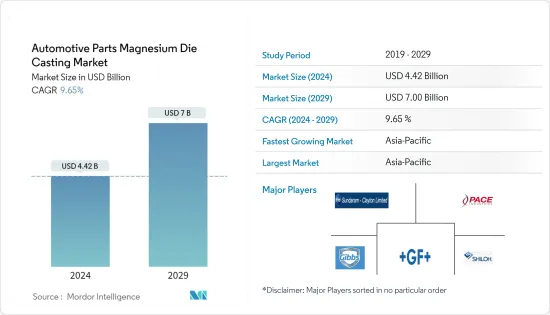

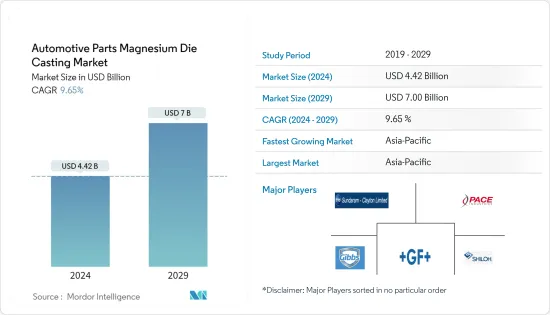

자동차 부품용 마그네슘 다이캐스트(Automotive Parts Magnesium Die Casting) 시장 규모는 2024년에는 44억 2,000만 달러로 추정되며, 2029년에는 70억 달러에 이를 것으로 예측 되며, 예측 기간 중(2024-2029년) CAGR은 9.65%로 추이하며 성장할 것으로 예상됩니다.

2020년에는 COVID-19 팬데믹으로 인해 자동차 판매와 생산이 감소하면서 자동차 시장이 어려움을 겪었습니다. 2020년 전 세계 차량 판매량은 2019년 차량 판매량에 비해 16% 감소했습니다. 모든 주요 차량 생산 국가에서 11%에서 거의 40%까지 큰 폭으로 감소했습니다. 유럽은 전 세계 생산량의 약 22%를 차지했습니다. 그러나 팬데믹 이후 자동차 산업은 2020년 한 해 동안 상당한 성장세를 보였습니다. 전반적인 차량 판매 증가와 예상되는 전기차 판매 증가가 예측 기간 동안 주로 시장을 견인할 것으로 예상됩니다.

경량 차량은 자동차의 연비 향상과 핵심 부품을 제조하는 경량 자동차 소재의 채택으로 인해 자동차 제조업체들 사이에서 인기를 얻고 있습니다. 또한 차량의 경량화는 품질과 성능에 앞서 안전성을 손상시키지 않으면서 이루어져야 합니다.

전 세계적으로 엄격한 배기가스 배출 규범이 제정됨에 따라 자동차 경량화 시장은 크게 성장할 것으로 보입니다. 차량 경량화에 대한 소비자 트렌드가 증가함에 따라 마그네슘 및 탄소섬유 강화 플라스틱과 같은 경량 부품의 보급이 증가하여 차량 부품을 제조할 가능성이 높으며, 이는 결국 시장을 활성화할 것으로 예상됩니다.

주요 제조 산업은 새로운 마그네슘 합금 및 효율적인 제조 기술에 대한 R&D 활동에 투자하고 있습니다. 예를 들어 인도공과대학인 마드라스, 미국 육군연구소, 노스텍사스대학은 자동차 산업에서 알루미늄 합금과 강철 합금을 대체하여 자동차 연비를 향상시킬 수 있는 새로운 마그네슘 합금을 개발했습니다.

제조 공정 자동화에 대한 투자가 증가함에 따라 시장이 크게 성장할 것으로 보입니다. 마그네슘 다이캐스팅 제조 공정의 높은 비용은 자동차 부품용 마그네슘 다이캐스팅 시장을 방해 할 가능성이 높습니다.

전기 자동차에 대한 수요 증가와 소비자 선호도의 변화로 인해 자동차 제조업체는 무거운 부품을 마그네슘과 같은 합금으로 제조된 경량 부품으로 대체하고 있습니다.

주요 자동차 제조업체는 미러 하우징, 스티어링 칼럼, 운전석 에어백 케이스, 시트 프레임, 대시보드 케이스 등에 마그네슘 합금을 사용하고 있습니다. 배터리 및 연비 향상에 대한 요구와 함께 성능 향상에 대한 수요가 증가함에 따라 고압 다이캐스트 마그네슘 합금에 대한 관심이 높아지고 있습니다. 이 합금은 기계적 특성이 뛰어나고 구조용 금속 중 무게 대비 강도가 가장 높습니다.

또한 EV를 제조하는 기업도 적극적으로 고압 다이캐스트 머신을 조달하고 소비자 수요 증가에 대응하기 위해 이 기술을 채택하고 있습니다.

이 지역에서 자동차용 압력 다이캐스트 부품을 제공하는 주요 기업으로는 OEFORM Limited, CNM Tech, Dalian Yaming Automotive Parts, LC Rapid 등이 있습니다. 포트폴리오의 업그레이드에 주력하는 기업이 있는 한편, 제조 공장의 확대나 제휴 등에 주력해, 시장의 주요 기업으로서의 지위를 확립하고 있는 기업도 있습니다.

아시아 태평양 지역은 자동차 부품용 마그네슘 다이캐스팅 시장에 대한 기회를 창출 할 가능성이있는 제조 산업의 주요 존재입니다. 이 지역 전역의 중소 제조 산업의 급속한 확장은 시장의 주요 성장을 목격 할 가능성이 높습니다. 이 지역의 차량 생산 증가는 마그네슘 다이캐스팅 부품에 대한 수요를 증가시켜 시장의 주요 성장을 목격 할 가능성이 높습니다.

엄격한 배기 가스 배출 규범의 제정으로 인해 지역 전체에서 전기 자동차에 대한 수요가 증가함에 따라 차량 제조업체는 차량에 경량 부품을 통합하도록 촉구하고 있습니다. 중국은 다이캐스팅 부품의 주요 생산국 중 하나이며 지역(아시아 태평양) 다이캐스팅 시장 점유율의 60% 이상을 차지하고 있습니다. 중국의 금속 주조 산업에는 26,000개 이상의 시설이 있으며, 이 중 8,000개 시설이 비철 주물을 생산합니다. 중국에서는 4,930만 톤 이상의 주물을 생산합니다. 첨단적이고 효율적인 자동 다이캐스팅 기계는 중국의 금속 다이캐스팅 수요를 뒷받침합니다. 중국 마그네슘 다이캐스팅 시장은 국제적으로 빠르게 성장하고 있는 자동차 산업에서 높은 수요를 경험하고 있습니다. 이는 예측 기간 동안 중국 시장의 성장을 견인할 것으로 예상됩니다.

인도 정부는 자동차 산업을 발전시키기 위해 '메이크 인 인디아'에 집중하고 있으며, 엄격한 배기가스 배출 규제로 인해 인도에서 자동차 부품용 마그네슘 다이캐스팅 시장이 성장하고 있습니다. 자동차 부문에서 소비되는 주물은 인도 전체 생산량의 35%를 차지합니다. 인도는 경기 침체, 연료 및 보험료 상승 등 여러 가지 이유로 인해 승용차 판매가 감소하는 추세를 보였습니다. 그러나 개정된 액셀 규범과 NBFC 위기 등 여러 압박에도 불구하고 전체 상용차 판매량은 증가하여 27.28%의 견고한 성장세를 보였습니다.

2016년 도입된 최신 규제 프레임워크인 차이나 6는 2020년 7월부터 1단계 차이나 6a가 시행되었고, 2단계는 2023년 7월부터 시행될 예정입니다. 규제 기준의 변화는 이 지역 자동차 시장의 역학 관계를 결정하는 데 결정적인 역할을 했습니다. 중국 환경보호부(MEP)는 신규 등록되는 모든 차량에 대해 배출가스 성능 기준을 강화하고 있습니다. 이는 예측 기간 동안 아시아 태평양 지역의 자동차 부품용 마그네슘 다이캐스팅 시장이 크게 성장할 것으로 예상됩니다.

세계의 자동차 부품용 마그네슘 다이캐스트 시장은 세계 신흥국과 선진국 지역의 중소규모 선수들에 의해 지배되고 있습니다. Georg Fischer Automotive, Ryobi Die Casting, Shiloh Industries, Pace Industries와 같은 대기업은 전 세계 시장의 30% 이상의 점유율을 차지합니다.

세계의 자동차 제조업체와 자동차 부품 제조 기업 간의 합병 및 인수 증가는 시장의 큰 성장을 보여줍니다. 주요 산업은 자동차의 연비 효율을 높이기 위해 경량 부품의 R&D 시설에 투자하고 있습니다. 예를 들어, 2022년 5월, GF, Schaffhausen의 부문인 GF Casting Solutions와 Bocar Group은 전 세계에서 전문적인 제품과 서비스를 제공하는 계약을 체결했습니다. 이 제휴는 북미, 유럽 및 아시아 고객을 지원하는 신기술 및 서비스 개발 및 투자에 도움이 되었습니다.

The Automotive Parts Magnesium Die Casting Market size is estimated at USD 4.42 billion in 2024, and is expected to reach USD 7 billion by 2029, growing at a CAGR of 9.65% during the forecast period (2024-2029).

The COVID-19 pandemic hampered the market in focus for the year 2020, primarily attributed to decline in vehicle sales and production. The global vehicle sale declined by 16% in 2020 as compared to the 2019 vehicle sales. All main vehicle-producing countries had major declines, ranging from 11% to almost 40%. Europe represented an almost 22% share of global production. However, post-pandemic the automotive industry witnessed significant growth for the year 2020. The overall increase in vehicle sales and expected increase in electric vehicle sales is anticipated to primarily drive the market during the forecast period.

Lightweight vehicles are gaining popularity among vehicle manufacturers owing to an enhanced fuel economy of automobiles with adoption of lightweight automotive materials manufacturing crucial parts. Additionally, the light-weighting of vehicles must be done without compromising on safety before quality and performance.

An enactment of stringent emission norms across the globe is liekly to witness significant growth for the market. Rising consumer trend towards light weight vehicle is likely to increase the penetration of light weight parts such as magnesium and carbon fiber reinforced plastic, to manufacture vehicle components, which in turn is anticipated to boost the market.

Major manufacturing industries are investing in research and development activities regarding new magnesium alloys and efficient manufacturing techniques. For instance, the Indian Institute of Technology, Madras, the US Army Research Laboratory, and the University of North Texas developed a new magnesium alloy that can replace aluminum and steel alloys in the automotive industry and increase the fuel efficiency of vehicles.

Growing investment in automation of manufacturing process is likely to witness major growth for the market. High cost of magnessium die casting manufacturing process is liekly to hamper the automotive parts magnesium die casting market.

Rise in demand for electric vehicles and a shift in consumer preferences have pushed vehicle manufacturer to replace heavier components with lightweight which are manufactured from alloys like Magnesium.

Major vehicle manufcturer use magnesium alloy for applications like mirror housings, steering columns, driver's airbag casings, seat frames, and dash encasings. Growing trend towards greater battery and fuel efficiency, along with demand for improved performance, has driven an increased interest in high-pressure die cast magnesium alloys. These alloys have an excellent combination of mechanical properties and the highest strength to weight ratio of any structural metal.

In addition, the companies manufacturing EV are also actively procuring pressure diecasting machines and are adopting this technology to make themselves ready for growing consumer demand.

Some of the key players offering automotive pressure die casting components in the region include OEFORM Limited, CNM Tech, Dalian Yaming Automotive Parts Co. Ltd, LC Rapid, and others. While some players focusing on upgrading their portfolio others focus on the manufacturing plants expansion, collaborations, etc. to pitch themselves as top players in the market. For instance,

Asia Pacific has major presence of manufacturing industries which is likely to create an opprtunity for automotive parts magnesium die casting market. Rapid expansion of small and medium manufacturing industries across the region is likely to witness major growth for the market. Rise in vehicle production across the region is likely to increase the demand for magnesium die casting parts which in turn is likely to witness major growth for the market.

Rise in demand for electric vehicle across the region owing to an enactment of stringent emission norms is prmpting vehicle manufacturer to integrate lightweight parts in vehicle. China is one of the major producers of die casting parts and accounts for more than 60% of the regional (Asia-Pacific) die casting market share. The metal casting industry in China has more than 26,000 facilities, out of which 8,000 facilities produce non-ferrous castings. The country produces over 49.3 million metric tons of castings. The advanced and efficient automatic die casting machines supported the demand for metal die castings in the country. The Chinese magnesium die casting market experiences high demand from the automotive industry, which is rapidly growing at the international level. This is expected to drive the Chinese market's growth over the forecast period.

The Government of India focus on Make in India, developing the automotive industry, and the stringent emission norms are driving the market for automotive parts magnesium die casting in the country. The castings consumed by the automotive sector accounted for 35% of the country's production. India witnessed a declining trend in passenger vehicle sales, owing to numerous reasons, such as economic slowdown, rise in fuel, and insurance costs. However, despite numerous pressures, such as revised axel norms and NBFC crisis, the overall commercial vehicle sales increased and showcased a robust 27.28% growth.

The latest regulatory framework, the China 6, which was introduced in 2016 and the first stage China 6a came into effect from July 2020 and the second stage is planned for July 2023. The change in the regulatory standards that have been crucial in determining the dynamics of the automotive market in the region. The Ministry of Environmental Protection (MEP), has been maintaining the record of emission performance standard for each new vehicle registered in. This is likely to witness major growth for the automotive part magnesium die casting market across the Asia-Pacific during the forecast period.

The global automotive parts magnesium die casting market isdomnaitng by regional small- and medium-scale players across both developing and developed countries around the world. Major recognized players, such as Georg Fischer Automotive, Ryobi Die Casting, Shiloh Industries, and Pace Industries, accounted for over 30% of the overall global market share.

Growing merger and acquisition between vehicle manufacturer and automotive parts manufacturing companies across the globe is witnessing major growth for the market. Major industries investing on research and development facilities on the light weight parts to enhance vehicle fuel efficiency. For instance,