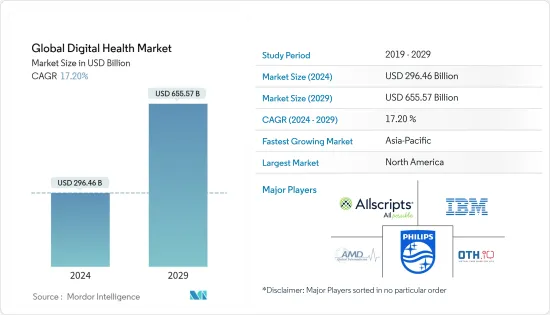

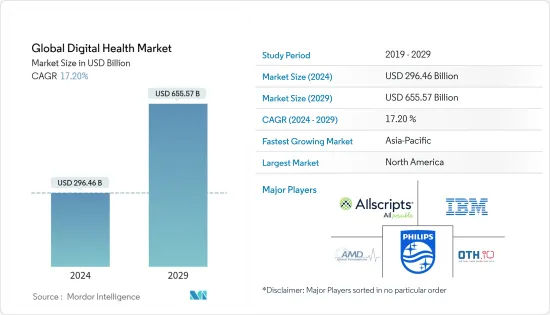

세계의 디지털 헬스 시장 규모는 2024년에 2,964억 6,000만 달러로 추정되고, 2029년까지 6,555억 7,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간(2024-2029년) 동안 17.20%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

신형 코로나바이러스 감염(COVID-19)의 감염 확대와 세계 봉쇄는 헬스케어의 디지털 제공이 그 어느 때보다 중요해졌습니다. 예를 들어, 2021년 4월에 공개된 기사 'COVID-19를 계기로 한 유럽 디지털 헬스 혁명'에 따르면, 유럽 위원회는 COVID-19 회복 대응 프로그램의 일환으로 EU4 헬스 프로그램을 제안했습니다. 이 이니셔티브는 유럽 의료 분야의 디지털 변혁을 위해 51억 유로를 조달하고 미래의 국경을 넘어 건강 위협에 대비할 수 있도록 보장하기 위한 것이었습니다. 따라서 신형 코로나바이러스 감염(COVID-19)으로 인해 헬스케어의 디지털 변혁을 향한 유럽 정부의 투자 증가는 조사 대상 시장 성장에 중요한 역할을 했습니다. 이처럼 신형 코로나바이러스 COVID-19는 팬데믹 단계에서 시장의 성장에 심각한 영향을 미쳤습니다.

디지털 헬스케어 채용 증가, 인공지능, IoT, 빅데이터 상승, 모바일 헬스 애플리케이션 채용 증가, 정부 활동 등도 시장 성장을 가속하고 있습니다.

디지털 플랫폼과 시스템 개발을 위해 정부가 제공하는 보조금도 시장 성장을 가속하고 있습니다. 예를 들어, 2021년 5월 영국의 헬스텍 기업인 my m 헬스와 그 협력자는 CUOREMA라는 프로젝트의 개발에 대해 유로스타즈 보조금으로 250만 유로를 획득했습니다. CUOREMA 프로젝트는 환자 중심의 새로운 심장 재활 지원 시스템의 개발에 중점을 둡니다.

마찬가지로 기술 도입 및 제품 출시 증가도 시장 성장의 핵심 요소입니다. 예를 들어, 2021년 6월에 MicroPort CRM은 AlizeaTM 및 BoreaTM 심박 조율기를 출시했습니다. 이 맥박 조정기에는 블루투스 기술이 탑재되어 있으며 유럽의 SmartView Connect 홈 모니터와 함께 원격 모니터링을 간소화할 수 있습니다. 이 심박 조율기는 심장 전문가가 장치를 원격으로 모니터링하는 데 도움이 되며, 간단한 정기 검사를 위해 환자가 병원에 갈 필요가 줄어들고 의료 시스템의 부담이 줄어듭니다.

또한, 2020년 12월, Entremo는 헝가리 병원과 간호 시설에서 환자의 생명 징후를 원격으로 모니터링하기 위해 자사 제품의 손목 밴드를 도입했습니다. 게다가 2021년 3월에는 스페인의 모바일 네트워크 Yoigo가 'Doctor Go'라는 원격 의료 서비스를 시작했습니다. Doctor Go Remote Medical Services는 의사 및 전문가와의 비디오 상담 외에도 전자 처방전 및 약물 전달을 위한 원격 약국 서비스를 제공합니다.

따라서 위의 요인으로 인해 조사 대상 시장은 예측 기간 동안 크게 성장할 것으로 예상됩니다. 그러나 환자 데이터에 대한 보안 우려는 미래 시장의 성장을 방해할 수 있습니다.

m 헬스(모바일 헬스)는 모바일 및 무선 기술을 사용하여 건강 목표 달성을 지원하는 것입니다. m 헬스의 가장 일반적인 용도는 소비자에게 예방 건강 관리 서비스에 대해 교육하기 위해 모바일 장치를 사용하는 것입니다. 또한 m 헬스은 질병 모니터링, 치료 지원, 유행 발생 추적, 만성 질환 관리에도 사용됩니다. 만성 질환 부담 증가, 기술 진보, 국민 건강에 대한 의식 증가, 정부 이니셔티브 등의 요인이 예측 기간 동안 시장 부문의 성장을 추진하고 있습니다.

시장 성장을 가속하는 또 다른 요인은 조사 연구의 수가 증가하는 것입니다. 예를 들어, 2020년 10월, “ m 헬스와 eHealth는 접근하기 어려운 사람들의 당뇨병과 고혈압 관리를 개선할 수 있는가? 캄보디아의 피어 에듀케이터 모델을 지원하기 위한 디지털 헬스 프로세스 평가에서 배운 교훈'이라는 제목의 연구 결과가 발표되었습니다. “RE-AIM 프레임워크 사용”은 비감염성 질환(NCD) 부담이 중저소득국(LMIC)에서 증가하고 있다고 말합니다. LMIC에서 NCD에 의한 사망률은 4:5이며, 더 가난한 사람들에게 불균형한 영향을 미치고 경제적 부담 및 엄청난 피해를 초래합니다. 디지털 개입은 의료 시스템이 불충분하고 휴대전화의 보급률이 높은 등 접근하기 어려운 사람들의 NCD 관리를 개선할 수 있습니다. 이러한 연구는 건강 관리 시스템의 부담을 줄이는데 모바일 건강이 유용하다는 것을 입증합니다.

제품 출시도 시장 부문의 성장을 가속할 수 있습니다. 예를 들어, 의료 실험실에서 샘플의 빠르고 정확한 처리를 지원하는 혁신적인 클라우드 소프트웨어 회사인 GoMeyra는 2021년 5월 GoMeyra pass라고 불리는 COVID-19 감염 백신 접종의 검증 또는 PCR 및 빠른 항원 검사 결과를 공유하는 무료 모바일 앱을 출시했습니다. GoMeyra Pass는 시장에서 가장 빠른 LIMS 중 하나인 GoMeyra 검사 정보 관리 시스템(LIMS)과 통합되어 인증 기관의 전국 네트워크가 24시간 이내에 COVID-19 검사 결과를 제공할 수 있습니다. 게다가 유럽연합은 시민의 힘과 퍼스센터드 케어를 위한 디지털 툴을 우선하기 위해 “유럽에서 신뢰할 수 있는 m 헬스 라벨의 추진 : 헬스 및 웰니스 앱의 품질과 신뢰성에 관한 기술 사양 도입” 라는 제목의 프로그램을 추진하고 있으며, 그 제출일이 2021년 9월이었던 사람 중심의 치료를 위해 디지털 도구를 우선시하고 있으며, 이러한 이니셔티브는 향후 m 헬스의 인지도와 접근성도 향상시켜 부문의 성장을 가속합니다.

따라서 위의 요인으로 인해 시장 부문은 예측 기간 동안 성장이 예측될 것으로 예상됩니다.

디지털 헬스는 만성 질환 부담 증가, 첨단 의료 기술의 선진 도입, 정부 및 공공 기관의 지원, 제품 및 서비스 출시 등의 요인으로 인해 북미의 헬스케어 구성 요소로 빠르게 성장하고 있습니다.

모바일 테크놀로지에 대한 수요가 높아지고, 환자에 의한 재택 케어의 채용 증가, 통원의 감소에 의해 예측 기간 중에 시장의 성장이 촉진될 것으로 예상됩니다. 북미의 헬스케어에서는 특히 COVID-19 감염증 팬데믹 중에 사람들이 개인의 헬스케어에 적극적으로 참여할 수 있도록 지원하는 원격 의료 애플리케이션의 출현으로 긍정적인 동향을 볼 수 있습니다. 스마트폰과 모바일 기술의 존재로 임상 및 라이프스타일 애플리케이션을 모두 사용하여 건강한 행동을 교육하고 통합할 수 있습니다.

또한 정부 및 공공기관의 노력도 시장을 견인할 것으로 예상됩니다. 예를 들어, 2020년 3월 메디케어 및 메디케이드 서비스 센터(CMS)는 메디케어 원격 의료 서비스에 대한 액세스를 확대하고 수혜자가 의료 현장으로 향하지 않고도 의료 전문가로부터 광범위한 서비스를 받을 수 있게 했습니다. 또한, 2020년 3월 6일부터는 전국에서 원격 의료를 통해 제공되는 병원, 클리닉 및 기타 방문비가 메디케어에 의해 지급됩니다. 이는 조사 대상 시장에 긍정적인 영향을 미칠 수 있습니다.

또한, 공급업체는 시장에서 살아남기 위해 파트너십, 협업, 인수, 합병 및 제품 출시를 추진하고 있습니다. 예를 들어, 2020년 11월에 Morneau Shepell은 미국 최초의 통합 원격 의료 솔루션을 도입했습니다. 이 서비스 하에서 지역 직원과 그 가족은 모든 중요하고 당분간의 건강 요구를 충족시키는 디지털 헬스 지원에 액세스할 수 있습니다. 또한, 2020년 8월, AMD Global Telemedicine Inc.는 온타리오에 본사를 둔 기업 iTelemed와 협력하여 COVID-19 감염의 팬데믹에 따라 캐나다 내에서 소외된 사람들의 충족되지 않은 헬스케어 요구에 대응하는 가상 헬스케어 솔루션을 제공했습니다.

따라서 앞서 언급한 요인을 고려하면 조사 대상 시장은 예측기간 동안 북미에서 크게 성장할 것으로 예상됩니다.

디지털 헬스 시장의 경쟁은 중간 정도입니다. 시장 점유율 면에서 현재, 몇몇 대기업은 시장을 독점하고 있습니다. 현재 시장을 독점하고 있는 기업으로는 Allscripts Healthcare Solutions Inc., Koninklijke Philips NV, OTH.IO, International Business Machinery Corporation(IBM), AMD Global Telemedicine Inc. 등이 있습니다.

The Global Digital Health Market size is estimated at USD 296.46 billion in 2024, and is expected to reach USD 655.57 billion by 2029, growing at a CAGR of 17.20% during the forecast period (2024-2029).

With the strike of COVID-19 and lockdowns all over the globe, the digital delivery of healthcare became more important than ever. For instance, according to the article "The European digital health revolution in the wake of COVID-19," published in April 2021, the European Commission proposed the EU4Health program as part of a COVID-19 recovery response program. The initiative aimed to raise EUR 5.1 billion for the digital transformation of the European health sector and ensure preparedness for future cross-border health threats. Thus, the increased investments by European governments toward the digital transformation of healthcare amid COVID-19 played a significant role in the growth of the studied market. Thus, COVID-19 had a profound impact on the growth of the market amid the pandemic phase.

The factors such as increasing adoption of digital healthcare, the rise in artificial intelligence, IoT, and big data, growing adoption of mobile health applications coupled with initiatives taken by the government are also propelling the growth of the market.

The grants provided by the government for the development of digital platforms and systems are also driving the growth of the market. For instance, in May 2021, the United Kingdom health tech company, my mhealth, and collaborators were awarded EUR 2.5 million in Eurostars Grants for the development of their project, named CUOREMA. The CUOREMA project will focus on developing a new, patient-centered cardiac rehabilitation support system.

Similarly, increasing adoption of technology and product launches are key factors for the growth of the market. For instance, in June 2021, MicroPort CRM launched AlizeaTM and BoreaTM pacemakers, which are equipped with Bluetooth technology for streamlined remote monitoring when paired with the SmartView Connect home monitor in Europe. These pacemakers help the cardiologists monitor the devices remotely and decrease the patient's need to travel to the hospital for a simple routine examination, thus reducing the burden on the healthcare system.

Moreover, in December 2020, Entremo deployed its product, a wristband, to remotely monitor the vital signs of patients in hospitals and nursing homes in Hungary. Additionally, in March 2021, the Spanish mobile network Yoigo launched a telemedicine service named "Doctor Go". The Doctor Go telemedicine service offers video consultations with family doctors and specialists, as well as telepharmacy services for electronic prescriptions and the delivery of medicines.

Hence, due to the abovementioned factors, the studied market is expected to grow significantly during the forecast period. However, security concerns regarding patient data may hinder market growth in the future.

mHealth, or Mobile Health, is the use of mobile and wireless technologies to support the achievement of health objectives. The most common application of mHealth is the use of mobile devices to educate consumers about preventive healthcare services. Moreover, mHealth is also used for disease surveillance, treatment support, epidemic outbreak tracking, and chronic disease management. Factors such as the growing burden of chronic diseases, advancements in technology, rising awareness about health among the population, and initiatives taken by the government are driving the growth of the market segment over the forecast period.

Another factor driving the growth of the market is the increasing number of research studies. For instance, in October 2020, a research study was published titled "Can mHealth and eHealth improve management of diabetes and hypertension in a hard-to-reach population? lessons learned from a process evaluation of digital health to support a peer educator model in Cambodia using the RE-AIM framework" stated that the burden of non-communicable diseases (NCDs) is increasing in low- and middle-income countries (LMICs), where NCDs cause 4:5 deaths, disproportionately affect poorer populations, and carry a large economic burden. Digital interventions can improve NCD management for these hard-to-reach populations with inadequate health systems and high cell phone coverage. Such studies demonstrate the usefulness of mobile health in reducing the burden on the healthcare system.

Product launches are also likely to favor the growth of the market segment. For instance, in May 2021, GoMeyra, an innovative cloud software company that helps medical laboratories process samples faster and more accurately, launched a free mobile app for sharing COVID-19 vaccination verification or PCR and rapid antigen test results called GoMeyra pass. GoMeyra Pass integrates with the GoMeyra lab information management system (LIMS), one of the fastest LIMS on the market that allows its nationwide network of accredited laboratories to provide COVID-19 test results within 24 hours. Additionally, the European Union is promoting a program titled "Promoting a trusted mHealth label in Europe: uptake of technical specifications for Quality and Reliability of Health and Wellness Apps" to prioritize digital tools for citizen empowerment and for person-centered care, whose submission date was in September 2021. Such initiatives also increase the awareness and accessibility of mHealth in the upcoming future and thus promote segment growth.

Thus, owing to the abovementioned factors, the market segment is expected to project growth over the forecast period.

Digital health is a rapidly growing component of healthcare in North America owing to factors such as the growing burden of chronic diseases, the high adoption of advanced healthcare technologies, support from the government and public authorities, and the launch of products and services.

The rising demand for mobile technologies, rising adoption of home care by patients, and reduction in hospital visits are expected to propel the market's growth over the forecast period. Healthcare in North America is experiencing positive trends with the emergence of telemedicine applications that help the population to be active in personal health management, especially during the COVID-19 pandemic. Smartphones and the presence of mobile technology make it possible to use both clinical and lifestyle applications to help educate and adopt healthy behaviors.

Also, the initiatives by the government and public organizations are expected to drive the market. For instance, in March 2020, the Centers for Medicare and Medicaid Services (CMS) widened access to Medicare telehealth services so beneficiaries could get a broader range of services from healthcare professionals without traveling to healthcare settings. Additionally, from March 6, 2020, Medicare will pay for hospital, office, and other visits furnished via telehealth across the country. This is likely to have a positive impact on the market studied.

Moreover, vendors are engaged in partnerships, collaborations, acquisitions, mergers, and product launches to sustain in the market. For instance, in November 2020, Morneau Shepell introduced its first unified telemedicine solution in the United States. Under this service, regional employees and their families get access to digital health care support for all their crucial and immediate well-being needs. Also, in August 2020, AMD Global Telemedicine Inc. collaborated with iTelemed, an Ontario-based company, to provide virtual healthcare solutions to cater to the unmet healthcare needs of the marginalized populations within Canada during the COVID-19 pandemic.

Thus, given the aforementioned factors, the studied market is expected to grow significantly in North America over the forecast period.

The digital health market is moderately competitive. In terms of market share, a few of the major players are currently dominating the market. Some of the companies which are currently dominating the market are Allscripts Healthcare Solutions Inc., Koninklijke Philips N.V., OTH.IO, International Business Machinery Corporation (IBM), and AMD Global Telemedicine Inc., among others.