북미의 스탠드업 파우치 포장 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

North America Stand-Up Pouch Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693971

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

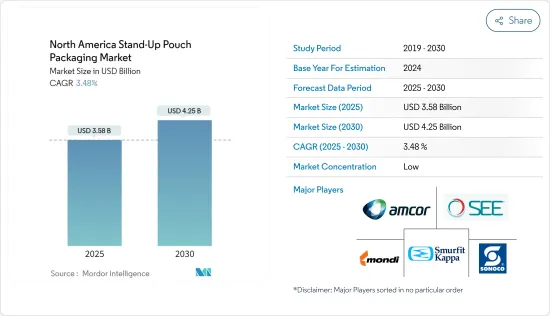

북미 스탠드업 파우치 포장 시장 규모는 2025년 35억 8,000만 달러, 2030년에는 42억 5,000만 달러에 이를 것으로 예측됩니다. 예측 기간(2025-2030년)의 CAGR은 3.48%를 나타낼 전망입니다.

시장 규모에서는 2025년 269억 9,000만개에서 2030년에는 314억 9,000만개가 될 것으로 예측되며, 예측기간(2025-2030년)의 CAGR은 3.13%를 나타낼 전망입니다.

표준, 무균, 레토르트 등의 스탠드 업 파우치 포장 제품은 시장 조사 대상입니다.

주요 하이라이트

지역 전체의 냉동 포장 산업의 성장은 시장에 플러스의 영향을 미칠 것으로 예측됩니다.

게다가, 외출처에서 스낵에 대한 요구 고조가, 고객에게 편리성을 제공하는 재폐쇄 가능한 스탠드업 파우치 수요로 이어지고 있습니다. 또한, 소비자의 라이프 스타일이나 음식의 기호의 변화, 식품 기술의 변화가 시장 수요를 한층 더 끌어 올리고 있습니다.

환경 문제에 대한 소비자의 관심이 높아지고, 역동적인 규제 기준, 플라스틱 기반의 포장 제품을 생분해성 재료로 대체하는 것으로 이루어지는 지속가능성에의 지속적인 추진, 최첨단의 재활용 시설의 부족에 의한 불충분한 재활용률이, 시장의 성장에 과제를 주고 있습니다.

급속히 변화하는 시장 요건에 대응하기 위해 포장기계의 혁신이 진행되고 있지만, 기존의 기계를 사용하고 있는 포장제조업체는 현재 시장요구사항이 증가하는 작업부하에 대응하기 위한 충분한 설비가 갖추어져 있지 않기 때문에 이것이 과제가 됩니다.

COVID-19 후의 유행은 식품 및 제약 산업에서의 수요 증가에 도움이 되어 포장 수요의 급증을 가져왔습니다.

북미 스탠드업 파우치 포장 시장 동향

스탠다드 파우치 유형 부문이 큰 시장 점유율을 차지할 전망

베이비 푸드나 액체 포장(차, 커피, 주스)을 포함한 스탠다드 파우치는 음식 식품 산업에서 널리 사용되고 있습니다.

스탠다드 스탠드업 파우치는 최종 사용자 산업 수요가 급증하고 있어, 제조업체에 혁신적인 솔루션에 대한 노력을 촉구하고 있습니다.

미국 농무부 해외농업국에 따르면 미국의 2022/2023 회계연도 커피 소비량은 60킬로그램 포대 2,630만 개를 넘었습니다.

커피 소비량이 증가함에 따라 커피를 보관하고 유통시키기 위한 포장 솔루션에 대한 수요도 높아진다고 생각됩니다.

커피 시장은 경쟁이 치열하고 각 브랜드는 차별화를 도모하기 위해 포장을 이용하는 경우가 많습니다.

큰 성장이 기대되는 캐나다.

캐나다의 스탠드업 파우치 수요 증가의 주요 원동력은 포장식품과 가공식품에 대한 의존도가 높다는 점입니다.

식품산업은 급속히 확대 및 변화하고 있어 포장의 선택사항을 넓혀 더욱 생산성이 높은 방법을 모색하고 있습니다.

캐나다 반려동물 먹이 산업은 호황을 누리고 있으며 캐나다 농업 및 농업 식품부(AAFC)의 데이터에 따르면 캐나다의 반려동물 먹이 소매 매출은 연평균 4.9% 증가하고 2025년까지 53억 캐나다 달러(22억 2000만 달러) 도달할 것으로 예측됩니다. 반려동물 식품 산업에서는 건식 식품 및 습식 식품 포장에 스탠드 업 파우치가 자주 사용됩니다.

이 지역에서는 포장 옵션에 대한 소비자 수요가 높아져 식품, 식품 및 제약 산업에서의 채택이 증가하고 있습니다.

확대하는 외국인 거주 인구와 새로운 신제품을 시험하고 싶다는 충동도 즉석식품 수요를 뒷받침하고 있습니다. 건강 문제가 증가함에 따라 소비자는 식물성 반찬에도 주목하고 있습니다.

또한 캐나다 국내의 다양한 최종 사용자에 있어서 수요 증가에 의해 캐나다 시장에 있어서의 기업 프레즌스 확대를 위한 기업 확대, 합병, 인수도 이루어졌습니다.

북미 스탠드업 파우치 포장 산업 개요

북미 스탠드업 파우치 포장 시장은 세분화되어 있으며, Amcor PLC, Mondi Group, Sealed Air Corporation, Sonoco Products Company, Smurfit Kappa Group 등의 대기업이 존재합니다.

2023년 7월 - Full Tamaki OYJ는 미국 텍사스 주 파리의 시설에 많은 투자를할 것이라고 발표했습니다. 3,000만 달러로 창고와 제조시설은 리스가 됩니다.

2023년 1월 - 글렌로이사는 2년간의 개발 프로세스를 거쳐 재활용 가능한 STANDCAP이 플라스틱 재활용 협회(APR)로부터 크리티컬 가이던스 인정을 받았다고 발표했습니다. 100% 폴리에틸렌 재활용 스탠드캡은 환경, 소비자, 브랜드, 소매업체, 식품 안전에 큰 도움이 됩니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

구매자, 소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

산업 생태계 분석

산업표준과 규제

스탠드 업 파우치 시장의 최근 혁신

비교 분석 : 플랫 파우치 포장과 스탠드업 파우치 포장의 비교

제5장 시장 역학

시장 성장 촉진요인

북미에서의 식음료 수요 증가가 예상되어 시장 성장에 공헌

표준 파우치는 편리성이 높고(지퍼, 슬라이더, 스파우트 팩 등이 있음) 대체품에 비해 재료량이 적어

시장의 과제

스탠드업 파우치를 제조하기 위한 충전기 변경으로 전환 구현이 어려워짐

제6장 시장 세분화

팩 유형별

스탠다드

아셉틱

레토르트

기타 팩 유형

재료 유형별

플라스틱(PE, PP, PVC, EVOH, 바이오플라스틱)

금속, 박

종이

최종 사용자별

식품

음료

의료 의약품

반려동물 식품

홈&퍼스널케어

기타

국가별

미국

캐나다

제7장 경쟁 구도

기업 프로파일

Amcor PLC

Mondi Group

Sealed Air Corporation

Sonoco Products Company

Smurfit Kappa Group

ProAmpac LLC

Clondalkin Group

Huhtamaki Oyj

Dazpak Flexible Packaging

Glenroy Inc.

PPC Flexible Packaging LLC

제8장 시장의 미래

SHW

영문 목차

영문목차

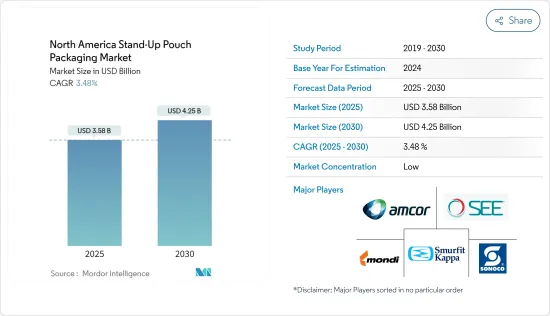

The North America Stand-Up Pouch Packaging Market size is estimated at USD 3.58 billion in 2025, and is expected to reach USD 4.25 billion by 2030, at a CAGR of 3.48% during the forecast period (2025-2030). In terms of market size, the market is expected to grow from 26.99 billion units in 2025 to 31.49 billion units by 2030, at a CAGR of 3.13% during the forecast period (2025-2030).

Stand-up pouch packaging products such as Standard, Aseptic, and Retort are considered under the scope of the market study. Stand-up pouch packaging offers an ideal protective barrier during shipment and transit and prevents any external element, such as moisture and dirt, from coming into contact with the item.

Key Highlights

The growth of the frozen packaged industry across the region is expected to impact the market positively. Rising demand for packaged food and beverages, increasing demand for Ready-to-Eat (RTE) food, convenience of use, and cost-effectiveness of pouches are primary factors supporting the market growth.

In addition, the rise in the need for on-the-go snacks has led to the demand for re-closable stand-up pouches as they offer convenience to customers. In addition, the changing lifestyle and food preferences among consumers and changing food technology further boost the market's demand.

The growing consumer attention to environmental concerns, dynamic regulatory standards, the ongoing drive for sustainability, which comprises replacing plastic-based packaging products with biodegradable materials, and inadequate recycling rates due to the lack of cutting-edge recycling facilities are challenging the market's growth.

The ongoing technological changes in packaging machinery to cope with the rapidly changing market requirements will pose a challenge as packaging manufacturers using traditional machinery are not well equipped to take the increasing workload of current market requirements. Players must either invest in new tools, spare parts, and software to meet the changing market needs or switch to new machinery.

The post-COVID-19 pandemic resulted in a surge in demand for packaging aided by the growing demand from the food and beverage and pharmaceutical industries, which will likely continue for the next few years.

North America Stand-Up Pouch Packaging Market Trends

Standard Pack Type Segment is Expected to Hold Significant Market Share

Standard pouches, including baby food and liquid packaging (tea, coffee, and juices), are widely used in the food and beverage industry. Consumers' expectations for packaged fresh food to store all the natural properties and aromas drive the usage of standard pouches.

The Standard Stand-up pouches are experiencing a surge in end-user industry demand, prompting manufacturers to strive for innovative solutions. The landscape is characterized by dynamic strategies, with companies adopting approaches such as collaboration, expansion, acquisition, and product launches to stay competitive.

According to the USDA Foreign Agricultural Service, Coffee consumption in the United States amounted to over 26.3 million 60-kilogram bags in the 2022/2023 fiscal year. This is a slight increase from the total United States coffee consumption in the 2020/2021 fiscal year, which amounted to 25.94 million 60-kilogram bags.

With increased coffee consumption, there is likely to be a higher demand for packaging solutions to contain and distribute the coffee. Standard Stand-up Pouches are a popular, versatile packaging option offering convenience, protection, and visibility. As coffee consumption rises, the demand for these pouches may also increase.

The coffee market is highly competitive; brands often use packaging to differentiate themselves. Stand-up pouches provide ample space for branding, labeling, and marketing messages. As coffee consumption increases, companies will invest more in packaging that helps their products stand out on the shelves, which could boost the demand for stand-up pouches.

Canada Expected to Witness Significant Growth

A key driving factor for the increased demand for stand-up pouches in Canada is the prevalent reliance on packaged and processed foods. University of Toronto's report indicated that approximately 75% of the nation's food supply comes from processed foods. The shift in consumption patterns underscores the need for convenient and sustainable packaging solutions, making stand-up pouches a preferred choice in the Canadian market.

The food industry is expanding and changing swiftly, extending its packaging alternatives and looking for methods to be more productive. Additionally, more businesses, such as Logos Pack, Omniplast, Canada Brown, Rootree, and Grauman Packaging, are reconsidering their packaging decisions as more eco-friendly and sustainable packaging solutions become available.

The pet food industry in Canada is booming, and as per Agriculture and Agri-Food Canada (AAFC) data, retail sales of pet food in Canada are expected to increase in CAGR by a further 4.9%, attaining CAD 5.3 billion (USD 0.22 billion) by 2025. In the pet food industry, stand-up pouches are a popular choice for packaging dry and wet pet food. Pouches with tear notches and easy-open features cater to the convenience of pet owners when serving their pets meals.

The region is witnessing increased consumer demand for packaging options and rising adoption in the food, beverage, and pharmaceutical industries. Also, growing healthcare concerns and environmental regulations have increased the use of lightweight, high-barrier packaging products. The resealable benefit bolsters the growth of personal care and cosmetic applications.

The existence of an expanding ex-pat population and the urge to try new products also drive the demand for ready meals. The region's need for quick and easy food, including prepared meals, is increasing due to shifting social and economic patterns. With rising health concerns, consumers are also focused on plant-based ready meals. According to Agriculture and Agri-Food Canada, the retail sales of plant-based ready meals (free from meat) in Canada were 19.1 million USD in 2021, reaching 22.1 million USD in 2022.

The market also witnessed corporate expansions, mergers, and acquisitions to expand corporate presence in the Canadian market due to increased demand across various end-users in the country.

North America Stand-Up Pouch Packaging Industry Overview

The North America stand-up pouch packaging market is fragmented, with the precence of major players like Amcor PLC, Mondi Group, Sealed Air Corporation, Sonoco Products Company, and Smurfit Kappa Group. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

July 2023 - Huhtamaki OYJ announced a significant investment in its Paris, Texas, facility in the United States. The investment consists of an expansion of its manufacturing capacity as well as a consolidation of an external warehouse. The investment into production assets is approximately USD 30 million, and the warehouse and manufacturing facility will be leased. This brings significant opportunities to increase the North America business segment's capacity to support the growth of the food service business.

January 2023- Glenroy Inc. announced that after a two-year development process, they received Critical Guidance Recognition from the Association of Plastic Recyclers (APR) for the recyclable STANDCAP. As a complete eco-friendly alternative to rigid plastic and glass bottles, the 100% Polyethylene recyclable STANDCAP is a major win for the environment, consumers, brands, retailers, and food safety. By emphasizing the company's sustainable, flexible packaging options, Glenroy contributes to ecological goals while also capitalizing on the growing market preference for sustainable solutions, driving business growth in the long term.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers/Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Ecosystem Analysis

4.4 Industry Standards and Regulations

4.5 Recent Innovations in the Stand-Up Pouch Market

4.6 Comparative Analysis: Flat Packaging vs Stand-Up Pouch Packaging

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Demand for Food and Beverage Expected to Grow in North America, thereby Contributing to the Market Growth

5.1.2 Standard Pouches Offer a High Level of Convenience (Available in Zipper, Slider, Spout Packs, Etc.) and Require Less Material Volumes as Compared to Alternative

5.2 Market Challenges

5.2.1 Filling Machinery Changes for Producing Stand-Up Pouches Make Transitions Difficult to Implement