ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

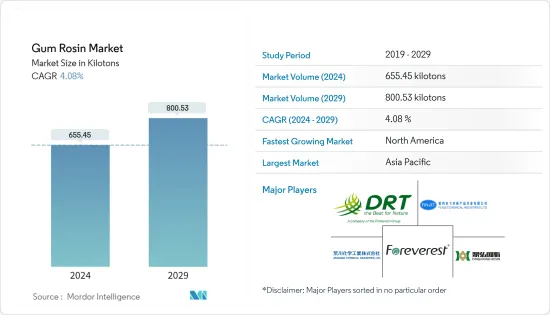

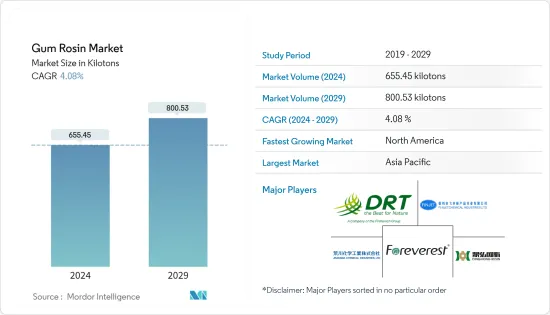

검로진 시장 규모는 2024년 65만 5,450톤으로 추정되며, 2029년까지 80만 530톤에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 4.08%의 CAGR로 성장할 것으로 예상됩니다.

주요 하이라이트

검로진 시장은 신종 코로나바이러스 감염증(COVID-19) 팬데믹으로 인해 부정적인 영향을 받았습니다. 그러나 COVID-19 이후 접착제, 실란트, 인쇄 잉크 등의 용도가 증가하면서 시장이 크게 회복되었습니다.

바이오 기반 접착제 및 실란트에 대한 수요 증가와 종이 포장 산업의 급속한 성장은 중기적으로 검로진 시장 성장의 주요 원동력이 될 수 있습니다.

한편, 톨루로진 기반 페놀 수지로의 관심 전환은 검로진 시장의 성장을 제한할 것으로 예상됩니다.

그럼에도 불구하고 경기장 바닥용 미끄럼 방지제에 대한 수요 증가와 제약 산업에서의 새로운 용도는 곧 세계 시장에서 유리한 성장 기회를 창출할 수 있습니다.

아시아태평양은 중국, 인도, 일본 등 국가의 막대한 소비로 인해 예측 기간 동안 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다.

검로진 시장 동향

접착제 및 실란트 부문이 시장을 독점할 것으로 예상

검로진은 접착제의 우수한 점착제 역할을 하기 때문에 수십 년 동안 접착제 및 실란트 산업 밸류체인의 중요한 구성요소 중 하나였습니다.

검로진은 열용융 접착제, 감압 접착제 및 고무 기반 접착제의 원료로 널리 사용됩니다. 이 로진은 주로 접착제의 강도, 가소성 및 점도를 높이는 데 사용됩니다.

접착제는 신발, 자동차, 종이팩, 가구, 부직포 및 기타 여러 제품의 필수 구성요소입니다. 접착제와 실란트는 건설, 제약, 포장 등 많은 산업 분야에서 응용되고 있습니다.

옥스포드 이코노믹스에 따르면 세계 건설 산업은 2025년까지 13조 3,000억 달러에 달할 것으로 예상되며, 2020년부터 5년 동안 생산량은 2조 6,000억 달러 증가할 것으로 예상됩니다. 중국, 인도, 미국, 인도네시아는 건설 산업에서 상당한 성장을 기록할 것으로 예상됩니다. 향후 몇 년 동안 산업. 중국만 세계 성장의 26.1%를 차지할 것입니다. 인도는 세계 성장의 14.1 %, 미국은 11.1 %, 인도네시아는 7.0%를 차지할 것으로 예상됩니다.

미국 인구조사국에 따르면 2022년 미국의 상업용 건설 규모는 1,147억 9,000만 달러로 전년 대비 21.4%의 성장률을 기록할 것으로 예상됩니다.

전 세계 접착제 및 실란트 제조업체의 식품 및 포장 안전은 전 세계 접착제 및 실란트 제조업체의 관심사이기 때문에 검로진 산업은 접착제 및 실란트 산업과 협력 기회를 식별하고 파트너십을 구축하려고 노력하고 있습니다.

중국은 국내 E-Commerce 당 소득 증가 등의 요인으로 인해 세계 최대 포장재 소비국이 되었습니다. 인도 플라스틱 산업 협회에 따르면 인도의 포장 산업은 세계에서 5번째로 큰 산업으로 매년 약 22-25%씩 성장하고 있습니다. 고도로 숙련된 인력과 저렴한 인건비 덕분에 식품 포장 및 가공 비용은 유럽보다 40% 낮을 수 있습니다.

인도포장산업협회(PIAI)에 따르면 인도의 포장 산업은 예측 기간 동안 22% 성장할 것으로 예상됩니다. 또한 인도의 포장 시장은 2025년까지 2,048억 1,000만 달러에 달할 것으로 예상되며, 2020년에서 2025년 사이에 26.7%의 CAGR을 기록할 것으로 예상됩니다.

환경 오염에 대한 우려가 높아지고 접착제의 바람직한 특성에 따라 검로진 수지를 조정할 수 있기 때문에 바이오 기반 접착제 및 실란트의 적용으로 인해 향후 몇 년 동안 검로진에 대한 시장 수요가 증가할 것으로 예상됩니다.

아시아태평양이 시장을 독점

아시아태평양은 급성장하는 자동차 부문과 중국과 인도의 건설 활동 증가로 인해 예측 기간 동안 감로진 시장을 장악할 것으로 예상됩니다.

세계 도료 및 코팅 산업 협회에 따르면 2022년 아시아태평양의 도료 및 코팅 산업의 가치는 630억 달러에 달할 것으로 추정됩니다. 이 지역 시장은 중국이 주도하고 있으며 CAGR 5.8%로 성장하고 있습니다. 2022년 중국 시장은 5.7% 성장할 것으로 예상됩니다. 현재 추세에 따르면 2022년 중국의 페인트 및 코팅 총 매출액은 450억 달러를 넘어설 것으로 예상됩니다. 동아시아에서 중국은 78%로 가장 큰 시장 점유율을 차지했습니다.

인도는 2022년 기준 세계 4위의 고무 소비국입니다. 인도의 1인당 고무 사용량은 현재 1.2킬로그램이지만 세계적으로는 3.2킬로그램입니다. 인도 고무 산업은 약 12,000 인도 루피(약 14억 달러)의 수익을 창출하고 있습니다.

자동차 산업에서 검로진은 휘발유, 테레빈유, 알코올 등 유기 용매에 쉽게 용해되기 때문에 코팅 및 페인트 제조에 사용됩니다. 중국자동차공업협회(CAAM)에 따르면 중국은 세계 최대의 자동차 생산기지를 보유하고 있으며, 2022년 자동차 총 생산량은 2,700만 대에 달해 지난해 생산량 2,600만 대에 비해 3.4% 증가할 것으로 예상했습니다. 또한 2022년 첫 7개월 동안 1,457만 대의 자동차를 생산해 전년 대비 31.5%의 성장률을 기록했습니다.

건설 업계에서 검로진은 주로 콘크리트 발포제 및 바닥 타일의 접착제로 사용됩니다. 인도 정부는 약 13억 명에게 주택을 제공하기 위해 주택 건설을 적극적으로 추진하고 있습니다. 향후 7년간 약 1조 3,000억 달러의 주택 투자가 이루어질 것으로 예상되며, 인도에서 6,000만 채의 신규 주택이 건설될 것으로 예상됩니다. 2024년까지 저렴한 주택의 가용성은 약 70% 증가할 것으로 예상됩니다.

앞서 언급한 요인으로 인해 예측 기간 동안 검로진에 대한 수요가 증가할 수 있습니다.

검로진 산업 개요

세계 검로진 시장은 본질적으로 매우 세분화되어 있습니다. 주요 업체로는 Guangxi Dinghong Resin Co. Ltd, Finjet chemical industries, Foreverest Resources Ltd, Arakawa Chemical Industries Ltd, DRT 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 서론

조사 가정

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

바이오 기반 접착제와 실란트에 대한 수요 증가

종이 포장 업계의 급성장

기타 촉진요인

성장 억제요인

톨유 로진 기반 페놀 수지로의 관심 이동

기타 저해요인

업계의 밸류체인 분석

Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협

경쟁 정도

제5장 시장 세분화(금액 기준 시장 규모)

용도

종이 사이즈

인쇄 잉크

접착제와 실란트

고무

페인트

기타 용도

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카공화국

기타 중동 및 아프리카

제6장 경쟁 상황

M&A, 합작투자, 제휴, 협정

시장 점유율(%)**/순위 분석

주요 기업의 전략

기업 개요

Arakawa Chemical Industries Ltd

DRT(Derives Resiniques et Terpeniques)

Finjetchemical Co. Ltd

Forestar Chemical Co. Ltd

Foreverest Resources Ltd

Guangxi Dinghong Resin Co. Ltd

Guangxi Tone Resin Chemical Co. Ltd

Harima Chemicals Group Inc.

Kemipex

KH Chemicals

Novotrade Invest AS

PT INDOPICRI(Indonesia Pine Chemical Industri)

Silver Fern Chemical Inc.

United Resins

Wuzhou Sun Shine Forestry and Chemicals Co. Ltd

제7장 시장 기회와 향후 동향

경기장 바닥용 미끄럼 방지제 수요 확대

제약 업계의 새로운 용도

ksm

영문 목차

영문목차

The Gum Rosin Market size is estimated at 655.45 kilotons in 2024, and is expected to reach 800.53 kilotons by 2029, growing at a CAGR of 4.08% during the forecast period (2024-2029).

Key Highlights

The gum rosin market was negatively impacted by the COVID-19 pandemic. However, the market recovered significantly after the pandemic, owing to rising applications in adhesives, sealants, printing inks, and others.

The growing demand for bio-based adhesives and sealants and the burgeoning paper packaging industry are likely to be the main drivers of the gum rosin market's growth over the medium term.

On the flip side, the shift of interest toward tall oil rosin-based phenolic resins is expected to limit the growth of the gum rosin market.

Nevertheless, growth in demand for anti-slip agents for floors in stadiums and emerging applications in the pharmaceutical industry are likely to create lucrative growth opportunities for the global market soon.

The Asia-Pacific region is expected to account for the largest share of the market over the forecast period, owing to the huge consumption from countries such as China, India, and Japan.

Gum Rosin Market Trends

The Adhesives and Sealants Segment is Expected to Dominate the Market

For decades, gum rosin has become one of the vital components of the adhesives and sealants industry value chain, as it serves as an excellent tackifier for adhesives.

Gum rosin is widely used as an ingredient for heat-melt adhesives, pressure-sensitive adhesives, and rubber adhesives. This rosin is mainly used to enhance the strength, plasticity, and viscosity of adhesives.

Adhesives are essential components of shoes, automobiles, cartons, furniture, non-woven fabrics, and a host of other products. Adhesives and sealants have applications in numerous industries, including construction, pharmaceutical, packaging, and others.

According to Oxford Economics, the global construction industry is expected to reach USD 13.3 trillion by 2025 - adding USD 2.6 trillion to output in five years from 2020. China, India, the United States, and Indonesia are expected to record significant growth in the construction industry in the coming years. China alone will account for 26.1% of global growth. India is expected to account for 14.1% and the United States for 11.1%, while Indonesia is expected to account for 7.0% of global growth.

According to the United States Census Bureau, the value of commercial construction in the year 2022 in the country was USD 114.79 billion, registering a growth rate of 21.4% compared to the previous year.

The gum rosin industry seeks to identify collaboration opportunities and build partnerships with the adhesives and sealants industry, as food and packaging safety is of concern to adhesives and sealants manufacturers worldwide.

China is the world's largest packaging consumer across the world owing to the factors such as growing per capita income, coupled with rising e-commerce giants in the country. India's packaging industry is the fifth-largest in the world, and it is growing at about 22-25% per year, as per the Plastics Industry Association of India. Costs of packaging and processing food can be 40% lower than in Europe because of highly skilled labor and cheap labor costs.

According to the Packaging Industry Association of India (PIAI), the Indian packaging industry is expected to grow at a rate of 22% during the forecast period. Moreover, the Indian packaging market is expected to reach USD 204.81 billion by 2025, registering a CAGR of 26.7% between 2020 and 2025.

With increasing concerns related to environmental pollution and the ability to tailor gum rosin resin according to the desired properties of adhesives, the applications of bio-based adhesives and sealants are likely to increase the market demand for gum rosin in the coming years.

Asia-Pacific Region to Dominate the Market

Asia-Pacific is expected to dominate the gum rosin market during the forecast period due to the fast-growing automotive sector and the rise in construction activities in China and India.

In 2022, according to the World Paint & Coatings Industry Association, the Asia-Pacific paints and coatings industry was estimated to be worth USD 63 billion. China dominated the region's market, which is growing at a CAGR of 5.8%. In 2022, the Chinese market is expected to have grown by 5.7%. According to current trends, China's total sales of paints and coatings exceeded USD 45 billion in 2022. In East Asia, the country had the largest market share of 78%.

India is the fourth-largest consumer of rubber in the world as of 2022. Rubber usage per capita in India is currently 1.2 kilograms, compared to 3.2 kilograms globally. The rubber industry in India generates revenue of approximately INR 12,000 crores (~USD 1.4 billion).

In automobile industries, gum rosin is used in the manufacturing of coatings and paints as they can easily dissolve in organic solvents, including gasoline, turpentine, alcohol, and others. According to the China Association of Automobile Manufacturers (CAAM), China has the largest automotive production base in the world, with a total vehicle production of 27 million units in 2022, registering an increase of 3.4 % compared to 26 million units produced last year. Further, in the first 7 months of 2022, the country has produced 14.57 million units of cars, registering a growth rate of 31.5% Year on Year.

In the construction industry, gum rosin is mainly used as a concrete frothing agent and floor-tiling adhesive. The Indian government has been actively boosting housing construction, as it aims to provide houses to about 1.3 billion people. The country is likely to witness around USD 1.3 trillion of investment in housing over the next seven years, to witness the construction of 60 million new houses in the country. The availability of affordable housing in the country is expected to increase by around 70% by 2024.

The aforementioned factors are likely to increase the demand for gum rosin during the forecast period.

Gum Rosin Industry Overview

The global gum rosin market is highly fragmented in nature. The major players include Guangxi Dinghong Resin Co. Ltd, Finjet chemical industries, Foreverest Resources Ltd, Arakawa Chemical Industries Ltd, and DRT, among others (not in any particular order).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Demand for Bio-based Adhesives and Sealants

4.1.2 Burgeoning Paper Packaging Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Shift of Interest toward Tall Oil Rosin-based Phenolic Resins

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Application

5.1.1 Paper Sizing

5.1.2 Printing Ink

5.1.3 Adhesives and Sealants

5.1.4 Rubber

5.1.5 Paints and Coatings

5.1.6 Other Applications

5.2 Geography

5.2.1 Asia-Pacific

5.2.1.1 China

5.2.1.2 India

5.2.1.3 Japan

5.2.1.4 South Korea

5.2.1.5 Rest of Asia-Pacific

5.2.2 North America

5.2.2.1 United States

5.2.2.2 Canada

5.2.2.3 Mexico

5.2.3 Europe

5.2.3.1 Germany

5.2.3.2 United Kingdom

5.2.3.3 Italy

5.2.3.4 France

5.2.3.5 Rest of Europe

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Rest of South America

5.2.5 Middle-East and Africa

5.2.5.1 Saudi Arabia

5.2.5.2 South Africa

5.2.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Arakawa Chemical Industries Ltd

6.4.2 DRT (Derives Resiniques et Terpeniques)

6.4.3 Finjetchemical Co. Ltd

6.4.4 Forestar Chemical Co. Ltd

6.4.5 Foreverest Resources Ltd

6.4.6 Guangxi Dinghong Resin Co. Ltd

6.4.7 Guangxi Tone Resin Chemical Co. Ltd

6.4.8 Harima Chemicals Group Inc.

6.4.9 Kemipex

6.4.10 KH Chemicals

6.4.11 Novotrade Invest AS

6.4.12 PT INDOPICRI ( Indonesia Pine Chemical Industri )

6.4.13 Silver Fern Chemical Inc.

6.4.14 United Resins

6.4.15 Wuzhou Sun Shine Forestry and Chemicals Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Growth in Demand for Anti-slip Agents for Floors in Stadiums

7.2 Emerging Applications in the Pharmaceutical Industry