유럽의 냉동식품 포장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Europe Frozen Food Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1629763

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

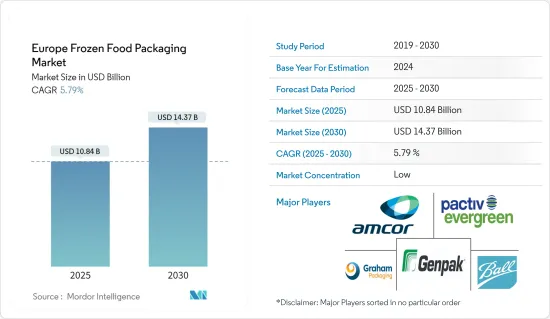

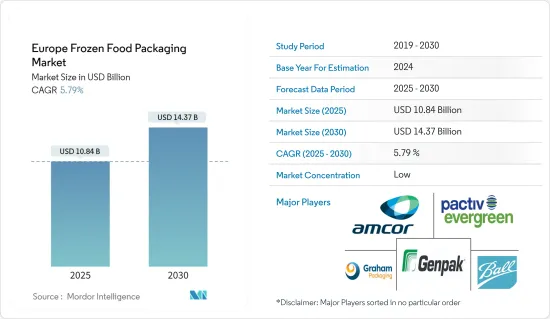

유럽의 냉동식품 포장 시장 규모는 2025년 108억 4,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 5.79%의 CAGR로 2030년에는 143억 7,000만 달러에 달할 것으로 예상됩니다.

도시화의 급속한 발전과 빠르게 변화하는 라이프스타일로 인해 소비자의 취향은 전통적인 가정식보다 조리 시간이 짧은 냉동식품으로 옮겨가고 있습니다.

주요 하이라이트

식품 품질에 대한 소비자의 기대치가 높아지면서 냉동식품 포장에 대한 수요가 증가하고 있습니다. 또한 제품 품질에 대한 소비자의 평가도 시장 성장을 촉진하는 요인입니다. 또한, 경제 및 라이프스타일의 변화로 인해 유럽에서 냉동 식품 포장에 대한 수요가 증가하고 있습니다. 이 시장은 예측 기간 동안 높은 성장률을 보일 것으로 예상됩니다.

최근 새로운 포장 기술도 개발되어 냉동 식품 포장을 더욱 실용적이고 안전하게 만들고 있습니다. 이러한 기술에는 지능형 패키징, 활성 포장, 엔지니어링 과학 등이 있습니다. 환경 오염을 줄이고 정부 규제를 준수하기 위해 기업들은 재활용, 재생, 재사용이 가능한 생분해성 포장재를 사용하여 환경 친화적인 포장에 초점을 맞추고 있습니다.

또한, 편의성은 전 세계적으로 냉동식품 소비를 증가시키는 주요 요인 중 하나입니다. 이에 따라 주요 기업들은 소비자의 지역적 선호도를 충족시키기 위해 새로운 유형과 원재료를 도입하고 있습니다. 편의성 제품에 대한 소비자의 선호도가 높아짐에 따라 처음부터 조리하는 것보다 조리 과정이 간단하고 시간을 절약할 수 있는 냉동 제품에 대한 수요가 증가하고 있습니다.

또한, 노동 인구의 바쁜 라이프스타일 증가로 인해 냉동 스낵 식품 시장이 빠르게 성장하고 있으며, 이는 냉동 스낵 시장을 촉진하고 냉동 식품 포장 시장의 수요를 촉진하고 있습니다.

그러나 유럽 시장은 유럽위원회와 같은 기관의 식품 포장 유형 및 접촉 재료에 대한 엄격한 규제로 인해 앞으로도 높은 규제가 지속될 것으로 예상됩니다. 냉동식품 포장은 오염, 수분 침투, 온도 변동을 방지하고 공급망 전반에 걸쳐 식품의 품질과 안전성을 유지하기 위해 견고한 솔루션이 필요합니다.

유럽의 냉동식품 포장 시장 동향

플라스틱이 큰 시장 점유율을 차지

유럽에서는 편리성, 보존성, 비용 효율성에 힘입어 냉동식품 분야에서 플라스틱 포장에 대한 수요가 급증하고 있습니다. 플라스틱 포장은 소비자들이 바로 먹을 수 있는 식사와 냉동 간식에 대한 선호도가 높아지면서 더욱 각광받고 있습니다. 밀폐성은 냉동 식품에 필수적인 제품의 유통기한을 크게 연장시켜줍니다. 습기, 냉동 화상 및 산화를 방지하는 것은 맛, 질감 및 영양가를 유지하는 데 가장 중요합니다. 유럽에서는 가볍고 사용하기 편리하며 식품의 품질 유지에 도움이 되는 유연한 플라스틱 필름, 봉지, 파우치가 인기를 끌고 있습니다.

소비자 라이프스타일의 변화는 유럽 냉동식품 시장의 성장을 더욱 촉진하고 있습니다. 현대 생활의 번잡함에 따라 많은 유럽인들은 편리함과 유통기한 연장을 위해 냉동식품을 선호하고 있으며, 1회용 플라스틱 포장의 등장은 1회용 플라스틱 포장의 등장으로 인해 1회 제공량을 조절하고 음식물 쓰레기를 최소화하며, 유럽 소비자들의 환경보호에 대한 인식이 높아진 것과 일치하고 있습니다. 또한, 유럽에서 E-Commerce와 온라인 식료품 쇼핑이 급증하면서 운송 중 냉동 제품의 무결성을 보장하는 견고하고 내구성이 뛰어난 포장에 대한 수요가 증가하고 있습니다.

그러나 플라스틱의 장점이 더욱 두드러짐에 따라 환경 문제가 점점 더 유럽의 수요 상황을 형성하고 있습니다. 이에 따라 많은 유럽 국가들이 플라스틱 폐기물을 억제하고 지속가능한 포장을 지지하는 규제를 마련하고 있으며, EU의 지속가능성 서약은 단순한 약속이 아니라 포장 분야의 혁신을 촉진하는 촉매제가 되고 있습니다. 그 결과, 재활용 가능한 플라스틱, 생분해성 플라스틱, 식물성 플라스틱과 같은 발전이 이루어졌습니다. 소비자들의 환경에 대한 인식이 높아짐에 따라 제조업체들은 대체 소재를 찾고 있습니다. 그 목적은 무엇일까? 냉동식품 포장에 있어 플라스틱이 제공하는 본질적인 기능과 품질을 유지하면서 규제 의무와 소비자 요구를 충족시키는 것입니다.

유럽의 밀레니얼 세대가 냉동 식품 포장에 대한 수요를 주도하고 있으며, 1인분 또는 테이크아웃 옵션을 선호합니다. 밀레니얼 세대는 편의성, 양 조절, 빠른 식사를 중요시하기 때문에 플라스틱 포장이 필수적입니다. 1인분 용기와 플렉서블 파우치는 식품의 신선도와 안전성을 유지하면서 이러한 니즈를 충족시켜 냉동식품 포장에 대한 플라스틱 수요를 촉진하고 있습니다.

독일 냉동식품협회(German Frozen Food Institute)에 따르면 독일의 냉동식품 소비가 증가하고 있으며, 2020년 101억 7,000만 달러에서 2023년 125억 9,000만 달러로 증가할 것으로 예상했습니다. 이 추세는 냉동 식품이 바쁜 소비자의 주식이 된 유럽 전역의 변화를 반영합니다. 매출 증가는 플라스틱 포장에 대한 수요를 직접적으로 증가시킬 것이며, 플라스틱 포장은 품질 유지와 유통기한 연장에 필수적입니다.

냉동식품에 대한 수요가 증가함에 따라 제조업체들은 다층 필름, 트레이, 파우치 등 플라스틱 솔루션의 다재다능함과 비용 효율성으로 인해 플라스틱 솔루션에 의존하고 있습니다. 재활용이 가능하고 지속가능한 포장재에 대한 혁신은 환경적 책임을 중시하는 유럽의 움직임에 부응하기 위해 생겨나고 있습니다.

봉지 포장 유형이 시장 성장을 주도

밀폐 밀봉에 대한 수요가 증가하는 배경에는 아로마를 포함한 제품의 품질을 장기간 유지하는 높은 차단성을 가진 가방에 대한 요구가 있습니다. 또한 재밀봉 및 재밀봉이 가능한 포장에 대한 수요로 인해 지퍼백은 조사 대상 시장에서 점점 더 보편화되고 있습니다. 공간 절약형 포장 형태로 인해 기업들은 지퍼백을 선택하고 있으며, 이는 조사 대상 시장에서 이 부문의 성장을 촉진하고 있습니다. 또한, 플라스틱 백이 제공하는 유연성, 찢어짐 방지, 투명성, 방습성 등의 특성은 시장 성장을 더욱 가속화할 것으로 예상됩니다.

또한 동종업계는 50% 재활용 플라스틱으로 만든 새로운 고급 스낵 포장재를 출시하는 데 주력하고 있습니다. 예를 들어, 2024년 3월 펩시콜라(PepsiCo)가 영국과 아일랜드의 썬바이트(Sunbites) 스낵 브랜드에 50% 재활용 플라스틱을 사용한 새로운 고급 스낵 포장재를 출시하는 데 INEOS가 중요한 역할을 했습니다. 첨단 재활용 공정을 통해 생산된 이 패키지는 식품 접촉 포장에 대한 EU의 엄격한 규제 기준을 충족합니다.

이 이정표를 달성하기 위해 유연한 식품 포장 공급망 전반에 걸쳐 다양한 파트너가 협력하여 GreenDot은 소비자 플라스틱 포장 폐기물을 제공하고 Plastic Energy의 기술을 통해 TACOIL로 전환되었습니다. INEOS는 이 열분해 오일을 이용하여 재생 프로필렌과 버진 품질의 재생 폴리프로필렌 수지를 생산했고, IRPLAST는 이 수지를 사용하여 50% 재활용 원료로 포장용 필름을 생산했으며, Amcor는 PepsiCo를 위해 이 필름을 인쇄했습니다. 이 파트너십은 2030년까지 포장재에서 화석 유래 플라스틱을 제거하겠다는 펩시콜라의 약속에 따른 것입니다.

또한, 온라인 식료품 쇼핑이 증가함에 따라 운송 중 냉동 제품의 신선도를 유지시켜주는 포장 솔루션에 대한 수요가 증가하고 있습니다. 편리한 식사 준비에 대한 소비자의 선호는 반찬, 채소, 과일, 디저트 등 냉동식품에 대한 수요 증가를 견인하고 있습니다.

봉지 형태는 냉동 스낵의 정확한 분량 관리를 가능하게 하고, 소비 관리를 용이하게 하고, 식품 폐기물을 최소화할 수 있습니다. 캐나다 농업식품부에 따르면 2023년 영국의 스낵류 소매 매출은 143억 7,290만 달러로 1위, 프랑스, 이탈리아, 기타 유럽 국가들이 그 뒤를 이었습니다.

유럽의 냉동식품 포장 산업 개요

편의성과 다용도성으로 인해 냉동식품을 선호하는 소비자가 증가하면서 이 지역의 시장 성장을 촉진하고 있습니다. 혁신적인 포장 형태와 포장재도 소비자 경험을 개선하고 폐기물을 최소화하는 데 도움을 주고 있습니다.

유럽의 냉동식품 포장 시장은 단편화되어 있으며, Genpack LLC, Graham Packaging Company, Ball Corporation, Pactiv LLC, Amcor Group 등 여러 대기업으로 구성되어 있습니다. 이 지역의 기업들은 냉동식품을 위한 지속가능한 포장재 출시에 주력하고 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 소개

조사 가정과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

산업 밸류체인 분석

업계의 매력 - Porter's Five Forces 분석

공급 기업의 교섭력

구매자의 교섭력

신규 참여업체의 위협

대체품의 위협

경쟁 기업 간의 경쟁 강도

세계의 냉동식품 포장 시장 개요

제5장 시장 역학

시장 성장 촉진요인

소비자에 의한 컨비니언스 포장에 대한 수요 상승

유럽의 가처분 소득 증가와 소비자 행동 변화

시장 성장 억제요인

정부 규제와 개입에 의한 시장 제한

제6장 시장 세분화

재료 유형별

유리

종이

금속

플라스틱

기타

제품 유형별

백

박스

터브와 컵

트레이

파우치

기타 제품 유형

식품 유형별

즉석 조리 식품

야채·과일

육류

해산물

제빵 제품

기타 식품

국가별

영국

독일

프랑스

스페인

이탈리아

제7장 경쟁 구도

기업 개요

Pactiv LLC

Amcor Group

Genpak LLC

Graham Packaging Company, Inc.

Ball Corporation Inc

Crown Holdings

Tetra Pak International

Placon Corporation

Toyo Seikan Group Holdings, Ltd.

WestRock Company

Sealed Air Corporation

Berry Global Inc.

제8장 투자 분석

제9장 시장 전망

ksm

영문 목차

영문목차

The Europe Frozen Food Packaging Market size is estimated at USD 10.84 billion in 2025, and is expected to reach USD 14.37 billion by 2030, at a CAGR of 5.79% during the forecast period (2025-2030).

The rapid growth of urbanization and fast-paced lifestyles have shifted consumers' preferences toward frozen food products, which require less time for cooking than traditional home-cooked meals.

Key Highlights

The rise in consumer expectations related to food quality has propelled the demand for frozen food packaging. Also, consumer appreciation of the product quality is another factor driving the market growth. Additionally, with changes in the economy and lifestyles, there is an increased demand for frozen food packaging in Europe. The market is expected to grow lucratively during the forecast period.

New packaging technologies have also developed recently, making packaging for frozen food products more practical and secure. These technologies include intelligent packaging, active packaging, and engineering science. To reduce environmental pollution and comply with government regulations, companies focus on eco-friendly packaging by employing biodegradable packaging materials that can be recycled, regenerated, and reused.

Furthermore, convenience is one of the primary factors driving the global increase in frozen food consumption. As a result, leading players are introducing new types and ingredients to cater to consumers' regional tastes. The growing consumer preference for convenience products fuels the increasing demand for frozen products due to their ease of preparation and time savings compared to cooking from scratch.

Moreover, the frozen snacks food market is expanding rapidly due to the increasing volume of the hectic lifestyle of the working population, which is boosting the frozen snacks market and propelling the demand for the frozen food packaging market.

However, the European market is anticipated to remain highly regulated, owing to stringent regulations regarding food packaging types and contact materials by agencies such as the European Commission. Frozen food packaging requires robust solutions to maintain food quality and safety across the supply chain by preventing contamination, moisture intrusion, and temperature fluctuations.

Europe Frozen Food Packaging Market Trends

Plastic to Hold Significant Market Share

In Europe, a surge in demand for plastic packaging in the frozen food sector is evident, spurred by convenience, preservation, and cost-effectiveness. Plastic packaging stands out as consumers gravitate towards ready-to-eat meals and frozen snacks. Its airtight seal capability significantly extends product shelf life, a vital feature in frozen food. Safeguarding against moisture, freezer burn, and oxidation is paramount to preserving taste, texture, and nutritional value. In Europe, flexible plastic films, bags, and pouches have gained traction, offering food quality preservation while being lightweight and user-friendly.

Changing consumer lifestyles have further propelled the growth of Europe's frozen food market. With the hustle and bustle of modern life, many Europeans are gravitating towards frozen foods for convenience and extended shelf life. The rise of single-serve plastic packaging caters to portion control and minimizes food waste, aligning with the heightened environmental awareness among European consumers. Moreover, the burgeoning e-commerce and online grocery shopping scene in Europe amplifies the demand for robust, durable packaging, ensuring the integrity of frozen products during transit.

Yet, as the advantages of plastic become more pronounced, environmental concerns increasingly shape Europe's demand landscape. In response, numerous European nations are rolling out regulations to curb plastic waste and champion sustainable packaging. The EU's sustainability pledge is not just a commitment but a catalyst, spurring innovations in the packaging domain. This has birthed advancements like recyclable, biodegradable, and even plant-based plastics. With a growing environmental consciousness among consumers, manufacturers are searching for alternative materials. Their goal? To align with regulatory mandates and consumer desires, all while preserving the essential functionality and quality plastic offers in frozen food packaging.

Europe's Millennials drive demand for frozen food packaging, favoring single-serving and on-the-go options. They value convenience, portion control, and quick meals, making plastic packaging essential. Single-serve containers and flexible pouches meet these needs while keeping food fresh and secure, fueling demand for plastic in frozen food packaging.

According to the German Frozen Food Institute, Germany's frozen food consumption is rising, with retail revenue growing from USD 10.17 billion in 2020 to USD 12.59 billion in 2023. This trend reflects a broader European shift, where frozen foods are staples for busy consumers. Increased sales directly boost demand for plastic packaging, which is crucial for preserving quality and extending shelf life.

As frozen food demand grows, manufacturers rely on plastic solutions like multi-layer films, trays, and pouches for their versatility and cost-effectiveness. Innovations in recyclable and sustainable packaging are also emerging to address Europe's focus on environmental responsibility.

Bags Packaging Type to Drive the Market Growth

The rising demand for airtight sealing is driven by the need for bags with high barrier properties, which retain product quality, including aroma, for a prolonged period. Furthermore, zippered bags are becoming more and more common in the market under study, driven by the demand for packaging that can be resealed and reclosed. Due to space-saving packaging formats, businesses choose bags, boosting the segment's growth in the market under study. Moreover, properties such as flexibility, tear-resistance, transparency, and moisture protection offered by plastic bags are expected to accelerate the market's growth further.

Additionally, in line with the same players are focusing on launching new, premium-quality snack packaging containing 50% recycled plastic. For instance, in March 2024, INEOS played a pivotal role in launching new, premium quality snack packaging containing 50% recycled plastic, which PepsiCo introduced for their Sunbites snack brand in the UK and Ireland. This packaging, made through advanced recycling processes, meets strict EU regulatory standards for food contact packaging.

Various partners collaborated across the flexible food packaging supply chain to achieve this milestone. GreenDot provided post-consumer plastic packaging waste, which was converted into TACOIL by Plastic Energy's technology. INEOS utilized this pyrolysis oil to produce recycled propylene and virgin-quality recycled polypropylene resin. IRPLAST used this resin to create packaging films with 50% recycled materials, while Amcor printed these films for PepsiCo. This partnership aligns with PepsiCo's commitment to eliminating fossil-based plastic in its packaging by 2030.

Moreover, the growth in online grocery shopping has increased demand for packaging solutions such as bags that maintain frozen product freshness during transportation. Consumer preference for convenient meal preparation has driven increased demand for frozen foods, including ready meals, vegetables, fruits, and desserts.

The bag format enables precise portion control for frozen snacks, facilitating consumption management and minimizing food waste. According to Agriculture and Agri-Food Canada, the retail sales of snacks in the United Kingdom in 2023 took first position with USD 14,372.9 million sales, followed by France, Italy, and many other countries across Europe.

Europe Frozen Food Packaging Industry Overview

Rising consumer preference for frozen foods due to their convenience and versatility is driving the market growth in the region. Innovative packaging formats and materials are also helping to improve consumer experience and minimize waste.

The European frozen Food packaging market is fragmented and consists of several major players, such as Genpack LLC, Graham Packaging Company, Ball Corporation, Pactiv LLC, and Amcor Group. Players in the region are also focusing on launching sustainable packaging materials for frozen food.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Force Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Buyers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Overview of the Global Frozen Food Packaging Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Demand for Convenience Packaging by Consumers

5.1.2 Increase in Disposable Income and Changing Consumer Behavior in Europe

5.2 Market Restraint

5.2.1 Government Regulations and Interventions limit the Market