ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

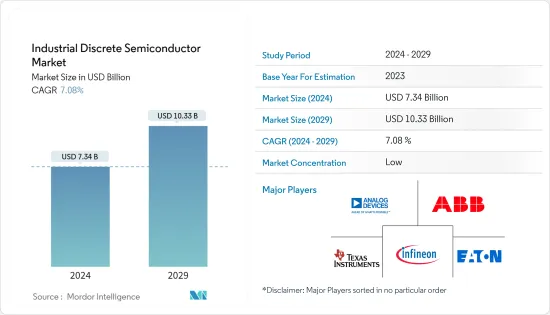

산업용 디스크리트 반도체 시장 규모는 2024년에 73억 4,000만 달러로 추정되고, 2029년에는 103억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029)의 CAGR은 7.08%로 성장할 전망입니다.

주요 하이라이트

산업용 디스크리트 반도체는 산업 장비, 제조 장비, 기계, UPS 등에 널리 사용됩니다. 산업 분야에서 디스크리트 반도체의 주요 용도는 지게차, 무정전 전원 공급 장치(UPS) 시스템, 태양광 인버터 등의 대형 배터리 구동 용도, 전동 공구와 같은 소형 전원 구동 시스템입니다. 또한 전력 조정, 모터 제어, 센서 인터페이스 등 산업 공정에서 정밀한 제어 및 자동화도 가능합니다.

산업용 시스템의 효과를 극대화하려면 개별 구성 요소가 필수적입니다. 이러한 특정 부품은 자동화 시스템의 다양한 부분에 안정적인 에너지 공급을 보장합니다. 또한 산업용 자동화 시스템의 속도와 기능성을 향상시킵니다. 게다가 그 적응성은 전반적인 성능을 향상시키기 위한 간단한 사용자 정의를 가능하게 합니다.

산업용 사물인터넷과 인더스트리 4.0은 스마트 공장 자동화이라고도 불리는 완전한 물류 프로세스의 진보, 제조, 감독에 매우 중요합니다. 이러한 기술은 인터넷을 통해 기계와 장치의 연결을 용이하게하기 위해 현재 산업 부문을 이끌고 있습니다.

스마트 공장은 산업 분야에서 또 다른 눈에 띄는 동향입니다. 스마트 공장은 생산성을 크게 향상시키고 획기적인 혁신과 기술 투자를 통해 산업계가 새로운 시장에 접근할 수 있도록 도와줍니다. 공장 자동화에 대한 정부 투자 증가도 이 동향을 뒷받침하고 있습니다.

예를 들어, 미국 정부는 2023년 10월 미국의 중소 시설에서 스마트 제조업을 지원하기 위해 2,200만 달러를 투자할 것이라고 발표했습니다. 대통령의 초당파 인프라법(Bipartisan Infrastructure Act)이 자금원이 되는 동정권의 제조 리더십 프로그램은 미국의 탄소 배출량의 1/6 이상을 차지하는 국내 제조 부문으로 스마트 제조 기술과 고성능 컴퓨팅 잉을 보다 이용하기 쉽게 하는 것을 목적으로 하고 있습니다.

IC나 마이크로칩으로도 알려진 집적회로 수요가 산업분야에서 높아지고 있는 것이 시장의 성장을 더욱 방해할 것으로 보입니다. IC 또는 마이크로칩이라고도 불리는 집적 회로는 복수의 전자 회로를 하나의 반도체 기판에 집적한 전자 부품입니다. 한편, 디스크리트 반도체는 전류 조정, 신호 증폭, 스위칭 등 특정 기능을 수행하도록 설계된 전자 부품입니다.

러시아와 우크라이나의 분쟁은 현저한 가격 상승을 일으켜 산업용 디스크리트 반도체 제조에 필수적인 원재료의 입수를 제한하고 있습니다. 또한 미국과 중국의 긴장 격화는 마이크로칩과 원재료 부족을 초래하고 있습니다. 엔지니어링 공급망의 혼란은 광범위하게 영향을 미치고 제품 가용성에 영향을 미치며 업계 전반에 걸쳐 비용이 급격히 상승하고 있습니다.

산업용 디스크리트 반도체 시장 동향

파워 트랜지스터 부문이 큰 시장 점유율을 차지

산업용 디스크리트 반도체는 높은 효율과 성능 향상을 실현하기 때문에 수요가 증가하고 있습니다. 디스크리트 반도체는 고전류 및 고전압 관리가 필요한 상황에서 중요한 위치를 차지합니다.

IGBT 및 MOSFET과 같은 파워 트랜지스터가 모터 드라이브에 통합됨에 따라 모터 드라이브의 효율이 높아지고 있습니다. 특히 실리콘 카바이드(SiC) MOSFET은 모터 드라이브의 파워 스테이지에서 점점 더 많이 사용되고 있습니다. IGBT와 SiC MOSFET은 고전류 및 고전압 정격으로 고전력 AC 파워 스테이지 용도에 적합합니다.

그러나 SiC MOSFET은 스위칭 주파수 요구 사항에서 IGBT와 다릅니다. IGBT가 낮은 스위칭 주파수 범위에서 동작하는 반면, SiC MOSFET은 훨씬 높은 스위칭 주파수 범위에서 동작합니다. 더 높은 주파수에서 스위칭하면 전력 밀도, 효율, 방열과 같은 시스템의 이점을 얻을 수 있습니다.

급속히 발전하는 Industry 4.0의 동향은 시장 진출기업에 많은 기회를 가져오고 있으며, 이는 모터 구동 용도에서 IGBT의 요구를 촉진하는 요인 중 하나입니다. 많은 기업들이 운영을 간소화하고 생산량을 향상시키기 위해 기존 모터를 첨단 모터 드라이브로 교체하고 있습니다.

예를 들어 2023년 7월, Nexperia는 30A NGW30T60M3DF를 필두로 하는 일련의 600V 디바이스를 발표하여 절연 게이트 바이폴라 트랜지스터(IGBT) 시장에 진출했습니다. 이러한 디바이스는 전력 변환, 모터 구동, UPS, 20kHz에서 5kW-20kW의 서보 모터, 로봇, 그리퍼, 엘리베이터, 전력 인버터, 태양광 발전 스트링, 유도 가열 및 용접 등의 산업용도 등 다양한 용도로 전력 밀도를 높이기 위해 설계되었습니다.

세계 산업 부문은 현저한 동향으로 자동화 증가를 목격하고 있으며, 그 결과, 이 시장에서 사업을 전개하는 벤더에게 새로운 기회가 탄생하고 있습니다. 산업 로봇 연맹에 따르면 산업용 로봇 수요는 세계적으로 안정적인 성장을 이루고 있습니다. 예를 들어 전년도 세계의 산업용 로봇 시장은 7% 성장해 세계에서 59만대 이상이 될 것으로 예상되고 있습니다.

마찬가지로 vdma.org에 따르면 지난해 독일 로봇 산업과 자동화 산업은 국내와 수출을 합쳐 약 175억 8,000만 달러의 매출을 기록해 전년보다 증가할 것으로 예측되고 있습니다.

중국이 큰 시장 점유율을 차지할 전망

중국 경제는 수년에 걸쳐 큰 변화를 경험해 왔습니다. 중국 정부가 실시한 정책은 경제의 고부가가치화를 목표로 다양한 산업의 성장을 가속하는데 중요한 역할을 해왔습니다.

중국의 산업 부문의 급속한 확대는 이 나라를 세계 제조업에서 중요한 기업으로 자리매김하게 했습니다. 이 분야의 성장을 계속 촉진하기 위해 중국 정부는 최근 '메이드 인 차이나 2025' 구상 등 다양한 전략을 실시했습니다. 이 프로그램은 생산 효율성을 높이고 국제 품질 기준을 유지하기 위해 산업 기업의 첨단 기술 채택을 촉진하는 것을 목표로합니다.

마찬가지로 2024년 4월 중국 산업정보화부(MIIT)와 다른 6개 부서는 산업 부문에서 설비 갱신을 추진하기 위한 실시 계획을 발표했습니다.

중국 제조업의 산업 설비 갱신 이니셔티브의 범위는 광범위하고, 구식 설비, 특히 10년 이상 사용되고 있는 공작기계의 대체, 항공우주, 태양에너지, 배터리 제조 등의 중요한 분야의 설비 강화, 산업용 로봇과 산업용 인터넷의 통합, 환경의 지속가능성을 촉진하는 그린 기술의 채용 등 다양한 측면을 커버하고 있습니다. 그 결과 이러한 신흥국 시장의 개척이 새로운 기회를 창출할 것으로 기대되고 있습니다.

2023년 세계 로봇 회의 보고서에 따르면 중국의 로봇 산업은 눈부신 발전을 이루고 있습니다. 2022년 이 산업의 매출은 1,700억 위안(233억 달러 상당)을 넘어섰습니다. 또한 중국의 산업용 로봇 매출은 2022년 세계 시장 점유율의 절반 이상을 차지하며 10년 연속 세계 최고 자리를 유지하고 있습니다.

중국의 특징은 산업 활동의 활성화와 제조업 증가입니다. 예를 들어, 중국 국가 통계국의 데이터에 따르면, 2023년, 중국의 산업 부문은 국가의 GDP에 약 31.7% 기여해, 경제 성장의 주요 엔진으로서 기능했습니다. 세계 2위 경제대국인 중국이 산업부문에서만 독일의 경제 전체를 웃도는 가치를 창출하고 있다는 것을 강조하는 것은 필수적입니다.

산업용 디스크리트 반도체 산업 개요

산업용 디스크리트 반도체 시장은 단편화되어 있으며 여러 기업로 구성되어 있습니다. 이 시장에 진입하고 있는 기업은 신제품의 투입, 사업의 확대, 전략적 인수 및 합병, 제휴, 협력 관계의 체결 등에 의해 시장에서의 존재감을 높이려고 끊임없이 노력하고 있습니다. 주요 공급업체로는 ABB Ltd, Infineon Technologies AG, Texas Instruments Inc., Analog Devices Inc., Eaton Corporation PLC 등이 있습니다.

2024년 6월-Mitsubishi Electric Corporation은 최신 제품인 쇼트키 배리어 다이오드(SBD) 내장 탄화규소(SiC) 금속-산화막-반도체 전계 효과 트랜지스터(MOSFET) 모듈의 3.3kV/400A 및 3.3kV/200A 모델 출하를 시작했습니다. 이 모듈은 철도 차량 및 전력 시스템과 같은 헤비 듀티 산업 용도에 맞게 조정됩니다.

2024년 5월-Infineon Technologies는 SiC MOSFET의 개발 범위를 650V 미만의 전압으로 확장했습니다. 올해 초에 발표된 2세대(G2) 기술을 기반으로 하는 CoolSiCMOSFET 400V 제품군의 도입은 이 회사의 최신 제품입니다. 이 MOSFET의 새로운 라인업은 인피니언의 최근 PSU 로드맵을 따라 AI 서버의 AC/DC 스테이지에 특화된 것입니다. 서버 용도 외에도 이러한 디바이스는 인버터 모터 제어, 태양에너지 저장 시스템 및 SMPS에서도 목적을 수행합니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건 및 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도-Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

업계 밸류체인 분석

COVID-19의 부작용과 기타 거시 경제 요인이 시장에 미치는 영향

제5장 시장 역학

시장 성장 촉진요인

산업 자동화에 있어서의 고에너지 및 고전력 효율 디바이스 수요 증가

산업분야에 있어서의 오토메이션 및 로보틱스의 채용 증가

시장의 과제

집적회로 수요 증가

제6장 시장 세분화

유형별

다이오드

소신호 트랜지스터

파워 트랜지스터

MOSFET 파워 트랜지스터

IGBT 파워 트랜지스터

기타 파워 트랜지스터

정류기

사이리스터

지역별

미국

유럽

일본

중국

한국

대만

제7장 경쟁 구도

기업 프로파일

ABB Ltd

On Semiconductor Corporation

Infineon Technologies AG

STMicroelectronics NV

Toshiba Electronic Devices and Storage Corporation

NXP Semiconductors NV

Diodes Incorporated

Nexperia BV

Semikron Danfoss Holding A/S(Danfoss A/S)

Eaton Corporation PLC

Hitachi Energy Ltd(Hitachi Ltd)

Texas Instrument Inc.

Wolfspeed Inc.

Microchip Technology

Renesas Electronics Corporation

Mitsubishi Electric Corporation

Analog Devices Inc.

Vishay Intertechnology Inc.

Rohm Co. Ltd

Littelfuse Inc.

제8장 투자 분석

제9장 시장 기회 및 향후 동향

AJY

영문 목차

영문목차

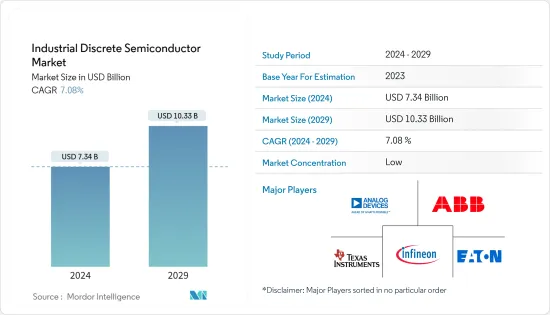

The Industrial Discrete Semiconductor Market size is estimated at USD 7.34 billion in 2024, and is expected to reach USD 10.33 billion by 2029, growing at a CAGR of 7.08% during the forecast period (2024-2029).

Key Highlights

Industrial discrete semiconductors are widely used in industrial equipment, manufacturing equipment and machines, UPS, etc. The primary use of discrete semiconductors in the industrial sector is in large battery-driven applications, such as forklifts, uninterruptible power supply (UPS) systems, solar inverters, and smaller power-driven systems, like power tools. They also enable precise control and automation in industrial processes, such as power regulation, motor control, and sensor interfacing.

It is essential to have individual components to maximize the effectiveness of industrial systems. These particular components guarantee a consistent energy supply to various parts of automated systems. Moreover, they boost the speed and functionality of industrial automation systems. In addition, their adaptability allows for simple customization to enhance overall performance.

The industrial Internet of Things and Industry 4.0 is pivotal in advancing, manufacturing, and supervising the complete logistics process, also called smart factory automation. These technologies are currently leading the way in the industrial sector, as they facilitate the connection of machinery and devices through the internet.

Smart factories are another prominent trend in the industrial sector. Smart factories help generate significant productivity gains and help industries make new markets accessible through breakthrough innovations and technological investments. The rising government investment in factory automation also supports the trend.

For instance, in October 2023, the government of the United States announced that it would invest USD 22 million to support smart manufacturing at small and medium-sized facilities across the nation. The administration's Manufacturing Leadership Program, funded by the President's Bipartisan Infrastructure Act, aims to make smart manufacturing technologies and high-performance computing more available in the domestic manufacturing sector, accounting for more than one-sixth of the US carbon emissions.

Rising demand for integrated circuits, also known as ICs or microchips, in the industrial sector will further hamper the market's growth. Integrated circuits, also known as ICs or microchips, are electronic components that integrate multiple electronic circuits onto a single semiconductor substrate. In contrast, discrete semiconductors are electronic components designed to carry out specific functions like regulating current flow, amplifying signals, and switching.

The conflict between Russia and Ukraine has caused a notable price surge, constraining the availability of raw materials essential for manufacturing industrial discrete semiconductors. Additionally, escalating tensions between the United States and China have resulted in shortages of microchips and raw materials. The disturbance in the supply chain for engineering has had widespread implications, impacting product availability and causing a sharp increase in costs throughout the industry.

Industrial Discrete Semiconductor Market Trends

Power Transistor Segment Holds the Significant Market Share

The demand for discrete semiconductors in the industrial sector is increasing as they offer high efficiency and performance improvements. They hold a crucial position in circumstances that require the management of high currents or voltages.

The efficiency of motor drives is increasing as power transistors like IGBTs and MOSFETs are incorporated into them. Particularly, silicon carbide (SiC) MOSFETs are increasingly used in the power stage for motor drives. Due to their high current and high voltage ratings, IGBTs and SiC MOSFETs fit well in high-power AC power stage applications.

SiC MOSFETs, however, differ from IGBTs in the switching frequency requirement. While IGBTs operate in a lower switching frequency range, SiC MOSFETs operate in a much higher switching frequency range. Switching at higher frequencies allows system benefits such as higher power density, efficiency, and heat dissipation.

The rapidly advancing trend of Industry 4.0 has created a stream of opportunities for market participants, which is one of the factors driving the need for IGBTs in motor drive applications. Many businesses continue replacing conventional motors with advanced motor drives to simplify operations and improve output.

For instance, in July 2023, Nexperia entered the insulated gate bipolar transistor (IGBT) market by introducing a series of 600 V devices led by the 30 A NGW30T60M3DF. These devices are designed to enhance power density in various applications, including power conversion, motor drives, and industrial uses such as UPS, servo motors ranging from 5kW to 20 kW at 20 kHz, robotics, grippers, elevators, power inverters, photovoltaic strings, and induction heating and welding.

The industrial sector across the globe is witnessing a rise in automation as a prominent trend, thus creating new opportunities for the vendors operating in the market. According to the Industrial Federation of Robotics, the demand for industrial robots is witnessing stable growth globally. For instance, in the previous year, the global market for industrial robots was expected to grow by 7% to more than 590,000 units worldwide.

Similarly, according to vdma.org, last year, the German robotics and automation industries were forecast to record a combined domestic and export turnover of around USD 17.58 billion, an increase from the year before that.

China is Expected to Hold the Significant Market Share

China's economy has experienced substantial changes throughout the years. The policies implemented by the Chinese government have played a crucial role in fostering growth across different industries, with the goal of advancing the economy to higher-value-added activities.

The rapid expansion of the industrial sector in China has positioned the country as a key player in global manufacturing. To continue fostering growth in this sector, the Chinese government has implemented various strategies in recent years, such as the 'Made in China 2025' initiative. This program aims to promote industrial companies' adoption of advanced technologies to improve production efficiency and uphold international quality standards.

Similarly, in April 2024, China's Ministry of Industry and Information Technology (MIIT) and six other departments released a notice unveiling the Implementation Plan for Advancing Equipment Renewal in the industrial sector.

The scope of China's initiative to upgrade industrial equipment in manufacturing is extensive, covering various aspects such as substitution of outdated equipment, particularly machine tools that have been in use for over a decade; enhancement of equipment in critical sectors like aerospace, solar energy, and battery manufacturing; integration of industrial robots and the industrial internet; and adoption of green technology to promote environmental sustainability. As a result, these developments are expected to create new opportunities within the market.

According to the 2023 World Robot Conference report, China's robotics sector has made remarkable advancements. In 2022, the industry generated a revenue of over 170 billion yuan (equivalent to USD 23.3 billion). Moreover, China's sales of industrial robots accounted for more than half of the global market share in 2022, maintaining its position as the top global leader for ten consecutive years.

China is characterized by a rise in industrial operations and an increase in manufacturing. For instance, data from the National Bureau of Statistics of China revealed that in 2023, China's industrial sector contributed around 31.7% to the nation's GDP, serving as the main engine of economic growth. It is essential to highlight that China, as the world's second-largest economy, produced more value from its industrial sector alone than the entire economy of Germany.

Industrial Discrete Semiconductor Industry Overview

The industrial discrete semiconductor market is fragmented and consists of several players. Companies in the market continuously try to increase their market presence by introducing new products, expanding their operations, or entering into strategic acquisitions and mergers, partnerships, and collaborations. Some of the major vendors include ABB Ltd, Infineon Technologies AG, Texas Instruments Inc., Analog Devices Inc., Eaton Corporation PLC, and many more.

June 2024: Mitsubishi Electric Corporation started shipping its newest products: a 3.3kV/400A and a 3.3kV/200A model of a Schottky barrier diode (SBD) integrated silicon carbide (SiC) metal-oxide-semiconductor field-effect transistor (MOSFET) module. These modules are tailored for heavy-duty industrial applications, such as rolling stock and electric power systems.

May 2024: Infineon Technologies broadened its SiC MOSFET development to cover voltages lower than 650 V. The introduction of the CoolSiCMOSFET 400 V family, based on the second-generation (G2) technology released earlier this year, marks the company's latest offering. This new lineup of MOSFETs is tailored explicitly for the AC/DC stage of AI servers, which is in line with Infineon's recent PSU roadmap. Apart from server applications, these devices also serve a purpose in inverter motor control, solar and energy storage systems and SMPS.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Rising Demand for High-energy and Power-efficient Devices in the Industrial Automation

5.1.2 Increasing Adoption of Automation and Robotics in the Industrial Sector

5.2 Market Challenges

5.2.1 Rising Demand for Integrated Circuits

6 MARKET SEGMENTATION

6.1 By Type

6.1.1 Diode

6.1.2 Small Signal Transistors

6.1.3 Power Transistors

6.1.3.1 MOSFET Power Transistors

6.1.3.2 IGBT Power Transistors

6.1.3.3 Other Power Transistors

6.1.4 Rectifier

6.1.5 Thyristor

6.2 By Geography

6.2.1 United States

6.2.2 Europe

6.2.3 Japan

6.2.4 China

6.2.5 South Korea

6.2.6 Taiwan

7 COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 ABB Ltd

7.1.2 On Semiconductor Corporation

7.1.3 Infineon Technologies AG

7.1.4 STMicroelectronics NV

7.1.5 Toshiba Electronic Devices and Storage Corporation