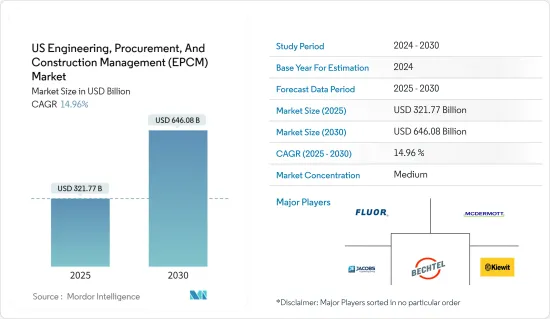

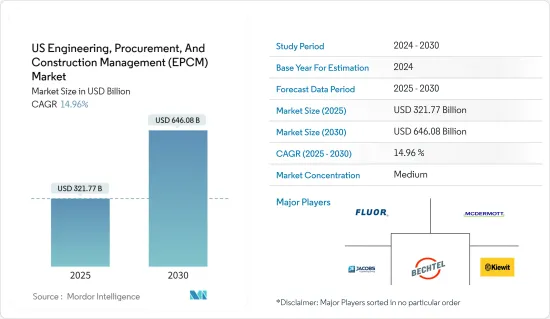

미국의 엔지니어링, 조달 및 건설 관리(EPCM) 시장 규모는 2025년에 3,217억 7,000만 달러로 추정되며, 2030년에는 6,460억 8,000만 달러에 달할 것으로 예상되며, 예측 기간(2025-2030년) 동안 14.96%의 CAGR을 기록할 것으로 예상됩니다.

미국 엔지니어링, 조달 및 건설 관리(EPCM) 시장은 미국 인프라 및 산업 환경에서 매우 중요한 역할을 하고 있습니다. 수십억 달러의 매출과 일관된 성장 궤도를 자랑하며, 주로 인프라 업그레이드, 재생에너지 사업, 산업 확장에 대한 대규모 투자가 그 원동력이 되고 있습니다. 특히, 인프라 투자 및 고용 촉진법으로 대표되는 정부의 노력으로 교통, 공공사업, 급성장 중인 스마트 시티 부문에 많은 자금이 투입되고 있습니다. 또한 풍력, 태양광, 에너지 저장을 포함한 지속가능한 에너지에 대한 국가의 축은 EPC 기업의 프로젝트 파이프라인을 강화하고 있습니다. 이러한 모멘텀은 제조 공장 현대화, 의료 및 데이터센터 인프라에 대한 수요 증가로 인해 더욱 가속화되고 있습니다.

유망한 전망에도 불구하고, 미국 EPC 시장은 성장을 저해할 수 있는 도전에 직면해 있습니다. 복잡한 규제, 노동력 부족, 자재 가격 상승, 인플레이션 압력 등이 대표적인 장애물입니다. 그러나 이러한 장애물에도 불구하고, 이 시장은 특히 스마트 인프라, 재생에너지, 첨단 제조 분야에서 다양한 비즈니스 기회를 제공하고 있으며, Bechtel, Fluor, Jacobs Engineering과 같은 주목할 만한 산업 참여자들이 선두에 서고 있습니다. 빌딩 정보 모델링(BIM), IoT, AI 등의 기술을 활용하여 프로젝트의 효율성과 지속가능성을 높이고 있습니다. 따라서 미국 EPC 시장은 정부 지원, 기술 발전, 현대적 인프라에 대한 의욕에 힘입어 더욱 확대될 것으로 예상됩니다.

미국의 인프라 투자, 특히 엔지니어링, 조달, 건설관리(EPC) 부문에 대한 투자는 경제 성장과 현대화에 있어 매우 중요합니다. 미국은 인구 증가와 기술 발전에 대응하기 위해 교통망과 공공사업 등 핵심 인프라 강화에 막대한 자금을 투입하고 있습니다.

2023년 대통령과 교통부 장관은 바이든-해리스 행정부가 새로운 국가 인프라 프로젝트 지원(메가) 재량 보조금 프로그램에서 9개의 국가 프로젝트에 약 12억 달러를 배정했다고 발표했습니다. 이 이니셔티브는 경제 활성화, 고임금 일자리 창출, 공급망 강화, 주민 이동성 향상, 교통 시스템 안전성 향상을 목표로 하고 있습니다.

메가 보조금 이니셔티브는 바이든 대통령의 획기적인 인프라 구축법에서 비롯된 것으로, 규모와 복잡성에서 기존 자금 지원 프로그램을 능가하는 프로젝트를 대상으로 합니다. 대상 사업에는 고속도로, 교량, 항만, 대중교통이 포함됩니다.

2026년까지 이 메가 프로그램은 현재와 미래 세대에 이익을 가져다주는 데 중점을 두고 미국의 인프라 혁신에 총 50억 달러를 투입할 것으로 예상됩니다. 최근 미국 교통부는 2022년 10억 달러보다 훨씬 많은 약 300억 달러를 신청했습니다. 주목할 만한 프로젝트는 다음과 같습니다.

허드슨 야드 콘크리트 케이스 3공구(뉴욕주)에 2억 9,200만 달러: 이 자금은 콘크리트 케이스의 마지막 구간을 완성하고 새로운 허드슨강 터널을 위한 부지를 확보하여 게이트웨이 프로젝트의 무대를 마련할 수 있도록 합니다. 허드슨 터널 계획이 실현되면 출퇴근 시간 단축, 북동부 회랑(NEC)에서 Amtrak의 신뢰성 향상, 미국 인구의 17%가 거주하는 지역 경제 활성화가 기대되며, Amtrak은 이 프로젝트가 건설 기간 동안 7만 2,000개의 일자리를 창출할 것으로 예상하고 있습니다. 직업훈련을 위한 노조와의 제휴에 중점을 두고 있습니다.

오하이오주 신시내티와 켄터키주 코빙턴의 브렌트 스펜스 교량 개선에 2억 5,000만 달러: 오하이오 강을 가로지르는 이 중요한 화물 통로는 연간 4,000억 달러 이상의 화물 운송을 담당하고 있으며, 트럭 병목 현상으로 악명 높은 곳입니다. 이 메가 그랜트는 브렌트 스펜스 교량의 업그레이드와 기존 교량에 인접한 새로운 교량 건설을 촉진하여 교통 체증을 완화하고 이동 시간의 신뢰성을 향상시켜 지역 경제를 강화하는 것을 목표로 하고 있습니다.

전반적으로 미국의 인프라 투자, 특히 EPC 부문에 대한 투자는 경제 성장과 현대화를 촉진하는 데 있어 매우 중요합니다. 바이든-해리스 행정부가 국가 인프라 프로젝트 지원(메가) 재량 보조금 프로그램에서 약 12억 달러가 배정된 것을 보면 알 수 있습니다. 허드슨강 터널과 브렌트 스펜스 다리와 같은 주목할 만한 프로젝트들은 교통망 강화, 일자리 창출, 공급망 탄력성 강화에 중점을 두고 있는 행정부의 의지를 잘 보여주고 있습니다. 모빌리티, 안전, 경제적 강인성을 향상시켜 현재와 미래 세대에게 혜택을 줄 준비가 되어있습니다.

2023년, 미국의 전력 및 유틸리티 부문은 탈탄소화 노력을 크게 진전시켜 태양광발전과 에너지 저장장치의 도입량을 기록했습니다. 이러한 발전은 매우 중요한 청정에너지 및 기후 관련 법안에 힘입어 2024년까지 지속될 것으로 예상됩니다. 이 부문의 펀더멘털은 엇갈렸지만, 전력 생산량은 2023년 말까지 전년 대비 약 1.2% 감소할 것으로 예상되며, 이는 주로 따뜻한 겨울로 인한 것으로 분석됩니다. 공급망 문제는 완화되기 시작했지만, 철강 및 변압기와 같은 주요 자재의 지속적인 부족은 운영을 방해하고 비용을 증가시켰습니다.

2023년 발전용 천연가스 비용이 전년 대비 53% 하락하면서 많은 지역에서 전력 도매가격이 하락했습니다. 그러나 모든 전력회사가 도매시장에서 전력을 조달하는 것은 아니며, 연료비는 고객 청구서의 구성요소에 불과하기 때문에 가격 변동과 직접적인 상관관계가 없을 수 있습니다. 2023년 주요 전력 및 가스 회사는 송전망 현대화 및 탈탄소화에 총 1,710억 달러에 가까운 비용을 지출하여 새로운 기록을 세울 것입니다. 탈탄소화에 지출하여 새로운 기록을 세웠습니다. 이러한 대규모 자본 지출은 향후 예상되는 지출과 금리 상승과 함께 고객 부담 증가로 이어질 수 있습니다.

2024년, 전기요금은 안정적으로 유지될 것으로 예상되지만, 매출액은 약 2% 증가할 것으로 예상됩니다. 공급망의 혼란은 점차 해소될 것으로 예상됩니다. 다양한 촉매제가 뒷받침하는 청정에너지에 대한 노력의 모멘텀은 앞으로도 지속될 것으로 보입니다. 미국에서는 탄소 감축 목표를 앞당기는 전력회사들이 늘어나고 있으며, 기존 '2050년까지 탄소 순배출량 제로'라는 목표에서 2030년까지 80% 감축을 목표로 하고 있습니다. 인플레이션 억제법(IRA) 시행 1주년이 되는 2023년 8월까지 투자자들은 이미 1,220억 달러 이상을 청정에너지 발전에 투자했으며, 추가로 1,100억 달러를 국내 청정에너지 제조 강화에 투자하고 있습니다.

2023년 인프라 투자 및 고용 촉진법(IIJA)은 송전망 신뢰성 향상, 배터리 공급망, 전기자동차 프로그램, 에너지 효율 향상을 위해 수십억 달러를 배정했습니다. 미국 에너지정보국(EIA)은 실용 규모의 태양광발전 설비가 크게 증가하여 2023년에는 2배 이상 증가한 24기가와트, 2024년에는 36기가와트에 달할 것으로 예상했습니다. 또한 재생에너지의 전력 비중은 2023년 22%에서 2024년 25%에 육박할 것이라는 예측도 있습니다.

전반적으로 미국의 전력 및 유틸리티 부문은 실질적인 법적 지원과 기록적인 투자에 힘입어 탈탄소화 및 청정에너지 도입에 큰 진전을 이루었습니다. 공급망 문제와 전력량 감소가 예상되지만, 전력 부문은 2024년까지 안정적인 전력 가격 및 전력량 증가를 위해 준비하면서 야심찬 탄소 감축 목표를 달성하기 위한 모멘텀을 지속할 수 있도록 준비하고 있습니다.

미국의 EPCM 시장은 여러 대형 다국적 기업의 존재와 대규모 인수합병 활동으로 인해 중간 정도의 시장 집중도를 보이고 있습니다. 경쟁 환경은 역동적이며, 지속적인 기술 발전과 정부 정책이 시장 구조를 형성하고 있습니다. 이 부문의 주요 기업으로는 Fluor Corporation, McDermott International Ltd, Jacobs Engineering Group, Bechtel Corporation, Kiewit Corporation 등이 있습니다.

The US Engineering, Procurement, And Construction Management Market size is estimated at USD 321.77 billion in 2025, and is expected to reach USD 646.08 billion by 2030, at a CAGR of 14.96% during the forecast period (2025-2030).

The engineering, procurement, and construction management (EPCM) market in the United States plays a pivotal role in the nation's infrastructure and industrial landscape. It boasts multi-billion dollar revenues and a consistent growth trajectory, primarily fueled by substantial investments in infrastructure upgrades, renewable energy ventures, and industrial expansions. Notably, government initiatives, exemplified by the Infrastructure Investment and Jobs Act, channel significant capital into transportation, utilities, and the burgeoning smart city sector. Furthermore, the nation's pivot toward sustainable energy, encompassing wind, solar, and energy storage, bolsters the project pipeline for EPC firms. This momentum is further fueled by the imperative for modernizing manufacturing plants and the expanding need for healthcare and data center infrastructure.

Despite its promising outlook, the US EPC market grapples with challenges that could impede its growth. Regulatory intricacies, labor scarcities, escalating material prices, and inflationary pressures pose notable hurdles. However, amid these obstacles, the market presents a range of opportunities, especially in the realms of smart infrastructure, renewable energy, and cutting-edge manufacturing. Noteworthy industry players like Bechtel, Fluor, and Jacobs Engineering are at the forefront, harnessing technologies like building information modeling (BIM), IoT, and AI to elevate project efficiency and sustainability. Therefore, the US EPC market is poised for further expansion, buoyed by governmental backing, technological strides, and an escalating appetite for contemporary infrastructure.

Infrastructure investment in the United States, especially in the engineering, procurement, and construction (EPC) sector, is pivotal for economic growth and modernization. The country is channeling significant funds into enhancing transportation networks, public utilities, and other crucial infrastructure to keep pace with a growing population and advancing technology.

In 2023, the President and Transportation Secretary unveiled that the Biden-Harris Administration had allocated nearly USD 1.2 billion from the new National Infrastructure Project Assistance (Mega) discretionary grant program to nine national projects. These initiatives aim to bolster the economy, create well-paying jobs, fortify supply chains, enhance resident mobility, and elevate the safety of the transportation systems.

The Mega grant initiative, a product of President Biden's landmark infrastructure legislation, is tailored for projects that outstrip conventional funding programs in scale or complexity. Eligible ventures include highways, bridges, ports, and public transportation.

By 2026, the Mega program is expected to infuse a total of USD 5 billion into revamping the US infrastructure, with a focus on benefiting current and future generations. In the latest application round, the US Department of Transportation fielded requests totaling around USD 30 billion, far surpassing the available USD 1 billion in 2022. Notable projects include:

USD 292 million for Hudson Yards Concrete Casing, Section 3 (New York): This funding will complete the final section of the concrete casing, securing the right-of-way for the new Hudson River Tunnel and setting the stage for the Gateway Project. The Hudson Tunnel initiative, upon fruition, promises improved commute times, enhanced Amtrak reliability on the Northeast Corridor (NEC), and a boost to the regional economy, which houses 17% of the US population. Amtrak anticipates the project will create 72,000 jobs during construction, with a focus on union partnerships for job training.

USD 250 million for Brent Spence Bridge improvements (Cincinnati, OH, and Covington, KY): This vital freight corridor, spanning the Ohio River, witnesses over USD 400 billion in annual freight movement and is notorious for its truck bottlenecks. The Mega grant will facilitate essential upgrades to the Brent Spence Bridge and the construction of a new bridge alongside the existing one, aimed at alleviating congestion and enhancing travel time reliability, thus bolstering the regional economy.

Overall, infrastructure investment in the United States, especially in the EPC sector, is pivotal in driving economic growth and modernization. The Biden-Harris Administration's commitment is evident in allocating nearly USD 1.2 billion from the National Infrastructure Project Assistance (Mega) discretionary grant program. Noteworthy projects like the Hudson River Tunnel and Brent Spence Bridge highlight the administration's focus on bolstering transportation networks, job creation, and supply chain resilience. With the Mega program eyeing a USD 5 billion investment by 2026, the nation is poised to witness enhanced mobility, safety, and economic robustness, benefiting current and future generations.

In 2023, the US power and utilities sector significantly advanced its decarbonization efforts, achieving record solar and energy storage installations. This progress, bolstered by pivotal clean energy and climate legislation, continued into 2024. While the sector's fundamentals were a mixed bag, electricity sales were forecasted to dip by approximately 1.2% YoY by the end of 2023, primarily due to a mild winter. Supply chain challenges began to ease, yet persistent shortages of key materials like steel and transformers disrupted operations and drove up costs.

Many regions saw a drop in wholesale electricity prices, largely attributed to a 53% YoY decrease in natural gas costs for power generation in 2023. However, since not all utilities procure electricity from wholesale markets and fuel expenses are just one component of customer bills, the correlation with price movements may not be direct. In 2023, major electric and gas utilities collectively spent nearly USD 171 billion on grid modernization and decarbonization, setting a new record. Coupled with anticipated future spending and rising interest rates, these high capital outlays could translate to increased customer bills.

In 2024, electricity prices are anticipated to hold steady, while sales are projected to increase by around 2%. Supply chain disruptions are expected to resolve gradually. The momentum for clean energy initiatives, supported by various catalysts, is likely to persist. A growing number of US electric firms have accelerated their carbon reduction targets, aiming for an 80% cut by 2030, shifting from the previous "net zero by 2050" goal. By August 2023, on the first anniversary of the Inflation Reduction Act (IRA), investors had already earmarked over USD 122 billion for clean energy generation and an additional USD 110 billion for bolstering domestic clean energy manufacturing.

In 2023, the Infrastructure Investment and Jobs Act (IIJA) allocated billions for enhancing grid reliability, battery supply chains, EV programs, and energy efficiency. The US Energy Information Administration (EIA) expected a significant surge in utility-scale solar installations of more than doubling to 24 gigawatts in 2023, followed by an additional 36 GW in 2024. Its projections also indicated a rise in the renewable electricity share from 22% in 2023 to nearly 25% in 2024.

Overall, the US power and utilities sector made significant strides in decarbonization and clean energy adoption, supported by substantial legislative backing and record investments. Despite facing supply chain challenges and a forecasted dip in electricity sales, the sector is poised for steady electricity prices and increased sales in 2024, with continued momentum toward ambitious carbon reduction goals.

The US EPCM market exhibits moderate market concentration, driven by the presence of several large multinational firms and significant merger and acquisition activities. The competitive landscape is dynamic, with ongoing technological advancements and government policies shaping the market structure. Prominent entities in this sector include Fluor Corporation, McDermott International Ltd, Jacobs Engineering Group, Bechtel Corporation, and Kiewit Corporation.