배터리 시뮬레이션 소프트웨어 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Battery Simulation Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1822568

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 240 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

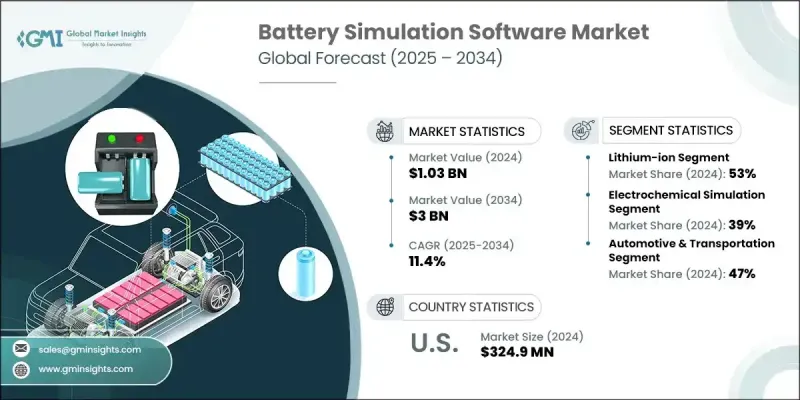

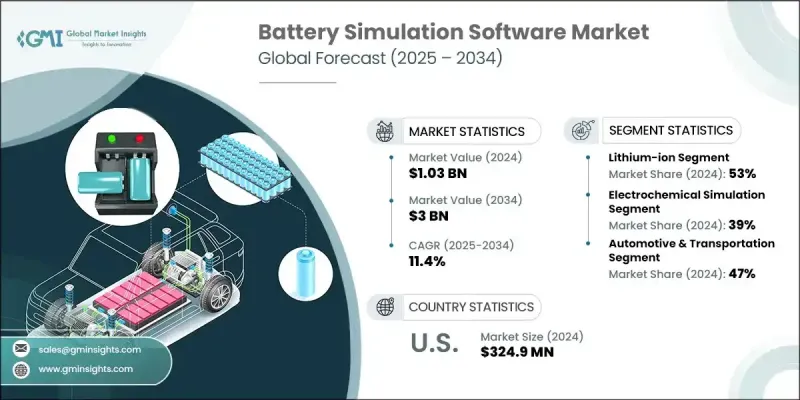

배터리 시뮬레이션 소프트웨어 세계 시장 규모는 2024년에 10억 3,000만 달러로 평가되었고, CAGR 11.4%로 성장하여 2034년에는 30억 달러에 이를 것으로 예측되고 있습니다.

이 성장은 전기자동차와 그리드 규모의 에너지 저장에 대한 수요의 급증에 대응하고, 보다 스마트하고 비용 효율적이고 에너지 효율적인 배터리 시스템을 요구하는 움직임이 확산되고 있음을 반영합니다. 시뮬레이션 소프트웨어는 배터리 동작을 모델링하고, 설계를 간소화하고, 성능을 최적화하는 강력한 도구 세트를 제공하는 한편, 비용이 많이 드는 물리적 프로토타입을 최소화할 수 있습니다. 자동차 제조업체와 에너지 솔루션 제공업체는 배터리의 안전성을 높이고 항속거리를 늘리고 진화하는 에너지 저장 규제에 대응하기 위해 점점 시뮬레이션을 활용하고 있습니다. 국가의 송전망에 재생에너지원이 추가되는 동안 부하 분산을 지원하고, 피크 압력을 줄이고 공급을 안정화시키는 신뢰성 높은 스토리지가 필요합니다. 이러한 목표를 달성하기 위해서는 특히 계통 운영자와 전력 사업자가 스마트 에너지 인프라의 규모를 확대하는 가운데 배터리 시뮬레이션 플랫폼이 필수적입니다. 디지털 엔지니어링으로의 전환은 COVID-19의 유행과 같은 혼란에 의해 가속화되고 있습니다. 이러한 혼란으로 인해 실험실에 대한 액세스가 제한되고 이동이 제한되어 기업이 원격 설계 및 가상 테스트를 수행하게 되었습니다. 기업은 현재 하이브리드 클라우드 환경, 디지털 트윈 시스템 및 검증된 가상 모델을 활용하여 배터리 기술 개발을 추진하고 혁신 사이클을 단축하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

10억 3,000만 달러

예측 금액

30억 달러

CAGR

11.4%

리튬 이온 배터리 분야는 2024년에 53%의 점유율을 차지하고 2034년까지 연평균 복합 성장률(CAGR) 11%로 성장할 것으로 예측됩니다. 리튬 이온 배터리는 높은 에너지 밀도, 긴 사이클 수명, 효율적인 성능 특성으로 인해 전기자동차, 그리드 에너지 시스템 및 모바일 전자 제품의 가장 유력한 선택입니다. 시뮬레이션 소프트웨어를 사용하면 열 거동, 전기 화학 반응, 충방전 사이클의 예측 모델링을 통해 리튬 이온 배터리의 설계를 개선 할 수 있습니다. 이러한 도구는 배터리 수명과 시스템 신뢰성을 향상시키는 데에도 중요한 역할을 합니다. 전동성과 청정 에너지 분야가 계속 확대됨에 따라 시뮬레이션은 기술 혁신에 필요한 기반을 제공하여 이러한 배터리가 점점 더 엄격해지는 성능과 안전성의 벤치마크를 충족할 수 있도록 보장합니다.

전기화학 시뮬레이션 분야는 2024년에 39%의 점유율을 획득했으며, 2025년부터 2034년에 걸쳐 CAGR은 11%를 나타낼 것으로 예측됩니다. 이 분야는 배터리 화학과 내부 공정을 분자 수준에서 시뮬레이션 할 수 있다는 점에서 두드러집니다. 이를 통해 제조업체는 물리적 테스트를 수행하기 전에 이온 역학, 충전 거동 및 반응 메커니즘을 평가할 수 있어 개발 속도를 높이고 비용 효율성을 높일 수 있습니다. 전기화학 모델링은 배터리 아키텍처 개선, 전극 재료 최적화, 전해액 조성 조정에 필수적입니다. 이 유형의 시뮬레이션은 전기자동차 및 항공우주 시스템과 같은 안전 및 내구성이 미션 크리티컬한 용도에 매우 중요한 다양한 작동 조건 하에서의 성능에 대한 깊은 통찰력을 지원합니다.

미국 배터리 시뮬레이션 소프트웨어 2024년 업계 점유율은 85%로 3억 2,490만 달러의 수익을 올렸습니다. 이 나라의 배터리 시뮬레이션 분야는 성숙한 기술 생태계, 고급 컴퓨팅 인프라 액세스, 시뮬레이션 워크로드를 위한 확장 가능한 환경을 제공하는 클라우드 서비스 제공업체의 강력한 존재로 이익을 얻고 있습니다. 멀티피직스, 고충실도 시뮬레이션 모델에 대한 수요는 특히 EV 제조업체, 항공우주기업, 청정에너지 신흥기업들 사이에서 높아지고 있습니다. 또한 미국은 R&D 투자 및 디지털 엔지니어링의 혁신을 이끌고 있으며, 기업은 클라우드 지원 모델링 플랫폼을 통해 물리적 프로토타이핑 비용을 절감하고 시장 출시 시간을 단축할 수 있습니다.

세계 배터리 시뮬레이션 소프트웨어 업계의 주목할만한 기업으로는 Dassault, ESI, Siemens, COMSOL, AVL List, MathWorks, Autodesk, Ansys, Altair Engineering 등이 있습니다. 배터리 시뮬레이션 소프트웨어 분야의 기업은 시장에서의 지위를 확고하게 하기 위해 혁신, 협업, 클라우드 통합을 우선하고 있습니다. 각 회사는 실제 배터리 사용에 적응하는 AI를 강화한 모델링 툴에 투자함으로써 시뮬레이션의 정확성을 높이고 있습니다. 많은 기업들이 OEM, 배터리 개발 기업, 학술 기관과 파트너십을 맺고, 독자적인 알고리즘을 개발하고, 업계 고유의 용도를 공동 개발하고 있습니다. 클라우드 기반 및 On-Premise 하이브리드 배포 옵션을 제공하는 데에도 힘을 실어 다양한 IP 감도 수준을 지원합니다. 또한 선도적인 공급업체는 사용자 인터페이스 개선, 시뮬레이션 실행 시간 단축, 멀티피직스 환경 지원을 통해 더 많은 기업 사용자를 끌어들이려고 합니다.

목차

제1장 조사 방법

시장의 범위와 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역/국가

기본 추정과 계산

기준연도 계산

시장 예측의 주요 동향

1차 조사와 검증

1차 정보

예측 모델

조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

전기자동차(EV)의 보급 증가

신재생에너지 저장에 대한 투자 증가

배터리 화학에 있어서의 기술의 진보

시뮬레이션에서 AI와 클라우드 컴퓨팅의 통합

업계의 잠재적 위험 및 과제

초기 투자가 높고 소프트웨어가 복잡

데이터의 가용성과 모델의 정밀도의 과제

시장 기회

신흥 시장으로 확대

배터리 제조업체 및 OEM과의 제휴

디지털 트윈과 IoT 기술의 통합

차세대 배터리 커스터마이즈

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신규기술

특허 분석

가격 동향과 경제 분석

이용 사례

세포 레벨 설계 및 최적화

모듈과 팩 레벨의 통합

시스템 레벨 성능과 통합

라이프사이클과 열화분석

최상의 시나리오

투자 상황과 자금 조달 분석

세계의 배터리 산업의 투자 동향

시뮬레이션 소프트웨어에 대한 투자와 연구 개발비

지역 투자 패턴과 정부의 지원

기술이전과 상업화

비용편익분석

소프트웨어 도입 비용 구조

운용상의 이점과 가치 창조

전략적 이점과 경쟁 우위

ROI 분석 및 투자 회수 평가

지속가능성과 환경영향 분석

수명 주기 평가 및 환경 모델링

지속가능한 설계와 최적화

환경 컴플라이언스 및 보고

그린테크놀로지와 혁신

미래의 기술 로드맵과 혁신의 타임라인

시뮬레이션 기술의 진화(2024-2034)

배터리 기술의 통합과 적응

기술의 융합과 플랫폼의 진화

시장의 진화와 파괴의 시나리오

품질 보증 및 검증의 프레임워크

모델 검증 및 검증

소프트웨어 품질 보증

규제 준수 및 문서화

지속적인 개선과 혁신

기술 통합 및 워크플로 최적화

CAD와 설계 툴의 통합

PLM과 데이터 관리의 통합

제조 및 테스트 통합

디지털 트윈과 IoT의 통합

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장계획과 자금조달

제5장 시장 추정 및 예측 : 배터리 유형별, 2021-2034

주요 동향

리튬 이온

납산 배터리

솔리드 스테이트

기타

제6장 시장 추정 및 예측 : 시뮬레이션별, 2021-2034

주요 동향

전기화학 시뮬레이션

열 시뮬레이션

구조 및 기계 시뮬레이션

전기 및 회로 시뮬레이션

기타

제7장 시장 추정 및 예측 : 전개 모드별, 2021-2034

주요 동향

On-Premise

클라우드

하이브리드

제8장 시장 추정 및 예측 : 용도별, 2021-2034

주요 동향

자동차 및 운송

가전

에너지 저장 시스템

산업기기

제9장 시장 추정 및 예측 : 기업별, 2021-2034

주요 동향

중소기업

대기업

제10장 시장 추정 및 예측 : 최종 용도별, 2021-2034

주요 동향

OEM

배터리 제조업체

연구개발조직

대학 및 학술기관

제11장 시장 추정 및 예측 : 지역별, 2021-2034

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

아시아태평양

중국

인도

일본

호주

한국

필리핀

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제12장 기업 프로파일

세계 기업

Ansys

Siemens

Altair Engineering

MathWorks

Dassault Systemes

AVL List GmbH

ESI Group

Ricardo

Intertek Group

Hexagon

Synopsys

COMSOL

dSPACE

Gamma Technologies

지역 기업

OpenCFD

TWAICE Technologies GmbH

Batemo

Maplesoft

ThermoAnalytics

Shenzhen Finite Element Technology

Suzhou Yilaikede Technology

Mid-Atlantic Power Specialists

UK Battery Industrialization Centre

신규 기업

Battery Design LLC

BATEMO GmbH

Keysight Technologies

Gamma Technologies

AVL List GmbH

Cadmus Group

Electrochemical Engine Simulation

SHW

영문 목차

영문목차

The Global Battery Simulation Software Market was valued at USD 1.03 billion in 2024 and is estimated to grow at a CAGR of 11.4% to reach USD 3 billion by 2034.

This growth reflects a broader push toward smarter, cost-effective, and energy-efficient battery systems in response to surging demand for electric vehicles and grid-scale energy storage. Simulation software offers a powerful toolset to model battery behavior, streamline design, and optimize performance while minimizing costly physical prototyping. Automakers and energy solution providers are increasingly leveraging simulation to enhance battery safety, extend range, and align with evolving energy storage regulations. With renewable energy sources being added to national grids, there's a need for dependable storage that supports load balancing, reduces peak pressure, and stabilizes supply. Battery simulation platforms are emerging as essential to meeting these goals, especially as grid operators and utility providers scale up smart energy infrastructure. The transition to digital engineering has been accelerated by disruptions like the COVID-19 pandemic, where limited access to labs and travel restrictions drove enterprises toward remote design and virtual testing. Companies now rely on hybrid cloud environments, digital twin systems, and validated virtual models to advance battery technology development and shorten innovation cycles.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$1.03 Billion

Forecast Value

$3 Billion

CAGR

11.4%

The lithium-ion battery segment held 53% share in 2024 and is projected to maintain a CAGR of 11% through 2034. Lithium-ion batteries remain the most prominent choice for electric vehicles, grid energy systems, and mobile electronics due to their high energy density, long cycle life, and efficient performance characteristics. Simulation software enables developers to improve lithium-ion battery design through predictive modeling of thermal behavior, electrochemical reactions, and charge-discharge cycles. These tools also play a vital role in improving battery longevity and system reliability. As electric mobility and clean energy sectors continue to scale, simulation provides a necessary foundation for innovation, ensuring these batteries meet increasingly rigorous performance and safety benchmarks.

The electrochemical simulation segment captured 39% share in 2024 and is anticipated to grow at a CAGR of 11% from 2025 to 2034. This segment stands out due to its capacity to simulate battery chemistry and internal processes at the molecular level. It allows manufacturers to evaluate ion dynamics, charging behavior, and reaction mechanisms before physical trials, making development faster and more cost-effective. Electrochemical modeling is essential for refining battery architecture, optimizing electrode materials, and tailoring electrolyte composition. This simulation type supports deeper insights into performance under variable operating conditions, which is crucial for applications where safety and durability are mission-critical, including electric vehicles and aerospace systems.

United States Battery Simulation Software Industry held an 85% share in 2024, generating USD 324.9 million. The country's battery simulation sector benefits from its mature tech ecosystem, access to advanced computing infrastructure, and a strong presence of cloud service providers offering scalable environments for simulation workloads. The demand for multi-physics, high-fidelity simulation models is growing, particularly among EV manufacturers, aerospace companies, and clean energy startups. The US also leads in R&D investment and digital engineering transformation, enabling companies to reduce physical prototyping costs and shorten time-to-market through cloud-enabled modeling platforms.

Notable players in the Global Battery Simulation Software Industry include Dassault, ESI, Siemens, COMSOL, AVL List, MathWorks, Autodesk, Ansys, and Altair Engineering. To solidify their market position, companies in the battery simulation software sector are prioritizing innovation, collaboration, and cloud integration. Firms are advancing simulation accuracy by investing in AI-enhanced modeling tools that adapt to real-world battery usage conditions. Many players are forming partnerships with OEMs, battery developers, and academic institutions to develop proprietary algorithms and co-develop industry-specific applications. There's a strong focus on offering hybrid deployment options-cloud-based and on-premises-catering to varying IP sensitivity levels. Leading providers are also improving user interfaces, reducing simulation runtimes, and supporting multi-physics environments to attract more enterprise users.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Battery Type

2.2.3 Simulation

2.2.4 Application

2.2.5 Enterprises

2.2.6 Deployment mode

2.2.7 End Use

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising adoption of electric vehicles (EVs)

3.2.1.2 Increasing investment in renewable energy storage

3.2.1.3 Technological advancements in battery chemistry

3.2.1.4 Integration of AI and cloud computing in simulation

3.2.2 Industry pitfalls and challenges

3.2.2.1 High initial investment and software complexity

3.2.2.2 Data availability and model accuracy challenges

3.2.3 Market opportunities

3.2.3.1 Expansion in emerging markets

3.2.3.2 Collaboration with battery manufacturers and OEMs

3.2.3.3 Integration with digital twin and IoT technologies

3.2.3.4 Customization for next-generation batteries

3.3 Regulatory landscape

3.3.1 North America

3.3.2 Europe

3.3.3 Asia Pacific

3.3.4 Latin America

3.3.5 Middle East & Africa

3.4 Porter's analysis

3.5 PESTEL analysis

3.6 Technology and Innovation landscape

3.6.1 Current technological trends

3.6.2 Emerging technologies

3.7 Patent analysis

3.8 Pricing trends and economic analysis

3.9 Use cases

3.9.1 Cell-level design and optimization

3.9.2 Module and pack-level integration

3.9.3 System-level performance and integration

3.9.4 Lifecycle and degradation analysis

3.10 Best-case scenario

3.11 Investment landscape and funding analysis

3.11.1 Global battery industry investment trends

3.11.2 Simulation software investment and R&D spending

3.11.3 Regional investment patterns and government support

3.11.4 Technology transfer and commercialization

3.12 Cost-benefit analysis

3.12.1 Software implementation cost structure

3.12.2 Operational benefits and value creation

3.12.3 Strategic benefits and competitive advantage

3.12.4 ROI analysis and payback assessment

3.13 Sustainability and environmental impact analysis

3.13.1 Lifecycle assessment and environmental modeling

3.13.2 Sustainable design and optimization

3.13.3 Environmental compliance and reporting

3.13.4 Green technology and innovation

3.14 Future technology roadmap and innovation timeline