ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

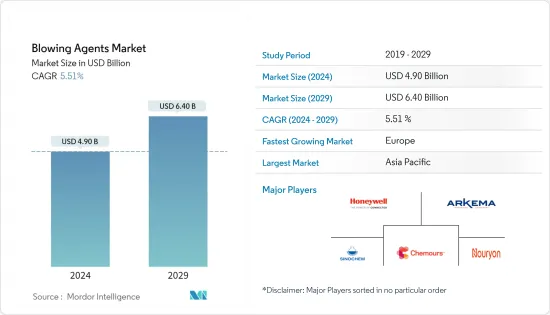

발포제 시장 규모는 2024년 49억 달러로 추정되고, 2029년까지 64억 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 복합 연간 성장률(CAGR) 5.51%로 성장할 전망입니다.

조사 대상 시장을 견인하는 주요 요인은 건물, 자동차 및 가전제품을 위한 고분자 단열 폼 수요 증가입니다. 발포제에 대한 엄격한 환경 규제는 조사 대상 시장의 성장을 방해할 것으로 예상됩니다.

주요 하이라이트

오존층 파괴계수(ODP)가 0이고 지구온난화계수(GWP)가 낮은 발포제에 대한 높은 수요는 향후 기회가 될 수 있습니다.

수익 측면에서 북미는 예측 기간 동안 조사된 시장을 독점했습니다. 양면에서 아시아태평양은 세계 시장을 독점했습니다.

발포제 시장 동향

건축 및 건설 업계 수요 증가

발포제는 VOC를 포함하지 않고 오존층을 파괴하지 않고 지구 온난화 계수가 낮고 에너지 소비가 적기 때문에 환경적으로 허용되고 건축 및 건설에 사용됩니다. 보다 균일한 컴포넌트를 생성하는 데 도움이 되므로, 보다 뛰어난, 보다 긴밀한 단열, 보다 높은 에너지 효율 및 제한된 에너지 소비가 실현됩니다.

발포제는 블록 파이프나 지붕의 단열재, 문, 외장재 등의 건물의 단열재나, 기초를 필요로 하는 구조물의 성분으로서 사용됩니다. 창문이나 문 실링재로도 사용됩니다.

이들은 주로 폴리우레탄 폼에 사용되며, 열 손실을 방지하고, 추운 곳에서도 온도를 유지하며, 장거리 가열 시 동결과 균열을 방지하기 위해 파이프에서 자주 사용됩니다.

이들은 페놀 형태에도 사용되지만 사용은 제한적입니다. 페놀 폼은 주로 지붕, 벽 공동 및 바닥 단열재의 단열 장벽 역할을 하는 패널에 사용됩니다. 전 세계적으로 건설 활동이 증가하고 있기 때문에 발포제 시장이 크게 확대될 것으로 예상됩니다.

아시아태평양은 건축 및 건설 부문을 지배하고 있으며 인도, 중국 및 기타 동남아시아 국가들이 시장 성장을 크게 견인하고 있습니다.

앞서 언급한 긍정적인 요인은 예측 기간 동안 시장 성장을 가속할 것으로 예상됩니다.

중국이 아시아태평양 시장을 독점으로

그룹 I의 멤버인 중국은 2024년까지 HFC의 생산과 사용을 합의된 기준 수준에서 동결할 것으로 예상되고 있으며, 2029년까지 동결 수준보다 10% 낮은 단계에서 단계적으로 생산 사용을 단계적으로 줄일 예정입니다.

CFC-11의 사용은 오존층 파괴의 영향으로 2010년에 국제적으로 금지되었지만, 경질 폴리우레탄 폼 단열 분야에서 발포제로서 CFC-11의 불법 제조 및 사용을 증명하는 증거가 발견되었습니다 있습니다. 영국에 본사를 둔 NGO인 환경조사국이 실시한 현지조사에 따르면 중국의 대기 중 CFC-11 농도는 예상을 크게 웃돌고 CFC-11의 유해성이 증명되고 있습니다.

금지된 CFC 및 HCFC(사용은 규제되며 2040년까지 단계적으로 폐지될 예정)과는 별도로 중국은 프리블렌드 CP(시클로펜탄), HFO 블렌드, 물 등의 대체 발포제 를 사용하고 있습니다.

중국에는 세계 최대의 건설 산업이 있습니다. 그러나 중국 정부가 서비스 주도형 경제로의 전환을 목표로 하고 있기 때문에 이 업계의 성장률은 점점 완만해지고 있습니다.

중국은 세계에서 2위의 포장산업을 갖고 있으며, 맞춤형 포장의 대두, 전자레인지용 식품, 스낵식품, 냉동식품 등 수요 증가로 예측기간 동안 일관된 성장이 예상된다 있습니다.

중국에는 세계 최대의 섬유 및 의류 산업이 있으며, 이 나라 경제의 중요한 선수이기도 합니다. 그러나 미국과의 무역전쟁과 시장의 성숙으로 인해 미국의 의류 수출시장에서 이 나라의 점유율이 떨어지고 있습니다.

따라서 앞서 언급한 요인은 예측 기간 동안 중국의 발포제 수요에 영향을 줄 수 있습니다.

발포제 산업 개요

세계 발포제 시장은 세분화되어 있습니다. 시장에는 국제적인 선수뿐만 아니라 현지 선수도 많이 있습니다. 주요 기업으로는 Honeywell International Inc., The Chemours Company, Arkema, Sinochem Group, Nouryon 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

건축물, 자동차, 가전제품용 폴리머 단열 폼 수요 증가

폴리우레탄 폼 제조에 있어서의 발포제 수요 증가

억제요인

발포제에 관한 엄격한 환경 규제

COVID-19의 영향

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

규제와 정책

제5장 시장 세분화

제품 유형

하이드로클로로플루오로카본(HCFC)

하이드로플루오로카본(HFC)

탄화수소(HC)

하이드로플루오로올레핀(HFO)

기타 제품 유형

폼 유형

폴리우레탄 폼

폴리스티렌 폼

페놀 폼

폴리프로필렌 폼

폴리에틸렌 폼

기타 폼

용도

건축 및 건설

자동차

침구?가구

가전제품

포장

기타 용도

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

기타 북미

유럽

독일

영국

프랑스

이탈리아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

합병, 인수, 합작사업, 제휴, 협정

시장 점유율(%)**/랭킹 분석

주요 기업의 전략

기업 프로파일

A-Gas

Americhem

Arkema

Form Supplies Inc.(FSI)

Harp International Ltd

HCS Group GmbH

Honeywell International Inc.

Huntsman International LLC

Lanxess

Nouryon

Sinochem Group Co. Ltd

Solvay

The Chemours Company

The Linde Group

Zeon Corporation

제7장 시장 기회와 앞으로의 동향

오존층 파괴계수(ODP) 제로로 지구온난화계수(GWP)가 낮은 발포제에 대한 높은 수요

발포 포장용 폴리스티렌 압출 시트의 높은 소비량

BJH

영문 목차

영문목차

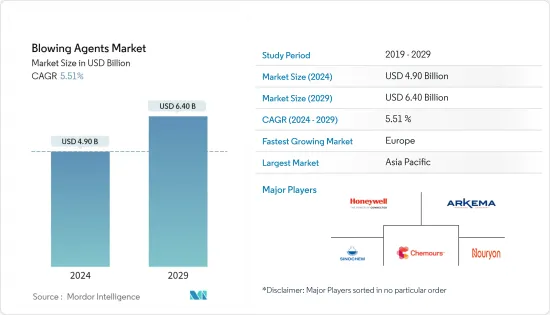

The Blowing Agents Market size is estimated at USD 4.90 billion in 2024, and is expected to reach USD 6.40 billion by 2029, growing at a CAGR of 5.51% during the forecast period (2024-2029).

Major factors driving the market studied is rise in demand for polymeric insulation foams for buildings, automotive, and appliances. stringent environmental regulations regarding blowing agents is expected to hinder the growth of the market studied.

Key Highlights

High Demand for Zero Ozone Depletion Potential (ODP) and Low Global Warming Potential (GWP) Blowing Agents is likely to act as an opportunity in the future.

In terms of revenue, North America dominated the market studied during the forecast period. In terms of volume, Asia-Pacific dominated the global market.

Blowing Agents Market Trends

Increasing Demand from the Building and Construction Industry

Owing to their non-VOC, non-ozone depleting, low global warming potential, and reduced energy consumption, blowing agents are environmentally acceptable, and are thus, used in building and construction. They help to create better uniform components, resulting in better, tighter insulation, higher energy efficiency, and limited energy consumption.

Blowing agents are used as a component in building insulation, such as block pipe and roof insulation, doors, sheathing, and in structures that require foundation. They are also used as sealants for windows and doors.

They are majorly used in polyurethane foams that have high utilization in pipes to prevent loss of heat and to maintain temperatures even during cold climates, to avoid freezing or cracking for long-distance heating.

They are also used in phenolic foams, but with limited usage. Phenolic foams are majorly used in panels to act as insulating barriers in roofing, wall cavities, and floor insulation. The increasing construction activities worldwide is expected to significantly boost the blowing agents market.

The Asia-Pacific region dominates the building and construction sector, with India, China, and various other South East Asian countries driving the market growth significantly.

The positive factors like the aforementioned ones are expected to drive the market growth through the forecast period.

China to Dominate the Asia-Pacific Market

As a Group I member, China is expected to freeze HFC production and use at agreed baseline levels, by or before 2024, and is expected to phase down the production and use, beginning with a 10% phasedown below freeze levels, by 2029.

Though the usage of CFC-11 was banned internationally in 2010, owing to the ozone depletion effects of the substance, evidence has been found proving the illegal production and usage of CFC-11 as a blowing agent in the rigid polyurethane foam insulation sector. According to a field study carried out by the Environmental Investigative Agency, a UK-based NGO, the atmospheric levels of CFC-11 in China are significantly greater than expected, proving the harmful nature of CFC-11.

Apart from the banned CFCs and HCFCs (whose usage is regulated and is expected to phase out by 2040), China has been using alternative blowing agents, like preblended CP (cyclopentane), HFO blends, and water.

China has the world's largest construction industry. However, the growth rate of the industry has become increasingly modest, as the Chinese government is looking to shift toward a services-led economy.

China has the second-largest packaging industry in the world and is expected to witness a consistent growth during the forecast period, owing to the rise of customized packaging, increased demand for microwave food, snack foods, and frozen foods, among others.

China has the world's largest textile and apparel industry, which is also a key player for the country's economy. However, there has been a drop in the market share occupied by the country in the global apparel export market, owing to the trade war with the United States and maturation of the market.

Hence, the aforementioned factors are likely to affect the demand for blowing agents in China during the forecast period.

Blowing Agents Industry Overview

The global market for blowing agents is fragmented. There are many local players in the market along with international players. The major companies include Honeywell International Inc., The Chemours Company, Arkema, Sinochem Group Co. Ltd, and Nouryon, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Rise in Demand for Polymeric Insulation Foams for Buildings, Automotive, and Appliances

4.1.2 Increasing Demand for Foam Blowing Agents in the Manufacturing of Polyurethane Foams