ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

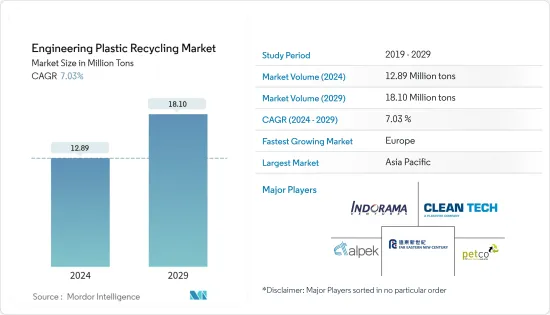

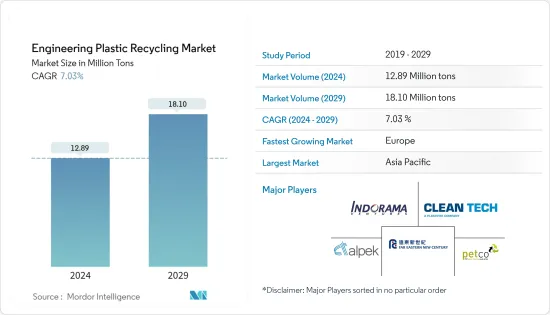

엔지니어링 플라스틱 재활용 시장 규모는 2024년 1,289만 톤으로 추정되며, 2029년까지 1,810만 톤에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 7.03%의 CAGR로 성장할 것으로 예상됩니다.

신종 코로나바이러스 감염증(COVID-19) 사태는 엔지니어링 플라스틱 재활용 부문에 큰 타격을 입혔습니다. 전 세계 봉쇄와 각국 정부의 엄격한 규제로 인해 대부분의 생산 기지가 폐쇄되어 큰 타격을 입었습니다. 그럼에도 불구하고 2021년 이후 사업이 회복되고 있으며 향후 몇 년 동안 크게 증가할 것으로 예상됩니다.

주요 하이라이트

조사 대상 시장의 성장을 촉진하는 주요 요인은 소비자와 포장 제품 사이에서 지속가능성에 대한 중요성이 증가하고 재활용 폴리에스테르의 사용이 증가하고 있다는 점입니다.

한편, 혼합 플라스틱의 수집 및 분류의 어려움은 시장 성장을 저해할 것으로 예상됩니다.

플라스틱의 자동 처리 및 분류를 위한 재활용 기술의 혁신은 세계 엔지니어링 플라스틱 재활용 시장에 충분한 기회를 제공할 것으로 예상됩니다.

아시아태평양이 가장 큰 점유율을 차지했습니다. 그러나 유럽은 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 예상됩니다.

엔지니어링 플라스틱 재활용 시장 동향

시장을 독식하는 포장 산업

PET는 포장용으로 가장 널리 사용되는 플라스틱 중 하나이며, 식품에 안전할 뿐만 아니라 강도가 높고, 가볍고, 투명하고, 비산 방지 특성이 있습니다. 또한 PET는 이산화탄소를 효과적으로 차단하는 특성으로 인해 음료 및 경질 식품 포장에 탁월한 선택이 될 수 있습니다.

영국 플라스틱 연맹(BPF)은 현재 청량음료(탄산음료, 탄산음료, 탄산음료, 탄산음료, 과일주스, 생수)의 거의 70%가 PET 플라스틱 병으로 포장되어 있다고 밝혔습니다.

또한 BP plc는 PET는 일반적으로 식품의 경질 포장에 사용되며 전 세계적으로 연간 약 2,700 만 톤의 PET가 이러한 용도로 사용되며 그 중 약 2,300 만 톤의 대부분이 병에 사용된다고 밝혔습니다. 재활용 PET는 새로운 포장 제품에서 버진 PET 폴리머의 전부 또는 일부를 대체 할 수 있습니다.

많은 대형 포장 회사들이 폐기물 관리에 대한 계획을 세우고 있으며, 재활용이 주목을 받고 있습니다. 많은 기업들이 가정용 폐기물 관리에서 플라스틱 병을 회수하여 플라스틱 조각으로 가공하여 포장 용도로 더 많이 사용하고 있습니다.

전 세계 많은 대형 브랜드가 음료 제품의 탄소 배출량을 줄이기 위해 재활용 PET를 사용하기 위해 노력하고 있습니다. 여기에는 코카콜라, 네슬레 워터스, 펩시콜라, 다논 등이 포함되며, 다른 청량음료 및 생수 판매 회사들은 2030년까지 일회용 플라스틱 사용을 중단할 것을 약속했습니다.

FPA(Flexible Packaging Association)에 따르면 미국 포장 산업은 2022년 연포장 분야에서 1,850억 달러로 평가되어 전체 시장의 약 20%를 차지할 것으로 예상됩니다. 2022년 연 포장의 전년 대비 성장률은 12.1% 증가했습니다.

따라서 포장 산업은 시장을 독점 할 것으로 예상되며 엔지니어링 플라스틱 재활용 시장에서 활동하는 플레이어에게 많은 성장 기회를 제공 할 것으로 예상됩니다.

아시아태평양이 시장을 독점

아시아태평양은 중국, 일본, 인도의 플라스틱 재활용 수요로 인해 엔지니어링 플라스틱 재활용 시장을 장악했습니다.

중국은 세계 최대의 폴리에틸렌 테레프탈레이트(PET) 소비국 중 하나입니다. 풍부한 원자재 가용성과 낮은 생산 비용으로 인해 지난 몇 년 동안 중국 내 PET를 비롯한 엔지니어링 플라스틱의 생산 성장이 지속되고 있습니다.

중국 국가통계국에 따르면 2022년 상반기 중국의 플라스틱 제품 생산량은 약 3,821만 톤, 2021년에는 약 8,004만 톤에 달할 것으로 예상됩니다.

인도 브랜드 주식 재단(IBEF)에 따르면 2022년 4월부터 2023년 2월까지 인도의 플라스틱 수출은 109억 달러였습니다. 또한 PET 포장 청정 환경 협회(PACE)와 국립 화학 연구소(NCL)에 따르면 인도의 재활용 PET 플라스틱 산업 규모는 약 4억 - 5억 5 천만 달러로 추산됩니다. 이처럼 플라스틱 수출과 재활용 활동의 증가로 인해 엔지니어링 플라스틱 재활용 시장이 확대되고 있습니다.

또한 포장, 자동차, 전기, 전자 등 많은 최종 사용 산업에서 재생 플라스틱에 대한 수요가 크게 증가하여 시장 성장을 더욱 촉진하고 있습니다.

예를 들어, OICA에 따르면 2022년 아시아태평양의 총 자동차 생산량은 5,002,793대로 2021년 4,676만 8,800대에 비해 7% 증가할 것으로 예상됩니다.

따라서 플라스틱 생산 증가, 재활용 활동의 눈에 띄는 성장, 일부 최종사용자 산업의 큰 수요는 엔지니어링 플라스틱 재활용 시장의 성장을 주도하고 있습니다.

플라스틱 재활용 산업 개요

엔지니어링 플라스틱 재활용 시장은 지역 시장 기업의 지배력이 매우 높기 때문에 매우 세분화되어 있습니다. 시장의 주요 기업으로는(순서에 관계없이) Indorama Ventures Public Company Limited, Clean Tech UK Ltd, Far Eastern New Century Corporation(Phoenix Technologies), Alpek SAB de CV, Petco 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 서론

조사 가정

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

소비자 제품 및 포장 제품의 지속가능성 중시 상승

재생 폴리에스테르 사용 증가

기타 촉진요인

성장 억제요인

혼합 플라스틱의 회수·분별 어려움

기타 저해요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협

경쟁 정도

제5장 시장 세분화(시장 규모 : 수량 기준)

플라스틱 종류

폴리카보네이트

폴리에틸렌 테레프탈레이트(PET)

스티렌 코폴리머(ABS, SAN)

폴리아미드

기타

최종 이용 산업

포장

산업용 실

전기·전자

기타

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

세계 기타 지역

남미

중동 및 아프리카

제6장 경쟁 상황

M&A, 합작투자, 제휴, 협정

시장 점유율 분석(%)/순위 분석

주요 기업의 전략

기업 개요

Alpek S.A.B. de C.V.

Clean Tech UK Ltd

Euresi Plastics SL

EF Plastics UK Ltd

Far Eastern New Century Corporation(Phoenix Technologies)

Indorama Ventures Public Company Limited

JFC Group

Krones AG

Petco

Placon

PolyClean Technologies

Reliance Industries Limited

REPRO-PET

TEIJIN LIMITED

UltrePET LLC

제7장 시장 기회와 향후 동향

ksm

영문 목차

영문목차

The Engineering Plastic Recycling Market size is estimated at 12.89 Million tons in 2024, and is expected to reach 18.10 Million tons by 2029, growing at a CAGR of 7.03% during the forecast period (2024-2029).

The COVID-19 pandemic harmed the engineering plastic recycling sector. Global lockdowns and severe rules enforced by governments resulted in a catastrophic setback as most production hubs were shut down. Nonetheless, the business has been recovering since 2021 and is expected to rise significantly in the coming years.

Key Highlights

The major factor driving the growth of the market studied is the growing emphasis on sustainability among consumers and packaging products and the increasing use of recycled polyester.

On the flip side, difficulty in collecting and sorting mixed plastic is expected to hinder the market's growth.

Innovations in recycling technologies for the automatic processing and sorting of plastics are expected to provide ample opportunities in the global engineering plastic recycling market.

The Asia-Pacific region accounted for the largest share; however, Europe is expected to register the highest CAGR during the forecast period.

Plastic Recycling Market Trends

Packaging Industry to Dominate the Market

PET is one of the most widely used plastics for packaging applications. Apart from being food-safe, PET is also strong, lightweight, transparent, and shatter-resistant. Moreover, the characteristics of PET, as an effective barrier to carbon dioxide, make it an unrivaled choice for beverage and rigid food packaging.

British Plastics Federation (BPF) stated that, at present, nearly 70% of soft drinks (carbonated drinks, still and dilatable drinks, fruit juices, and bottled water) are packaged in PET plastic bottles.

Further, BP p.l.c. stated that PET is usually used in rigid food packaging, and per year, nearly 27 million metric tons of PET are used in these applications globally, with the majority, around 23 million tons, used in bottles. Recycled PET can replace all or a proportion of virgin PET polymer in new packaging products.

Recycling has been gaining traction as many major packaging companies are planning initiatives for waste management. Many companies are collecting PET bottles from domestic waste management and then processed into plastic flakes to further use in packaging applications.

Numerous major brands worldwide are committed to using recycled PET to reduce the carbon footprint of their drink products. Some of these include Coca-Cola, Nestle Waters, PepsiCo, and Danone, others that sell soft drinks and bottled water, have committed to stop using single-use plastics by 2030.

According to Flexible Packaging Association (FPA), the United States packaging industry was valued at USD 185 billion in 2022 in flexible packaging, accounting for around 20% of the total market share. The year-on-year growth of flexible packaging in 2022 was up 12.1%.

Hence, the packaging industry is expected to dominate the market and expect to provide numerous growth opportunities to the players operating in the engineering plastic recycling market.

Asia-Pacific Region to Dominate the Market

The Asia-Pacific region dominated the engineering plastic recycling market owing to the demand for plastic recycling from China, Japan, and India.

China is one of the largest global polyethylene terephthalate (PET) consumers. The abundant availability of raw materials and the low cost of production have supported the production growth of engineering plastics, such as PET, in the country for the past few years.

According to the National Bureau of Statistics of China, in H1 2022, China produced plastic products to nearly 38.21 million metric tons, around 80.04 million metric tons in 2021.

According to the Indian Brand Equity Foundation (IBEF), India's plastic export from April-2022 to February 2023 stood at USD 10.9 billion. Further, according to PET Packaging Association for Clean Environment (PACE) and National Chemical Laboratory (NCL), the Indian recycled PET plastic industry was estimated to be around USD 400-550 million. Thus, increasing plastic export and recycling activities is boosting the engineering plastic recycling market.

Further, the significant demand for recycled plastic in numerous end-use industries, such as packaging, automotive, electrical, and electronics, is further propelling the market growth.

For instance, according to OICA, in 2022, the total production of motor vehicles in Asia-Pacific amounted to 50,020,793 units which was increased by 7% compared to 2021, which accounted for 46,768,800 units.

Thus, the rise in plastic production, remarkable growth in recycling activities, and significant demand for several end-user industries is propelling the growth of the engineering plastic recycling market.

Plastic Recycling Industry Overview

The engineering plastic recycling market is highly fragmented as the dominance of regional market players is extremely high. Some of the major players in the market (in no particular order) include Indorama Ventures Public Company Limited, Clean Tech U.K. Ltd, Far Eastern New Century Corporation (Phoenix Technologies), Alpek S.A.B. de C.V., and Petco.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Emphasis on Sustainability among Consumer and Packaging Products

4.1.2 Increasing Use of Recycled Polyester

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Difficulty in Collecting and Sorting Mixed Plastic

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Plastic Type

5.1.1 Polycarbonate

5.1.2 Polyethylene Terephthalate (PET)

5.1.3 Styrene Copolymers (ABS and SAN)

5.1.4 Polyamide

5.1.5 Other Engineering Plastics

5.2 End-user Industry

5.2.1 Packaging

5.2.2 Industrial Yarn

5.2.3 Electrical and Electronics

5.2.4 Other End-user Industries

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Rest of Europe

5.3.4 Rest of the World

5.3.4.1 South America

5.3.4.2 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share Analysis (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Alpek S.A.B. de C.V.

6.4.2 Clean Tech UK Ltd

6.4.3 Euresi Plastics SL

6.4.4 EF Plastics UK Ltd

6.4.5 Far Eastern New Century Corporation (Phoenix Technologies)

6.4.6 Indorama Ventures Public Company Limited

6.4.7 JFC Group

6.4.8 Krones AG

6.4.9 Petco

6.4.10 Placon

6.4.11 PolyClean Technologies

6.4.12 Reliance Industries Limited

6.4.13 REPRO-PET

6.4.14 TEIJIN LIMITED

6.4.15 UltrePET LLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Innovations in Recycling Technologies for Automatic Processing and Sorting of Plastics