 때문에 전기자동차의 전력원으로 매우 중요합니다. 리튬의 추출과 가공은 점점 고도화되고 있으며, 남미 국가들은 추출효율과 환경의 지속가능성을 향상시키는 기술에 투자하고 있습니다. 물의 사용이나 채굴 작업이 환경에 미치는 영향과 같은 과제가 있지만 이러한 문제를 경감하기 위한 그린 광업 기술의 진보가 모색되고 있습니다.

2024년 5월 Rio Tinto, Eramet, LG Energy는 칠레의 살랄레스 알토 안디노스에서 혁신적인 접근법을 제안했습니다. 이 이니셔티브는 단순한 증산에 그치지 않고 리튬 채굴이 환경에 미치는 영향을 재정의하고 선구적인 지속가능성 기준을 확립하기 위한 것입니다.

직접 리튬 추출법(DLE)으로 알려진 이 방법은 전통적인 접근법으로부터의 현저한 도약을 의미합니다. 남미의 리튬이 풍부한 지역의 일반적으로 시간이 소요되고 지형적 특징이 강한 증발못과는 달리 DLE법은 화학적, 물리적, 전기적 프로세스를 이용하여 염수로부터 리튬을 추출합니다. 이는 효율을 높일 뿐만 아니라 환경 파괴를 최소화합니다.

마찬가지로 브라질에서는 원료 추출뿐만 아니라 전지 셀 제조 및 재활용 시설을 포함한 종합적인 전지 제조 생태계 개발을 위한 노력이 진행되고 있어 전지 이용을 중심으로 한 순환 경제가 형성되고 있습니다. 리튬의 매장량이 많은 아르헨티나도 원료 수출에서 부가가치 생산으로의 전환을 목표로 현지에 전지 제조 시설을 설립하기 위한 외국 투자 유치에 주력하고 있습니다.

이러한 개발 상황을 감안하면 리튬 이온 전지 섹터는 향후 수년에 크게 성장할 가능성이 있습니다.

브라질의 시장 독점

브라질은 전략적, 경제적, 기술적 요인이 중첩되어 남미의 전기자동차(EV)용 전지 제조 시장을 독점하는 추세를 보이고 있습니다. 남미 최대의 경제대국인 브라질은 견고한 산업기반과 확립된 자동차산업을 가지고 있으며 이는 전기자동차 전지 제조에 진출하기 위한 견고한 기반이 되고 있습니다.

브라질의 풍부한 천연 자원, 특히 니켈, 코발트, 리튬 등의 광물은 리튬 이온 전지의 생산에 필수적이며 주요 원료의 자국 내 조달에 큰 잠재력을 제공합니다. 브라질의 지리적 위치와 개발된 인프라는 대륙 내 수출입 물류 허브로서의 잠재력을 더욱 높여 효율적인 물자의 이동을 촉진하고 국제 무역 관계를 촉진합니다.

게다가 브라질 정부는 지속 가능한 에너지 솔루션으로의 전환과 이산화탄소 배출량 감소를 위한 확고한 노력을 보여주며, 이는 세계 동향과 일치하며 전기자동차 판매 및 관련 전지 기술에 대한 자국 내 시장 성장 전망을 강화하고 있습니다.

국제에너지기구(IEA)에 따르면 브라질의 전기차 판매량은 2023년 급증하여 1만9,000대에 달했습니다. 이는 2022년부터 123.5% 증가한 현저한 성장세이며, 지난 5년간 판매량이 급증하여 100배 이상의 인상적인 성장을 보이고 있습니다.

브라질 정부는 신재생에너지 개발과 전기자동차 도입에 인센티브를 주는 시책을 적극적으로 추진하고 있으며, 그 결과 자국산 전지 수요를 높이고 있습니다. 감세, 보조금, R&D 투자 등의 이니셔티브는 국내외의 투자를 전지 제조 부문에 유치하기 위한 노력입니다. 이러한 조치는 브라질의 광대한 시장 잠재력과 숙련 노동력 활용을 열망하는 국제 기술 기업과의 제휴에 의해 보완됩니다.

예를 들어 BYD는 2023년 7월 브라질의 포드 공장 유적지에 3개의 생산 시설을 건설할 예정입니다. 하나는 전기자동차 및 하이브리드 자동차 생산용, 하나는 전기 버스 및 트럭 차대용, 세 번째는 전기자동차 전지 시장용 리튬과 인산철을 가공하는 시설입니다. BYD는 브라질 바이어에 있는 카마카리 공업 단지의 부지를 전용으로 사용하기 위해 최대 6억 1,700만 달러를 투입할 준비가 되어 있습니다.

이러한 시나리오는 예측 기간 동안 브라질이 시장을 독점할 것으로 예상합니다.

남미의 전기자동차 전지 제조 산업 개요

남미의 전기자동차 전지 제조 시장은 부분 통합되어 있습니다. 동시장의 주요 기업(순서부동)은 BYD, SK innovation, EnerSys, LG Chem Ltd, Exide Industries입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

서문

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

촉진요인

전기자동차 보급 확대

풍부한 원료

성장 억제요인

기존 시장과의 경쟁

공급망 분석

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협 제품 및 서비스

경쟁 기업간 경쟁 관계

투자 분석

제5장 시장 세분화

전지

리튬 이온

납축전지

니켈 수소 전지

기타

전지 형태

각형

파우치형

원통형

차량

승용차

상용차

기타

추진

전지 전기자동차

하이브리드 전기자동차

플러그인 하이브리드 전기자동차

지역

브라질

아르헨티나

콜롬비아

기타 남미

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 개요

BYD Co. Ltd

SK innovation Co., Ltd.

EnerSys

LG Chem Ltd

Exide Industries

Panasonic Corporation

기타 유력 기업 목록

시장 순위/점유율(%) 분석

제7장 시장 기회와 앞으로의 동향

지역 협업

CSM

영문 목차

영문목차

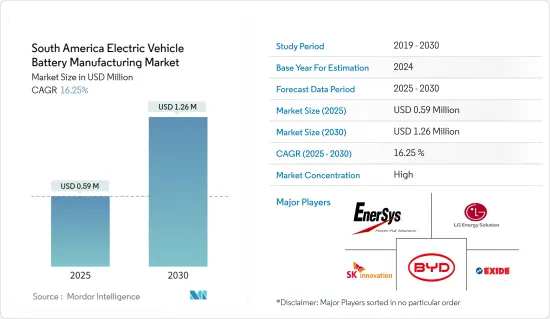

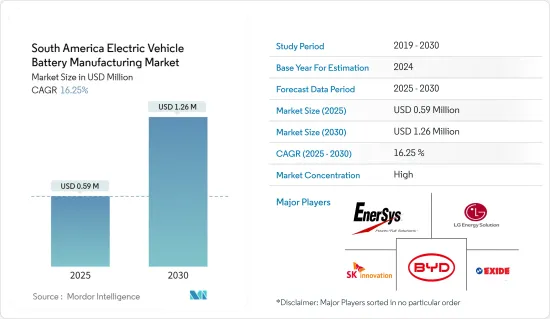

The South America Electric Vehicle Battery Manufacturing Market size is estimated at USD 0.59 million in 2025, and is expected to reach USD 1.26 million by 2030, at a CAGR of 16.25% during the forecast period (2025-2030).

Key Highlights

Over the medium term, factors such as the increasing adoption of electric vehicles in the region coupled with the abundance of raw materials in the region are expected to be among the most significant drivers for the South American electric Vehicle Battery Manufacturing Market during the forecast period.

On the other hand, established battery markets such as Asia Pacific are competing. This poses a threat to the South American electric Vehicle Battery Manufacturing Market during the forecast period.

Nevertheless, continued efforts to create collaborations and partnerships between South American countries are expected to create several opportunities for the market in the future.

Brazil is expected to dominate the market and will likely register the highest growth during the forecast period due to the government's rising efforts to establish battery manufacturing and the growing adoption of electric vehicles.

South America Electric Vehicle Battery Manufacturing Market Trends

Lithium-ion Battery to Witness Significant Growth

The lithium-ion battery segment is a cornerstone of the electric vehicle (EV) battery manufacturing market in South America, driven by the region's abundant natural resources, evolving industrial capabilities, and increasing commitment to sustainability. South America is home to the "Lithium Triangle," encompassing Brazil, Chile, and Argentina, which collectively hold over a significant share of the world's known lithium reserves.

For instance, the Energy Institute Statistical Review of World Energy reported that South America's lithium reserves exceeded 71.03 thousand tonnes of lithium content in 2023. This marked a substantial growth of 22.82% from 2022, positioning it as one of the fastest-growing regions globally. Notably, from 2018 to 2023, South America boasted an impressive annual average growth rate of over 38.1%, underscoring the region's escalating lithium reserves and production capacity.

This strategic advantage positions the region as a vital player in the global supply chain for lithium-ion batteries, which are pivotal in powering electric vehicles due to their high energy density, long cycle life, and relatively low self-discharge rates. The extraction and processing of lithium have become increasingly sophisticated, with South American countries investing in technology to improve extraction efficiency and environmental sustainability. Despite challenges such as water usage and the environmental impact of mining operations, advancements in green mining techniques are being explored to mitigate these issues.

In May 2024, Rio Tinto, Eramet, and LG Energy proposed an innovative approach in Chile's Salares Altoandinos: a new lithium extraction technology. This initiative goes beyond mere production increases; it aims to redefine lithium mining's environmental impact, establishing pioneering sustainability benchmarks.

Known as Direct Lithium Extraction (DLE), this method marks a notable leap from conventional practices. Unlike the slow and landscape-dominating evaporation ponds typical in South America's lithium-rich areas, DLE methods employ chemical, physical, or electrical processes to extract lithium from brine. This not only enhances efficiency but also minimizes environmental disturbances.

Similarly, in Brazil, initiatives are underway to develop a comprehensive battery manufacturing ecosystem that includes not only raw material extraction but also the production of battery cells and recycling facilities, thus creating a circular economy around battery use. Argentina, with its significant lithium reserves, is also focusing on attracting foreign investment to establish local battery manufacturing facilities, aiming to move beyond raw material exportation to value-added production.

Given these developments, the lithium-ion battery sector is poised for significant growth in the coming years.

Brazil to Dominate the Market

Brazil is poised to dominate the South American electric vehicle (EV) battery manufacturing market due to a confluence of strategic, economic, and technological factors that favor its development as a regional powerhouse in this burgeoning sector. As the largest economy in South America, Brazil offers a robust industrial base and a well-established automotive industry, which collectively provide a solid foundation for expanding into electric vehicle battery manufacturing.

Brazil's extensive natural resources, particularly minerals such as nickel, cobalt, and lithium, are crucial for lithium-ion battery production and offer significant potential for domestic sourcing of critical raw materials. Brazil's geographical location and developed infrastructure further enhance its potential as a logistical hub for both import and export within the continent, facilitating the efficient movement of goods and fostering international trade relationships.

In addition, Brazil's government has demonstrated a solid commitment to transitioning toward sustainable energy solutions and reducing carbon emissions, aligning with global trends and reinforcing the domestic market's growth prospects for electric vehicle sales and related battery technologies.

According to the International Energy Agency, Brazil witnessed a surge in electric vehicle sales in 2023, reaching 19,000 units. This marked a notable 123.5% increase from 2022. Impressively, over the last five years, sales have skyrocketed, growing by over 100 times, underscoring the escalating demand for electric vehicles in the nation.

The Brazilian government is actively promoting policies to incentivize the development of renewable energy and the adoption of electric vehicles, which in turn is stimulating demand for locally manufactured batteries. Initiatives such as tax breaks, subsidies, and investment in research and development are designed to attract both domestic and foreign investment into the battery manufacturing sector. These policy measures are complemented by partnerships with international technology firms, which are eager to leverage Brazil's vast market potential and skilled labor force.

For instance, in July 2023, BYD is planning to build three production facilities on a former Ford industrial site in Brazil: one for the production of electric and hybrid cars, one for chassis for electric buses and trucks, and a third that will process lithium and iron phosphate for the electric vehicle battery market. To convert the site in the Camacari industrial park in the Brazilian state of Bahia, BYD is ready to spend up to USD 617 million.

Thus, such a scenario is expected to Brazil the dominating player in the market during the forecast period.

South America Electric Vehicle Battery Manufacturing Industry Overview

The South America Electric Vehicle Battery Manufacturing Market is semi-consolidated. Some of the key players in this market (in no particular order) are BYD Co. Ltd, SK innovation Co., Ltd., EnerSys, LG Chem Ltd, and Exide Industries.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Increasing Adoption of Electric Vehicles

4.5.1.2 Abundance of Raw Materials

4.5.2 Restraints

4.5.2.1 Competition From Established Markets

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery

5.1.1 Lithium-ion

5.1.2 Lead-Acid

5.1.3 Nickel Metal Hydride Battery

5.1.4 Others

5.2 Battery Form

5.2.1 Prismatic

5.2.2 Pouch

5.2.3 Cylindrical

5.3 Vehicle

5.3.1 Passenger Cars

5.3.2 Commercial Vehicles

5.3.3 Others

5.4 Propulsion

5.4.1 Battery Electric Vehicle

5.4.2 Hybrid Electric Vehicle

5.4.3 Plug-in Hybrid Electric Vehicle

5.5 Geography

5.5.1 Brazil

5.5.2 Argentina

5.5.3 Colombia

5.5.4 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements