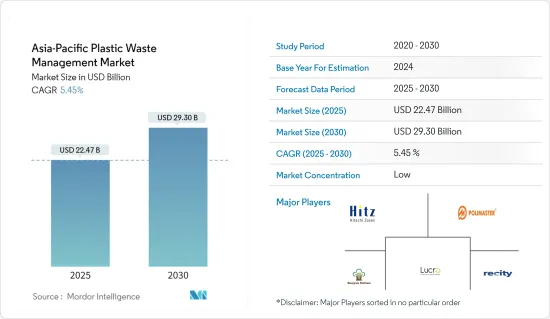

아시아태평양의 플라스틱 폐기물 관리 시장 규모는 2025년에 224억 7,000만 달러로 추정되며, 예측 기간 중(2025-2030년) 연평균 성장율(CAGR)은 5.45%로, 2030년에는 293억 달러에 달할 것으로 예측됩니다.

아시아태평양 지역의 급속한 도시화와 산업 확장은 플라스틱 소비와 폐기물 생산의 급증을 부추기고 있습니다. 특히 중국과 인도와 같은 국가의 도심이 플라스틱 폐기물의 주요 발생지로 떠오르고 있습니다. 아시아 태평양 지역의 각국 정부는 점점 더 엄격한 조치로 대응하고 있습니다. 여기에는 일회용 플라스틱 사용 금지, 생산자책임재활용(EPR) 프로그램 도입, 재활용 촉진을 위한 인센티브 등이 포함됩니다. 예를 들어, 중국은 플라스틱 폐기물 수입을 금지했고, 인도는 자체적인 플라스틱 폐기물 관리 규정을 시행하고 있습니다.

정교한 분류 시스템부터 화학적 및 생분해성 재활용 방법에 이르기까지 재활용 기술의 발전으로 플라스틱 폐기물 관리 환경이 재편되고 있습니다. 이와 동시에 디지털 폐기물 추적 및 관리 솔루션을 도입하는 추세도 증가하고 있습니다. 플라스틱 오염을 둘러싼 환경 문제에 대한 대중의 인식이 높아지면서 소비자들은 보다 지속 가능한 제품과 책임감 있는 폐기물 관리를 요구하고 있습니다. 이에 따라 기업들은 친환경적인 관행과 재활용 인프라에 대한 막대한 투자로 나아가고 있습니다.

아시아태평양 지역의 플라스틱 폐기물 관리 시장의 경제적 잠재력은 특히 수거, 분류, 재활용, 폐기물 에너지화 기술과 같은 분야에서 방대합니다. 이에 따라 재활용 인프라와 폐기물 관리 시설에 대한 투자가 증가하고 있습니다. 그러나 일부 아태지역 국가에서는 폐기물 관리 인프라의 미비, 낮은 재활용률, 혼합 및 오염된 플라스틱 폐기물의 만연 등의 문제가 여전히 남아 있습니다. 이러한 문제를 해결하려면 인프라를 업그레이드하고 쓰레기 분리수거에 대한 대중의 인식과 참여를 높여야 합니다.

인구가 약 40억 명에 달하는 아시아 태평양 지역은 급속한 도시화로 인해 플라스틱 문제가 더욱 악화되고 있습니다. 유엔 보고서에 따르면 이 지역에는 이미 28개의 거대 도시가 있으며, 매일 약 12만 명의 사람들이 이 지역의 도심으로 이주하고 있습니다. 2050년에는 무려 33억 명의 인구가 아시아태평양 지역의 도시에 거주할 것으로 예상됩니다. 이러한 도시화의 급증은 소비를 촉진했으며, 특히 연질 플라스틱 부문의 일회용 포장재에 대한 수요를 급증시켰습니다. 현재의 추세가 지속된다면 2030년까지 아시아태평양 지역에서는 1억 4천만 톤의 플라스틱 폐기물이 발생할 것으로 예상됩니다.

세계에서 가장 인구가 많은 나라의 대부분이 아시아태평양 지역에 있음을 감안할 때, 도시화의 급증은 라이프 스타일의 변화와 포장 상품에 대한 욕구 증가를 동반합니다. 포장의 유연성은 아시아태평양에서 중요한 관심사가 되었습니다. 이 지역의 생산, 특히 식품 분야의 매력은 낮은 관련 비용으로 인해 더욱 강화되었습니다. 2023년 아시아태평양는 연포장 시장에서 52.2%의 점유율을 차지했습니다. Uflex 및 Fuji Seal International과 같은 주목할만한 기업은 이 지역의 업계 입지를 강화하고 있습니다. 아시아태평양의 일회용 플라스틱 포장, 특히 파우치 및 파우치 포장(예 : 인도의 생수 포장)에 대한 선호도는 이러한 소재가 제공하는 비용 우위로 인한 것입니다.

인도네시아의 일회용 비닐봉지 사례는 아시아 태평양 지역 규제의 효과를 생생하게 보여줍니다. 자카르타는 23개 도시와 지방 자치단체에서 성공적인 시범 운영을 거친 후 2020년 7월부터 비닐봉지 사용을 전면 금지했습니다. 처음에는 기업들의 반발이 있었지만, 규정을 준수하지 않는 기업은 벌금을 부과하고 상습 위반자는 허가가 취소될 위험에 처하는 등 규제가 유지되었습니다.

보고된 결과는 이 금지령이 성공적이었다는 것을 보여줍니다. 2018년 자카르타에서는 연간 약 2억 4천만-3억 개의 비닐봉지가 소비되었습니다. 2021년까지 이 소비량은 11,192톤에서 6,452톤으로 42% 감소했습니다.

전 세계적으로는 방글라데시가 2002년에 전국적인 비닐봉지 사용 금지 조치를 시행하여 선도적인 역할을 했습니다. 중국은 2020년에 금지 조치를 시작했으며, 2025년에 최종 단계가 시작될 예정입니다. 인도도 2022년에 일회용 플라스틱 사용 금지를 시행하며 이 운동에 동참했습니다.

이러한 진전에도 불구하고 아시아 태평양(APAC) 지역의 일부 국가는 이러한 추세에 발맞추기 위해 고군분투하고 있습니다. 한국의 제로 웨이스트 운동 네트워크에 따르면 한국은 매년 무려 190억 개의 비닐봉지를 소비하고 있습니다. 한편, 태국 정부 조사에 따르면 연간 약 2,000억 개의 비닐봉지가 소비되며, 이는 국민 1인당 하루 평균 8개의 비닐봉지를 소비하는 것으로 나타났습니다. 해양보존협회는 태국을 전 세계 해양 쓰레기 배출량 6위 국가로 꼽았습니다.

결론적으로, 아시아태평양 국가에서 플라스틱 규제의 현저한 진전에도 불구하고, 이 지역은 여전히 플라스틱의 소비와 폐기물 관리의 큰 과제를 극복할 필요가 있습니다. 특히 이 지역의 급속한 도시화를 고려하면, 이를 다루기 위해서는 엄격한 시행과 혁신적인 해결책이 필수적입니다.

2023년, 저장성에서 6,000명 이상의 개인과 200개 이상의 기업이 주도한 중국의 노력은 해양 플라스틱 쓰레기 문제 해결을 위한 진전을 인정받아 유엔에서 수여하는 최고의 환경상을 수상했습니다. 이 프로그램은 해양 플라스틱의 재활용 과정을 투명하게 공개하여 지역 어민들을 돕고 특히 연안 해역의 오염을 억제하는 데 기여하고 있습니다. 이 프로젝트는 시작 이래 61,600명 이상이 참여하여 약 10,936톤의 해양 쓰레기를 수거했으며, 그 중 2,254톤이 플라스틱 쓰레기였습니다.

중국은 인프라와 기술에 대한 막대한 투자를 통해 폐기물 관리에 대한 의지를 분명히 하고 있습니다. 중국은 폐기물 에너지화 플랜트 및 최첨단 재활용 센터와 같은 노력을 선도적으로 추진하여 쓰레기 매립을 줄이고 있습니다. 중국 동부의 저장성은 음식 배달에 사용되는 플라스틱을 줄이고 재활용하는 것을 목표로 하는 '저장성 음식 배달 플라스틱 제로 웨이스트 프로그램'을 발표했습니다. 이 전략은 2023년 말까지 대학을 비롯한 주요 부문에서 음식 배달 플라스틱에 대한 '폐기물 제로' 모델을 구축하는 것을 목표로 합니다. 2025년까지 이 모델은 학교, 상업 공간 및 지역사회 전반에 걸쳐 도입될 예정입니다.

저장성의 전략에는 음식 배달 플랫폼, 상인, 대학, 폐기 회사 및 재활용 협회와 같은 이해 관계자를 통합하여 음식 배달 플라스틱 폐기물에 대항하는 통일된 전선을 형성하는 협업 노력이 포함됩니다. 저장성은 또한 플라스틱 쓰레기가 많은 지역에 쓰레기 수거 시설을 설치하여 음식 배달 플랫폼이 대학 기숙사 및 식당과 같은 장소에 이러한 시설을 설치하고 대학이 유지 관리를 담당하도록 할 계획입니다.

저장성의 '플라스틱 제로 폐기물 프로그램'에서 볼 수 있는 중국의 쓰레기 문제 해결을 위한 노력은 플라스틱 오염을 막기 위한 중국의 혁신적이고 협력적인 노력을 보여줍니다. 이러한 노력은 더 넓은 아시아태평양 지역의 청사진을 제시하고 선구적인 역할을 하고 있습니다.

아시아 태평양 지역의 플라스틱 폐기물 관리 시장은 매우 세분화되어 있으며, 현지 기업과 글로벌 기업이 혼재되어 있습니다. 이러한 다양성은 국가마다 다른 고유한 폐기물 관리 요건과 규제 프레임워크에서 비롯됩니다. 이 분야의 주요 기업으로는 Hitz 히타치 조선, Polimaster, Banyan Nation, Lucro, Recity 등이 있습니다.

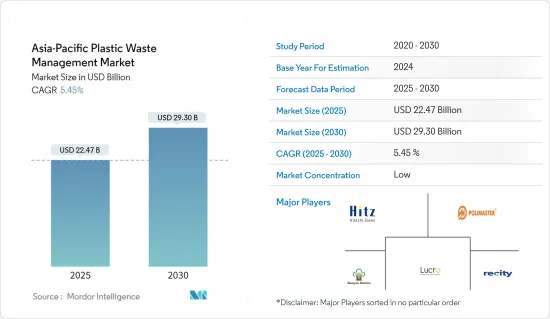

The Asia-Pacific Plastic Waste Management Market size is estimated at USD 22.47 billion in 2025, and is expected to reach USD 29.30 billion by 2030, at a CAGR of 5.45% during the forecast period (2025-2030).

Rapid urbanization and industrial expansion in Asia-Pacific are fueling a surge in plastic consumption and waste production. Notably, urban centers in countries like China and India stand out as primary plastic waste generators. Governments in the APAC region are responding with increasingly stringent measures. These include bans on single-use plastics, the introduction of extended producer responsibility (EPR) programs, and incentives to promote recycling. For instance, China has enforced a ban on plastic waste imports, while India has rolled out its own set of plastic waste management regulations.

Technological advancements in recycling, spanning from sophisticated sorting systems to chemical and biodegradable recycling methods, are reshaping the plastic waste management landscape. Simultaneously, there is a rising trend in adopting digital waste tracking and management solutions. As public awareness of environmental issues surrounding plastic pollution grows, consumers demand more sustainable products and responsible waste management. This, in turn, pushes companies toward eco-friendly practices and substantial investments in recycling infrastructure.

The economic potential of the plastic waste management market in Asia-Pacific is vast, especially in areas like collection, sorting, recycling, and waste-to-energy technologies. As a result, investments in recycling infrastructure and waste management facilities are rising. However, challenges persist, including inadequate waste management infrastructure in several APAC nations, low recycling rates, and the prevalence of mixed and contaminated plastic waste. Addressing these challenges will require infrastructure upgrades and heightened public awareness and engagement in waste segregation.

With a population of approximately 4 billion, Asia-Pacific (APAC) is witnessing rapid urbanization, exacerbating its escalating plastic predicament. A UN report highlights that APAC already hosts 28 megacities, and an estimated 120,000 individuals are relocating to urban centers in the region daily. Projections suggest that a staggering 3.3 billion people will live in cities in Asia-Pacific by the year 2050. This surge in urbanization has fueled consumption, notably spiking the demand for single-use packaging, especially in the flexible plastic segment. If the current trajectory persists, APAC is set to generate a colossal 140 million tonnes of plastic waste by 2030.

Given that many of the world's most populous countries reside in the APAC region, the surge in urbanization is accompanied by shifting lifestyles and heightened appetites for packaged goods. Flexibility in packaging emerges as a focal concern in APAC. The region's allure for production, especially in the food sector, is bolstered by its lower associated costs. In 2023, APAC commanded a 52.2% share in the flexible packaging market. Noteworthy players like Uflex and Fuji Seal International fortify the industry's standing in the region. APAC's penchant for single-use plastic packaging, notably in pouches and sachets (e.g., single-serve water packages in India), is largely due to the cost advantage these materials offer.

The case of single-use plastic bags in Indonesia vividly illustrates the efficacy of APAC regulations. Following a successful trial in 23 cities and municipalities, Jakarta enforced a blanket ban on plastic bags in July 2020. Despite initial pushback from businesses, the regulation was upheld, with non-compliant companies facing fines and repeat offenders risking permit revocation.

The reported results indicate the ban's success. In 2018, Jakarta consumed an estimated 240-300 million plastic bags annually. By 2021, this consumption had dropped by 42%, from 11,192 tons to 6,452 tons.

On a global scale, Bangladesh led the way by implementing a national plastic bag ban in 2002. China initiated its ban in 2020, with the final phase set for 2025. India also joined the movement, implementing a ban on single-use plastics in 2022.

Despite these advancements, parts of the Asia-Pacific (APAC) region are struggling to keep pace. South Korea consumes a staggering 19 billion plastic bags each year, as reported by the Korea Zero Waste Movement Network. Meanwhile, Thailand's government survey revealed an annual consumption of around 200 billion plastic bags, translating to an average of eight bags per citizen per day. The Ocean Conservancy highlights Thailand as the sixth-largest contributor to global marine waste.

The conclusion is that despite notable progress in plastic regulation across various APAC nations, the region still needs to overcome significant plastic consumption and waste management challenges. Stringent enforcement and innovative solutions are imperative to address this, especially given the region's rapid urbanization.

In 2023, China's initiative, spearheaded by over 6,000 individuals and 200+ enterprises from Zhejiang, clinched the UN's top environmental accolade for its strides in tackling marine plastic waste. The program offers a transparent view of marine plastics' recycling journey, aiding local fishermen and notably curbing pollution in coastal waters. Since its inception, the project has engaged over 61,600 participants and collected approximately 10,936 tons of marine debris, 2,254 tons of which were plastic waste.

China's commitment to waste management is evident through substantial investments in infrastructure and technology. The nation is pioneering initiatives like waste-to-energy plants and cutting-edge recycling centers to slash landfill contributions. Zhejiang Province in eastern China unveiled the "Zhejiang Food Delivery Plastic Zero Waste Program," targeting reducing and recycling plastics used in food delivery. The initiative was aimed at establishing a "zero waste" model for food delivery plastics in key sectors, notably universities, by the end of 2023. By 2025, this model will be rolled out across schools, commercial spaces, and communities.

Zhejiang's strategy involves a collaborative effort, uniting stakeholders like food delivery platforms, merchants, universities, disposal firms, and recycling associations to form a unified front against plastic waste in food delivery. Zhejiang also plans to install waste collection facilities in areas with heightened plastic waste, tasking food delivery platforms with setting up these facilities in locations like university dorms and cafeterias, with the universities handling their maintenance.

Overall, China's commitment to tackling waste, which is evident in Zhejiang's "Plastic Zero Waste Program," showcases the nation's innovative and collaborative efforts to combat plastic pollution. These initiatives are pioneering and establishing a blueprint for the broader APAC region.

In Asia-Pacific, the plastic waste management market is highly fragmented, featuring a mix of local and global players. This diversity stems from the unique waste management requirements and regulatory frameworks that vary from country to country. Some of the key players in this sector are Hitachi Zosen Corporation, Polimaster, Banyan Nation, Lucro, and Recity.