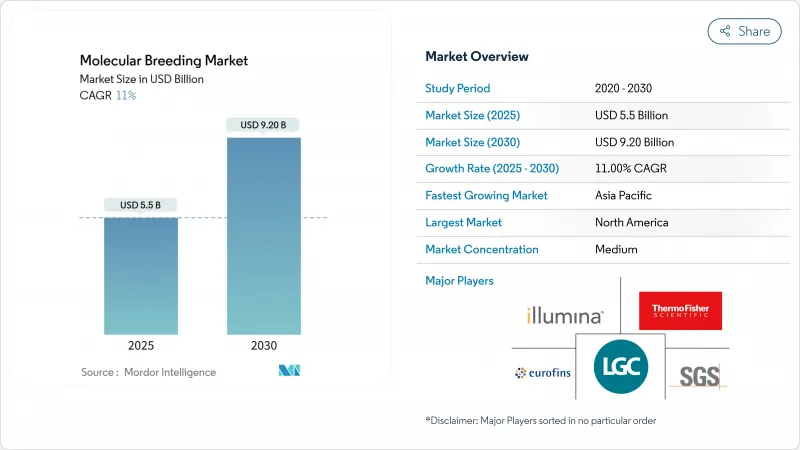

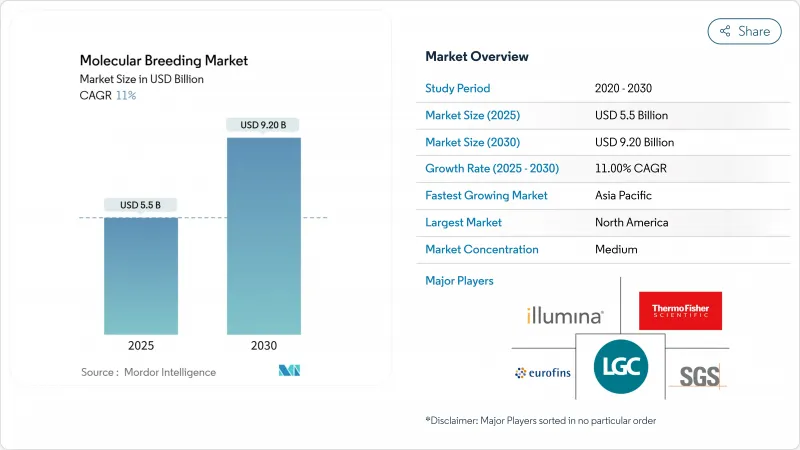

분자 육종 시장은 2025년에 55억 달러로 평가되었고, 2030년에 92억 달러에 이를 것으로 예상되며 CAGR은 11.0%를 나타낼 전망입니다.

인공 지능과 게놈 선택의 통합으로 육종 주기가 수년에서 수개월로 단축되어 제품 개발 효율성이 향상되었습니다. 미국 ‘적응형 작물 및 토양 비전(Vision for Adapted Crops and Soils)'과 인도 '국가 식량 안보 실행 계획(National Action Plan on Food Security)’ 등 정부 주도 정책이 기후 변화에 강한 작물 품종 수요를 촉진하고 있습니다. 고효율 표현형 분석, 시퀀싱 비용 감소, 접근성 높은 유전자형 분석 서비스가 시장 확장을 뒷받침합니다. 북미는 연구 인프라 우위를 유지하는 반면, 아시아태평양 지역은 규제 개혁과 식량 안보 요구로 상당한 성장 잠재력을 보입니다.

시장 내 민간 및 공공 지출이 급속히 증가하고 있습니다. 써모 피셔는 차세대 시퀀싱 및 시약 혁신을 위해 2023년 연구개발에 13억 달러를 투자하여 중견 육종업체의 진입 비용을 낮췄습니다. 미국 농무부의 데이터 표준화 프로그램은 유전체 데이터셋을 통합하여 중복 시험을 방지하고 시장 출시 기간을 단축하고 있습니다. 이러한 자본 투자는 소규모 기업의 규제 준수 장벽을 낮추어 신형 특성 개발자들이 규제 요건을 효과적으로 대응할 수 있게 합니다. 또한 CGIAR의 4억 달러 규모 영양 중심 포트폴리오와 같은 다자간 이니셔티브는 기부자 자금을 유치하고 생물강화 성과를 가속화하고 있습니다.

인도가 기록적 고온을 견딜 수 있는 100일형 밀 품종을 출시하면서 내열성·내가뭄성 유전자형이 시범 단계에서 상업화 단계로 진전되었습니다. 일본 연구 센터들은 기후 취약국에서 생산 수준을 유지하기 위해 염분 및 수분 스트레스 조건에 적응한 퀴노아와 대두 품종을 개발 중입니다. 식물 육종의 우선순위는 이제 수확량 최적화를 넘어 다중 스트레스 내성을 포함하며, 생산성과 환경 회복력을 통합하는 다중 분자 마커의 사용이 필수적입니다. 극한 기상 현상으로 인해 현재 매 시즌 수십억 달러 상당의 작물 손실이 발생하고 있어 기후 회복력 종자 포트폴리오의 투자 수익률이 증가함에 따라 재정적 영향은 상당합니다.

신규 형질당 준수 비용은 1,500만 달러에 달할 수 있으며, 이는 총 개발 예산의 약 절반을 소모하여 중소 혁신 기업들의 진입을 저해합니다. 유럽연합(EU)의 유전자 변형 작물(GMO) 법규에 따른 유전자 편집 작물 규제는 기업들로 하여금 미국 및 브라질과 같이 유리한 규제를 가진 시장에 집중하도록 유도합니다. 아르헨티나, 우루과이, 태국이 2024년 승인 절차를 간소화하기 위해 규정을 개정했음에도 불구하고, 규제 불확실성은 여전히 일정을 연장하고 자금 조달 비용을 증가시키고 있습니다.

2024년 분자 육종 시장의 63%를 식물 응용 분야가 차지했으며, 이는 주로 옥수수, 밀, 대두 육종 프로그램에서의 게놈 선택 도입에 기인합니다. 가축 부문은 유우우에서 전통적 추정값 대비 우수한 성능을 입증하는 게놈 육종 가치와 CRISPR 기반 질병 저항성 돼지 개발에 힘입어 13.1%의 연평균 성장률(CAGR)로 성장하고 있습니다. 앵거스 스티어셀렉트(Angus SteerSELECT)와 같은 도구는 중요한 도체 특성 예측 정확도 0.72 이상을 입증하여 사육장 수익성을 높이고 투자를 유치하고 있습니다.

가금류 부문은 번식력과 성장 유전자의 정밀 편집을 도입하여 세대 간격을 단축하고 있습니다. 또한 돼지 육종에서 통합된 대사체학 및 유전체 모델은 현재까지는 소폭의 성과에 그치고 있으나 일평균 증체량 개선 가능성을 보여주고 있습니다. 이러한 발전은 가축 부문이 2030년까지 분자 육종 시장에 대한 기여도를 크게 높일 수 있음을 시사합니다.

단일 염기 다형성(SNP)은 2024년 분자 육종 시장 규모의 42%를 차지했으며, 고처리량 플랫폼과의 호환성과 전장 유전체 연관성 분석 결과의 향상으로 인해 13.2%의 연평균 복합 성장률(CAGR)을 유지하고 있습니다. 단위 비용 감소로 단순 반복 서열(SSR)이 보유하던 가격 경쟁력이 약화되면서 개발도상국 프로그램들이 직접 SNP 솔루션을 채택하게 되었습니다. RNA-seq 및 ATAC-seq 데이터로부터 기능적 변이 패널을 구현함으로써 유제품 단백질 형질의 육종 정확도가 3% 포인트 향상되어 해당 기술의 신뢰성을 입증하였습니다.

SNP 워크플로의 표준화로 인해 익스프레스 시퀀스 태그(EST) 및 기타 전통적 마커는 주로 발현 프로파일링과 같은 특수한 응용 분야에 위치하게 되었습니다. SNP의 채택 증가로 데이터 상호운용성이 향상되었으며, 이는 AI 기반 육종 시스템 개발의 기초가 됩니다.

북미는 선진 연구 인프라와 효율적인 규제 체계에 힘입어 2024년 분자 육종 시장 점유율의 36%를 차지합니다. 일루미나(Illumina)는 2024년 43억 3,000만 달러의 매출을 기록했으며, LGC 바이오서치 테크놀로지스(LGC Biosearch Technologies)와 협력하여 밭작물 및 가축 부문의 표적 유전체형 분석(genotyping-by-sequencing) 역량을 강화하고 있습니다. 미국 농무부(USDA)의 SECURE 규정은 유전자 편집 제품 승인 절차를 간소화하여 해당 지역의 시장 주도권을 유지하고 있습니다.

아시아태평양 지역은 2030년까지 연평균 12.1%의 성장률을 기록할 것으로 예상되며 가장 높은 성장 잠재력을 보여줍니다. 중국은 2024년 질병 저항성 유전자 편집 밀을 승인했으며, 인도의 규제 업데이트는 특정 게놈 편집에 대한 승인을 간소화하여 민간 육종 사업을 가속화하고 있습니다. 일본의 단계적 규제 체계와 작물 스트레스 연구 집중은 해당 지역 핵심 허브로서의 입지를 공고히 합니다. 정부 자금과 민간 벤처 캐피털의 결합은 식량 안보 수요 대응을 위한 지역 육종 인프라를 강화하고 있습니다.

유럽은 규제 제약에도 불구하고 상당한 시장 점유율을 유지합니다. 2024년 말 EU 환경위원회의 신규 유전체 기술 법안 승인은 위험 기반 평가로의 전환을 시사합니다. 영국은 정밀 육종법을 시행하여 유전자 편집 작물 시험을 신속히 진행하기 위한 2단계 안전성 검토 체계를 구축했습니다. 스위스도 유사한 규제 개편을 진행 중입니다. 시장 성장은 정책 발전에 달려 있으며, 유럽 그린딜 지속가능성 요건을 충족하는 품종에 대한 수요가 상당합니다.

The molecular breeding market attained USD 5.5 billion in 2025 and is projected to reach USD 9.2 billion by 2030, registering a CAGR of 11.0%.

The incorporation of artificial intelligence with genomic selection has reduced breeding cycles from years to months, enhancing product development efficiency. Government initiatives, including the U.S. Vision for Adapted Crops and Soils and India's National Action Plan on Food Security, are driving demand for climate-resilient crop varieties. Market expansion is facilitated by high-throughput phenotyping, decreased sequencing costs, and accessible genotyping services. While North America retains its advantage in research infrastructure, the Asia-Pacific region demonstrates substantial growth potential due to regulatory reforms and food security requirements.

Private and public spending in the market is increasing rapidly. Thermo Fisher invested USD 1.3 billion in research and development in 2023 to advance next-generation sequencing and reagent innovation, reducing entry costs for midsized breeders. The U.S. Department of Agriculture's data-standards programs are harmonizing genomic datasets, preventing redundant trials, and reducing time-to-market. These capital investments have decreased compliance barriers for smaller firms, enabling novel trait developers to navigate regulatory requirements. Additionally, multilateral initiatives, such as CGIAR's USD 400 million nutrition-focused portfolio, are attracting donor funds and accelerating biofortification outcomes.

India's release of 100-day wheat varieties capable of withstanding record temperatures has enabled heat- and drought-tolerant genotypes to advance from pilot to commercial scale. Japanese research centers are developing quinoa and soybean varieties adapted to saline and water-stress conditions to maintain production levels in climate-vulnerable countries. Plant breeding priorities now extend beyond yield optimization to include multistress tolerance, necessitating the use of multiplexed molecular markers that integrate productivity with environmental resilience. The financial implications are significant, as extreme weather events currently cause crop losses worth billions of USD per season, increasing the return on investment for climate-resilient seed portfolios.

The compliance cost per new trait can reach USD 15 million, consuming approximately half of the total development budgets and deterring smaller innovators. The European Union's regulation of gene-edited crops under GMO legislation drives companies to focus on markets with favorable regulations, such as the United States and Brazil. While Argentina, Uruguay, and Thailand updated their regulations in 2024 to simplify approvals, regulatory uncertainty continues to extend timelines and increase financing costs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plant applications accounted for 63% of the molecular breeding market in 2024, primarily through genomic selection implementation in maize, wheat, and soybean breeding programs. The livestock segment is experiencing growth at a 13.1% CAGR, driven by genomic breeding values that demonstrate superior performance compared to traditional estimates in dairy cattle and CRISPR-based disease-resistant pig development. Tools such as Angus SteerSELECT have demonstrated prediction accuracies exceeding 0.72 for critical carcass traits, enhancing feedlot profitability and attracting investment.

The poultry sector is implementing precision editing of fertility and growth genes to reduce generation intervals. Furthermore, integrated metabolomic and genomic models in swine breeding demonstrate potential for improving average daily gain, despite current modest outcomes. These developments indicate that the livestock segment may substantially increase its contribution to the molecular breeding market by 2030.

Single nucleotide polymorphisms (SNPs) accounted for 42% of the molecular breeding market size in 2024 and maintain a 13.2% CAGR due to their compatibility with high-throughput platforms and enhanced genome-wide association outputs. The reduction in unit costs has diminished the price advantage previously held by simple sequence repeats, prompting developing-country programs to adopt SNP solutions directly. The implementation of functional-variant panels from RNA-seq and ATAC-seq data has improved breeding accuracies by 3 percentage points in dairy-protein traits, demonstrating the technology's reliability.

The standardization of SNP workflows has positioned express sequence tags and other traditional markers primarily in specialized applications such as expression profiling. The increased adoption of SNPs enhances data interoperability, which is fundamental for developing AI-enabled breeding systems.

The Molecular Breeding Market Report is Segmented by Application (Plant, Livestock, and More), by Marker Type (Simple Sequence Repeats (SSR), and More), by Breeding Process (Marker-Assisted Selection (MAS), and More), by Trait Target (Yield Enhancement, and More), by End-User (Seed and Crop-Protection Companies, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America holds 36% of the molecular breeding market share in 2024, supported by advanced research infrastructure and efficient regulatory frameworks. Illumina reported USD 4.33 billion revenue in 2024 and has partnered with LGC Biosearch Technologies to increase targeted genotyping-by-sequencing capabilities for row-crop and livestock segments. The USDA's SECURE rule streamlines the approval process for gene-edited products, maintaining the region's market leadership.

Asia-Pacific demonstrates the highest growth potential with a projected 12.1% CAGR through 2030. China approved disease-resistant gene-edited wheat in 2024, while India's regulatory updates streamline approvals for specific genome edits, accelerating private breeding initiatives. Japan's tiered regulatory system and focus on crop-stress research establishes it as a key regional hub. The combination of government funding and private venture capital is strengthening the region's breeding infrastructure to address food security needs.

Europe maintains significant market presence despite regulatory constraints. The EU Environment Committee's approval of new genomic technology legislation in late 2024 indicates movement toward risk-based assessment. The UK implemented the Precision Breeding Act, establishing a two-tier safety review system to expedite gene-edited crop trials. Switzerland is implementing similar regulatory changes. Market growth depends on policy developments, with substantial demand for varieties meeting European Green Deal sustainability requirements.