디지털 헬스 시장 : 제공별, 질환별, 사용 사례별, 최종사용자별, 지역별 - 예측(-2030년)

Digital Health Market by Offering (Hardware, Apps (Telehealth, DTx, Patient Portals, Pharmacy)), Disease, Use Case, End User, and Region - Global Forecast to 2030

상품코드:1812621

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 452 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

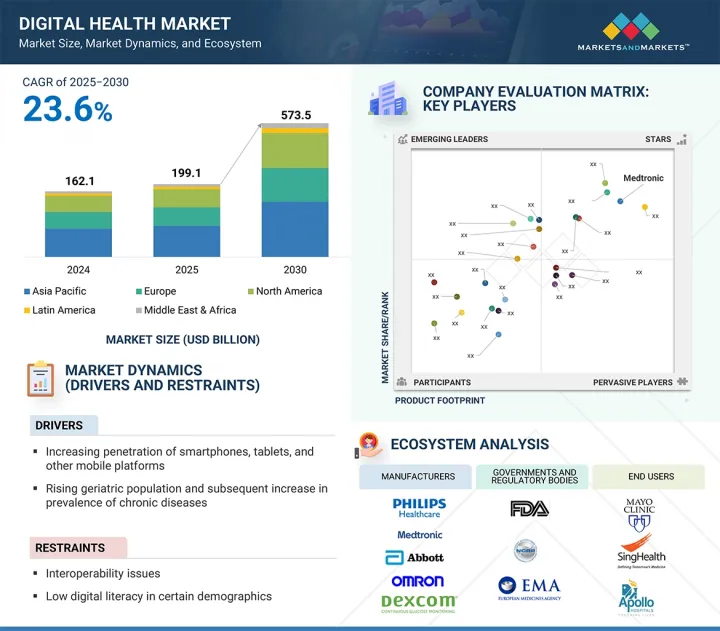

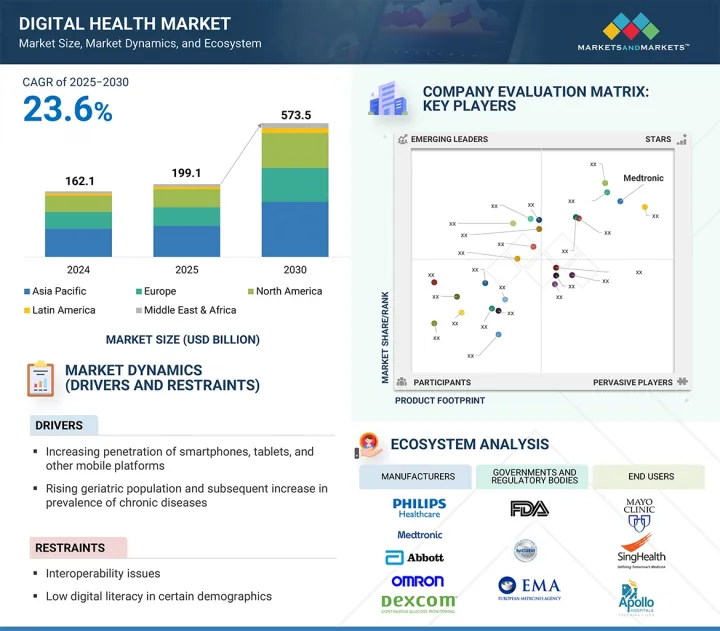

세계의 디지털 헬스 시장 규모는 예측 기간 동안 23.6%의 높은 CAGR로 확대되어 2025년 1,991억 달러에서 2030년에는 5,735억 달러에 달할 것으로 예측됩니다.

조사 범위

조사 대상 연도

2024-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문

제공별, 질환별, 사용 사례별, 최종사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카

가치 기반 케어에 대한 수요 증가, 만성질환의 부담 증가, 예방적 건강관리의 중요성 증가에 힘입어 시장은 꾸준히 발전하고 있습니다. 인구 고령화와 의료비 상승에 따라 의료 제공자와 지불자는 자원 활용을 최적화하고 치료 결과를 개선할 수 있는 디지털 도구에 주목하고 있습니다.

원격 환자 모니터링, 디지털 치료제, 모바일 헬스 앱 등의 솔루션은 특히 당뇨병, 고혈압, 심장병 등 만성질환의 지속적인 재택 치료를 가능하게 하는 데 중요한 역할을 하고 있습니다. 이 시장은 또한 디지털 개입에 대한 보험 적용 범위 확대, 건강 추적에 대한 소비자의 높은 관심, 의료 기술 및 주요 하이테크 기업의 혁신에 의해 뒷받침되고 있습니다. 이러한 기세에도 불구하고, 이 분야는 지속적인 도전에 직면해 있습니다. 데이터 보안과 프라이버시에 대한 우려, 신흥 디지털 치료제에 대한 규제의 불확실성, 고령층과 저소득층의 접근을 제한하는 디지털 격차 등이 대표적입니다. 확장 가능하고 공평하며 양질의 치료를 제공하는 디지털 헬스의 잠재력을 충분히 실현하기 위해서는 이러한 장벽을 해결해야 합니다.

2024년, 정신 및 행동 건강은 디지털 헬스 시장에서 가장 빠르게 성장하는 분야로 부상했습니다. 그 배경에는 정신건강에 대한 인식의 증가, 스트레스, 불안, 우울증의 유병률 증가, 도움 요청에 대한 편견의 감소 등이 있습니다. 원격 정신 의료, 치료 앱, AI 기반 정신건강 플랫폼의 확장으로 접근성, 경제성, 기밀성을 보장하는 동시에 웨어러블 기기 및 원격 모니터링과의 통합을 통해 행동 패턴의 실시간 추적이 가능해졌습니다. 이러한 요인들은 고용주의 웰니스 프로그램 및 지원적인 건강 관리 정책과 함께 이 부문의 급속한 보급과 시장 확장을 촉진하고 있습니다.

2024년 디지털 헬스 시장에서 가장 빠르게 성장하는 최종사용자 분야는 환자 및 소비자입니다. 이는 건강에 대한 인식의 증가, 스마트폰과 웨어러블의 보급률 증가, 개인화된 온디맨드 헬스케어 솔루션에 대한 수요 증가에 기인합니다. 디지털 건강 앱, 원격의료 플랫폼, 원격 모니터링 도구를 통해 개인은 자신의 건강을 능동적으로 관리하고, 언제든 의료 서비스를 이용할 수 있으며, 활력 징후와 생활습관 지표를 실시간으로 추적할 수 있습니다. 예방 의료, 편의성 중심의 의료 서비스 제공, 만성질환의 자가 관리로의 전환으로 환자와 소비자는 시장의 가장 역동적인 성장 동력이 되고 있습니다.

아시아태평양은 예측 기간 동안 디지털 헬스 시장에서 가장 빠른 성장을 기록할 것으로 예상됩니다. 원격의료, 전자의무기록, AI 주도형 헬스케어에 대한 정부의 추진 노력은 헬스케어 투자 증가와 민간 부문의 참여 확대와 맞물려 도입을 가속화하고 있습니다. Halodoc(인도네시아)과 같은 기업은 1억 달러(2023년)를 모금하여 총 2억 5,800만 달러에 달하며, 플랫폼의 월간 이용자 수는 2,000만 명을 넘어섰습니다. 인도의 Ayushman Bharat Digital Mission(ABDM)과 같은 정부 주도 이니셔티브는 EHR, 시민 건강 ID, 분석에 걸친 국가 디지털 건강 인프라를 구축하고 있습니다. 또한, 민간 기업의 강력한 참여, 벤처 캐피탈의 투자 증가, 기술 기업과 의료 서비스 제공자와의 전략적 제휴가 혁신을 촉진하고 있습니다.

본 보고서는 세계 디지털 헬스 시장을 조사했으며, 제품별, 질환별, 사용 사례별, 최종사용자별, 지역별 동향, 시장 진입 기업 프로파일 등을 정리하여 전해드립니다.

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요

소개

시장 역학

고객의 비즈니스에 영향을 미치는 동향/디스럽션

업계 동향

생태계 분석

공급망 분석

기술 분석

관세 및 규제 분석

가격 분석

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

특허 분석

미충족 수요와 최종사용자 기대

주요 회의와 이벤트

사례 연구 분석

디지털 헬스 시장 : 투자 상황과 자금 조달 시나리오

무역 분석

디지털 헬스 시장 비즈니스 모델

디지털 헬스 시장의 AI/생성형 AI의 영향

2025년 미국 관세의 영향 - 디지털 헬스 시장

상환 분석

위험요인과 시장 진입 장벽

향후 전망과 혼란 시나리오

제6장 디지털 헬스 시장(제공별)

소개

하드웨어

솔루션/애플리케이션

모바일 헬스 앱

디지털 치료제

디지털 약국과 의약품 액세스

디지털 진단과 재택 검사

환자 포털

기타

제7장 디지털 헬스 시장(질환별)

소개

당뇨병

심장병

정신건강과 행동 헬스

호흡기질환

라이프스타일과 건강 개선

신경학

근골격계 장애/통증 관리

종양학

여성 건강과 생식에 관한 건강

기타

제8장 디지털 헬스 시장(사용 사례별)

소개

예방 케어와 웰니스

진단

치료

환자 모니터링

재활과 회복

기타

제9장 디지털 헬스 시장(최종사용자별)

소개

헬스케어 제공자

의료 지불자

환자와 소비자

제약, 바이오테크놀러지, 의료 기술 기업

기타

제10장 디지털 헬스 시장(지역별)

소개

북미

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 거시경제 전망

독일

영국

프랑스

이탈리아

스페인

기타

아시아태평양

아시아태평양의 거시경제 전망

중국

일본

인도

호주

한국

기타

라틴아메리카

라틴아메리카의 거시경제 전망

브라질

멕시코

기타

중동 및 아프리카

중동 및 아프리카의 거시경제 전망

GCC

남아프리카공화국

기타

제11장 경쟁 구도

소개

주요 진출 기업의 전략/강점

주요 진출 기업의 매출 점유율 분석

시장 점유율 분석, 2024년

브랜드/소프트웨어 비교

기업 평가와 재무 지표

기업 평가 매트릭스 : 주요 진출 기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오와 동향

제12장 기업 개요

주요 진출 기업

MEDTRONIC

ABBOTT

DEXCOM, INC.

KONINKLIJKE PHILIPS N.V.

FITBIT, INC.(GOOGLE)

OMRON HEALTHCARE, INC.

APPLE, INC.

BOSTON SCIENTIFIC CORPORATION

MASIMO

TELADOC HEALTH, INC.

AMERICAN WELL

HIMS & HERS HEALTH, INC.

HEADSPACE

NOOM, INC.

CEREBRAL INC.

EPIC SYSTEMS CORPORATION

OMADA HEALTH INC.

ORACLE

CLICK THERAPEUTICS, INC.

WELLDOC, INC.

EVERLYWELL

기타 기업

TRUDOC HEALTHCARE LLC

CARESIMPLE INC.

VIVALNK, INC.

BIOBEAT

VIRTUAL THERAPEUTICS CORP.

제13장 부록

KSM

영문 목차

영문목차

The global digital health market is projected to reach USD 573.5 billion by 2030 from USD 199.1 billion in 2025, at a high CAGR of 23.6% during the forecast period.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Offering, disease, use case, and end user

Regions covered

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

The market is advancing steadily, propelled by the increasing demand for value-based care, the rising burden of chronic diseases, and a growing emphasis on preventive healthcare. With aging populations and escalating healthcare costs, providers and payers are turning to digital tools to improve care outcomes while optimizing resource utilization.

Solutions such as remote patient monitoring, digital therapeutics, and mobile health apps are playing a critical role in enabling continuous, at-home care, especially for chronic conditions like diabetes, hypertension, and heart disease. The market is further supported by expanding insurance coverage for digital interventions, strong consumer interest in health tracking, and innovation from both medtech and big tech players. Despite this momentum, the sector faces persistent challenges, chief among them are concerns over data security and privacy, regulatory uncertainty for emerging digital therapeutics, and the digital divide that limits access for elderly and low-income populations. These barriers must be addressed to fully realize the potential of digital health in delivering scalable, equitable, and high-quality care.

"Mental & behavioral health under the disease segment is expected to register the fastest growth during the forecast period."

In 2024, mental & behavioral health emerged as the fastest-growing segment of the digital health market. This is due to the rising awareness of mental well-being, increasing prevalence of stress, anxiety, and depression, and the reduced stigma around seeking help. The expansion of telepsychiatry, therapy apps, and AI-driven mental health platforms provides accessible, affordable, and confidential support, while integration with wearable devices and remote monitoring allows real-time tracking of behavioral patterns. These factors, combined with employer wellness programs and supportive healthcare policies, are driving rapid adoption and market expansion in this segment.

"The patients & consumers segment is projected to dominate the digital health market, by end user, during the forecast period."

In 2024, patients & consumers was the fastest-growing end-user segment in the digital health market. This is because of increasing health awareness, rising smartphone and wearable adoption, and the demand for personalized, on-demand healthcare solutions. Digital health apps, telemedicine platforms, and remote monitoring tools empower individuals to actively manage their health, access care anytime, and track vital signs or lifestyle metrics in real time. The shift toward preventive care, convenience-focused healthcare delivery, and self-management of chronic conditions has made patients and consumers the most dynamic growth driver in the market.

"Asia Pacific to witness the highest growth rate during the forecast period."

The Asia Pacific region is expected to register the fastest growth in the digital health market over the forecast period. Government initiatives promoting telemedicine, electronic health records, and AI-driven healthcare, combined with rising healthcare investments and expanding private sector participation, are accelerating adoption. Companies such as Halodoc (Indonesia) raised USD 100 million (in 2023), bringing its total to USD 258 million, with over 20 million monthly users on its platform. Government-led initiatives such as India's Ayushman Bharat Digital Mission (ABDM) is building a national digital health infrastructure, spanning EHRs, citizen health IDs, and analytics. In addition, strong private sector participation, increasing venture capital investments, and strategic partnerships between technology companies and healthcare providers are fueling innovation.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the authentication and brand protection marketplace. The break-down of primary interviews is as mentioned below:

By Company Type - Tier 1: 31%, Tier 2: 28%, and Tier 3: 41%

By Designation - C-level: 31%, Director-level: 25%, and Others: 44%

By Region - North America: 32%, Europe: 32%, Asia Pacific: 26%, Middle East & Africa: 5%, Latin America: 5%

Key Players in the Digital Health Market

The key players operating in the digital health market include Medtronic (Ireland), Abbott (US), OMRON Healthcare, Inc. (Japan), Koninklijke Philips N.V. (Netherlands), Apple Inc. (US), Fitbit (US), Dexcom, Inc. (US), Boston Scientific Corporation (US), Masimo (US), Teladoc Health, Inc. (US), American Well (US), Hims & Hers Health, Inc. (US), Headspace (US), Noom, Inc. (US), Cerebral Inc. (US), Epic System Corporation (US), Omada Health Inc. (US), ORACLE (US), Click Therapeutics (US), Welldoc, Inc. (US), EverlyWell (US), TruDoc Healthcare LLC (UAE), CareSimple Inc. (US), VivaLNK, Inc. (US), Biobeat (Israel), and Virtual Therapeutics Corp. (US).

Research Coverage:

The report analyzes the digital health market and aims to estimate the market size and future growth potential of various market segments, based on offering, disease, use case, end user, and region. The report also provides a competitive analysis of the key players operating in this market, along with their company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

This report will enrich established firms as well as new entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them garner a greater share of the market. Firms purchasing the report could use one or a combination of the following strategies to strengthen their positions in the market.

This report provides insights into:

Analysis of key drivers (Increasing penetration of smartphones, tablets, and other mobile platforms, Rising geriatric population and subsequent increase in prevalence of chronic diseases, Rising focus on patient-centric healthcare solutions, Increase in the use of wearables, Advancements in Al, Sensors & Connectivity (5G and 6G), Growth of Al-Powered Virtual Assistants and Chatbots), restraints (Interoperability issues, Low Digital Literacy in Certain Demographics), opportunities (Shift toward intelligent health ecosystem to deliver personalized health experiences, Increasing shift towards outpatient care model, Improving regulatory support and reimbursements, Advancements in digital health), and challenges (Clinical Validation & Long-Term Efficacy, Data Privacy and security concerns) influencing the growth of the digital health market

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the digital health market

Market Development: Comprehensive information on the lucrative emerging markets, components, deployments, technologies, applications, end users, and regions

Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the digital health market

Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, and capabilities of the leading players, like Medtronic (Ireland), Abbott (US), OMRON Healthcare, Inc. (Japan), Koninklijke Philips N.V. (Netherlands), and Apple Inc. (US), in the digital health market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 MARKET SCOPE

1.3.1 MARKETS COVERED AND REGIONS CONSIDERED

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.4 STAKEHOLDERS

1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary interviews

2.1.2.2 Insights from primary experts

2.1.2.3 Breakdown of primary sources

2.2 RESEARCH METHODOLOGY

2.3 MARKET SIZE ESTIMATION

2.4 DATA TRIANGULATION

2.5 MARKET RANKING ANALYSIS

2.6 RISK ASSESSMENT

2.7 STUDY ASSUMPTIONS

2.8 LIMITATIONS

2.8.1 METHODOLOGY-RELATED LIMITATIONS

2.8.2 SCOPE-RELATED LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 DIGITAL HEALTH MARKET OVERVIEW

4.2 NORTH AMERICA: DIGITAL HEALTH MARKET, BY END USER AND COUNTRY

4.3 DIGITAL HEALTH MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

4.4 DIGITAL HEALTH MARKET: REGIONAL MIX

4.5 DIGITAL HEALTH MARKET: DEVELOPED MARKETS VS. EMERGING ECONOMIES

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Increasing penetration of smartphones, tablets, and other mobile platforms

5.2.1.2 Rising geriatric population and subsequent increase in prevalence of chronic diseases

5.2.1.3 Rising focus on patient-centric healthcare solutions

5.2.1.4 Rising use of wearables

5.2.1.5 Advancements in AI, sensors, and connectivity (5G and 6G)

5.2.1.6 Growth of AI-powered virtual assistants and chatbots

5.2.2 RESTRAINTS

5.2.2.1 Low digital literacy in certain demographics

5.2.2.2 Interoperability issues

5.2.3 OPPORTUNITIES

5.2.3.1 Shift toward intelligent health ecosystem to deliver personalized health experiences

5.2.3.2 Increasing shift towards outpatient care

5.2.3.3 Improving regulatory support and reimbursements

5.4.1 EMERGENCE OF VALUE-BASED STRATEGY FOR CONTINUOUS CARE

5.4.2 HOME: NEW HEALTHCARE HUB

5.4.3 TECHNOLOGICALLY ENABLED PRIMARY CARE SERVICES

5.4.4 RISING AWARENESS OF DIGITAL THERAPEUTICS TO TREAT HUMAN DISEASES

5.4.5 SURGE IN MHEALTH APPS

5.5 ECOSYSTEM ANALYSIS

5.6 SUPPLY CHAIN ANALYSIS

5.7 TECHNOLOGY ANALYSIS

5.7.1 KEY TECHNOLOGIES

5.7.1.1 mHealth apps

5.7.1.2 Wearable sensors & devices

5.7.1.3 Remote patient monitoring

5.7.1.4 Digital therapeutics

5.7.1.5 Telehealth/virtual care platforms

5.7.1.6 AI-powered tools

5.7.2 COMPLEMENTARY TECHNOLOGIES

5.7.2.1 Cloud computing & edge processing

5.7.2.2 Data analytics & visualization

5.7.2.3 Bluetooth & IoT connectivity

5.7.2.4 EHR integration

5.7.3 ADJACENT TECHNOLOGIES

5.7.3.1 Digital twins

5.7.3.2 AR/VR & extended reality (XR)

5.7.3.3 Voice assistants/smart speakers

5.8 TARIFF AND REGULATORY ANALYSIS

5.8.1 TARIFF DATA FOR HS CODE 9018

5.8.2 TARIFF DATA FOR HS CODE 9021

5.8.3 TARIFF DATA FOR HS CODE 8517

5.8.4 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.8.5 REGULATORY FRAMEWORK

5.9 PRICING ANALYSIS

5.9.1 INDICATIVE PRICE, BY OFFERING

5.9.2 INDICATIVE PRICE, BY REGION

5.10 PORTER'S FIVE FORCES ANALYSIS

5.10.1 INTENSITY OF COMPETITIVE RIVALRY

5.10.2 BARGAINING POWER OF BUYERS

5.10.3 THREAT OF SUBSTITUTES

5.10.4 THREAT OF NEW ENTRANTS

5.10.5 BARGAINING POWER OF SUPPLIERS

5.11 KEY STAKEHOLDERS AND BUYING CRITERIA

5.11.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.11.2 BUYING CRITERIA

5.12 PATENT ANALYSIS

5.12.1 PATENT PUBLICATION TRENDS FOR DIGITAL HEALTH MARKET

5.12.2 JURISDICTION ANALYSIS: TOP APPLICANT COUNTRIES FOR DIGITAL HEALTH

5.12.3 MAJOR PATENTS IN DIGITAL HEALTH MARKET

5.13 UNMET NEEDS AND END-USER EXPECTATIONS

5.13.1 UNMET NEEDS IN DIGITAL HEALTH MARKET

5.13.2 END-USER EXPECTATIONS

5.14 KEY CONFERENCES AND EVENTS

5.15 CASE STUDY ANALYSIS

5.15.1 CASE STUDY 1: CLINICAS DEL AZUCAR (CDA)

5.15.2 CASE STUDY 2: NOVA HOSPITAL & ENOVACOM

5.15.3 CASE STUDY 3: APPLE & NHS TEAMS

5.16 DIGITAL HEALTH MARKET: INVESTMENT LANDSCAPE AND FUNDING SCENARIO

5.17 TRADE ANALYSIS

5.17.1 TRADE ANALYSIS FOR DIGITAL HEALTH DEVICES (HSN CODE 8518)

5.17.2 TRADE ANALYSIS FOR DIGITAL HEALTH DEVICES (HSN CODE 9021)

5.17.3 TRADE ANALYSIS FOR DIGITAL HEALTH DEVICES (HSN CODE 9022)

5.17.4 TRADE ANALYSIS FOR DIGITAL HEALTH DEVICES (HSN CODE 9018)

5.18 DIGITAL HEALTH MARKET BUSINESS MODELS

5.18.1 SUBSCRIPTION-BASED MODELS

5.18.2 SOFTWARE AS A SERVICE (SAAS)/PLATFORM AS A SERVICE (PAAS)

5.18.3 FREEMIUM MODELS WITH TIERED ACCESS

5.18.4 OUTCOMES-BASED AND VALUE-BASED MODELS

5.19 IMPACT OF AI/GEN AI IN DIGITAL HEALTH MARKET

5.19.1 KEY USE CASES

5.19.2 CASE STUDIES OF AI/GENERATIVE AI IMPLEMENTATION

5.19.2.1 Artificial intelligence in public health

5.19.2.2 Artificial intelligence in digital health-issues and dimensions of ethical concerns

5.19.3 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

5.19.3.1 Telehealth and telemedicine

5.19.3.2 Wearable devices

5.19.3.3 Remote patient monitoring (RPM)

5.19.3.4 Mobile health (mHealth)

5.19.4 USER READINESS & IMPACT ASSESSMENT

5.19.4.1 User readiness

5.19.4.1.1 User A: Healthcare providers

5.19.4.1.2 User B: Healthcare payers

5.19.4.1.3 User C: Patients & consumers

5.19.4.1.4 User D: Pharmaceutical, biotech, and MedTech companies (including CROs)

5.19.4.1.5 User E: Other end users (academic institutes, research centers, government bodies)

5.19.4.2 Impact assessment

5.19.4.2.1 User A: Healthcare providers

5.19.4.2.1.1 Implementation

5.19.4.2.1.2 Impact

5.19.4.2.2 User B: Healthcare payers

5.19.4.2.2.1 Implementation

5.19.4.2.2.2 Impact

5.19.4.2.3 User C: Patients & consumers

5.19.4.2.3.1 Implementation

5.19.4.2.3.2 Impact

5.19.4.2.4 User D: Pharmaceutical, biotech, and MedTech companies (including CROs)

5.19.4.2.4.1 Implementation

5.19.4.2.4.2 Impact

5.19.4.2.5 User E: Other end users (academic institutes, research centers, government bodies)

5.19.4.2.5.1 Implementation

5.19.4.2.5.2 Impact

5.20 IMPACT OF 2025 US TARIFFS-DIGITAL HEALTH MARKET

5.20.1 INTRODUCTION

5.20.2 KEY TARIFF RATES

5.20.3 PRICE IMPACT ANALYSIS

5.20.4 IMPACT ON COUNTRIES/REGIONS

5.20.4.1 US

5.20.5 EUROPE

5.20.6 ASIA PACIFIC

5.20.7 IMPACT ON END-USE INDUSTRIES

5.20.7.1 Healthcare providers

5.20.7.2 Healthcare payers

5.20.7.3 Patients and consumers

5.20.7.4 Pharmaceutical, biotechnology, and MedTech companies

5.20.7.5 Other end users

5.21 REIMBURSEMENT ANALYSIS

5.22 RISK FACTORS AND MARKET ENTRY BARRIERS

5.23 FUTURE OUTLOOK AND DISRUPTION SCENARIOS

6 DIGITAL HEALTH MARKET, BY OFFERING

6.1 INTRODUCTION

6.2 HARDWARE

6.2.1 SMART HARDWARE SOLUTIONS VITAL IN POWERING DIGITAL HEALTH

6.2.2 WEARABLES

6.2.2.1 Wearables to empower patients with real-time health monitoring

6.2.3 CONSUMER-GRADED WEARABLE HEALTHCARE DEVICES

6.2.3.1 Wearable healthcare devices to empower consumers to be proactive about their well-being

6.2.4 CLINICAL-GRADE WEARABLE HEALTHCARE DEVICES

6.2.4.1 Clinical-grade devices to allow remote care with continuous monitoring

6.2.5 IMPLANTABLE DEVICES

6.2.5.1 Real-time data transmission to healthcare providers for proactive intervention and personalized care

6.2.6 HANDHELD & PORTABLE DEVICES

6.2.6.1 Compact design and integration with mobile health applications to make them highly effective for use in remote care

6.2.7 STATIONARY DEVICES

6.2.7.1 Stationary devices to be upgraded with IoT integration, AI-driven analytics, and cloud-enabled interoperability

6.3 SOLUTIONS/APPLICATIONS

6.3.1 TELEHEALTHCARE/TELEMEDICINE

6.3.1.1 Demand to advance connected care via virtual health platforms

6.3.2 REMOTE PATIENT MONITORING

6.3.2.1 Expected to be more seamlessly integrated with telemedicine platforms, expanding their capabilities

6.3.3 VIRTUAL CARE & VIDEO CONSULTATION

6.3.3.1 Offering enhanced efficiency, accessibility, and accuracy in remote healthcare, assisting in triaging patients and automating documentation

6.3.4 VIRTUAL SITTING & NURSING PLATFORMS

6.3.4.1 Offering remote patient monitoring with bidirectional communication

6.4 MHEALTH APPS

6.4.1 TRANSFORMING CARE DELIVERY WITH MOBILE HEALTH SOLUTIONS

6.5 DIGITAL THERAPEUTICS

6.5.1 EMPOWERING HEALTH BY COMBINING REAL-TIME DATA COLLECTION, PATIENT ENGAGEMENT TOOLS, AND INTEGRATION WITH HEALTHCARE PROVIDERS' SYSTEMS

6.6 DIGITAL PHARMACY & MEDICATION ACCESS

6.6.1 ENHANCING MEDICATION ACCESS BY REACHING RURAL OR UNDERSERVED POPULATIONS, REDUCING TRAVEL AND WAIT TIMES, AND IMPROVING CONTINUITY OF CARE

6.7 DIGITAL DIAGNOSTICS & AT-HOME TESTING

6.7.1 MOSTLY USED IN GLUCOSE MONITORING AND OTHER INFECTIOUS DISEASE TESTS, CHOLESTEROL AND LIPID PANELS, GENETIC TESTING, AND HORMONE OR FERTILITY ASSESSMENTS

6.8 PATIENT PORTALS

6.8.1 PERSONALIZED HEALTH CONTENT, APPOINTMENT REMINDERS, AND SECURE MESSAGING AIM TO IMPROVE PATIENT ENGAGEMENT AND CARE COORDINATION

6.9 OTHER DIGITAL HEALTH SOLUTIONS/APPLICATIONS

7 DIGITAL HEALTH MARKET, BY DISEASE

7.1 INTRODUCTION

7.2 DIABETES

7.2.1 INTEGRATING AI IN DIGITAL HEALTH TO CATER TO DIABETIC PATIENTS

7.3 CARDIOLOGY

7.3.1 OFFERING EARLIER DETECTION, CONTINUOUS MONITORING, AND PERSONALIZED MANAGEMENT OF CARDIOVASCULAR CONDITIONS

7.4 MENTAL HEALTH & BEHAVIORAL HEALTH

7.4.1 IMPROVING ACCESSIBILITY TO MENTAL HEALTH SERVICES, ESPECIALLY IN UNDERSERVED REGIONS

7.5 RESPIRATORY DISORDERS

7.5.1 ENABLING REAL-TIME MONITORING OF LUNG FUNCTION, MEDICATION ADHERENCE, AND OXYGEN LEVELS

7.6 LIFESTYLE & WELLNESS IMPROVEMENT

7.6.1 EXPANDING ACCESS AND PERSONALIZING CARE IN MENTAL & BEHAVIORAL HEALTH THROUGH DIGITAL HEALTH

7.7 NEUROLOGY

7.7.1 ADVANCING NEUROLOGICAL CARE WITH DIGITAL HEALTH INNOVATIONS

7.8 MUSCULOSKELETAL DISORDERS/PAIN MANAGEMENT

7.8.1 ACCELERATING INNOVATION IN HANDHELD & PORTABLE DEVICES TO BOOST MARKET GROWTH

7.9 ONCOLOGY

7.9.1 ADOPTION OF AI IN REMOTE PATIENT MONITORING (RPM) TO LEAD TO ITS EMERGING AS PROMISING SOLUTION TO SUPPORT PERSONALIZED CARE

7.10 WOMEN'S HEALTH & REPRODUCTIVE HEALTH

7.10.1 ENHANCING PREVENTIVE CARE, EMPOWERING WOMEN WITH SELF-MANAGEMENT TOOLS, AND STRENGTHENING OUTCOMES IN REPRODUCTIVE AND MATERNAL HEALTH

7.11 OTHER DISEASES

8 DIGITAL HEALTH MARKET, BY USE CASE

8.1 INTRODUCTION

8.2 PREVENTIVE CARE & WELLNESS

8.2.1 DRIVING PROACTIVE HEALTH MANAGEMENT THROUGH DIGITAL INNOVATION

8.3 DIAGNOSIS

8.3.1 ADVANCING DIAGNOSIS THROUGH AI-POWERED SYMPTOM CHECKING AND EARLY DETECTION

8.4 TREATMENT

8.4.1 FEEDING REAL-TIME DATA TO HEALTHCARE PROVIDERS, ALLOWING TREATMENT ADJUSTMENTS AND PROACTIVE INTERVENTIONS

8.5 PATIENT MONITORING

8.5.1 SHIFT TOWARD PERSONALIZED, SCALABLE, AND PREVENTIVE CARE

8.6 REHABILITATION & RECOVERY

8.6.1 PARTICULARLY IMPACTFUL IN POST-SURGICAL CARE, NEUROLOGICAL REHABILITATION, STROKE RECOVERY, AND MUSCULOSKELETAL THERAPY

8.7 OTHER USE CASES

9 DIGITAL HEALTH MARKET, BY END USER

9.1 INTRODUCTION

9.2 HEALTHCARE PROVIDERS

9.2.1 HOSPITALS

9.2.1.1 Rise in demand for high-quality care and government support to encourage digital health adoption in hospitals

9.2.2 CLINICS & OTHER OUTPATIENT SETTINGS

9.2.2.1 Increase in demand for cost-effective care and postoperative monitoring to drive digital health adoption in outpatient settings

9.2.3 OTHER HEALTHCARE PROVIDERS

9.3 HEALTHCARE PAYERS

9.3.1 PUBLIC PAYERS

9.3.1.1 Driving population health and value-based care through digital innovation