호주 및 뉴질랜드의 파우치 포장 시장은 식품 산업 수요 증가에 힘입어 괄목할 만한 성장세를 보이고 있습니다. 기존 포장에 비해 파우치 포장의 비용 효율성이 시장 성장을 주도하고 있습니다.

주요 하이라이트

파우치 포장은 운송 및 보관 중에 온도를 조절하고 산소를 제거하고 수분을 흡수하여 제품의 신선도를 유지합니다. 폴리에틸렌이나 폴리프로필렌과 같은 일반적으로 사용되는 재료는 포장의 빠른 분해를 보장합니다. 연포장은 식품, 음료, 퍼스널케어, 의약품 등 다양한 산업에서 사용할 수 있는 다목적성 때문에 다양한 산업에서 사용할 수 있습니다.

지난 10년간 호주의 인구가 급증하면서 특히 플라스틱 포장을 선호하는 소모품에 대한 수요가 증가했습니다. 이러한 선호는 주로 플라스틱의 가벼운 특성으로 인해 휴대성이 높아졌기 때문입니다. 소모품에는 음료, 포장된 식사, 전자 레인지 및 오븐 사용 가능 옵션을 포함한 편의성 패키지가 포함됩니다. 이러한 소비자 선호는 파우치 포장의 필요성을 증가시킬 수 있습니다.

호주는 이러한 추세에 발맞추어 야심찬 2025년 국가 포장 목표를 발표했습니다. 이 목표는 보다 지속가능한 포장 접근 방식을 향한 큰 진전이며, 시장 관계자와 정부의 광범위한 지지가 필요하며, 2025년 목표는 종합적이며, 호주의 모든 포장 활동을 대상으로 하며, 호주포장규약기구(APCO)가 그 실행을 주도하고 있습니다.

뉴질랜드의 식료품 및 식품 소매 부문은 계속 확대되고 있습니다. 미국으로부터의 수입품에는 포장 식품, 반려동물사료, 육류 등이 포함됩니다. 이로 인해 이 지역의 파우치 포장 시장에 대한 수요가 증가하고 있습니다.

또한 뉴질랜드의 소매 시장은 견고한 매출을 유지하고 있으며, 슈퍼마켓과 식료품 부문이 인플레이션의 우세에 힘입어 주도권을 쥐고 있습니다. 이 지역에서는 포장 시장도 문제에 직면했습니다. 뉴질랜드는 2023년 지속적인 물류 장애물, 금리 상승, 가계 지출 증가에 직면하여 개인 소비가 둔화될 조짐을 보이고 있습니다. 식료품 부문의 매출은 2023년에 감소했습니다.

ANZ 파우치 포장 시장 동향

E-Commerce의 편리한 패키지 상품에 대한 수요 증가

라이프스타일의 변화로 인해 이 지역의 파우치 포장 시장이 성장하고 있습니다. 이 시장에서는 1회 제공량 및 편리한 휴대용 팩에 대한 수요가 증가하고 있습니다. 호주의 식품 수출의 번영은 E-Commerce의 급증과 물류 강화에 기인합니다. 포장 시장의 브랜드들은 편의성을 중시하는 브랜드 경험을 강화하는 데 초점을 맞추었습니다.

Australia Post의 조사에 따르면 E-Commerce 부문이 빠르게 성장하고 있으며, 그 중 식품 및 주류는 온라인 구매의 20.6%를 차지하여 전년 대비 11.4% 증가한 것으로 나타났습니다. 또한 대형 소매점과 온라인 마켓플레이스를 포함한 매장은 온라인 구매의 18.1%를 차지해 전년 대비 8.6% 성장했습니다.

호주 제조업체들은 편리하고 연포장 솔루션을 채택하고 있으며, E-Commerce의 급증은 포장 시장을 재구성하고 게임 체인저가 되고 있습니다. 제조업체들은 보다 빠르고 안전한 제품 배송을 약속하는 연포장에 관심을 기울이고 있습니다.

Retail NZ에 따르면 2030년까지 온라인 구매가 뉴질랜드 전체 소매 매출의 20%를 차지할 것으로 예상됩니다. 소비자들은 원활한 쇼핑 여정을 기대하며 옴니채널 소매업에 대한 요구가 점점 더 커지고 있습니다. 전통적인 소매업체들은 경쟁력을 유지하기 위해 온라인 플랫폼에 우선순위를 두고 마케팅을 진행해야 합니다. 고객과의 소통을 위해 다양한 커뮤니케이션 채널을 도입하는 것이 표준 관행으로 자리 잡고 있습니다.

National Australia Bank에 따르면 2024년 4월 기준 국내 소매업체의 온라인 소매 지출 연간 성장률은 백화점이 38.7%로 가장 높았고, 개인 및 엔터테인먼트 산업이 12.6%, 식료품 및 주류가 10.7%로 그 뒤를 이었습니다. 가계는 변화하는 라이프스타일에 맞추어 경질 포장보다 부드러운 포장을 선호하고 있습니다. 소인 가구가 증가함에 따라 1회용 포장에 대한 수요가 증가하고 있습니다.

조리식품 및 식품산업이 큰 성장을 이룰 것으로 예상

호주에서는 노동 인구 증가와 직장 생활 역학의 발전에 힘입어 바로 먹을 수 있는 포장 식품이 인기를 끌고 있으며, CSIRO의 보고서에 따르면 2030년까지 조리 및 냉동 포장 식품의 국내 소비량은 소비 패턴과 인구 통계의 변화를 반영하여 37억 달러에 달할 것으로 예상됩니다. 미화 3.7억 달러에 달할 것으로 예상됩니다.

호주가 간편식 생산을 확대함에 따라 연포장에 대한 수요가 급증하고 시장 성장에 박차를 가하고 있습니다. 주둥이와 마개가 있는 연포장 파우치는 신선도와 풍미를 유지하며 다양한 고체 및 액체 식품을 담을 수 있습니다.

호주의 포장 시장은 주로 라이프스타일의 변화로 인해 휴대용 식품 포장에 대한 수요가 눈에 띄게 급증하고 있습니다. 또한 E-Commerce의 부상으로 인해 호주는 식품 거래에서 중요한 기업으로서의 입지를 확고히하고 있습니다. 호주 통계청에 따르면 2020년 식품 소매업의 연간 매출액은 1,515억 5,500만 호주 달러로 2023년에는 1,684억 5,000만 호주 달러로 증가하며, 2004년 이후 호주 식품 소매업의 매출액은 전년 대비 꾸준히 증가하고 있습니다.

국제통화기금(IMF)에 따르면 2021년에는 고용자 수가 279만 명에서 297만 명에 달할 것으로 예상됩니다. 뉴질랜드의 식료품 부문은 Foodstuffs New Zealand, Progressive Enterprises(Countdown으로 운영) 및 Warehouse Group의 세 가지 주요 기업이 지배하고 있습니다. 이 세 회사는 국내 식료품 소매업의 90%라는 엄청난 점유율을 차지하고 있습니다. 주목할 만한 점은 독립, 식료품점, 소규모 편의점이 섞여 있다는 점입니다.

미국 농무부에 따르면 물가 상승률이 7%로 치솟으면서 뉴질랜드 소비자들은 식비 지출의 상당 부분을 재량품에서 필수품으로 전환하고 있다고 합니다. 이러한 조정으로 인해 고급 제품에 대한 안목이 높아지고 있습니다. 소비자들은 독특한 판매 포인트를 제공하는 제품이나 실제 영양 상태나 인지된 건강 상태와 같은 주목할 만한 건강상의 이점을 자랑하는 제품에 끌리게 되었습니다. 뉴질랜드의 소매 시장은 계속해서 호황을 누리고 있습니다. 현재 뉴질랜드의 인플레이션 환경으로 인해 슈퍼마켓과 식료품 판매는 빠르게 성장하고 있으며, 시장 성장을 주도하고 있습니다.

호주 및 뉴질랜드 파우치 포장 시장

호주와 뉴질랜드 파우치 포장 시장은 단편화 되고 있으며, Amcor PLC, Mondi PLC, Sonoco Products Company, Transcontinental Packaging New Zealand, Filton Packaging 등 많은 국내 대기업이 존재합니다. 이 지역에서 사업을 운영하는 기업은 기술 혁신, 제휴, 인수, 합병 등을 통해 사업 확장에 주력하고 있습니다.

2023년 9월, 호주에 본사를 둔 연포장 회사 필튼 포장은 호주에서 윤곽 슬리브 및 가방 솔루션을 제공하는 호주 윤곽 포장(ACP)을 인수했습니다. 이번 인수를 통해 Filton Packaging은 가방, 윤곽 슬리브 및 인쇄 제조 능력을 강화할 것으로 예상되며 ACP는 Filton의 광범위한 제품 및 서비스를 활용하여 고객의 요구 사항을 충족시킬 것으로 예상됩니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 상정과 시장 정의

조사 범위

제2장 조사 방법

제3장 개요

제4장 시장 인사이트

시장 개요

업계의 매력 - Porter's Five Forces 분석

공급 기업의 교섭력

바이어의 교섭력

신규 진출업체의 위협

대체품의 위협

경쟁 기업 간 경쟁 관계

산업 밸류체인 분석

제5장 시장 역학

시장 성장 촉진요인

E-Commerce와 편리한 패키지 제품에 의한 수요 증가

시장 성장 억제요인

포장재료에 대한 역동적이고 엄격한 규제

제6장 업계 규제와 정책, 규격

제7장 시장 세분화

소재 유형별

플라스틱

종이

알루미늄박

수지 유형별 - 플라스틱

폴리에틸렌

폴리프로필렌

PET

PVC

EVOH

기타 수지

유형별

스탠다드

무균

레토르트

핫필

제품별

플랫(필로우 & 사이드 실)

스탠드 업

최종사용자 산업별

식품

제과

냉동식품

신선식품

유제품

건물

육류, 가금육, 어개류

애완동물 사료

기타 식품(시즈닝, 스파이스, 스프레드류, 소스, 조미료 등)

의료·의약품

퍼스널케어와 가정용품

기타 최종사용자 산업(자동차, 화학, 농업)

국가별

호주

뉴질랜드

제8장 경쟁 구도

기업 개요

Amcor PLC

Sonoco Products Company

Favourite Packaging

ePac Holdings LLC

Mondi Plc

Caspack New Zealand

Transcontinental Packaging New Zealand

TotalPak Ltd

Filton Packaging

Allflex Packaging

제9장 재활용과 지속가능성 전망

제10장 향후 전망

KSA

영문 목차

영문목차

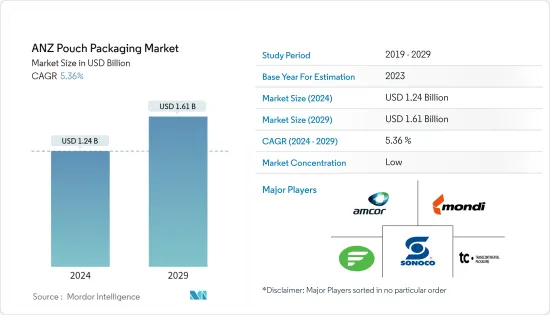

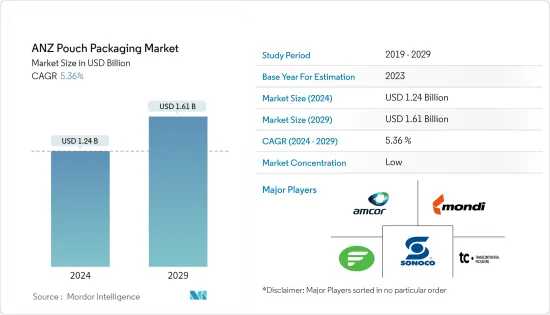

The ANZ Pouch Packaging Market size is estimated at USD 1.24 billion in 2024, and is expected to reach USD 1.61 billion by 2029, growing at a CAGR of 5.36% during the forecast period (2024-2029). In terms of shipment volume, the market is expected to grow from 11.89 billion units in 2024 to 15.77 billion units by 2029, at a CAGR of 5.81% during the forecast period (2024-2029).

The pouch packaging market in Australia and New Zealand is witnessing significant growth, driven by increasing demand from the food industry. The cost efficiency of pouch packaging compared to traditional packaging is driving the market growth.

Key Highlights

Pouch packaging maintains product freshness by regulating temperature, eliminating oxygen, and absorbing moisture during transit or storage. Commonly used materials like polyethylene and polypropylene ensure the packaging breaks down quickly. Its versatility makes flexible packaging accessible across various industries, including food, beverage, personal care, pharmaceutical, and others.

Over the last decade, Australia's population surged, leading to increased demand for consumables, particularly favoring plastic packaging. This preference is primarily attributed to the lightweight nature of plastic, which bolsters their portability. The consumables include beverages, packaged meals, and convenience packages, including microwave and oven-safe options. Such consumer preferences in the country might push the need for pouch packaging.

Australia unveiled its ambitious 2025 National Packaging Targets in response to these trends. These targets represent a significant stride toward a more sustainable packaging approach, requiring widespread backing from market players and the government. The 2025 Targets are comprehensive, covering all packaging activities in the nation, with the Australian Packaging Covenant Organisation (APCO) leading the charge in their execution.

The grocery and food retail sector continues to expand in New Zealand. Imports from the United States include packaged food, pet food, and meat, among others. This would leverage the need for the pouch packaging market in the region.

Additionally, the retail market in New Zealand sustained robust sales, with supermarkets and grocery segments leading the charge, buoyed by the nation's prevailing inflation. The region also witnessed challenges in the packaging market. New Zealand grappled with persistent logistical hurdles, elevated interest rates, and increased household expenses in 2023, and consumer spending showed signs of moderation. The grocery sector's revenue declined in 2023.

ANZ Pouch Packaging Market Trends

Rising Demand From E-commerce for Convenient Packaging Products

Lifestyle changes are propelling the pouch packaging market in the region. The market witnessed an increase in demand for single-serve and convenient portable packs. Australia's rising prominence in food exports can be attributed to the surge in e-commerce and enhanced logistics. Brands in the packaging market are pivoting toward enhancing brand experiences, with a notable emphasis on convenience.

According to a survey by Australia Post, the e-commerce sector witnessed rapid growth, including food and liquor, which accounted for a 20.6% share of online purchases and an 11.4% Y-o-Y increase. Additionally, stores encompassing large retailers and online marketplaces accounted for an 18.1% share of online purchases, marking an 8.6% Y-o-Y increase.

Manufacturers in Australia are increasingly adopting convenient and flexible packaging solutions. The surge in e-commerce has been a game-changer, reshaping the packaging market. Manufacturers are gravitating toward flexible packaging primarily for its promise of swifter and more secure product deliveries.

According to Retail NZ, by 2030, online purchases are projected to account for 20% of all retail sales in New Zealand. Consumers increasingly demand omnichannel retailing, expecting a seamless shopping journey. Traditional retailers must pivot, prioritizing and marketing their online platforms to stay competitive. Embracing diverse communication channels for customer engagement is set to become standard practice.

According to the National Australia Bank, in the annual growth in online retail spending by domestic merchants as of April 2024, the departmental stores took the top position with 38.7%, followed by the personal and recreational industry with 12.6% and grocery and liquor with 10.7%. Households prefer more flexible packaging over rigid options to align with their evolving lifestyles. With the rise of smaller households, the demand for single-serve packaging is increasing.

Ready-to-eat Meals and the Food Industry are Expected to Witness Significant Growth

Ready-to-eat packaged meals are popular in Australia, driven by the growing working population and evolving work-life dynamics. As per a CSIRO report, the domestic consumption of prepared and frozen packaged meals is projected to be valued at USD 3.7 billion by 2030, reflecting spending patterns and demographic shifts.

As Australia ramps up its production of convenient meals, the demand for flexible packaging is set to soar, fueling market growth. Flexible packaging pouches equipped with spouts and closures preserve freshness and flavor and accommodate a wide array of solid and liquid food products.

Australia's packaging market is primarily propelled by shifting lifestyles, with a notable surge in demand for portable food packs. Additionally, bolstered by a rise in e-commerce, Australia is solidifying its position as a critical player in the food trade. According to the Australian Bureau of Statistics, the annual revenue of the food retail industry in 2020 was AUD 151.55 billion, which increased to AUD 168.45 billion in 2023. Since 2004, Australia's food retail revenue has witnessed steady year-on-year growth.

According to the International Monetary Fund (IMF), the country's employment is expected to reach 2.97 million from 2.79 million in 2021. New Zealand's grocery sector is dominated by three key players: Foodstuffs New Zealand, Progressive Enterprises (operating as Countdown), and the Warehouse Group, the latter resembling a Walmart, with a significant focus on groceries. These three entities command a staggering 90% share of the nation's grocery retail landscape. Notably, the sector is further diversified by a mix of independents, greengrocers, and small convenience stores.

According to the US Department of Agriculture, with price inflation soaring 7%, consumers in New Zealand are shifting a significant portion of their food spending from discretionary items to staples. This adjustment has led to a more discerning approach to luxury goods. Consumers are gravitating toward products that offer a unique selling point or boast notable health benefits, whether in actual nutrition or perceived well-being. The retail market in New Zealand has continued to show strong sales. Due to New Zealand's current inflationary environment, supermarkets and grocery sales are witnessing rapid growth, driving the market growth as well.

ANZ Pouch Packaging Industry Overview

The pouch packaging market in Australia and New Zealand is fragmented, with the presence of many domestic and major players, such as Amcor PLC, Mondi PLC, Sonoco Products Company, Transcontinental Packaging New Zealand, and Filton Packaging. Companies operating in the region are focused on expanding their business through innovations, collaborations, acquisitions, mergers, etc.

September 2023: Australia-based flexible packaging company Filton Packaging acquired Australian Contour Packaging (ACP), a domestic provider of contoured sleeves and bag solutions. The deal was expected to help Filton Packaging bolster its manufacturing capacity to produce bags, contour sleeves, and printing work. ACP was expected to leverage Filton's extensive range of products and services to fulfill its customers' requirements.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumption and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Rising Demand from E-commerce and Convenient Packaging Products

5.2 Market Restraints

5.2.1 Dynamic and Stringent Regulations Against Packaging Materials