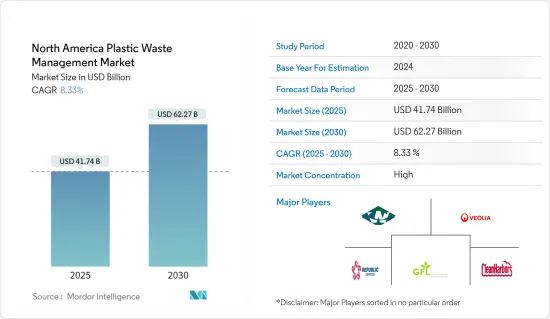

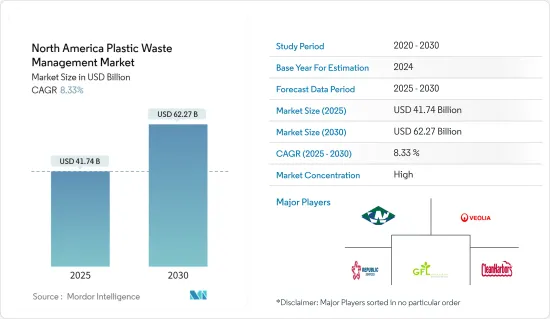

북미의 플라스틱 폐기물 관리 시장 규모는 2025년에 417억 4,000만 달러로 예측되어 예측 기간 중(2025-2030년)의 연평균 성장율(CAGR)은 8.33%로, 2030년에는 622억 7,000만 달러에 달할 것으로 예측되고 있습니다.

북미의 플라스틱 폐기물 관리 시장은 왕성한 플라스틱 소비와 엄격한 규제에 힘입어 성장하고 있습니다. 이 기세는 환경 의식 증가, 규제 강화, 폐기물 관리 솔루션의 기술적 진보 때문입니다.

미국의 플라스틱 생산량은 연간 3,500만 톤을 넘어섰습니다. 비닐봉지부터 포장재에 이르기까지 미국인들의 플라스틱 소비는 엄청납니다. 하지만 플라스틱에 대한 이러한 욕구는 심각한 결과를 초래합니다. 매년 약 800만 톤의 폐기물이 바다로 흘러들어가고 재활용되는 양은 9%에 불과합니다. 이러한 환경 과실은 엄청난 대가를 치르게 되는데, 미국에서는 플라스틱 오염으로 인해 연간 130억 달러의 비용이 발생하고 있습니다. 이러한 비용에도 불구하고 플라스틱 산업은 여전히 100만 명 이상의 미국인에게 일자리를 제공하는 중요한 고용주입니다. 지방 정부는 매년 33억 달러 이상의 비용을 지출하며 폐기물 관리의 가장 큰 부담을 안고 있습니다. 플라스틱 생산은 미국 국내총생산의 약 2.7%를 차지합니다.

미국과 캐나다는 플라스틱 사용 금지 및 재활용 의무화 등 플라스틱 쓰레기 문제를 해결하기 위해 상당한 조치를 취했습니다. 이와 동시에 플라스틱이 환경에 미치는 영향에 대한 대중의 인식이 높아지면서 보다 효과적인 폐기물 관리 솔루션에 대한 수요도 증가하고 있습니다. 화학 물질 재활용 및 첨단 분류 시스템과 같은 주목할 만한 혁신으로 플라스틱 폐기물 관리의 효율성이 높아지고 있습니다. 또한 기업들이 지속 가능성과 순환 경제 원칙에 점점 더 집중하면서 시장은 더욱 강화되고 있습니다.

북미의 플라스틱 폐기물 관리 시장은 규제 지원, 기술 혁신, 높아진 환경 의식에 힘입어 지속적인 성장세를 보일 것으로 전망됩니다. 이 분야의 기업들은 혁신적인 재활용 기술을 우선시하고, 재활용 역량을 강화하며, 전략적 제휴를 맺어 시장 입지를 공고히 할 것입니다.

플라스틱 업계의 로드맵은 내구재의 수명 종료 단계를 재편할 수 있는 중요한 기회를 강조합니다. 북미에서 생산되는 플라스틱의 약 60%가 내구재에 사용된다는 점을 고려할 때, 플라스틱을 폐기하지 않고 새로운 제품으로 재활용하는 순환 경제로 전환하여 이러한 재료를 보존하는 솔루션을 찾는 것이 필수적입니다.

미국화학위원회(ACC)의 플라스틱 사업부는 정책 입안자, 비즈니스 리더, 대중을 보다 지속 가능한 관행으로 안내하기 위한 업계 로드맵을 발표했습니다. 이 로드맵은 자동차, 건축 및 건설, 전자, 인프라, 의료 등 5개 주요 부문에서 순환 관행의 채택을 촉진하기 위한 정책과 전략을 개괄적으로 설명합니다.

로드맵에서 강조하는 몇 가지 핵심 사항에는 분해, 수리, 재활용이 용이하도록 제품과 구성품을 설계해야 한다는 점과 사용 후 부품을 새로운 제품으로 전환하는 것을 강조하는 내용이 포함됩니다.

첨단(화학) 재활용의 중추적인 역할은 재활용 가능한 플라스틱의 범위를 넓히고, 특히 기존의 기계적 재활용이 어려움을 겪는 내구성 있는 용도에 사용되는 플라스틱의 범위를 넓혀줍니다. 내구성이 뛰어난 제품을 보장하기 위한 표준, 방법 및 인증 프로그램을 확립하는 것은 플라스틱 순환 경제에 부합하는 중요한 일입니다.

내구성 플라스틱의 분리, 분류, 재활용의 기술적, 경제적 타당성을 평가하기 위해 ACC가 오크리지 국립연구소와 협력하는 것과 같은 파일럿 프로그램이 더 많이 필요하다는 요구가 있습니다. ACC는 정책 입안자 및 내구성 플라스틱 가치 사슬과 협력하여 업계 로드맵에 명시된 순환성 목표를 실현하기 위해 최선을 다하고 있습니다.

미국화학회의 지침에 따라 플라스틱 산업은 특히 자동차, 건설, 전자 분야에서 순환 경제로 전환하고 있습니다. 업계의 로드맵에서 강조된 이러한 변화는 고급 재활용, 분해 설계, 엄격한 표준 설정에 중점을 두고 있습니다. 이는 내구성이 뛰어난 플라스틱 관리 방식을 혁신하기 위해 정책 입안자, 업계 대기업, ACC가 함께 노력한 결과입니다. 재활용과 용도 변경의 지속적인 사이클을 보장하여 폐기물을 크게 줄이는 것이 목표입니다.

미국을 포함한 고소득 국가들은 덜 부유한 국가들에 비해 1인당 플라스틱 소비량이 높은 경향을 보입니다. 특히 미국이 두드러지는데, 미국인은 매일 평균 약 0.34kg의 플라스틱을 사용합니다. 이는 캐나다와 멕시코의 1인당 하루 사용량인 0.09kg의 거의 세 배에 달하는 수치입니다. 연간 3,783만 톤을 소비하는 미국은 세계에서 두 번째로 큰 플라스틱 소비국으로, 6,000만 톤을 소비하는 중국의 뒤를 크게 뒤쫓고 있습니다. 하지만 플라스틱 소비량이 많다고 해서 자동적으로 오염원이 되는 것은 아닙니다. 부유한 국가일수록 1인당 플라스틱 소비량이 많지만, 더 효과적인 폐기 방법을 위한 재정적 자원도 보유하고 있습니다.

미국을 비롯한 부유한 국가들은 주로 잘 관리된 매립지에 플라스틱 폐기물을 처리하거나 최소한의 재정적 수익에도 불구하고 재활용을 선택합니다. 반대로 플라스틱 소비율이 낮은 많은 저소득 국가에서는 규제되지 않은 매립지나 폐기물 관리 시스템이 부족하여 플라스틱 폐기물이 해양으로 유입될 위험이 높습니다.

2024년 미국 해양대기청(NOAA)은 미국 해안, 오대호, 영토 및 자유 연합 국가를 따라 상당한 해양 쓰레기를 제거하고 쓰레기를 차단하는 검증된 기술을 배치하기 위한 혁신적인 다년간 지원에 약 7천만 달러를 배정했습니다. 또한 NOAA는 장기적으로 해양 쓰레기 퇴치를 위한 연합 구축과 혁신적인 연구에 초점을 맞춘 29개의 씨 그랜트 프로젝트에 2,700만 달러를 배정했습니다.

플라스틱 소비의 격차를 강조하면서 미국은 세계에서 두 번째로 큰 플라스틱 소비국으로 부상하여 부유한 국가와 그렇지 않은 국가 간의 폐기물 관리 능력에서 극명한 대조를 보이고 있습니다. 미국은 선진적인 폐기물 관리와 해양 쓰레기 제거에 대한 의지를 보여주고 있으며, 해양 쓰레기 프로젝트에 7천만 달러의 막대한 자금을 지원하는 NOAA와 같은 이니셔티브는 플라스틱 오염을 방지하고 해양 생태계를 보호하기 위한 헌신적인 접근 방식을 강조합니다. 이러한 노력은 소비와 지속 가능한 폐기물 관리 관행 사이의 글로벌 격차를 해소하는 데 중추적인 역할을 하고 있습니다.

북미의 플라스틱 폐기물 관리 시장은 소수의 대기업이에 의해 매우 집중되어 있으며 대부분의 점유율을 차지하고 있습니다. 이 업계의 선두 주자는 엄청난 자원, 최첨단 기술 및 견고한 인프라를 자랑하며 지역 규모의 플라스틱 폐기물의 효과적인 관리를 촉진합니다. 이 시장의 주요 기업으로는 Waste Connection, Veolia Environment, GFL Environmental, Republic Services, Clean Harbors 등이 있습니다.

The North America Plastic Waste Management Market size is estimated at USD 41.74 billion in 2025, and is expected to reach USD 62.27 billion by 2030, at a CAGR of 8.33% during the forecast period (2025-2030).

The North American plastic waste management market is growing, fueled by robust plastic consumption and stringent regulations. This momentum is attributed to a rising environmental consciousness, tightening regulations, and technological strides in waste management solutions.

Plastic production in the United States surpasses 35 million tons annually. From plastic bags to packaging, Americans' consumption is voracious. However, this appetite for plastic has dire consequences. About 8 million metric tons of waste end up in the oceans yearly, with a mere 9% recycled. This environmental negligence comes at a steep price, with plastic pollution costing the United States an estimated USD 13 billion annually. Despite these costs, the plastic industry remains a significant employer, providing jobs for over 1 million Americans. Local governments bear the brunt of waste management, shelling out more than USD 3.3 billion annually. Plastic production contributes around 2.7% to the US gross domestic product.

The United States and Canada have taken significant steps to combat plastic waste, including bans and recycling mandates. Concurrently, a swelling public awareness of plastic's environmental repercussions is spurring the demand for more effective waste management solutions. Noteworthy innovations, like chemical recycling and advanced sorting systems, are elevating the efficacy of plastic waste management. Moreover, as corporations increasingly pivot toward sustainability and circular economy principles, the market is further fortified.

The North American plastic waste management market is set for sustained growth, propelled by regulatory backing, technological innovations, and a heightened environmental consciousness. Companies in this space will likely prioritize innovative recycling technologies, bolster recycling capacities, and forge strategic alliances to solidify their market standing.

The plastics industry's roadmap underscores significant opportunities to reshape the end-of-life phase for durable goods. Given that nearly 60% of domestically produced North American plastics are channeled into durable goods, it is imperative to find solutions that preserve these materials, pivoting toward a circular economy where plastics are recycled into new products rather than discarded.

The American Chemistry Council's (ACC) Plastics Division has unveiled an industry roadmap to guide policymakers, business leaders, and the public toward more sustainable practices. This roadmap outlines policies and strategies to expedite the adoption of circular practices within five key sectors: automotive, building and construction, electronics, infrastructure, and medical.

Some of the key points highlighted in the roadmap include the necessity of designing products and their components for easy disassembly, repair, and recycling, emphasizing the transformation of spent components into new products.

The pivotal role of advanced (chemical) recycling broadens the scope of recyclable plastics, especially those used in durable applications that traditional mechanical recycling struggles with. The significance of establishing standards, methods, and certification programs to ensure durable products align with a circular economy for plastics.

There is a call for more pilot programs, akin to ACC's collaboration with Oak Ridge National Laboratory to assess the technical and economic feasibility of separating, sorting, and recycling durable plastics. ACC is committed to collaborating with policymakers and the durable plastics value chain to realize the circularity goals outlined in the industry roadmap.

As guided by the American Chemistry Council, the plastics industry is pivoting toward a circular economy, especially in the automotive, construction, and electronics sectors. This shift, highlighted in the industry's roadmap, focuses on advanced recycling, designing for disassembly, and setting stringent standards. It is a concerted effort involving policymakers, industry giants, and the ACC to revolutionize how durable plastics are managed. The goal is to ensure a continuous cycle of recycling and repurposing, significantly curbing waste.

High-income countries, including the United States, exhibit a trend of higher per capita plastic consumption compared to their less affluent counterparts. The United States stands out, with the average American using approximately 0.34 kilograms of plastic daily. This figure is nearly triple the usage of Canada and Mexico, each at 0.09 kg/person per day. With an annual consumption of 37.83 million tons, the United States ranks as the world's second-largest plastic consumer, trailing significantly behind China's staggering 60-million-ton consumption. However, being a top consumer does not automatically equate to being a polluter. Wealthier nations, while consuming more plastic per person, also possess the financial resources for more effective disposal methods.

The United States and other affluent nations predominantly dispose of their plastic waste in well-managed landfills or opt for recycling, even with minimal financial returns. Conversely, many lower-income countries with lower plastic consumption rates grapple with unregulated landfills or lack waste management systems, leading to heightened risks of plastic waste entering the oceans.

In 2024, the National Oceanic and Atmospheric Administration (NOAA) allocated nearly USD 70 million for transformative, multi-year initiatives aimed at removing significant marine debris and deploying proven technologies to intercept debris along the US coasts, Great Lakes, territories, and Freely Associated States. Furthermore, NOAA earmarked USD 27 million for 29 Sea Grant projects, focusing on coalition-building and innovative research to combat marine debris over the long term.

Highlighting the disparity in plastic consumption, the United States emerges as the world's second-largest consumer, showcasing a stark contrast between affluent and less affluent nations in waste management capabilities. While the United States demonstrates a commitment to advanced waste management and marine debris removal, initiatives like NOAA's substantial funding of USD 70 million for marine debris projects underscore a dedicated approach to combatting plastic pollution and safeguarding marine ecosystems. These endeavors play a pivotal role in bridging the global gap between consumption and sustainable waste management practices.

The plastic waste management market in North America is highly concentrated, with a few major players holding the majority share. These industry leaders boast significant resources, cutting-edge technologies, and robust infrastructure, facilitating the effective management of plastic waste on a regional scale. Some of the key players in this market are Waste Connection, Veolia Environment, GFL Environmental, Republic Services, and Clean Harbors.